欧州のヘルスケアコールドチェーンロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Healthcare Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645080

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

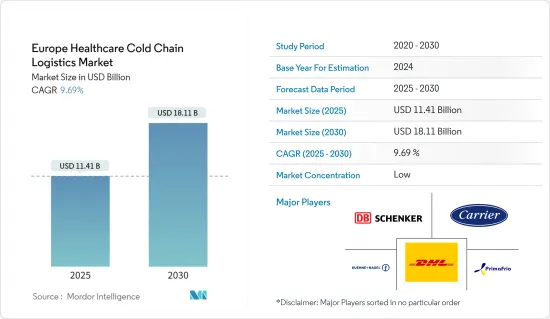

欧州のヘルスケアコールドチェーンロジスティクス市場規模は2025年に114億1,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは9.69%で、2030年には181億1,000万米ドルに達すると予測されます。

バイオ医薬品ワクチンや先端治療薬の開発・生産の急増、技術の進歩、研究開発に対するこの地域の関心が、市場の成長に大きく寄与しています。

COVID-19パンデミックの際、製薬業界は最も影響を受けた分野のひとつであり、世界中でワクチンと解毒剤の生産と供給が増加しました。米国運輸省は、2021年に港湾・水路のインフラ整備を目的とした「港湾インフラ開発プログラム」に基づき、約6億5,300万米ドルの助成金を受け取る41のプロジェクトを選定しました。旅程中、特別な温度条件が必要とされる医薬品やその他の医療製品のための港湾における温度管理された保管施設の改善は極めて重要でした。

欧州医療機関が承認する医薬品は年間平均38品目であり、バイオ医薬品の開発が増加していることを示しています。規制遵守と患者の安全がメーカーの最大の関心事であるため、バイオ医薬品分野の成長には、製品の保管と供給に高度な要件が求められます。

2023年、ドイツは国民1人当たり8,011米ドルを医療に費やし、これはGDPの約12.7%に相当します。また、ヘルスケア製品の最大級の生産国および輸出国でもあります。

欧州のヘルスケアコールドチェーンロジスティクス市場動向

OTC医薬品の消費は大幅な成長が予測される

欧州では、パンデミック(世界的大流行)の間、消費者の健康意識が顕著に高まりました。人々に力を与え、ヘルスケアへのアクセス方法を改善することで、セルフケアはこうした課題に対応できる可能性を秘めています。欧州のヘルスケアコールドチェーンロジスティクスの成長は、こうした理由によるものです。

人々は自分の健康を管理する方法を積極的に探しており、それがセルフケアやOTC医薬品の需要の伸びにつながっています。その結果、eコマース・プラットフォームの開発により、欧州におけるOTC医薬品の消費は消費者にとってより身近なものとなった。このセグメントの成長は、個人が電子プラットフォームを通じてヘルスケア製品を購入する利便性に起因しています。業界専門家によると、2023年のOTC医薬品消費額は2022年の504億6,000万米ドルから527億2,000万米ドルに増加し、2024年には547億9,000万米ドルに達すると予測されています。

地域全体の政府も市場プレイヤーを支援しています。例えば、2023年11月、スウェーデン政府は、オピオイドの過剰摂取を逆転させるナロキソンスプレーの使用を拡大しました。鎮痛、咳・風邪、アレルギー、消化器疾患など、一般的な病気に対する幅広い医薬品を提供するため、欧州の製薬企業はOTC製品のポートフォリオを拡大しています。その結果、厳格で効率的なコールドチェーン物流システムがますます求められています。

ドイツが医薬品生産をリード

2022年、ドイツにおける医薬品生産は374億ユーロ(403億1,000万米ドル)で最高と評価されました。2023年11月に発表されたStrategy 4.0によると、ドイツ政府はドイツの製薬産業の条件を改善するための多くの改革を盛り込んだ新たな製薬戦略についても議論しています。

医薬品生産が増加している背景には、慢性疾患の増加があり、病気の予防やセルフメディケーションが重視されるようになっています。加えて、OTC医薬品の使用増加も同国の成長を牽引しています。

加えて、研究開発に対する政府の支援が医薬品開発のスピードアップに役立っています。Eurostatが発表した2023年の記事によると、2022年にはEU全体で、研究開発のための政府予算配分(GBARD)総額は1,173億7,000万ユーロ(1,265億2,000万米ドル)で、GDPの0.74%に相当します。2021年と比較すると5.4%の増加です。

欧州のヘルスケアコールドチェーンロジスティクス業界の概要

欧州のヘルスケアコールドチェーンロジスティクス市場は、さまざまな企業が存在するため競争が激しいです。欧州のヘルスケアコールドチェーンロジスティクス業界は、専門的なインフラ、温度管理された保管施設、厳格な規制要件の遵守が必要なため、参入障壁が高い可能性があります。効率的に競合を勝ち抜くためには、新規参入企業は技術、専門知識、設備に多額の投資を行う必要があります。新規参入企業は、適正流通規範(GDP)ガイドラインなど、厳しい規制やコンプライアンス基準という課題に直面します。企業が競争力を維持するために用いる主な成長戦術は、技術の統合、世界のネットワークの拡大、冷蔵センターの近代化です。欧州のヘルスケアコールドチェーンロジスティクス市場のプレーヤーは、DBシェンカーやRhenus Logisticsなどドイツに本社を置く企業が数社あります。DHL International GmbhとKuehne+Nagelは、この分野で最も重要な企業のひとつです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- 業界のバリューチェーン分析

- 政府の規制と取り組み

- 環境・温度管理された保管庫への注目

- 冷蔵倉庫で使用される冷媒と包装材料に関する洞察

- COVID-19が市場に与える影響

第5章 市場力学

- 促進要因

- ワクチン流通への注目の高まり

- 製薬・バイオ産業の成長

- 抑制要因

- 高い初期設備投資

- 温度異常のリスク

- ビジネスチャンス

- ヘルスケアにおけるeコマースの成長

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 製品別

- バイオ医薬品

- ワクチン

- 臨床試験材料

- サービス別

- 輸送

- 保管

- 付加価値サービス(包装・ラベリング)

- エンドユーザー別

- 病院、クリニック、医薬品

- バイオ医薬品

- バイオテクノロジー

- 国別

- ドイツ

- フランス

- スペイン

- その他欧州

第7章 競合情勢

- 企業プロファイル

- Carrier Transicold

- Primafrio

- Alloga

- Kuehne+Nagel

- Cavalier Logistics

- Marken Ltd

- Biocair

- DB Schenker

- DHL

- Envirotainer*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

目次

The Europe Healthcare Cold Chain Logistics Market size is estimated at USD 11.41 billion in 2025, and is expected to reach USD 18.11 billion by 2030, at a CAGR of 9.69% during the forecast period (2025-2030).

A surge in the development and production of biopharmaceutical vaccines and advanced therapies, technological advancement, and the region's interest in R&D have contributed significantly to the market's growth.

During the COVID-19 pandemic, the pharmaceutical industry was one of the most affected sectors, witnessing increased production and supply of vaccines and antidotes worldwide. The United States Department of Transport selected 41 projects to receive around USD 653 million in grants under the Port Infrastructure Development Programme for infrastructure spending for ports and waterways in 2021. Improved temperature-controlled storage facilities at ports for pharmaceutical and other medical products, which require special temperature conditions throughout their journey, were crucial.

The European Medical Agency approves an average of 38 drugs annually, depicting an increase in the development of biopharmaceuticals. The growth in the biopharmaceuticals sector demands advanced requirements for the storage and supply of the products, as regulatory compliance and patient safety are manufacturers' primary concerns.

In 2023, Germany spent USD 8,011 per capita on health, approximately 12.7% of GDP. It is also one of the largest producers and exporters of healthcare products.

Europe Healthcare Cold Chain Logistics Market Trends

The OTC Pharmaceuticals Consumption is Projected to Grow Significantly

A notable increase in health awareness among consumers in Europe has been noticed during the pandemic. By empowering people and making better ways of accessing healthcare, self-care has the potential to meet these challenges. The growth of European healthcare cold chain logistics is a result of these reasons.

People are looking proactively for ways to manage their health, which has led to a growth in the demand for self-care and OTC pharmaceuticals. Consequently, OTC pharmaceutical consumption in Europe has become more accessible to consumers as a result of the development of e-commerce platforms. The growth of this segment can be attributed to the convenience of individuals buying healthcare products through electronic platforms. As per industry experts, in 2023, OTC pharmaceuticals consumption increased from USD 50.46 billion in 2022 to USD 52.72 billion in 2023 and is projected to reach USD 54.79 billion in 2024.

Governments across the region are also supporting market players. For instance, in November 2023, the Swedish Government expanded the use of naloxone spray that reverses opioid overdose. To offer a wider range of medicines for common illnesses such as pain relief, cough and cold, allergies, digestive disorders, and more, pharmaceutical companies in Europe are expanding their OTC product portfolio. As a result, stringent and efficient cold chain logistics systems are increasingly in demand.

Germany is Set to Lead Pharmaceuticals Production

In 2022, pharmaceutical production in Germany was valued at its highest at EUR 37.4 billion (USD 40.31 billion). According to Strategy 4.0, published in November 2023, the German Government is also discussing a new Pharma Strategy with a number of reforms to improve the conditions for the pharmaceutical industry in Germany.

The increase in pharmaceutical production is due to the growing instances of chronic diseases and increased emphasis on prevention and self-medication for disease. In addition, the country's growth has been driven by an increase in the use of OTC medicines.

In addition, government support for research and development helps speed up the development of medicines. In 2022, according to a 2023 article published by Eurostat, across the EU, the total government budget allocations for R&D (GBARD) stood at EUR 117.37 billion (USD 126.52 billion), equivalent to 0.74% of GDP. An increase of 5.4% compared with 2021.

Europe Healthcare Cold Chain Logistics Industry Overview

The market for healthcare cold chain logistics in Europe is competitive, owing to the presence of various companies. The healthcare cold chain logistics industry in Europe may have high barriers to entry due to the need for specialized infrastructure, temperature-controlled storage facilities, and compliance with stringent regulatory requirements. To be competitive efficiently, newcomers would need to invest significantly in technology, expertise, and facilities. New entrants face the challenge of stringent regulations and compliance standards, including guidelines on Good Distribution Practice (GDP) guidelines. The primary growth tactics used by businesses to maintain their competitiveness are the integration of technologies, worldwide network expansion, and modernization of cold storage centers. Several European healthcare cold chain logistics market players are headquartered in Germany, such as DB Schenker and Rhenus Logistics. DHL International Gmbh and Kuehne + Nagel are among the most important players in this sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Spotlight on Ambient/Temperature-controlled Storage

- 4.6 Insights into Refrigerants and Packaging Materials Used in Refrigerated Warehouses

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increasing Focus on Vaccine Distribution

- 5.1.2 Growing Pharmaceutical and Biotechnology Industries

- 5.2 Restraints

- 5.2.1 High Initial Capital Investment

- 5.2.2 Risk of Temperature Excursions

- 5.3 Opportunities

- 5.3.1 E-commerce Growth in Healthcare

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Biopharmaceuticals

- 6.1.2 Vaccines

- 6.1.3 Clinical Trial Materials

- 6.2 By Services

- 6.2.1 Transportation

- 6.2.2 Storage

- 6.2.3 Value Added Services (Packaging and Labeling)

- 6.3 By End User

- 6.3.1 Hospitals, Clinics and Pharmaceuticals

- 6.3.2 Biopharmaceutical

- 6.3.3 Biotechnology

- 6.4 By Country

- 6.4.1 Germany

- 6.4.2 France

- 6.4.3 Spain

- 6.4.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Carrier Transicold

- 7.2.2 Primafrio

- 7.2.3 Alloga

- 7.2.4 Kuehne + Nagel

- 7.2.5 Cavalier Logistics

- 7.2.6 Marken Ltd

- 7.2.7 Biocair

- 7.2.8 DB Schenker

- 7.2.9 DHL

- 7.2.10 Envirotainer*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日