南米の空気絶縁開閉装置:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

South America Air Insulated Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644975

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

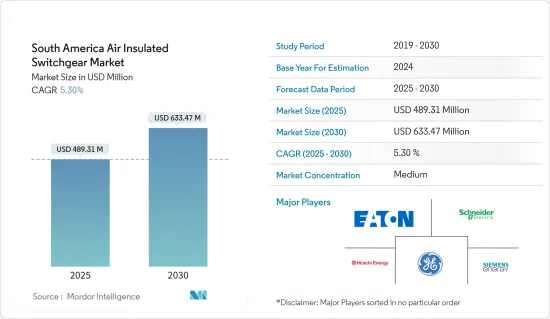

南米の空気絶縁開閉装置市場規模は2025年に4億8,931万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.3%で、2030年には6億3,347万米ドルに達すると予測されます。

主なハイライト

- 中期的には、トランスミッションと配電インフラへの投資の増加が、予測期間中の空気絶縁開閉装置の需要を牽引すると予想されます。

- 一方、空気絶縁開閉装置の変電所は高いメンテナンスが必要であるため、ガス絶縁開閉装置(GIS)が空気絶縁開閉装置の代替として採用され、運用コストが高くなることが、予測期間中の市場成長を抑制する可能性が高いです。

- とはいえ、再生可能エネルギー分野への投資の拡大と電力インフラの老朽化は、今後数年間、市場関係者に大きなビジネスチャンスをもたらすと予想されます。

南米の空気絶縁開閉装置市場動向

高電圧セグメントが著しい成長を遂げる

- 36kV以上の電圧を扱う電力システムは高圧スイッチギヤと呼ばれます。電圧レベルが高いため、スイッチング動作中に発生するアーク放電も非常に大きくなります。そのため、高圧開閉装置の設計には特別な注意が必要です。高圧サーキットブレーカは、高圧スイッチギヤの主要コンポーネントです。したがって、高圧サーキットブレーカ(CB)には、安全で信頼性の高い動作のための特別な機能が必要です。

- このスイッチギヤは、風力タービン、電気モーター、発電機、太陽光発電、住宅配電、電力供給システム、環境に配慮した設置、地下駅、鉄鋼、製紙、鉱業、増加する海洋用途など、さまざまな産業で使用されています。しかし、このセグメントの主な用途は、世界中で近代化・建設が進められている大規模なトランスミッションと配電ネットワークに由来します。

- また、高電圧直流(HVDC)プロジェクトの増加は、大規模プロジェクトによる市場の成長を助けると期待されています。2021年10月、チリ政府はチリ初の長距離HVDC送電線の建設と運用のための入札を発表しました。この送電線は1,500kmの600kV送電線で構成され、3,000MWの容量が見込まれ、アントファガスタ地域のキマル変電所とメトロポリタン地域のロ・アギーレ間を結ぶ。このプロジェクトの費用は25億米ドルです。

- さらにアルゼンチンは、2025年までに電力の20%を再生可能エネルギーで賄うという目標を掲げており、2021年現在のシェア約11.27%から大幅に増加します。2022年、アルゼンチンの発電量は150.8TWhに達します。

- 同様に、チリ政府は2019年に脱石炭計画を発表し、2040年までに5.5GWの石炭火力発電容量を完全に停止することを目指しています。その目標は、2035年までに再生可能エネルギーの割合を60%にし、2050年までにさらに70%にすることです。

- 結論として、この地域は、発電ミックスの多様化の進展、送配電部門への投資、電力部門の開発により、空気絶縁開閉装置市場にとって大きな可能性を秘めています。

市場を独占すると予想されるブラジル

- ブラジルは間違いなく南米最大の電力市場のひとつです。2021年1月現在、ブラジルは8,500万を超える住宅、商業、工業用消費者に電力を発電・配給しており、これは他の南米諸国が生産する電力の合計よりも多いです。

- ブラジルは長年にわたり、発電能力とトランスミッション、配電網の著しい成長を目の当たりにしてきたが、これは電力需要の増大と政府の目覚ましい努力によるものです。他の市場と同様、ブラジルの空気絶縁開閉装置市場も、国内の電力インフラの開拓に依存しています。

- ブラジルのエネルギー調査会社(EPE)の2019~2029年のエネルギー拡張計画(PDE)は、再生可能エネルギー源が引き続き同国の優先事項であることを示しており、2029年にブラジルのエネルギーミックスで48%の再生可能エネルギーの達成を目指しています。国際再生可能エネルギー機関(IRENA)によると、2022年のブラジルの再生可能エネルギー設備容量は1億7526万kWに達します。

- さらに、2026年に予定されているアングラ3発電所の運転開始により、原子力エネルギーも成長します。さらに、石油・ガスなどの非再生可能エネルギー源は、今後もブラジルのエネルギー供給に重要な役割を果たすと思われます。

- 2022年6月、国家電気エネルギー庁(ANEEL)と電気エネルギー商業化会議所(CCEE)は、29の再生可能エネルギー・プロジェクトに対する新エネルギー・オークションを開始し、約70億BRL(13億3,000万米ドル)の投資を見込んでいます。プロジェクトは約947MWと予測され、3つの市場販売会社(Cemig、Coelba、Light)の需要を満たすため、2026年から2045年の間に全国連系システムに接続される予定です。

- さらに、トランスミッションと配電セグメントへの投資の増加は、この地域における空気絶縁開閉装置の需要増につながると予想されます。2021年9月、Elecnor do Brazilの子会社であるElecnorは、ミナスジェライス州の太陽光発電所から全国連系システムに至る200kmのトランスミッションの建設を発表しました。最初の区間はジャナウバ市とジャイバ市に伸びる。この送電線は93キロの230キロボルト二重回路送電線となります。第2区間は、ピラポラとトレス・マリアスを112キロの345キロボルト単相送電線で結ぶ。このトランスミッションの総容量は160万kWで、総工費は約1,850万ユーロ(2,183万米ドル)と見積もられています。

- 国際貿易局(ITA)によると、2029年までにブラジルの送電部門への投資総額は220億米ドルに達すると予測されており、その内訳は送電線が150億米ドル、変電所が70億米ドルとなっています。さらに、配電部門にはすでに年間約22億米ドルが投資されており、そのうち69%が拡張、19%が改善、12%が配電網の更新に充てられています。

- このことは、ブラジルの送電・配電部門の開発と改善をさらに後押しし、ひいてはブラジルの空気絶縁開閉装置市場の成長を促進することになります。

南米の空気絶縁開閉装置産業の概要

南米の空気絶縁開閉装置市場は半固体化しています。主要企業(順不同)としては、Schneider Electric SE、Siemens AG、Hitachi ABB Power Grids Ltd、General Electric Company、Eaton corporationなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- トランスミッションと配電インフラへの投資の増加

- 抑制要因

- 空気絶縁開閉装置に代わるガス絶縁開閉装置(GIS)の採用増加

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 電圧別

- 低電圧

- 中電圧

- 高電圧

- エンドユーザー別

- 商業および住宅

- 電力会社

- 産業部門

- 国別

- ブラジル

- アルゼンチン

- その他南米

第6章 競争情勢

- 合併、買収、提携、合弁事業

- 主要企業の戦略

- 企業プロファイル

- Hitachi ABB Ltd

- Schneider Electric SE

- General Electric Company

- Eaton Corporation PLC

- Toshiba Corp.

- Mitsubishi Electric Corporation

- Siemens Energy AG

- Hyosung Heavy Industries Corp.

- Bharat Heavy Electricals Limited

- Powell industries Inc

第7章 市場機会と今後の動向

- 再生可能エネルギー分野への投資拡大と電力インフラの老朽化

目次

Product Code: 5000148

The South America Air Insulated Switchgear Market size is estimated at USD 489.31 million in 2025, and is expected to reach USD 633.47 million by 2030, at a CAGR of 5.3% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing investments in transmission and distribution infrastructure are expected to drive the demand for air-insulated switchgear during the forecast period.

- On the other hand, the adoption of gas-insulated switchgear (GIS) as an alternative to air-insulated switchgear, as air-insulated switchgear substations require high maintenance, thus leading to high operational costs, which is likely to restrain the market growth during the forecast period.

- Nevertheless, growing investments in the renewable energy sector and the aging power infrastructure are expected to offer huge business opportunities for the market players in the coming years.

South America Air Insulated Switchgear Market Trends

High Voltage Segment to Witness Significant Growth

- The power system that deals with voltage above 36kV is referred to as high voltage switchgear. As the voltage level is high, the arcing produced during the switching operation is also very high. So, special care is to be taken while designing high-voltage switchgear. The high-voltage circuit breaker is the main component of high voltage switchgear. Hence high voltage circuit breakers (CB) should have special features for safe and reliable operation.

- This switchgear has multiple usages across industries such as wind turbines, electrical motors, generators, solar power generation, residential power distribution, power supply systems, environmentally sensitive installation, underground stations, steel, paper, and mining industry, and a growing number of marine applications. But the main application of the segment comes from large transmission and distribution networks being modernized and built across the globe.

- Also, the growing high-voltage direct current (HVDC) projects are expected to aid the growth of the market with large projects, in October 2021, the Chilean government announced a tender for the construction and operation of Chile's first long-distance HVDC power line. The power line consists of a 1,500 km 600 kV power line that is expected to have a capacity of 3,000 MW and run between the Kimal substation in the Antofagasta region and Lo Aguirre in the Metropolitan region. This cost of the project is USD 2.5 billion.

- Furthermore, Argentina has set a goal to generate 20% of its electricity from renewable sources by 2025, a significant increase from the current share of approximately 11.27% as of 2021. In 2022, Argentina's electricity generation reached 150.8 TWh.

- Similarly, Chile's government presented a coal-phase-out plan in 2019 that aims to completely turn off its 5.5 GW of coal-fired generation capacity by 2040, with 1.04 GW set to retire by 2025, which is expected to be replaced through renewable additions, storage technology, and low-emission natural gas plants. Their objective is to achieve a 60% share of renewable energy by 2035 and further increase it to 70% by 2050.

- In conclusion, the region has a significant potential for the air-insulated switchgear market owing to increasing diversification of the electricity generation mix, investments in the transmission and distribution sector, and developments in the power sector.

Brazil Expected to Dominate the Market

- Brazil is unarguably one of the largest electricity markets in South America. As of January 2021, Brazil generates and distributes electricity to over 85 million residential, commercial, and industrial consumers, more than all the combined power produced by other South American nations.

- Over the years, the country has witnessed significant growth in the electricity generation capacity and the transmission and distribution network, which can be attributed to the country's growing electricity demand coupled with remarkable efforts from the government. Much like the rest of the market, the air-insulated switchgear market in the country depends on the development of the electricity infrastructure in the country.

- The Brazilian Energy Research Company's (EPE) Energy Expansion Plan (PDE) for 2019-2029 indicates that renewable sources will remain a priority for the country, aiming to achieve 48% renewables in Brazils energy mix in 2029. According to International Renewable Energy Agency (IRENA), in 2022, Brazil's installed renewable capacity reached 175.26 GW.

- Furthermore, nuclear energy is also set to grow with the Angra 3 power plant's entry into operation, estimated for 2026. Additionally, non-renewable sources such as oil and gas will continue to play a vital role in the energy supply for the country.

- In June 2022, the National Electric Energy Agency (ANEEL) and the Electric Energy Commercialization Chamber (CCEE) commenced a new energy auction for 29 renewable energy projects, expecting an investment of around BRL 7 billion (USD 1.33 billion). The projects are estimated to be around 947 MW, which will be connected to the National Interconnected System between 2026 and 2045 to meet the demand of three market distributors (Cemig, Coelba, and Light).

- Further, increasing investment in the transmission and distribution segment is expected to translate into increased demand for air-insulated switchgear in the region. In September 2021, Elecnor, a subsidiary of Elecnor do Brazil, announced the construction of a 200 Km transmission line from a solar power plant in Minas Gerais to the National Interconnected System. The first section will stretch into the municipalities of Janauba and Jaiba. It will be of 93 Km 230 kV double-circuit transmission line. The second section will link Pirapora with Tres Marias via a 112 Km 345 kV single-circuit transmission line. The transmission network is expected to have a total capacity of 1.6 GW and is estimated to have an expenditure of around EUR 18.5 million (USD 21.83 million).

- According to the International Trade Administration (ITA), by 2029, total investments in the power transmission sector of Brazil are projected to reach USD 22 billion, representing USD 15 billion in transmission lines and USD 7 billion in substations. Furthermore, the power distribution sector already sees an annual investment of around USD 2.2 billion per year, of which 69% goes into expansion, 19% into improvement, and 12% into the renewal of distribution networks.

- This further endorses the development and improvement of the transmission and distribution segment of the country, which would, in turn, drive the growth of the air-insulated switchgear market in Brazil.

South America Air Insulated Switchgear Industry Overview

The South America Air Insulated Switchgear Market is semi-consolidated. Some of the key players (not in particular order) are Schneider Electric SE, Siemens AG, Hitachi ABB Power Grids Ltd, General Electric Company, and Eaton corporation., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investments in Transmission and Distribution Infrastructure

- 4.5.2 Restraints

- 4.5.2.1 Increasing Adoption of Gas-Insulated Switchgear (GIS) as an Alternative to Air-Insulated Switchgear

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Voltage

- 5.1.1 Low Voltage

- 5.1.2 Medium Voltage

- 5.1.3 High Voltage

- 5.2 End-User

- 5.2.1 Commercial & Residential

- 5.2.2 Power utilities

- 5.2.3 Industrial sector

- 5.3 Countries

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Hitachi ABB Ltd

- 6.3.2 Schneider Electric SE

- 6.3.3 General Electric Company

- 6.3.4 Eaton Corporation PLC

- 6.3.5 Toshiba Corp.

- 6.3.6 Mitsubishi Electric Corporation

- 6.3.7 Siemens Energy AG

- 6.3.8 Hyosung Heavy Industries Corp.

- 6.3.9 Bharat Heavy Electricals Limited

- 6.3.10 Powell industries Inc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Investments in the Renewable Energy Sector and the Aging Power Infrastructure

南米の空気絶縁開閉装置:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日