欧州の監査サービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Auditing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1651038

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

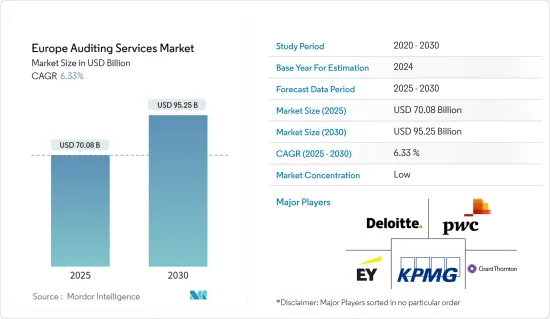

欧州の監査サービスの市場規模は2025年に700億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.33%で、2030年には952億5,000万米ドルに達すると予測されます。

監査は、正確で有用な財務諸表を保証することで、市場を円滑に運営するのに役立っています。法定監査が法的に義務付けられている企業もあり、その重要性がうかがえます。企業の世界化が進み、現在ではさまざまな大陸の資本市場に上場しています。EUは他国と協力し、投資家保護のため、監査人に対する十分な国際的監視を確保しています。

水平的措置は、被監査会社が公開会社であるか否かにかかわらず、すべての法定監査人および監査法人に共通であり、監査報告書を、財務諸表に対する単なる標準化された意見にとどまらず、被監査会社に関する関連情報を投資家に提供することにより、投資家にとってより有益なものとします。COVID-19がどの業種に及ぼす影響についても、割引はないです。このプロセスをより良く改善するために、政府は新たな規制を採用しました。

欧州の監査サービス市場の成長促進要因のひとつは、規制要件の増加と企業が国際会計基準に準拠する必要性の高まりです。また、データ分析や人工知能の利用など、技術的な進歩も市場を形成しており、監査の実施方法を変えつつあります。

欧州の監査サービス市場の動向

外部監査が市場を牽引

監査は資本市場の機能において重要な役割を果たしています。公開会社は規制により監査を受けなければならないため、監査サービスの需要は非弾力的であり、代替サービスは存在しないです。市場が拡大しているのは、財務記録の開示と記録に関する欧州の法律がますます厳しくなっているためです。さらに、財務監査や財務記録に対する企業の支出が増加しているため、新たな競合他社が監査サービスを選択するようになり、市場の拡大をさらに後押ししています。さらに、BFSI、IT・通信、ヘルスケアなど、さまざまな業界で監査サービスのニーズが高まっています。欧州の規制取引所に上場し、監査報酬を開示している公開会社の数は、過去10年間比較的安定しています。

欧州の外部監査は主に会計事務所によって行われており、「ビッグ4」(デロイト、PwC、EY、KPMG)が主要な監査法人です。これらの監査法人は欧州全域の監査のかなりの部分を担当しています。欧州監査裁判所はEUの外部監査人として、EU会計の信頼性と合法性を保証しています。さらに、IMFのような組織の外部監査委員会は、説明責任を果たすために外部監査プロセスを監督する上で極めて重要です。

英国市場を牽引する法定会計業務

法定会計業務は、英国の会計市場を牽引する重要な役割を担っています。この部門の特徴は、法律事務所や法律専門家独自のニーズに合わせた専門的な会計サービスです。

法律・会計活動部門は、裁判所やその他の司法機関において、弁護士資格を持つ個人による、一方の当事者の利益を他方に対して法的に代理する活動を包含しています。これには、民事訴訟、刑事訴訟、労働争議における助言や代理が含まれます。英国では、法律会計活動から発生する収益が当年度に大きく伸びた。

欧州の監査サービス産業の概要

欧州の監査サービス市場は断片化されており、多くのプレーヤーが存在します。監査法人は、新たなビジネスチャンスを獲得し、顧客基盤を拡大するため、欧州各国でのプレゼンス拡大に注力しています。各社はサービス提供の強化や市場競争力向上のため、提携や合併を進めています。主なプレーヤーは、デロイト、EY、KPMG、PwC、ATカーニー、グラント・ソントンLLPなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- ビジネスオペレーションの複雑化が市場の需要を促進

- 財務報告における技術利用の増加が市場の需要を促進

- 市場抑制要因

- 激しい競合と価格圧力

- 規制当局の監視と訴訟リスク

- 市場機会

- 監査法人によるサービス提供の拡大

- ビジネスの世界化の進展が監査サービスの需要拡大に影響

- 市場を形成する様々な規制動向に関する洞察

- 業界の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

- 業界の最新動向と技術革新に関する洞察

第5章 市場セグメンテーション

- タイプ別

- 内部監査

- 外部監査

- サービスライン別

- 業務監査

- 財務監査

- アドバイザリー及びコンサルティング

- 調査監査

- 情報システム監査

- コンプライアンス監査

- その他のサービス

- 国別

- 英国およびアイルランド

- ドイツ

- フランス

- イタリア

- オランダ

- スペイン

- その他欧州

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Deloitte

- EY

- KPMG

- PwC

- A.T. Kearney

- Grant Thornton LLP

- Bain & Company

- BDO USA

- Rodl and Partners

- Alvarez & Marsal*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

目次

The Europe Auditing Services Market size is estimated at USD 70.08 billion in 2025, and is expected to reach USD 95.25 billion by 2030, at a CAGR of 6.33% during the forecast period (2025-2030).

Auditing helps keep markets running smoothly by ensuring accurate and useful financial statements. Some companies are legally required to have a statutory audit, which shows its importance. Companies are becoming more global and are now listed on capital markets on different continents. The EU works with other countries to ensure adequate international oversight of auditors to protect investors.

Horizontal measures are the same for all statutory auditors and audit firms, regardless of whether or not the entity being audited is a public interest entity, making the audit report more informative for investors by providing them with relevant information about the audited company beyond a mere standardized opinion on the financial statements. There is no discount on COVID-19's effect on any industry. For better improvement of the process, the government has adopted new regulations.

One of the main drivers of growth in the European auditing services market is the increasing regulatory requirements and the need for companies to comply with international accounting standards. The market is also being shaped by technological advancements, such as the use of data analytics and artificial intelligence, which are changing the way audits are conducted.

Europe Auditing Services Market Trends

External Audit is Driving the Market

Audits play a vital role in the functioning of capital markets. The demand for audit services by public companies is also inelastic in that these companies must obtain an audit due to regulation, with no substitution for such services available. The market is expanding because of the increasingly stringent European laws governing the disclosure and recording of financial records. Additionally, rising corporate spending on financial auditing and recording pushes new competitors to choose auditing services, further driving market expansion. Additionally, there is a growing need for auditing services in several industries, including BFSI, IT and telecommunication, healthcare, and others. The number of public companies listed on regulated European exchanges that disclose audit fees has remained relatively consistent for the past 10 years.

External audits in Europe are primarily conducted by accounting firms, with the "Big Four" (Deloitte, PwC, EY, and KPMG) as major auditors. These firms handle a significant portion of audits across Europe. The European Court of Auditors serves as the external auditor for the EU, ensuring the reliability and legality of EU accounts. Additionally, the external audit committee of organizations like the IMF is crucial in overseeing external audit processes for accountability.

Legal Accounting Activities is Driving the Market in United Kingdom

Legal accounting activities play a significant role in driving the accounting market in the United Kingdom. This sector is characterized by specialized accounting services tailored to law firms and legal professionals' unique needs.

The legal and accounting activities sector encompasses legal representation of one party's interests against another, whether before courts or other judicial bodies, by individuals who are members of the bar. This includes advising and representation in civil cases, criminal actions, or labor disputes. In the United Kingdom, revenue generated from legal accounting activities experienced significant growth in the current year.

Europe Auditing Services Industry Overview

The European auditing services market is fragmented, with the presence of many players. Firms focus on expanding their presence in various European countries to tap into new business opportunities and broaden their client base. The companies are engaging in collaborations and mergers to enhance their service offerings and improve market competitiveness. The key players include Deloitte, EY, KPMG, PwC, AT Kearney, and Grant Thornton LLP.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Complexity of Business Operations Driving Demand for Market

- 4.2.2 Increasing Use of Technology in Financial Reporting Driving Demand for Market

- 4.3 Market Restraints

- 4.3.1 Intense Competition and Pricing Pressures

- 4.3.2 Regulatory Scrutiny and the Risk of litigation

- 4.4 Market Opportunities

- 4.4.1 Auditing Firms Expand their Service Offerings

- 4.4.2 Increasing Globalization of Business Impact the Growing Demand for Auditing Services

- 4.5 Insights on Various Regulatory Trends Shaping the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

- 4.8 Insights on Latest Trends and Technological Innovations in the Industry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Internal Audit

- 5.1.2 External Audit

- 5.2 By Service Line

- 5.2.1 Operational Audits

- 5.2.2 Financial Audits

- 5.2.3 Advisory and Consulting

- 5.2.4 Investigation Audits

- 5.2.5 Information System Audits

- 5.2.6 Compliance Audits

- 5.2.7 Other Service Lines

- 5.3 By Country

- 5.3.1 UK and Ireland

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Spain

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Deloitte

- 6.2.2 EY

- 6.2.3 KPMG

- 6.2.4 PwC

- 6.2.5 A.T. Kearney

- 6.2.6 Grant Thornton LLP

- 6.2.7 Bain & Company

- 6.2.8 BDO USA

- 6.2.9 Rodl and Partners

- 6.2.10 Alvarez & Marsal*

7 MARKET OPPORTUNTIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日