|

市場調査レポート

商品コード

1645046

北米の浮体式洋上風力発電:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)North America Floating Offshore Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の浮体式洋上風力発電:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

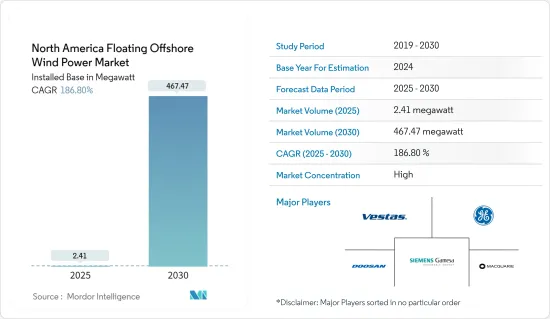

北米の浮体式洋上風力発電の市場規模は、設置ベースで2025年の2.41メガワットから2030年には467.47メガワットに成長し、予測期間(2025~2030年)のCAGRは186.8%になると予測されます。

主なハイライト

- 中期的には、洋上風力発電の需要拡大と二酸化炭素排出量削減のための国際的なコミットメントが、予測期間中の調査対象市場の成長を促進すると予想されます。

- その一方で、ガスや太陽光発電を中心としたクリーンな代替電源の採用が増加していることが、予測期間中の浮体式洋上風力発電の成長を妨げると予想されます。

- とはいえ、浮体式洋上風力発電における技術革新と最新技術の適応は、予測期間中に浮体式洋上風力発電市場にチャンスをもたらすと思われます。

- 米国が市場を独占しており、予測期間中に最も高いCAGRで推移する可能性が高いです。

北米の浮体式洋上風力発電市場動向

重要なセグメントとしての深海

- 深海での浮体式洋上風力発電技術は、最も経済的に実行可能な技術です。さらに、米国における洋上風力発電の技術的資源の大半は、水深60m以深にあります。

- 浮体式洋上風力発電技術の設計は、比較的浅い喫水と風車設置後の流体力学的安定性です。その他の利点としては、水深に左右されないこと(30m以上)、設置に適した天候の幅が広いこと、海底の土質条件に左右されないこと、比較的安価でシンプルな係留システム、設置・撤去がシンプルであること、ヒーブプレートによる移動が最小限であること、全体的にリスクが低いことなどが挙げられます。

- 浮体式深海洋上風力発電プロジェクトには、陸上ウィンドファームよりも多くの利点があります。洋上では風速が速く一定しており、周辺に地面がないため支障が少ないです。

- 国際再生可能エネルギー機関(International Renewable Energy Agency)の再生可能エネルギー容量2023年のデータによると、2022年の風力発電設備容量は1520万kWに達し、2021年の1400万kWから増加しました。

- 米国とカナダはともに、沿岸と深海の沖合に大きな面積を持つため、浮体式洋上風力発電の設備容量に適しています。アトランティック・カナダのノヴァ・スコシアにあるセーブル島銀行は、1年間に最大7万ギガワット時の電力を生産することが可能で、カナダが2050年に掲げるネット・ゼロの目標達成に貢献します。

- 同様に、洋上風力資源は、2050年までに米国の電力の4分の1を発電するのに十分なほど豊富です。2023年、米国はロードアイランド沖とバージニア沖に2つの小規模な風力発電所を建設しました。2023年6月、マサチューセッツ州マーサズ・ヴィンヤード沖に同国初の商業規模の風力発電所が建設されました。

- したがって、上記の点から、予測期間中は深海セグメントが市場を独占することになります。

米国が市場を独占する見込み

- 米国の風力発電部門は、国内エネルギー生産を促進することを目的としたアメリカ・ファースト政策により、政府から絶大な支援を受けています。浮体式洋上風力発電分野は、同国がリース可能な広大な沿岸地域を有していることから、主要な開発分野とみなされています。

- 米国は風力発電の総設備容量で第2位の国であり、2022年には140.1GWの容量を記録し、北米における風力発電の総設備容量の80%以上を占めました。

- Energy Institute Statistical Review of World Energy 2023のデータによると、風力発電による発電量は439.2テラワット時に達し、2021年より増加しています。

- 米国は、約4万5000メガワットの洋上風力発電の調達目標を設定しています。さらに、12件の洋上風力発電プロジェクトの開発により、2026年までに約10.3GWの洋上風力発電が見込まれています。こうした政府の取り組みは、予測期間中に浮体式洋上風力発電市場を拡大させる可能性が高いです。

- 国際再生可能エネルギー機関の再生可能エネルギー容量2023年のデータによると、洋上風力発電の容量は2022年に42MWに達しました。

- したがって、上記の点から、米国は予測期間中に浮体式洋上風力発電市場で大きな成長を遂げると予想されます。

北米の浮体式洋上風力発電産業の概要

北米の浮体式洋上風力発電市場は適度に断片化されています。この市場の主要企業(順不同)には、Vestas Wind Systems AS、General Electric Company、Siemens Gamesa Renewable Energy SA、Doosan Heavy Industries &Construction、Macquarie Groupなどがいます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 設置容量と2028年までの予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- カーボンフリー発電源の採用

- 有利な政府政策

- 抑制要因

- 代替再生可能エネルギーとの厳しい競合

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 水深別(定性分析のみ)

- 浅海(水深30m未満)

- 移行帯水域(水深30m~60m)

- 深海(水深60m以上)

- 地域

- 米国

- カナダ

- メキシコ

第6章 競争情勢

- 合併、買収、提携、合弁事業

- 主要企業の戦略

- 企業プロファイル

- vestas wind systems a/s

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- Doosan Heavy Industries & Construction

- Macquarie Group

- Equinor ASA

第7章 市場機会と今後の動向

- 超深海洋上風力発電所の変電所プラットフォームの開発

The North America Floating Offshore Wind Power Market size in terms of installed base is expected to grow from 2.41 megawatt in 2025 to 467.47 megawatt by 2030, at a CAGR of 186.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing demand for offshore wind power coupled with international commitments to reduce carbon emissions are expected to drive the growth of the market studied during the forecast period.

- On the other hand, increasing adoption of alternate sources of clean power generation, mainly gas and solar power, are expected to hinder the growth of Floating Offshore wind power during the forecast period.

- Nevertheless, technological innovation and adaptation of the latest technologies in Floating Offshore wind power are likely to create opportunities for the Floating Offshore wind power market in the forecast period.

- The United States dominates the market and is also likely to witness the highest CAGR during the forecast period.

North America Floating Offshore Wind Power Market Trends

Deep Water as a Significant Segment

- Deepwater floating offshore wind power technology is the most economically viable technology because, at these depths, the cost of deployment of fixed-base structures is prohibitively high. Additionally, most of the total technical offshore wind resources in the United States lie over water depths greater than 60 m.

- Floating offshore wind power technology design is a relatively shallow draft and hydrodynamic stability after wind turbine installation. Other benefits include depth independence (above 30 meters), broad weather window for installation, insensitivity to subsea soil conditions, relatively cheap and simple mooring systems, simple installation and decommissioning, minimal level of movement due to heave plates, and overall lower risk.

- Floating deepwater offshore wind power projects offer more advantages than onshore wind farms. The wind speeds are higher and constant in the offshore regions, and the areas offer fewer hindrances due to no ground nearby in the vicinity.

- According to the International Renewable Energy Agency Renewable Energy Capacity 2023 data, the installed wind power capacity reached 15.2 GW in 2022, increasing from 14 GW in 2021.

- Both the United States and Canada offer significant coastal and deepwater offshore areas, thus providing excellent floating offshore wind power capacities. The Sable Island Bank in Nova Scotia, Atlantic Canada, could churn up to 70,000 Gigawatt-hours of electricity in a year, thus helping Canada reach its goal of net zero in 2050.

- Similarly, offshore wind resources are plentiful enough to generate up to a quarter of the United States' electricity by 2050, thus helping the country meet its global climate goals. In 2023, the United States had two small wind farms off the Rhode Island and Virginia coasts. The country's first commercial-scale wind farm off Martha's Vineyard was constructed on the foundations, Massachusetts, in June 2023.

- Hence, due to the above points, the deep water segment will dominate the market during the forecast period.

United States Expected to Dominate the Market

- The wind power sector in the United States is receiving immense support from the government due to the America First policy, which aims to boost domestic energy production. The floating offshore wind power sector is considered a major development area, as the country has a large coastal area available for leasing.

- The United States was the second-largest country in terms of total installed wind energy capacity, recording 140.1 GW of capacity in 2022, or more than 80% of the total wind energy capacity in North America.

- According to the Energy Institute Statistical Review of World Energy 2023 data, the electricity generation from wind power reached 439.2 terawatt-hours, increasing from 2021.

- The United States has established nearly 45,000 MW of offshore wind procurement targets. Additionally, around 10.3 GW of offshore wind energy is expected by 2026, with the development of 12 offshore wind energy projects. Such government initiatives are likely to increase the floating offshore wind power market during the forecast period.

- According to the International Renewable Energy Agency Renewable Energy Capacity 2023 data, the offshore wind power capacity reached 42 MW in 2022.

- Hence, owing to the above points, the United States is expected to see significant growth in the Offshore Floating wind power market during the forecast period.

North America Floating Offshore Wind Power Industry Overview

The North American Offshore Floating wind power market is moderately fragmented. Some of the key players in this market (in no particular order) include Vestas Wind Systems AS, General Electric Company, Siemens Gamesa Renewable Energy SA, Doosan Heavy Industries & Construction, and Macquarie Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Adoption of Carbon Free Electricity Generation Sources

- 4.5.1.2 Favorable Government Policies

- 4.5.2 Restraints

- 4.5.2.1 Tough Competition from Alternative renewable energy sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water ( less than 30 m Depth)

- 5.1.2 Transitional Water (30 m to 60 m Depth)

- 5.1.3 Deep Water (higher than 60 m Depth)

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 vestas wind systems a/s

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy SA

- 6.3.4 Doosan Heavy Industries & Construction

- 6.3.5 Macquarie Group

- 6.3.6 Equinor ASA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developing Ultradeep water Offshore Wind farm Substation Platform