米国の監査サービス:市場シェア分析、産業動向、成長予測(2025年~2030年)

US Auditing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642093

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

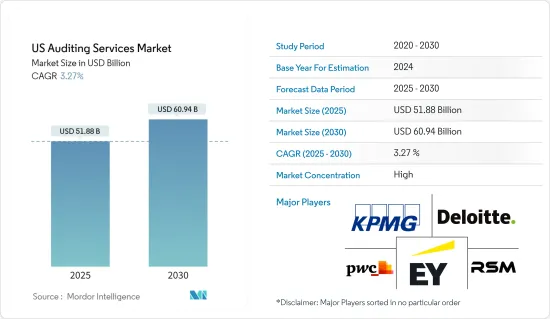

米国の監査サービスの市場規模は2025年に518億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.27%で、2030年には609億4,000万米ドルに達すると予測されます。

ここ数十年、監査法人がサービス提供の幅を広げ、既存の監査サービスを向上させるため、世界な会計事業体を戦略的に買収するため、市場の統合が顕著な動向となっています。この動向により、世界の監査法人の数は顕著に減少し、大手監査法人は一般にビッグ4と呼ばれる監査法人に統合されました。

米国では、この統合は特に顕著で、ビッグ4の会計事務所が合計で米国S&P500の時価総額全体の97%近くを監査しています。特定の業界への集中はさらに顕著で、1社または2社が特定のセクターを支配しています。例えば、米国通信サービス業界の大手監査法人は、S&P500の時価総額の92%近くを占めています。エネルギー、素材、情報技術などの業界にも同様のシナリオがあり、上位2社のサービス・プロバイダーがS&P500の時価総額の75%以上を支配しています。最近の市場促進要因や市場機会には、技術の進歩、規制の変更、専門的な監査サービスに対する需要の増加などが含まれ、米国の監査サービス市場の進化を後押ししています。

米国の監査市場の動向

ビッグ4による監査の質の低下

米国における監査サービス市場の高い集中度を考慮すると、投資家は監査の集中度が低下する可能性について問題を提起しており、その結果、投資家の保護も低下する可能性があります。いずれかの監査法人の監査が禁止されたり、停止されたりすれば、他の市場が対応できないような大きな空白が生じるため、市場に壊滅的な影響を与える可能性があります。同じことを考えると、これらの監査法人は、監査規制当局から自分たちの立場について合理的に保証されていることになります。監査人は急速に自己満足に陥っており、すでにコスト削減のために特定の監査手続を廃止し、よりリスクの高いクライアントを引き受け、経営陣の要求に同意し、信頼される監査法人というブランドの下で、よりリスクの高い非監査サービスラインを積極的に拡大しています。

その大きな要因は、Big4ファームとその子会社の仕組みにあると考えられます。これらの子会社は、同じ理念を共有する世界・ネットワークの子会社というよりも、法的に別個の事業関連会社として機能しています。規制当局が断固とした措置を取らない限り、監査の質はさらに低下することが予想されます。

ビッグ4は在任期間が長くなるにつれて監査報酬を引き上げる

大手4社が競争や規制の欠如を利用して収益を上げていることを示す重要な証拠のひとつが、在任期間の長い企業に対する監査報酬の増加です。慣例では、監査法人は長期に渡ってビジネスを提供してきた顧客には監査報酬を低く設定することになっているが、米国の4大監査法人はそうなっていないです。

ファームがこのような値上げを正当化する理由として挙げるのは、事業の成長に伴う仕事量の増加であり、企業構造の変化による監査への負担です。しかし、大手4社以外の監査法人は、監査報酬は横ばいで微減にとどまっています。Big4監査法人は14年平均で32%高い報酬を顧客に請求しているのに対し、非Big4監査法人は同期間で6%減少しています。手数料の増加は、監査分野におけるこれらの企業の力の直接的な結果です。他国での禁止リストを考慮すると、これらの企業がより厳しい規制に従うよう求められるのは時間の問題です。

米国の監査業界の概要

本レポートでは、米国の監査サービス市場の完全な背景分析(経済評価と経済セクターの貢献、市場概要、主要セグメントの市場規模推計、市場セグメントの新たな動向、市場力学と洞察、主要な健全性統計など)を掲載しています。Deloitte、KPMG、EY、PwC、RSM米国などの企業が本レポートで紹介されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術的進歩に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- タイプ別

- 内部監査

- 外部監査

- サービスライン別

- 業務監査

- 財務監査

- アドバイザリー及びコンサルティング

- 調査監査

- 情報システム監査

- コンプライアンス監査

- その他

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Deloitte

- EY

- KPMG

- PwC

- RSM US

- Grant Thornton LLP

- A.T Kearney

- BDO USA

- CBIZ & Mayer Hoffman McCann

- Crowe Horwath*

第7章 市場機会と今後の動向

目次

The US Auditing Services Market size is estimated at USD 51.88 billion in 2025, and is expected to reach USD 60.94 billion by 2030, at a CAGR of 3.27% during the forecast period (2025-2030).

In recent decades, market consolidation has become a prominent trend, as auditing firms strategically acquire global accounting entities to broaden their service offerings and improve existing auditing services. This trend has led to a notable decrease in the number of global audit firms, consolidating major players into what is commonly referred to as the Big Four.

In the United States, this consolidation is particularly pronounced, where the Big Four accounting firms collectively audit nearly 97% of the total US S&P 500 market capitalization. The concentration is even more pronounced in specific industries, with one or two firms dominating certain sectors. For instance, the leading auditing service provider in the US telecommunications services sector encompasses nearly 92% of the S&P 500 market capitalization. Similar scenarios exist in industries such as energy, materials, and information technology, where the top two service providers control at least 75% of the S&P 500 market capitalization. Recent market drivers and opportunities encompass technological advancements, regulatory changes, and increasing demand for specialized audit services, driving the evolution of the US Auditing Services Market.

US Audit Market Trends

Declining Quality of Auditing from the Big 4

Considering the high concentration of the audit service market in the US, investors raised issues with the probability of a lower concentration of audits, which can also result in lesser protection for investors. A ban or suspension on any of the firms could include a catastrophic effect on the market as it would create a huge void that the rest of the markets cannot handle. And considering the same, these firms are reasonably assured about their position from audit regulators. Auditors are fast becoming complacent and are already eliminating certain audit procedures to reduce costs, taking on riskier clients, consenting to the demands of management, and aggressively expanding their riskier non-audit service line under the trusted audit firm brand, which would only increase the auditing standards.

The major factor for this can be how the Big 4 firms and their subsidiaries work. These subsidiaries act as legally distinct business affiliates more than subsidiaries of the global networks, which share the same ethos. Unless regulators take firm action, the quality of the audits is expected to decline further.

Big 4 firms Increase the Auditing Fee as the Tenure Grows

One significant evidence of why the big four firms are monetizing on the lack of competition or regulation is the increased auditing fees for tenured companies. While convention dictates that firms should charge less to their tenured clients who provided the business for a long time, the same doesn't hold for the big four firms in the US.

The justification firms give for such a hike is the increasing workload as the business grows, and the changing corporate structure resulted in its toll on auditing. However, the same doesn't hold for non-big 4 firms whose fees remain flat and marginally decreasing. Big 4 firms, on average, charge their customers 32% higher fees in the 14th year compared to a 6% decline in fees by non-big 4 auditing firms in the same period. The fee increase is a direct consequence of these companies' power in the auditing space. Considering the list of bans imposed in other countries, it is only a matter of time before these companies are asked to follow stricter regulations.

US Audit Industry Overview

A complete background analysis of the US audit services market, including the assessment of the economy and contribution of the sectors in the economy, market overview, market size estimation for key segments and emerging trends in the market segments, market dynamics and insights, along with key health statistics, is covered in the report. Players including Deloitte, KPMG, EY, PwC, and RSM US, among others have been profiled in the report.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights on Technological Advancements in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Internal Audit

- 5.1.2 External Audit

- 5.2 Service line

- 5.2.1 Operational Audits

- 5.2.2 Financial Audits

- 5.2.3 Advisory and Consulting

- 5.2.4 Investigation Audit

- 5.2.5 Information System Audit

- 5.2.6 Compliance Audit

- 5.2.7 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Deloitte

- 6.2.2 EY

- 6.2.3 KPMG

- 6.2.4 PwC

- 6.2.5 RSM US

- 6.2.6 Grant Thornton LLP

- 6.2.7 A.T Kearney

- 6.2.8 BDO USA

- 6.2.9 CBIZ & Mayer Hoffman McCann

- 6.2.10 Crowe Horwath*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日