|

|

市場調査レポート

商品コード

1645104

英国のローターブレード:市場シェア分析、産業動向、成長予測(2025~2030年)United Kingdom Rotor Blade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のローターブレード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

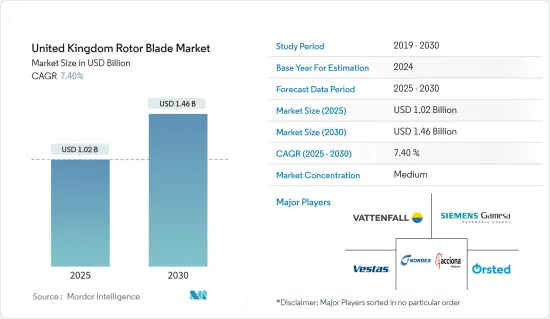

英国のローターブレード市場規模は2025年に10億2,000万米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは7.4%で、2030年には14億6,000万米ドルに達すると予測されています。

中期的には、洋上と陸上風力発電設備の増加、風力エネルギー価格の低下、風力発電セグメントへの投資の増加が、予測期間中の英国のローターブレード市場を牽引すると予想されます。

一方、輸送コストの高さや、太陽光発電、水力発電などの代替クリーンエネルギーの価格競合などの要因が、予測期間中の市場成長を制限する可能性があります。

風力発電セグメントは経済的な選択肢を模索しており、高効率製品は産業の力学を変える可能性を秘めています。古いタービンを交換しなければならなかったのは、破損のためではなく、より効率的なブレードが市場に出回っていたからだというケースもあります。このように、技術の進歩は最終的にローターブレード市場に絶好の機会をもたらします。

英国のローターブレード市場動向

洋上セグメントが市場を独占

過去5年間で、洋上風力発電技術は、風速の低いより多くの場所をカバーし、設置されたメガワット能力あたりの発電量を向上させるように進歩しました。これに加え、最近では風力タービンの数が増加し、風力タービンのブレードの大型化、直径の拡大、ハブの高さの向上が進んでいます。

2024年3月、英国政府は再生可能エネルギープロジェクトに10億英ポンド(12億5,000万米ドル)という最も重要な予算を発表しました。この中には、洋上風力発電に8億英ポンド(10億米ドル)、浮体式洋上風力発電と地熱技術に1億500万英ポンド(1億3,100万米ドル)が含まれています。

政府の目標を達成するため、英国の洋上風力発電容量は265%増加する予定です。2030年までに、英国政府は洋上風力発電を13.7GWから50GWに増やしたいと考えています。技術企業ABBによると、このためには今後7年間で平均1.5GWの風力発電所を24カ所建設する必要があります。その結果、英国のエネルギーミックスに占める洋上風力の割合は18%から62%に増加します。

英国は、風力エネルギー生産国として急成長している国のひとつです。同国は欧州における風力発電の理想的なスポットです。国際再生可能エネルギー機関(IRENA)によると、2023年の洋上風力発電設備容量は1万4,746MWで、2014年と比較して2.27倍に増加しています。

したがって、上記の要因を考慮すると、洋上風力タービンのローターブレードは、予測期間中に陸上風力エネルギープロジェクトの増加と相まって、政府の支援施策やイニシアチブによって大きく成長すると予想されます。

政府の支援施策と民間投資が市場需要を牽引

英国は、COP26で署名されたパリ気候協定の一環として、2050年までに純炭素排出量ゼロを達成することを約束しました。こうした目標は、英国の風力エネルギー市場に関わる企業にとって、間もなく大きな機会となるはずです。

国際再生可能エネルギー機関(IRENA)によると、2023年の風力発電設備容量は30,215MWで、2014年に比べて1.3倍に増加しました。今後、いくつかの風力発電プロジェクトが開始されるため、この数字は大幅に増加すると予想されます。

ここ数年、政府はこの地域全体で複数の洋上・陸上風力エネルギープロジェクトを立ち上げています。例えば2023年12月、政府はVestasとVattenfallが英国の洋上風力発電プロジェクトで140万kWの優先供給契約を、他の2つの英国プロジェクトで280万kWの独占契約を締結したと発表しました。この3つのプロジェクトの契約には、1,380MWのノーフォーク・ヴァンガード・ウェストプロジェクトの優先供給者契約も含まれています。

同様に、英国政府は2023年9月、95の新規再生可能エネルギー事業に対して差金決済契約(CFD)を締結し、3.7GWのクリーンエネルギー容量を確保すると発表しました。これらのプロジェクトには、陸上風力、太陽光、潮力エネルギー開発が含まれます。さらに、英国を拠点とするOctopus Energyは、2030年までに洋上風力発電に世界全体で200億米ドルを投資する計画です。 Octopus Energy Groupの子会社である同社は、この投資によって年間12ギガトン(GW)の再生可能エネルギー発電が行われ、これは1,000万世帯分の電力に相当すると述べています。

英国政府は、洋上・陸上風力発電を含む再生可能エネルギーへの投資について、他国と複数の協定を結びました。例えば、2023年5月、日本企業は、洋上風力、低炭素水素、その他のクリーンエネルギープロジェクトのために、英国への投資に180億英ポンド(225億米ドル)を約束しました。この投資は、洋上風力発電所全体のエネルギー発電量を増加させるのに役立ち、予測期間中にローターブレード市場を牽引する可能性が高いです。

したがって、投資の増加と今後のプロジェクトが、予測期間中の英国のローターブレード市場を牽引すると予想されます。

英国のローターブレード産業概要

英国のローターブレード市場は半固体化しています。この市場の主要企業(順不同)は、Vestas Wind Systems A/S、Siemens Gamesa Renewable Energy S.A.、Nordex SE、Orsted A/S、Vattenfall ABなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 洋上風力発電設備の増加

- 風力発電セグメントへの投資の増加

- 抑制要因

- 輸送コストの高さ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 展開場所別

- 陸上

- 洋上

- ブレード材料別

- 炭素繊維

- ガラス繊維

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy S.A.

- Nordex SE

- Orsted A/S

- Vattenfall AB

- BayWa R.E AG

- Enercon GmbH

- 市場ランキング分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 技術の進歩

The United Kingdom Rotor Blade Market size is estimated at USD 1.02 billion in 2025, and is expected to reach USD 1.46 billion by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

Over the medium term, the increasing number of offshore and onshore wind energy installations, the decreasing price of wind energy, and increased investments in the wind power sector are expected to drive the United Kingdom's rotor blade market during the forecast period.

On the other hand, factors that include the high cost of transportation and the price competitiveness of alternative clean energy sources such as solar power, hydropower, and others could restrict market growth during the forecast period.

Nevertheless, the wind power sector has been looking for economical options, and a highly efficient product has the potential to change the industry's dynamics. In some cases, old turbines had to be replaced not because of damage but because more efficient blades were available on the market. Thus, technological advancements eventually create an excellent chance for the rotor blade market.

United Kingdom Rotor Blade Market Trends

Offshore Segment to Dominate the Market

In the past five years, offshore wind power generation technology has advanced to cover more locations with lower wind speeds and to enhance electricity produced per installed megawatt capability. In addition to this, the number of wind turbines has increased recently, with larger wind turbine blades, wider diameters, and taller hub heights.

In March 2024, the government of the United Kingdom announced the most significant budget of GBP 1 Billion (USD 1.25 billion) for renewable energy projects, which includes GBP 800 million (USD 1 billion) for offshore wind and GBP 105 million (USD 131 million) for floating offshore wind and geothermal technologies.

In order to meet government targets, the UK's offshore wind capacity is going to be increased by 265%. By 2030, the UK government wants to increase offshore wind power from 13.7GW to 50GW. This will require the construction of 24 more wind farms with an average capacity of 1.5GW over the course of the next seven years, according to technology company ABB. As a result, the percentage of offshore wind in the UK's energy mix would increase from 18% to 62%.

The United Kingdom is one of the fastest-growing wind energy-producing countries. The country is Europe's ideal spot for wind power. According to the International Renewable Energy Agency (IRENA), installed offshore wind energy capacity was 14,746 MW in 2023, an increase of 2.27 times compared to 2014.

Hence, considering the above-mentioned factors, the offshore wind turbine rotor blade is expected to grow significantly due to supportive government policies and initiatives coupled with an increasing number of onshore wind energy projects during the forecast period.

Supportive Government Policies and Private Investments are Driving the Market Demand

The United Kingdom committed to achieving net-zero carbon emissions by 2050 as part of the Paris Climate Accord, which was signed during COP26. These objectives should soon offer significant opportunities for businesses involved in the United Kingdom wind energy market.

According to the International Renewable Energy Agency (IRENA), installed wind energy capacity was 30,215 MW in 2023, an increase of 1.3 times compared to 2014. The number is expected to rise significantly in the upcoming years as several wind energy projects start.

In the last few years, the government has launched multiple offshore and onshore wind energy projects across the region. For instance, in December 2023, the government announced that Vestas and Vattenfall signed a 1.4 GW preferred supplier agreement for the UK offshore wind project and exclusivity agreements for 2.8 GW for two other UK projects. The three projects' agreement includes a preferred supplier agreement for the 1,380 MW Norfolk Vanguard West project.

Similarly, In September 2023, the United Kingdom's Government announced the distribution of Contract for Difference (CFDs) to 95 new renewable energy initiatives, ensuring 3.7 GW of clean energy capacity. These projects include onshore wind, solar, and tidal energy developments. Furthermore, Octopus Energy, based in the United Kingdom, plans to invest USD 20 billion globally in offshore wind by 2030. The company, which is a subsidiary of Octopus Energy Group, stated that the investment will generate 12 gigatonnes (GW) of renewable electricity per year, enough to power 10 million homes.

The government of the UK signed multiple agreements with other countries for investment in renewable energy, including offshore and onshore wind energy. For instance, in May 2023, Japanese businesses committed GBP 18 billion (USD 22.5 billion) to investment in the UK for offshore wind, low-carbon hydrogen, and other clean energy projects. The investment helps to increase energy generation across offshore wind farms and is likely to drive the rotor blade market during the forecast period.

Therefore, increasing investments and upcoming projects are expected to drive the United Kingdom rotor blade market during the forecast period.

United Kingdom Rotor Blade Industry Overview

The United Kingdom Rotor Blade Market is semi-consolidated. Some of the key players in this market (in no particular order) are Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., Nordex SE, Orsted A/S, and Vattenfall AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Number of Offshore Wind Energy Installations

- 4.5.1.2 Increased Investments in the Wind Power Sector

- 4.5.2 Restraints

- 4.5.2.1 High Cost of Transportation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 By Blade Material

- 5.2.1 Carbon Fiber

- 5.2.2 Glass Fiber

- 5.2.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems A/S

- 6.3.2 Siemens Gamesa Renewable Energy S.A.

- 6.3.3 Nordex SE

- 6.3.4 Orsted A/S

- 6.3.5 Vattenfall AB

- 6.3.6 BayWa R.E AG

- 6.3.7 Enercon GmbH

- 6.4 Market Ranking Analysis

- 6.5 List of other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements