マルチベンダーサポートサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Multi Vendor Support Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645142

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

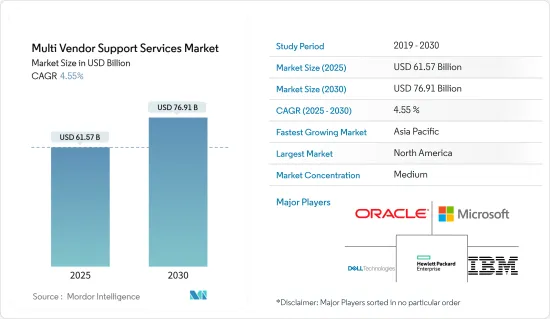

マルチベンダーサポートサービスの市場規模は、2025年に615億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.55%で、2030年には769億1,000万米ドルに達すると予測されます。

マルチベンダーサポートサービスは、複数のベンダーと契約していたIT管理を簡素化し、専門知識を持つ単一のベンダーがすべてのITインフラを保守できるようにします。そのため、マルチベンダーサポートは、IT環境全体にわたる問題の特定と解決を合理化することで、ダウンタイムを削減します。企業の間では、先進的なソリューションの開発と受け入れが大幅に増加しています。このようなマルチベンダーサポートサービスは、複数のITソリューションやサービスの管理に伴うリスクを軽減すると同時に、円滑な生産や日常業務を改善するのに役立っています。このため、マルチベンダーサポートサービスの需要は世界中で高まっています。

主なハイライト

- 過去数年のITインフラ移行期とは異なり、多くの企業は厳しい予算制約とCAPEXの削減を理由に、サードパーティーのマルチベンダーメンテナンス・プロバイダーへとシフトしています。コスト効率を維持しながらより多くのことを行おうとする企業は、従来のアップタイムとパフォーマンスを維持しながらソリューションとサービスの支出を抑えるために、サードパーティの保守に関心を寄せています。

- クラウド、IoTプラットフォーム、コンテナ、DevOps、ビッグデータ向けのITサービスは、予測期間中、マルチベンダーサポートサービスプロバイダーにとって大きな可能性を秘めていると予想されます。世界中の企業や政府機関は、従来の環境から、より業務上重要なワークロードや計算インスタンスをクラウドに移行しつつあります。

- さらに、デジタルトランスフォーメーション戦略の重要な一環として、複数の組織でIoT、クラウド、ビッグデータ分析の導入が急速に進んでいるため、データセンターへの負荷も増加しており、市場の成長につながっています。現在のシナリオでは、データセンターは数千ものコンポーネントを備え、かつてないほど複雑になっています。このような厳しい環境でのライフサイクル・メンテナンスは不可欠であるが、IT関係者がパフォーマンスとコストのバランスを取るために取り組むため、非常に困難でもあります。これが、今日の企業にとってライフサイクル・メンテナンスが管理者の頭痛の種となっている理由です。企業は何十社ものベンダーと保守契約を結んでおり、それぞれが複数の種類の機器を所有しています。マルチベンダーサポートサービスの導入が進むにつれ、データセンターのライフサイクル・メンテナンスはより管理しやすくなり、コスト効率も向上しています。

- 企業がITインフラに新しいテクノロジーを追加したり、サービスレベルを更新したり、新しいサポート契約を結んだり、各ベンダーとの保証を更新したりするにつれて、マルチベンダーサポート環境をサポートするための目まぐるしく変化する課題は、飛躍的に難しくなります。このような問題を解決するために、Dell Technologiesのようなテクノロジー・プロバイダが提供するトータル・サポート・マネジメントは、マルチベンダーサポートサービスを提供しています。このサービスは、IT組織全体のコストを削減し、生産性を向上させるだけでなく、すでに多くの日常管理タスクを管理しているリソースの負担を軽減します。

- COVID-19が大流行した当時、リモートワークは世界中で急増しました。マルチベンダーのサポート・サービス・プロバイダーは、円滑な作業環境を維持するために、企業の問題を解決する機会を活用しています。例えば、IBMのクラウド・ソリューションは、仮想化、モビリティ、コラボレーション、サポートのための柔軟でセキュアなクラウドとデジタル・サービスによって、企業がスモール・ビジネスへのシームレスな移行を行うのを支援することができます。リモート・ワークの状況では、シスコの詳細なナレッジ・ベースの助けを借りて、IBM Corporationのインテリジェント・ネットワーク・サポートは、問題が発生し企業運営に影響を及ぼす前にユーザーが問題を特定できるようにするプロアクティブ・サポート・モデルを提供します。

マルチベンダーサポートサービスの市場動向

IT・通信分野は予測期間中に大幅な成長が見込まれる

- IT・通信業界は、さまざまな技術の採用率の高さ、BYODポリシーの採用頻度の増加(企業運営をより快適で管理しやすくするため)、企業間のデータ急増によるハイエンド・セキュリティへのニーズの高まりから、マルチベンダーサポートサービスの重要なセグメントとなっています。

- 電気通信業界は過去数年間、大きな成長を遂げてきました。通信会社は、競争の激しい市場で顧客を維持するため、革新的なサービスを低コストで提供するよう常に求められています。マルチベンダーサポートサービスは、複雑な競合環境に対応するために通信事業者に広く求められるようになった。

- マルチベンダーSD-WANサービスの展開もかなりの割合で増加しています。これには、uCPEプラットフォームと、セキュリティ、ルーティング、SDNスイッチング、vBNG/vCGNAT、NFV、サービスアシュアランスを含む広範なソフトウェアサービスチェイニングとの包括的な検証と統合が含まれます。マルチベンダーネットワークの需要に対応するため、台湾のLanner社は、マルチコアコンピューティング能力、暗号アクセラレーションエンジン、WiFi/LTE/5G対応接続性を提供するオープンで相互運用可能なuCPEプラットフォームを幅広く提供しています。

- 企業は、クラウド、ワークフォース、アプリケーションの変革目標を達成するために、集中型から分散型ITパラダイムに移行する必要があります。企業は、旧式のリモート・アクセス、VPN接続、非効率的なクラウド/SaaSアクセス、劣悪なアプリケーション品質、安全性の低下など、従来のネットワーキング、セキュリティ、運用方法では困難な状況に直面することになります。

- Aruba NetworksとPonemon Instituteが昨年実施した調査では、北米の回答者の64%がゼロトラストを知っていると回答し、47%がSASEを知っていると回答しました。一般的に、回答者はSD-WANにほとんど触れていないです。セキュリティプロトコルはSASEやゼロトラストのようなセキュリティアーキテクチャを使って実装されます。一般的にゼロトラストセキュリティモデルと呼ばれる境界セキュリティの概念は、デバイスはデフォルトでは信頼されないというものです。

北米が大幅な市場成長を占める。

- 北米地域セグメントの成長の主な原動力は、テクノロジー・プロバイダーの存在感が大きいことです。これらのプレーヤーは、この地域と世界の競合情勢に勝ち残るために、パートナーシップの締結、合併買収、革新的なソリューションの提供に注力しています。米国のような国々は、北米市場セグメントの成長に大きく貢献しています。米国市場は、ITインフラ環境の変化、特に中小企業(SME)がITソリューションやサービスのアウトソーシングに継続的に注力していることから成長しています。

- 在宅ヘルスケアにおける医療機器の利用拡大、入院患者から外来患者への外科手術の移行、MVSプロバイダーやヘルスケア施設による技術受容の拡大などが背景にあります。MVS市場は、コンサルティング、分析、ITソリューション、在庫管理、サイバーセキュリティなどの専門サービスにより、従来の機器保守・修理サービス型モデルから完全マネージドサービス型モデルへの転換が予想されます。

- ITインフラの迅速な変化は、MVSS市場の拡大に拍車をかけている主な要素です。ITインフラの規模と複雑さはますます増大しています。これは、増大するコンピューティング需要に対応するため、より大規模で優れたネットワーク、サーバー、ストレージ・デバイスが必要とされているためです。組織は、クラウド、コンテナ、IoT、その他のテクノロジーを使って業務のデジタル化を進め、増大するビジネス・タスクのニーズを満たそうとしています。

- 米国とカナダでは、マルチクラウド環境の利用が急拡大しており、顧客は1つのクラウドを大量に利用する一方で、もう1つのクラウドを散発的に利用しています。MSPは、消費ベースのサービス価格モデルを提供することで、大きなチャンスを提供できます。このことも、同地域におけるマルチベンダーサポートサービス市場の成長を後押しすると思われます。

- さらに、さまざまな産業やセクターでIoTが急速に統合されているため、スマートデバイスの普及が進むと予想されます。このため、マネージド・マルチベンダーサービスの導入が促進され、市場の成長に拍車がかかると予測されます。

マルチベンダーサポートサービス産業の概要

マルチベンダーサポートサービス市場は適度な競争状態にあり、多くの世界および地域プレーヤーで構成されています。これらのプレーヤーはかなりの市場シェアを占めており、顧客基盤を世界に拡大することに注力しています。これらのベンダーは、研究開発活動、戦略的提携、その他の有機的・無機的成長戦略に注力し、予測期間における競争力を獲得しています。

- 2022年11月- 企業は競争力を維持するために、アプリケーションを近代化し、マルチクラウドやSaaSを導入し、ユーザーが職場や自宅などからこれらのアプリケーションにアクセスできるようにしようとしています。VMware, Inc.は、アプリ、データ、サービスを、それらがどこにあろうと、拠点、支店、自宅、あらゆるネットワーク、あらゆるデバイスに配信するビジネスを支援するために、新しいSD-WAN Clientを含む次世代SD-WANソリューションを発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- OEMサービスのメンテナンスコスト上昇

- 市場の課題

- セキュリティとプライバシー問題への懸念

第6章 マルチベンダーサポートサービス市場におけるCOVID-19の影響

第7章 市場セグメンテーション

- サービスタイプ別

- プロフェッショナル

- マネージド

- 企業規模別

- 中小企業

- 大企業

- エンドユーザー業界別

- IT・通信

- BFSI

- ヘルスケア

- エネルギー・電力

- 製造業

- その他(小売、メディア&エンターテインメント、旅行&観光)

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第8章 競合情勢

- 企業プロファイル

- IBM Corporation

- Oracle Corporation

- Microsoft Corporation

- Clear Technologies, Inc.

- Dell Technologies Inc

- Evernex Group SAS

- Hewlett Packard Enterprise Co

- Quantum Corp

- Blue Sky Group Ltd

- Softcat plc

- NetApp Inc.

第9章 投資分析

第10章 市場の将来

目次

The Multi Vendor Support Services Market size is estimated at USD 61.57 billion in 2025, and is expected to reach USD 76.91 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Multi-vendor support services can help any business to simplify IT management from multiple vendor contracts to a single vendor with expertise to maintain all the IT infrastructure. Therefore, multi-vendor support reduces downtime by streamlining problem identification and solving across the entire IT environment. There is a significant increase in the development and acceptance of advanced solutions among businesses. These multi-vendor support services help to decrease the risk associated with managing several IT solutions and services while improving smooth production or daily work. This is bolstering the demand for multi-vendor support services across the world.

Key Highlights

- Unlike the last couple of IT infrastructure transition years, many businesses are shifting towards the third-party multi-vendor maintenance provider because of the severe budget constraints and reductions in the CAPEX. Enterprises seeking to do more while keeping it cost-efficient are interested in third-party maintenance to limit their solutions and service expenditures while retaining their conventional uptime and performance.

- The IT services for cloud, IoT platforms, containers, DevOps, and Big Data are expected to hold tremendous potential for the multi-vendor support service providers in the forecast period. Enterprises and government organizations worldwide are moving from conventional environments to placing more work-critical workloads and compute instances into the cloud.

- Further, owing to the rapidly increasing adoption of IoT, cloud, and Big data Analytics across multiple organizations as a significant part of their digital transformation strategy, the burden on the data centers is also increasing, leading to the market's growth. In the current scenario, data centers are more complex than ever, with thousands of components. Lifecycle maintenance in this difficult environment is essential, but it is also very challenging as IT players work to balance performance and cost. This is why lifecycle maintenance is an admin headache for today's enterprises. They have maintenance contracts with dozens of vendors, each with multiple types of equipment. With the increasing adoption of multi-vendor support services, the lifecycle maintenance of data centers becomes more manageable and cost-effective.

- The fast-paced and ever-changing challenges of supporting a multi-vendor support environment get exponentially difficult as an enterprise adds new technology to its IT infrastructure, updates levels of service, new support agreements, or updates warranties with each vendor. To solve these arising problems, total support management provided by technology providers like Dell Technologies is offering multi-vendor support services, which not only cut costs and increase productivity across an IT organization but also lower the burden on resources already managing too many daily admin tasks.

- At the time of the COVID-19 pandemic, remote working has surged worldwide. Multi-vendor support services providers are taking the opportunity to take advantage to solve enterprise problems to maintain a smooth working environment. For example, IBM Cloud solutions can help an enterprise to make a seamless transition to small business with flexible, secure cloud and digital services for virtualization, mobility, collaboration, and support. In the remote working condition, with the help of Cisco's in-depth knowledge base, IBM Corporation's intelligent network support delivers a proactive support model that helps the user to identify problems before they occur and affect enterprise operations.

Multi-Vendor Support Services Market Trends

IT & Telecommunication Vertical is Expected to Grow at a Significant Rate Over the Forecast Period

- The IT and telecommunication vertical is a significant segment for the multi-vendor support services due to the high rate of various technological adoptions, increased frequency of adoption of the BYOD policy (to make business operations much more comfortable and controllable), and growing need for high-end security due to the rapidly increasing data among the organizations.

- The telecom industry has observed extensive growth during the past few years. Telecommunication companies are constantly pressured to deliver innovative services at lower costs to retain their customers in the competitive market. Multi-vendor support services have become a widespread demand for operators to address a complex and competitive environment.

- The deployment of multi-vendor SD-WAN services is also increasing at a significant rate. This involves comprehensive validation and integration of the uCPE platform with a wide range of software service chaining, including security, routing, SDN switching, vBNG/vCGNAT, NFV, and service assurance. To meet the demand for multi-vendor networks, Lanner, a Taiwan-based company, offers a wide range of open, interoperable uCPE platforms that offer multi-core computing power, crypto acceleration engines, and WiFi/LTE/5G-ready connectivity.

- An enterprise must transition from a centralized to a distributed IT paradigm to undertake these cloud, workforce, and application transformation objectives. Businesses will experience difficulties using conventional networking, security, and operational methods, such as old-fashioned remote access, VPN connectivity, ineffective cloud/SaaS access, subpar application quality, and compromised safety.

- In the last year, 64% of North American respondents to a survey by Aruba Networks and Ponemon Institute said they were familiar with zero trust, while 47% said they were aware of SASE. In general, respondents had little exposure to SD-WAN. Security protocols are implemented using security architectures like SASE and zero trust. The notion of perimeter security commonly referred to as the zero-trust security model holds that devices are not trusted by default.

North America to account for significant market growth.

- The primary driver for the North American geographic segment's growth is the significant presence of technology providers. These players focus on entering into partnerships, merger acquisitions, and innovative solutions offerings to stay in the regional and globally competitive landscape. Countries like the US are significant contributors to the growth of the North American market segment. The US market is growing due to the changing IT infrastructure landscape, especially in small and medium enterprises (SMEs) continually focusing on outsourcing IT solutions and services.

- The growing use of medical equipment in home healthcare, the transition of surgical procedures from inpatient to outpatient settings, and the increased technology acceptance by MVS providers and healthcare facilities. The MVS market is anticipated to transform from a conventional equipment maintenance and repair service-based model to a fully managed service model due to professional services like consulting, analytics, IT solutions, inventory management, and cybersecurity.

- The quick changes in IT infrastructure are the primary elements fueling the MVSS market expansion. The size and complexity of IT infrastructure are proliferating. This is because larger and better networks, servers, and storage devices are required to meet the growing computing demands. Organizations are progressively digitalizing their operations using the cloud, container, IoT, and other technologies to satisfy the increased needs of business tasks.

- The use of multi-cloud environments sees massive growth in the United States and Canada, wherein clients rely on one cloud massively while using the other sporadically. MSPs can offer a great opportunity by giving consumption-based service pricing models. This will also boost the growth of the multi-vendor support services market in the region.

- Furthermore, the penetration of smart devices is expected to increase, owing to the rapid integration of IoT across various industries and sectors. This is projected to propel the adoption and incorporation of managed multi-vendor services, thereby fueling the market's growth.

Multi-Vendor Support Services Industry Overview

The multi-vendor support services market is moderately competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their client base globally. These vendors focus on research and development activities, strategic alliances, and other organic & inorganic growth strategies to earn a competitive edge over the forecast period.

- In November 2022 - Enterprises are modernizing their applications, implementing multi-cloud and SaaS, and enabling users to access these applications from the workplace, home, or elsewhere to remain competitive. To assist businesses in delivering apps, data, and services-no matter where they are located-to the site, branch, and home, across any network, to any device, VMware, Inc. revealed its next-generation SD-WAN solution, which includes a new SD-WAN Client.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Maintenance Cost of OEM Services

- 5.2 Market Challenges

- 5.2.1 Concern Over Security and Privacy Issues

6 IMPACT OF COVID-19 ON THE MULTI VENDOR SUPPORT SERVICES MARKET

7 MARKET SEGMENTATION

- 7.1 By Service Type

- 7.1.1 Professional

- 7.1.2 Managed

- 7.2 By Enterprise Size

- 7.2.1 Small & Medium Enterprises

- 7.2.2 Large Enterprises

- 7.3 By End-user Verticals

- 7.3.1 IT & Telecommunication

- 7.3.2 BFSI

- 7.3.3 Healthcare

- 7.3.4 Energy & Power

- 7.3.5 Industrial Manufacturing

- 7.3.6 Others (Retail, Media & Entertainment, Travel & Tourism)

- 7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia

- 7.4.4 Australia and New Zealand

- 7.4.5 Latin America

- 7.4.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 IBM Corporation

- 8.1.2 Oracle Corporation

- 8.1.3 Microsoft Corporation

- 8.1.4 Clear Technologies, Inc.

- 8.1.5 Dell Technologies Inc

- 8.1.6 Evernex Group SAS

- 8.1.7 Hewlett Packard Enterprise Co

- 8.1.8 Quantum Corp

- 8.1.9 Blue Sky Group Ltd

- 8.1.10 Softcat plc

- 8.1.11 NetApp Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日