テレビとセットトップボックス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Television And Set Top Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645150

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

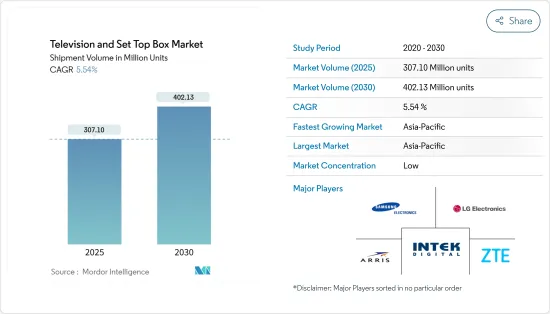

テレビとセットトップボックスの市場規模(出荷台数ベース)は、2025年の3億710万台から2030年には4億213万台に拡大し、予測期間(2025~2030年)のCAGRは5.54%と予測されます。

主要ハイライト

- セットトップボックスへの人工知能(AI)採用の急増、新興市場におけるインターネット普及率とブロードバンド普及率の上昇、OSベースのデバイスの継続的な展開が市場牽引に非常に大きな役割を果たしています。

- セットトップボックスの設置を義務付ける政府規制、STBベンダーによる利用可能なOSベース機器の展開、新興国におけるアナログ切り替え移行がSTB市場の需要を促進しています。例えば、インド政府はケーブルテレビ網(規制)法の改正によりSTBの設置を義務化しました。STBはデジタル信号のためより良い視聴体験を提供し、インドで違法チャネルが放送されるのを防ぐのに役立ちます。

- さらに、前年の第4四半期には、インドのテレビ格付け機関のガイドラインを見直すために情報放送省(MIB)が設置した4人の委員会が、RPD(Return Path Data)の規定を、配信プラットフォーム事業者(DPO)が今後導入するすべてのセットトップボックス(STB)の必須機能にするよう勧告し、RPDが暗号化、条件付きアクセス、その他のSTBレベルの必須機能と同等のユビキタス機能になるようにしました。

- また、様々な技術革新の高まりにより、様々な革新的機能を備えた幅広いSTBが開発されるようになりました。その結果、セットトップボックス企業間の競争が激化しています。さらに、デジタルビデオ録画は最も望まれている機能の1つであり、視聴者はお気に入りの番組を見たり録画したりすることができます。

- さらに、市場はデジタルエンターテインメントサービスとIPTVの統合を目の当たりにしています。例えば、今年第2四半期、アジア初の4K RDK IPTVボックス・プロバイダーであるSkyworth Digitalは、インドのマルチシステムオペレーターであるBhimavaram Community Network(BCN)が、BCNのデジタルエンターテインメントサービスの提供元としてSkyworth Digitalを選択したと発表しました。

- また、Convivaによると、2021年第1四半期現在、最も人気のあるOTT TVデバイスはRokuで、北米におけるTV視聴時間の37%を占めています。さらに、4Kのような技術の登場による視聴体験の向上と、インフラやデバイスの改良が相まって、音声ビデオとデータをバンドルしたサービスが登場しています。さらに、テレビ視聴率測定機関であるBARC India(Broadcast Audience Research Council of India)の報告によると、テレビ視聴率はパンデミック中も急上昇を続けた。このような動向は、調査対象市場の成長の触媒としてさらに作用すると予想されます。

- COVID-19の大流行により、ウイルスの蔓延を抑えるために政府による封鎖が行われました。各国での封鎖は、様々な通信サービスプロバイダのサプライチェーンに影響を与えました。昨年第3四半期、AirtelのDTH部門は、COVID-19によるサプライチェーンの混乱に対処するため、昨年末までに高解像度セットトップボックスの輸入を停止し、現地開発のセットトップボックスを製造する計画を発表しました。しかし、COVID-19の流行はオーバー・ザ・トップ(OTT)サービスの増加にもつながりました。Hulu、Prime Video、NetflixなどのOTTプラットフォームは、いずれも加入者数の増加を発表しています。OTTサービスへのシフトにより、サービスプロバイダーはライブストリーミングとオーバーザトップコンテンツを提供するハイブリッドセットトップボックスを提供するようになりました。

テレビとセットトップボックス市場動向

衛星技術は市場の大幅な成長が期待される

- 衛星テレビは、セットトップボックス市場で最も重要なアプリケーションの1つです。衛星テレビのイノベーションの1つは番組録画機能の導入であり、これにより消費者は番組をリアルタイムで録画し、後で都合の良いときに見ることができます。

- また、衛星STBユニットは、ビデオ・オン・デマンドや電子番組ガイドなど、さまざまな双方向機能を搭載するようになっています。より先進的STB装置は、基本機能に加えて、インターネット閲覧、電子メール、インスタントメッセージなど、一連の双方向マルチメディアサービスをユーザーテレビシステムを通じて直接記載しています。

- 各国政府は、国境内外でそれぞれのダイレクト・トゥ・ホーム(DTH)サービスの提供範囲を拡大するため、宇宙プログラムの拡大を検討してきました。今年第2四半期、ISROは通信衛星GSAT-24の打ち上げを発表しました。この衛星は、NewSpace India Limited(NSIL)により、初の需要主導型通信衛星ミッションとして打ち上げられました。GSAT-24に搭載された衛星の全容量は、タタ・グループのDTH事業であるタタ・プレイ(Tata Play)に貸与され、彼らのアプリケーション要件を満たします。

- さらに、衛星/DTHセットトップボックス市場のベンダーは、この市場の顧客ベースを誘致するために魅力的なオファーを打ち出しています。例えば、Dish TVは2021年最終四半期に、インドのマハラシュトラ州、ウッタル・プラデシュ州、西ベンガル州、北東部、アッサム州、さらにオリッサ州、パンジャブ州、ラジャスタン州、ハリヤナ州、グジャラート州、ヒマーチャル・プラデシュ州、チャッティースガル州、ジャンムー&カシミール州の8州のユーザーを対象にMPEG4ボックスの無料アップグレードオファーを提供しました。アップグレード時には、セットトップボックス、リモコン、HDMIケーブル、A/Vケーブル、アダプターが提供されます。加入者は新しいSTBの12ヶ月保証も受けられます。さらに、ハイブリッドDTHセットトップボックスの発売は、STB市場の衛星セグメントで人気を集めています。

- インド電気通信規制庁(TRAI)によると、昨年上半期のインドのDTH市場では、タタ・グループ傘下の事業者であるTata Skyが市場の約33%を占め、最も大きなシェアを占めていました。測定期間中、同社はAirtelを上回り、Dish TV、Sun Directが続きました。残りのDTH事業者は、市場シェアの下落に見舞われたDish TVを除き、同年の市場支配をさらに強固なものにしました。したがって、これらの事業者の市場シェアが上昇すれば、予測期間を通じて市場は拡大すると考えられます。

アジア太平洋が主要市場シェアを占める

- アジア太平洋は、技術導入の面でも顕著な地域のひとつです。有料テレビ市場は飽和状態にあり、競争も激しいため、アジア太平洋のベンダーはAndroid搭載テレビにゲートウェイ機能、セキュリティ、アプリケーション、HD機能などを追加しようとしています。

- さらに、アジア諸国ではセットトップボックスの設置を義務付ける政府の規制が後押ししており、これがアジア太平洋のセットトップボックス市場の成長を後押ししています。情報放送省(MIB)によると、MSOは1726社あります。さらに、加入者ベースがそれぞれ100万を超えるMSOが12社、Headend-in-the-Sky(HITS)事業者が1社あります。現在、インドには有料DTH事業者が4社あり、6,957万人のユーザーにテレビサービスを提供しています。

- さらに、この地域の市場は、より質の高い映画や強力な技術的インターフェースが重視されるようになり、豊富な資源と労働力の利用可能性によってもたらされる国の低製造コストによって拡大しています。テクニカラーなどの企業は、インドなどのアジア諸国で生産能力を拡大しています。さらに、昨年の第3四半期には、タタ・スカイがインド製のセットトップボックスの第一弾を発表しました。このセットトップボックスは、Technicolor Connected HomeとFlextronicsとの提携により製造されました。

- さらに、この地域では、ケーブルからオーバー・ザ・トップ(OTT)への移行がはっきりと見られました。この移行の主要原因は、COVID-19の蔓延を食い止めるために実施されたロックダウンです。動画広告・収益化プラットフォームのSpotXが昨年発表したレポートによると、アジア太平洋では4億人以上がOTT動画ストリーミングサービスを利用しており、動画視聴者の69%以上が週に1回以上ストリーミング動画を視聴しています。さらに、OTT視聴の上位3市場には、シンガポール(91%)、オーストラリア(81%)、インドネシア(76%)が含まれています。また、OTTストリーミングは東南アジアで急激に増加しています。

- また、TRAIが発表したデータによると、Netflix、Amazon Prime Video、AltBalajiが相当数の加入者を獲得したため、ケーブルテレビとDTHテレビサービスプロバイダーは、パンデミックの間にストリーミングサービスに地盤を譲った。これと同様に、通信事業者のDTHプロバイダーもOTT参入企業と提携し、完全なエンターテインメント・コンテンツを提供しています。Vodafone Ideaは昨年第3四半期に、OTTプラットフォームの消費拡大とモノのインターネット(IoT)の加速により、通信産業はデジタル変革期を迎えていると発表しました。同社はVoot SelectやSun NXTといった地元のOTTプラットフォームと提携しました。

テレビとセットトップボックス産業概要

テレビ産業はここ数年で無数の変化を目の当たりにし、より多様化しています。ARRIS International PLC、Intek Digital Inc.、ZTE Corporation、Samsung Electronics、LG Electronicsなどの主要企業は、戦略的合併、買収、提携を通じて継続的に技術革新を行い、市場拡大を模索しています。

2022年3月、Technicolor Connected Homeは、2,620万人以上の固定とモバイル加入者を有するフランスの著名なネットワークサービスプロバイダーの1つであるBouygues Telecomと提携し、フランス市場全体で消費者にビデオ体験を提供するクラス最高のWi-Fiと統合された、将来性のあるプレミアムAndroid 4K超高精細(UHD)STBを開発・展開しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヵ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 利害関係者分析

- COVID-19の市場への影響評価

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- 先進的技術革新

- 新興市場での採用拡大

- OSベースのデバイス展開

- 市場抑制要因

- 生産コストの増大とベンダー統合が成長鈍化の主要要因に

- 市場は成熟期を迎えつつある

第6章 市場セグメンテーション:セットトップボックス

- 技術別

- 衛星/DTH

- IPTV

- ケーブル

- その他のタイプ(DTTとOTT)

- 解像度別

- SD

- HD

- ウルトラHD以上

- 地域別

- 北米

- 欧州

- アジア

- オーストラリアとニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 市場セグメンテーション-テレビ

- 解像度別

- HD/FHD

- 4K

- 8K

- サイズ別(インチ)

- 32以下

- 39~43

- 48~50

- 55~60

- 65以上

- 技術別

- LCD

- 有機EL

- QLED

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第8章 ベンダー市場シェア分析

- ベンダー市場シェアセットトップボックス市場

- ベンダー市場シェアテレビ市場

第9章 競合情勢

- 企業プロファイル

- ARRIS International PLC(CommScope Inc.)

- Technicolor SA

- Intek Digital Inc.

- HUMAX Electronics Co. Ltd

- ZTE Corporation

- Skyworth Digital Ltd

- Sagemcom SAS

- Gospell Digital Technology Co. Limited

- Kaon Media Co. Limited

- Shenzhen Coship Electronics Co. Ltd

- Evolution Digital LLC.

- Shenzhen SDMC Technology Co. Ltd

- Samsung Electronics Co. Ltd

- LG Electronics

- TCL

- Hisense

- Xiaomi

第10章 投資分析

第11章 投資分析市場の将来

目次

The Television And Set Top Box Market size in terms of shipment volume is expected to grow from 307.10 Million units in 2025 to 402.13 Million units by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Key Highlights

- The surge in the adoption of artificial intelligence (AI) in set-top boxes, the rising internet penetration and broadband adoption in emerging markets, continuous deployment of OS-based devices is playing a very significant role in driving the market.

- The government regulations mandating the installation of set-top boxes, deployment of available OS-based devices by STB vendors, and analog switch-off transition in emerging countries are driving the demand for the STB market. For instance, the Government of India has made STBs compulsory through an amendment to the Cable Television Networks (Regulation) Act. STBs provide a better viewing experience because of digital signals and help prevent illegal channels from being broadcasted in India.

- Moreover, in the last quarter of the previous year, the four-member committee formed by the Ministry of Information and Broadcasting (MIB) to review guidelines for TV rating agencies in India recommended that the provision for Return Path Data (RPD) be made a mandatory capability in all future set-top boxes (STBs) deployed by Distribution Platform Operators (DPOs) so that the RPD becomes a ubiquitous capability on par with encryption, conditional access, and other such mandatory STB-level capabilities.

- Also, the rise in various technological innovations led to development a wide range of STBs with various innovative features. This, in turn, has made the competition fierce among the set-top box companies. Moreover, digital video recording is one of the most desired features, enabling viewers to watch and record their favorite shows.

- Additionally, the market is witnessing the integration of digital entertainment services and IPTV. For instance, in the second quarter of this year, Asia's first 4K RDK IPTV box provider Skyworth Digital announced that Bhimavaram Community Network (BCN), India's multi-system operator, had selected Skyworth Digital as the source of BCN's digital entertainment offerings.

- Also, according to Conviva, the most popular OTT TV device as of Q1 2021 was Roku, with a 37% share of TV viewing time in North America. Moreover, enhanced viewer experience, owing to the advent of technologies such as 4K, coupled with better infrastructure and devices, has led to the emergence of bundled voice video and data services. Further, TV viewership continued to surge during the pandemic, as reported by the television viewership measurement agency Broadcast Audience Research Council of India (BARC India). Such trends are further expected to act as catalysts for the growth of the studied market.

- The COVID-19 pandemic led to lockdowns imposed by the government to curb the spread of the virus. The lockdown across countries has affected the supply chains of various telecom service providers. In the 3rd quarter of the last year, Airtel DTH arm announced plans to stop imports of high-definition set-top boxes by the end of last year to tackle the COVID-19-induced supply chain disruption and make locally developed set-top boxes. However, the COVID-19 pandemic also led to an increase in over-the-top (OTT) services. OTT platforms, such as Hulu, Prime Video, Netflix, and more, have all announced their increase in subscriber rates. The shift toward OTT services has led service providers to offer hybrid set-top boxes that provide live streaming and over-the-top content.

TV Set Top Box Market Trends

Satellite Technology is Expected to Witness Significant Market Growth

- Satellite television is one of the most significant applications of the set-top box market. One of the innovations in satellite TV is introducing a show-recording facility, which enables consumers to record their shows in real-time and watch them later at their convenience.

- Also, the satellite STB units are increasingly equipped with various interactive features, like video-on-demand, electronic program guides, etc. More advanced STB units also provide a suite of interactive and multimedia services directly through a user television system, such as internet browsing, email, and instant messaging, in addition to basic functionality.

- The governments have been looking to expand their space programs to increase the range of respective direct-to-home (DTH) offerings within and outside their borders. In the 2nd quarter of this year, ISRO announced the launch of the communication satellite GSAT-24. The satellite was launched by NewSpace India Limited (NSIL) in its first demand-driven communication satellite mission. The total satellite capacity on board GSAT-24 will be leased to its committed customer Tata Play, the DTH business of Tata Group, to meet their application requirements.

- Moreover, satellite/DTH set-top box market vendors are coming up with attractive offers to lure the customer base in this market. For instance, in the last quarter of 2021, Dish TV offered a free MPEG4 box upgrade offer for users in Maharashtra, Uttar Pradesh, West Bengal, North East, and Assam, and eight more states, including Orissa, Punjab, Rajasthan, Haryana, Gujarat, Himachal Pradesh, Chhattisgarh and Jammu & Kashmir in India. The set-top box, remote, HDMI, or A/V cable and adapter would be provided upon upgrading. Subscribers will also get 12 monthly warranty on the new STB. Furthermore, the launch of Hybrid DTH set-top boxes is gaining popularity in the satellite segment of the STB market.

- As per Telecom Regulatory Authority of India (TRAI), in India's DTH market during the first half of the last year, Tata Sky, a business under the Tata Group, had the most significant share with around 33% of the market. During the measured time, the operator was ahead of Airtel, followed by Dish TV and Sun Direct. The remaining DTH operators further solidified their control of the market that year, except for Dish TV, which suffered a fall in its market shares. Hence, the rise in such market shares of these operators will amplify the market throughout the forecasted period.

Asia Pacific to Hold Major Market Share

- The Asia-Pacific region is also one of the prominent regions in terms of technology adoption. Due to the market saturation of Pay-TV consumers and stiff competition, vendors in the Asia Pacific region are constantly trying to add features to their Smart android-based televisions, such as gateway abilities, security, applications, and HD functionality.

- Moreover, the supportive government regulations mandating the installation of set-top boxes in Asian countries are driving the growth of the Asia Pacific set-top box market. According to the Ministry of Information and Broadcasting (MIB), there are 1726 MSOs. Further, there is 12 MSOs and one Headend-in-the-Sky (HITS) operator with a subscriber base greater than one million each. There are currently 4 Pay DTH operators in India, providing television services to 69.57 million users.

- Additionally, the region's market is expanding due to the growing emphasis on higher-quality movies and potent technological interfaces and the nation's low production costs brought on by the availability of plentiful resources and labor. Companies such as Technicolor, and others, have been expanding their manufacturing capabilities in Asian countries such as India. Moreover, in the 3rd quarter of the last year, Tata sky also unveiled its first batch of India-made set-top boxes. The set-top boxes were manufactured in partnership with Technicolor Connected Home and Flextronics.

- Additionally, the region has clearly seen the transition from cable to over-the-top (OTT). The main cause of the transition was the lockdowns implemented to stop the COVID-19 pandemic from spreading. According to last year's report by SpotX, a video advertising and monetization platform, more than 400 million people use OTT video streaming services across the Asia Pacific region, with over 69% of video viewers watching a streaming video at least once a week. Furthermore, the top three markets for OTT viewing included Singapore (91%), Australia (81%), and Indonesia (76%). Also, OTT streaming has increased drastically in Southeast Asia.

- Also, according to the data released by the TRAI, cable and DTH television service providers ceded ground to streaming services during the pandemic, as Netflix, Amazon Prime Video, and AltBalaji reached a significant number of subscribers. On similar lines, telecom DTH providers are also partnering with OTT players to offer complete entertainment content. In the third quarter of the last year, Vodafone Idea announced that the telecom industry is undergoing a digital transformation due to the growing consumption of OTT platforms and the Internet of Things (IoT) acceleration. The company partnered with local OTT platforms such as Voot Select and Sun NXT.

TV Set Top Box Industry Overview

The television industry has witnessed myriad changes over the past several years and has become more diverse. The major players, such as ARRIS International PLC, Intek Digital Inc., ZTE Corporation, Samsung Electronics Co. Ltd., and LG Electronics, continuously innovate and seek market expansion through strategic mergers, acquisitions, and partnerships.

In March 2022, Technicolor Connected Home partnered with Bouygues Telecom, one of France's prominent network service providers with over 26.2 million fixed and mobile subscribers, to develop and deploy a futureproof and premium Android 4K ultra high-definition (UHD) STB integrated with best-in-class Wi-Fi that delivers video experiences to consumers throughout the French market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Stakeholder Analysis

- 4.4 An Assessment of Impact of COVID-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Levels of Technological Innovations

- 5.1.2 Growing Adoption in the Emerging Markets

- 5.1.3 Deployment of OS-based Devices

- 5.2 Market Restraints

- 5.2.1 Growing Production Costs and Vendor Consolidation Cited as the Key Reasons for Slow Growth Forecast

- 5.2.2 Given that the Market is on the Verge of Reaching Maturity

6 MARKET SEGMENTATION - SET-TOP BOX

- 6.1 By Technology

- 6.1.1 Satellite/DTH

- 6.1.2 IPTV

- 6.1.3 Cable

- 6.1.4 Other Types (DTT and OTT)

- 6.2 By Resolution

- 6.2.1 SD

- 6.2.2 HD

- 6.2.3 Ultra-HD and Higher

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 MARKET SEGMENTATION - TELEVISION

- 7.1 By Resolution

- 7.1.1 HD/FHD

- 7.1.2 4K

- 7.1.3 8K

- 7.2 By Size (in inches)

- 7.2.1 32 and below

- 7.2.2 39-43

- 7.2.3 48-50

- 7.2.4 55-60

- 7.2.5 65 and above

- 7.3 By Technology

- 7.3.1 LCD

- 7.3.2 OLED

- 7.3.3 QLED

- 7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia

- 7.4.4 Australia and New Zealand

- 7.4.5 Latin America

- 7.4.6 Middle East and Africa

8 VENDOR MARKET SHARE ANALYSIS

- 8.1 Vendor Market Share Set-top box Market

- 8.2 Vendor Market Share Television Market

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 ARRIS International PLC (CommScope Inc.)

- 9.1.2 Technicolor SA

- 9.1.3 Intek Digital Inc.

- 9.1.4 HUMAX Electronics Co. Ltd

- 9.1.5 ZTE Corporation

- 9.1.6 Skyworth Digital Ltd

- 9.1.7 Sagemcom SAS

- 9.1.8 Gospell Digital Technology Co. Limited

- 9.1.9 Kaon Media Co. Limited

- 9.1.10 Shenzhen Coship Electronics Co. Ltd

- 9.1.11 Evolution Digital LLC.

- 9.1.12 Shenzhen SDMC Technology Co. Ltd

- 9.1.13 Samsung Electronics Co. Ltd

- 9.1.14 LG Electronics

- 9.1.15 TCL

- 9.1.16 Hisense

- 9.1.17 Xiaomi

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日