ドロップシッピング:世界の市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Global Dropshipping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645096

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

世界のドロップシッピング市場規模は2025年に4,100億米ドルと推定され、予測期間(2025-2030年)のCAGRは22.06%で、2030年には1兆1,200億米ドルに達すると予測されます。

同市場は、オンラインショッピングの需要の高まりと国際eコマース取引の動向の増加により、急成長が見込まれています。したがって、ドロップシッピング需要の増加は主にオンライン商取引分野の開発によるものです。

ドロップシッピングは、日進月歩の技術により、急成長している収益ビジネスのひとつです。ドロップシッピングビジネスは、eコマースやオンデマンドビジネスのパンデミックに見舞われた世界で、さまざまなイノベーションを提供しています。スマートフォンは消費者のオンラインショッピングを完全に変えました。何百ものモバイルアプリが利用できるようになり、消費者の体験はかつてないほど向上しました。

スマートフォンの普及は、消費者の可処分所得の増加と相まって、eコマースの成長を促進し、ドロップシッピングビジネスを牽引しています。eコマース業界では、オンラインショッピングプラットフォームを利用する買い物客の増加に伴い、大手企業による投資が大幅に増加しています。

エコシステムのプレイヤーの多くは、メーカー、流通業者/サプライヤー、ドロップシッピング企業、エンドユーザー/顧客です。APACのドロップシッピング業界は最も進んでいます。伝統的な流通チャネルに従う小売業者は、在庫管理に多額の投資を検討しています。

一方、eコマース・プラットフォームの利用が増えるにつれ、企業は在庫購入・管理にかかる資本コストを削減するためにドロップシッピングに目を向けています。さらに、加盟店が物流や在庫にかける費用を削減するため、ドロップシッピングの利用が増加しています。

世界のドロップシッピング市場動向

エレクトロニクス・メディア分野で大きな成長が見込まれる

エレクトロニクス・メディア分野は、他の主要経済圏のほとんどを凌ぐ急成長を続けており、最新動向に敏感な主要小売企業や主要ブランドが、エレクトロニクス企業にとって不可欠なこの成長を牽引しています。

WalmartとBest Buyが、2023年9月の家電量販店のトップでした。ウォルマートの台数シェアは33%、ベストバイは24%、アマゾンは12%だった。前年からの台数シェア増加率はウォルマートが最も大きく(1.2%)、減少率はベストバイが最も大きかった(0.9%)。

ドル・シェアでは、ベストバイが30%で家電量販店の中でトップ、次いでウォルマートが25%、アマゾンが11%。ウォルマートのドル・シェアは前年から0.8ポイント増加したが、ベスト・バイのドル・シェアは1.1ポイント減少しました。

2023年9月の販売台数では、ソニー(21%)とサムスン(18%)が家電ブランドの上位を占めました。上位ブランドの多くは販売台数シェアで前年を下回った。唯一のトップブランドであるソニーは、2021年9月から2022年9月にかけて台数シェアが1.0ポイント減少したのに続き、1.7ポイント増加しました。

2023年9月の家電製品の業界平均価格は463米ドルでした。これは平均価格が482米ドルであった昨年の同時期から減少しました。各販売店での平均消費額はさまざまです。

ベストバイの平均価格は最も低く573米ドル。Costcoは主要アウトレットの中で台数シェアと金額シェアが最も低いが、Costcoで家電製品に支払われる平均価格は他の主要アウトレットよりもかなり高いです。

2023年第2四半期、米国のトップ家電量販店ウェブサイトのランキングでは、アップル社がシェア・オブ・ボイス(オンライン市場全体に対するブランドのオンライン検索の認知度を示す指標)で1位となった。アップル社のシェアは9.2%で、アマゾン社の7.6%を上回った。ミネソタ州を拠点とし、北米を中心に展開するベスト・バイは、7%近いシェアで3位だった。アマゾンなどのオンライン大手との競合が激化しているにもかかわらず、ベスト・バイはアメリカの家電市場で独自の地位を保っています。同社は年々eコマースの存在感を高めており、2018年から2023年にかけてオンライン収益シェアを2倍以上に伸ばしています。

安定したペースで成長するアジア太平洋地域

eコマースがアジア太平洋を席巻していることは間違いないです。インターネットへのアクセスの向上と、効率的で迅速な商品の配送が相まって、世界中の消費者が買い物の習慣を実店舗からeコマースへとシフトさせています。

インターネットの普及と接続性は近年、アジア太平洋地域全体で著しく向上し、その後のデジタル化につながった。地域や地域の人々だけでなく、多くの重要な産業が、テクノロジー主導の新時代に対応するため、デジタルトランスフォーメーションを進めています。そのひとつが小売業です。小売業は常に地域全体に莫大な収益をもたらしてきたため、小売業が地域とともにデジタル化することは理にかなっていました。

この地域におけるeコマースの成長には、いくつかの要因が寄与しています。第一に、中産階級の成長と可処分所得の増加により、同地域のインターネット普及率とスマートフォン所有者数が増加しました。

第二に、世界中の消費者がインターネットに接する機会が増えたため、オフラインからオンライン・ショッピングへのシフトが自然に見られるようになった。第三に、ソーシャルメディアがアジア太平洋地域のeコマース分野の成長を促進する上で大きな役割を果たしています。

ソーシャル・プラットフォームは、消費者とオンライン小売業者を直接結びつけることで、商品を宣伝・販売する機会を活用しています。これはソーシャルコマースとして知られています。一部のソーシャル・メディア・チャンネルは、オンライン・マーケットプレースを兼ねているため、消費者は商品を購入するためにウェブサイトを離れる必要がないです。第四に、ライブコマースは一部の市場で非常に人気があります。

消費者はライブストリーミングを通じて、テレビショッピングなどの詳しい説明を受けることができます。第五に、アジア太平洋ではモバイル・コマースが増加傾向にあり、eコマース全体の売上の50%以上を占めています。

この地域のeコマース市場のトップ3は中国、日本、韓国で、世界の小売eコマースのかなりの部分を占めています。中国には、アリババ、Pinduoduo、JD.comなど、この地域でトップクラスのeコマース企業があります。

世界のドロップシッピング業界の概要

ドロップシッピング市場は競争が激しく、数多くの企業が市場シェアを争っています。ドロップシッピングは参入障壁が低く、高い利益率が見込めることから、近年人気を博しています。

ドロップシッピング市場の競争力を高めている主な要因の1つは、eコマースの台頭です。オンライン小売業者の増加に伴い、効率的で費用対効果の高い注文処理ソリューションへの需要が高まっています。小売業者が物理的に商品を在庫することなく販売できるドロップシッピングは、人気の選択肢として浮上しています。

市場の主要企業には、Shopify、AliExpress、Oberlo、SaleHoo、Dobaなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 市場を牽引する国際貿易の増加

- オンラインユーザーの増加

- 抑制要因

- 市場に影響を与える規制対応

- 市場競争の激化

- 機会

- 複合一貫輸送の拡大

- デジタル変革

- 促進要因

- バリューチェーン/サプライチェーン分析

- 技術の進歩

- 政府の規制と主な取り組み

- 需給分析

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- 玩具

- ホビー&DIY

- 家具・家電

- 食品・パーソナルケア

- エレクトロニクス&メディア

- ファッション

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ベネルクス諸国

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Shopify

- AliExpress

- Oberlo

- SaleHoo

- Doba

- Spocket

- Modalyst

- Printful

- Dropified

- Alibaba

- その他の企業

第7章 市場の将来

第8章 付録

目次

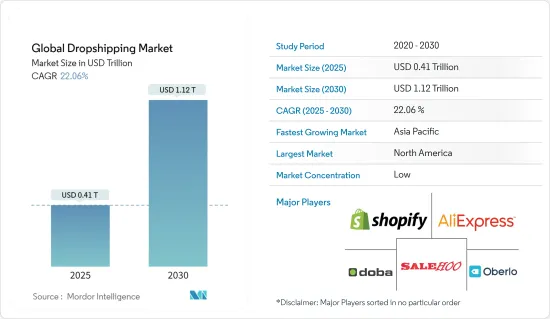

The Global Dropshipping Market size is estimated at USD 0.41 trillion in 2025, and is expected to reach USD 1.12 trillion by 2030, at a CAGR of 22.06% during the forecast period (2025-2030).

The market is expected to grow rapidly due to the growing demand for online shopping and the increasing trend of international e-commerce transactions. Therefore, the increase in dropshipping demand is mainly due to the development of the online commerce sector.

Dropshipping is one of the fastest-growing profit-making businesses due to the ever-evolving technology. Dropshipping businesses offer innovation in many different ways in the pandemic-stricken world of e-commerce and on-demand businesses. Smartphones have completely changed the way consumers shop online. The consumer experience has never been better with hundreds of mobile apps available.

The growing popularity of smartphones, combined with the growing disposable income of consumers, is driving the growth of e-commerce, which in turn is driving the dropshipping business. The e-commerce industry has seen a significant rise in investments by the leading players due to the growing number of shoppers turning toward online shopping platforms.

Most of the ecosystem's players are manufacturers, distributors/suppliers, dropshipping companies, and end-users/customers. The dropshipping industry in APAC is the most advanced. Retailers following traditional distribution channels are looking to invest heavily in inventory control.

On the other hand, companies are turning to dropshipping to reduce capital costs for inventory purchasing/management as the use of e-commerce platforms increases. Furthermore, as merchants are spending less on logistics and inventory, the use of dropshipping is increasing.

Global Dropshipping Market Trends

Immense Growth is Projected for the Electronics and Media Segment

The electronics and media segment continues to grow faster than almost all other major economies, and staying on top of the latest trends, leading retailers and leading brands are driving this growth, which is essential for any electronics company.

Walmart and Best Buy were the top Consumer Electronics retailers in September 2023. Walmart had a 33% unit share, while Best Buy had a 24% unit share, and Amazon had a 12% unit share. Walmart had the largest increase in unit share from the previous year (1.2%), while Best Buy had the largest decrease (0.9%).

Best Buy leads the Consumer Electronics retailers in dollar share at 30%, followed by Walmart at 25% and Amazon at 11%. Walmart increased in dollar share by 0.8 points from the previous year, while Best Buy decreased by 1.1 points in dollar share purchases.

Sony (21%) and Samsung (18%) were the top Consumer Electronics brands in terms of units sold in September 2023. Many of the top brands decreased year-on-year in terms of unit share. The only leading brand, Sony, saw a 1.7 percentage point increase in unit share, following a 1.0 percentage point decrease in unit share from September 2021 to September 2022.

The industry average price for Consumer Electronics in September 2023 was USD 463. This was a decrease from the same time last year when the average price was USD 482. The average amount spent at each outlet varies. Below are some outlet pricing insights: Costco has the highest average price at USD 728.

Best Buy has the lowest average price at USD 573. While Costco has the lowest unit and dollar shares among leading outlets, the average price paid for consumer electronics at Costco is significantly higher than that of other leading outlets.

In the Q2 2023 rankings of top electrical retail websites in the United States, Apple Inc. ranked first by share of voice (a measure of a brand's online search visibility relative to the entire online market). Apple's brand had a 9.2% share of voice, compared to Amazon's 7.6%. Best Buy, based in Minnesota and mostly in North America, was in third place with a nearly 7% share of voice. Despite growing competition from online giants such as Amazon, Best Buy has held its own in the American electronics market. The company has grown its e-commerce presence over the years, more than doubling its online revenue share from 2018 to 2023.

Asia-Pacific is growing at a steady pace

There is no doubt that e-commerce has taken over Asia-Pacific. Better internet access combined with efficient and fast delivery of goods has caused consumers around the world to shift their shopping habits from physical to e-commerce.

Internet penetration and connectivity have increased significantly across the region in recent years, leading to subsequent digitalization. In addition to the region and the people of the region, many important industries have gone through digital transformation to stay up-to-date with the new technology-driven era. One of these industries is retail. Since the retail sector has consistently generated huge revenue for the region as a whole, it only made sense that the retail industry would digitalize with the region.

Several factors have contributed to the growth of e-commerce in the region. Firstly, the growth of the middle class, coupled with the increase in disposable income, has led to an increase in internet penetration and the number of smartphone owners in the region.

Secondly, as consumers around the world have been exposed to the internet more, the shift from offline to online shopping seems natural. Thirdly, social media has played a major role in driving the growth of the E-commerce sector in Asia-Pacific.

Social platforms have taken advantage of the opportunity to promote and sell products by directly connecting consumers with online retailers. This is known as social commerce. Some social media channels also double as online marketplaces, so consumers do not have to leave the website to buy goods. Fourthly, live commerce is very popular in some markets.

Consumers are able to get detailed explanations, such as TV shopping, through live streaming. Fifthly, mobile commerce is on the rise in Asia-Pacific, accounting for more than 50% of total E-commerce sales.

The top three e-commerce markets in the region are China, Japan, and South Korea, which account for a significant portion of global retail e-commerce. China is home to some of the top e-commerce firms in the region, including Alibaba, Pinduoduo, and JD.com.

Global Dropshipping Industry Overview

The drop shipping market is highly competitive, with numerous players vying for market share. Drop shipping has gained popularity in recent years due to its low entry barriers and potential for high-profit margins.

One of the key factors driving the competitiveness of the drop shipping market is the rise of e-commerce. With the increasing number of online retailers, there is a growing demand for efficient and cost-effective order fulfillment solutions. Drop shipping, which allows retailers to sell products without physically stocking them, has emerged as a popular choice.

The major players in the market include Shopify, AliExpress, Oberlo, SaleHoo, Doba, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing International Trade Driving the Market

- 4.2.1.2 Increasing online users driving the market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory Compliance Affecting the Market

- 4.2.2.2 High Competition in the Market

- 4.2.3 Opportunities

- 4.2.3.1 Expansion of Intermodal Connectivity Driving the Market

- 4.2.3.2 Digital Transformation Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Technological Advancements

- 4.5 Government Regulations and Key Initiatives

- 4.6 Demand-Supply Analysis

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Toys

- 5.1.2 Hobby & DIY

- 5.1.3 Furniture & Appliances

- 5.1.4 Food & Personal Care

- 5.1.5 Electronics & Media

- 5.1.6 Fashion

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Benelux Countries

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Shopify

- 6.2.2 AliExpress

- 6.2.3 Oberlo

- 6.2.4 SaleHoo

- 6.2.5 Doba

- 6.2.6 Spocket

- 6.2.7 Modalyst

- 6.2.8 Printful

- 6.2.9 Dropified

- 6.2.10 Alibaba*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日