|

市場調査レポート

商品コード

1644964

中国の開閉装置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の開閉装置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

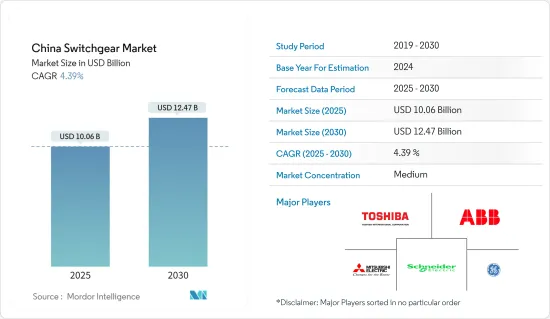

中国の開閉装置市場規模は2025年に100億6,000万米ドルと推定・予測され、2030年には124億7,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.39%です。

主要ハイライト

- 中期的には、発電量と消費量の増加、再生可能エネルギー発電の重視の高まりが、予測期間中の開閉装置市場を牽引すると予想されます。

- 一方、開閉装置市場に関連する厳しい環境規制や安全規制が抑制要因となっています。また、開閉装置市場全体で未組織部門との競合が増加していることも、今後数年間の開閉装置市場抑制要因になると予想されます。

- 中国における高い電力利用率を達成するための送配電(T&D)インフラの拡大は、開閉装置市場に大きな機会をもたらすと予想されます。

中国の開閉装置市場の動向

産業部門が大きな成長を遂げる見込み

- 開閉装置は、鉄道網やコンビナートなどの産業部門で使用されます。従来、開閉装置は変圧器の両側に設置されていました。産業では、開閉装置と関連機器の配置を、ユニット化された変電所として知られる1つの筐体にまとめることもあります。

- さらに、開閉装置の主要目的は、電気機器を保護、絶縁、制御することであり、高価な機械が電力変動による損傷から保護されるよう、産業と製造部門にとって不可欠です。さらに、開閉装置は、収益性の高い事業運営に必要な、機器の損傷によるダウンタイムを防止します。

- 世界各国は、経済成長と開閉装置市場を支援するため、国内製造部門の開発に注力しています。

- 同様に、中国の国家統計局によると、2022年には中国の工業生産が2020年比で3.6%成長するのに対し、約2.4%成長するという大幅な市場開拓があり、これは直接開閉装置産業市場を支援することになります。

- National Bureau of Statistics of China(NBS)によると、中国は米国に次ぐ世界第2位の経済大国であり、2022年のGDP総額は約17兆8,800億米ドルです。工業化と都市化の進展に伴い、中国経済は著しく成長しています。

- 継続的な都市化と人口増加に伴い、一次エネルギー消費量は2011年の約112.80エクサジュールから、2022年には159.39エクサジュールへと大幅に増加します。

- したがって、上記の点から、開閉装置の需要は予測期間中に大幅な成長が見込まれます。

インフラと再生可能エネルギー源への注目の高まりが市場成長を牽引

- 再生可能エネルギーによる発電の急増により、中国のように再生可能エネルギーによる電力網の統合が進んでいる国では、送電網の安定性が重要な問題となっており、旧式の送電・配電インフラを近代化する必要があります。太陽光や風力などの再生可能エネルギー発電は出力が変動するため、従来の送配電システムは再生可能エネルギーの送配電に適していない可能性があり、アップグレードや改修が必要となります。

- さらに、米国を凌駕し経済大国となるべく産業活動を活発化させている中国が、同国の変圧器市場を牽引する可能性が高いです。同国政府はまた、いくつかの場所で石炭火力発電所を禁止しています。こうした措置は、同国の再生可能エネルギー設備を即座に後押しし、電力供給のための送配電システムを拡大する可能性が高いです。

- 2021年、中国の再生可能エネルギー総設備容量は1,160.7ギガワット(GW)となり、2021年の設備容量1,020.2ギガワット(GW)を上回りました。再生可能エネルギー発電、特に風力発電と太陽光発電が増加し、それらを国の送電網に接続するため、変圧器の需要は国内で高水準を維持すると予想されます。

- さらに、政府の補助金が同国の大規模太陽光発電開発を支援しています。中国は再生可能エネルギーの固定価格買取制度を導入しており、太陽光発電開発にとって世界的に最も効果的な再生可能エネルギー支援施策の1つとして注目されています。

- 老朽化したインフラのアップグレードは、市場の成長をさらに後押しすると予想されます。寿命延長に関する機器のアップグレードは、開閉装置市場を牽引すると考えられます。開閉装置市場の成長を後押しするもう一つの重要な要因は、インフラへの注目の高まりによる世界の建設活動の活発化です。

- 2022年3月、State Grid Corp of Chinaは、総投資額17億米ドルの2つの超高圧送電プロジェクトの建設を開始しました。福州市と福建省アモイ市を結ぶ超高圧(UHV)送電線と、河南省駐馬店市と湖北省武漢市を結ぶ送電線です。このプロジェクトは2023年までに稼動する予定です。さらに、中国国民生用電子機器網総公司による電力ネットワークインフラへの投資計画は、2022年には5,000億人民元を超えそうで、これは国有企業が2021年に支出した金額よりも25%多いです。このような投資の増加は、開閉装置(GIS)の大規模な需要を生み出すと予想されます。

- BP統計レビュー2022によると、2022年の中国の発電量は8,848.7テラワット時です。年間成長率は10%で、電力需要の増加により発電量の増加が見込まれ、これが予測期間の開閉装置市場を牽引します。

中国の開閉装置産業概要

中国の開閉装置市場は半固体化しています。この市場の主要企業(順不同)には、ABB Ltd、Schneider Electric SE、General Electric Company、Toshiba International Corporation、Mitsubishi Electric Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 発電量と消費量の増加

- 再生可能エネルギー発電への注目の高まり

- 抑制要因

- 厳しい環境・安全規制

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- タイプ

- 電圧

- 低電圧

- 中電圧

- 高電圧

- 絶縁

- ガス絶縁開閉装置(GIS)

- 空気絶縁開閉装置(AIS)

- その他

- 設置方法

- 屋内

- 屋外

- 電圧

- エンドユーザー産業

- 商業

- 住宅

- 産業

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- General Electric Company

- Siemens AG

- Toshiba International Corporation

- Mitsubishi Electric Corporation

- SGC SwitchGear Company

- Larson & Turbo Limited

- KOHL Gmbh

- Hyosung Heavy Industries Corp.

- Hitachi Energy Ltd

第7章 市場機会と今後の動向

- 送配電(T&D)インフラの拡大

目次

Product Code: 5000120

The China Switchgear Market size is estimated at USD 10.06 billion in 2025, and is expected to reach USD 12.47 billion by 2030, at a CAGR of 4.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, increasing electricity generation and consumption, along with the rising emphasis on renewable energy generation, are expected to drive the switchgear market during the forecast period.

- On the other hand, stringent environmental and safety regulations related to the switchgear market are restraining factors. Also, increasing competition from the unorganized sector of the overall switchgear market is expected to restrain the switchgear market in the coming years.

- Nevertheless, the expansion of power transmission and distribution (T&D) infrastructure to achieve high rates of electricity access in China is expected to create significant opportunities for switchgear market.

China Switchgear Market Trends

Industrial Sector is Expected to Witness a Significant Growth

- Switchgear is used in the industrial sector, including railway networks and industrial complexes. Conventionally, switchgear is installed on both sides of voltage transformers. In industries, switchgear and associated equipment arrangement may be united in one housing known as a unitized substation.

- Furthermore, the primary purpose of switchgear is to protect, isolate, and control electrical devices, which is essential for the industrial and manufacturing sector so that the expensive machinery is prevented from damage caused by electricity fluctuations. In addition, switchgear prevents downtime caused by damaged equipment, which is necessary for a profitable business operation.

- Several countries globally focus on developing domestic manufacturing sectors to aid economic growth and the switchgear market.

- Similarly, according to the National Bureau of Statistics in China, in 2022, there was a significant growth in the development of China's industrial production compared to 2020, with about 2.4% growth compared to a growth of 3.6% in 2022, which is directly going to aid the Switchgear industrial market.

- China is the second-largest economy in the world, only after the United States, with a total GDP of about USD 17.88 trillion, in 2022, according to the National Bureau of Statistics of China (NBS). The country's economy is rising significantly with increasing ongoing industrialization and urbanization.

- With continuous urbanization and increased population, the country witnessed a significant rise in primary energy consumption from roughly around 112.80 exajoule in 2011 to 159.39 exajoule of primary energy consumption in 2022.

- Therefore, owing to the above points, the demand for switchgear is expected to witness significant growth during the forecast period.

Growing Focus on Infrastructure and Renewable Energy Sources Drives the Market Growth

- Due to the rapid rise in renewable power generation, grid stability has become a significant issue in countries like China with a high level of renewable integration in their grids, which needs the modernization of older T&D infrastructure. As renewable power generated from sources such as solar and wind provide variable power output, traditional T&D systems may not be suitable for renewable energy transmission & distribution and require up-gradation or retrofitting.

- Moreover, China's increasing industrial operations to surpass the United States and become a superpower in terms of the economy are likely to drive the transformers' market in the country. The country's government has also banned coal-fired power plants at several locations; such measures instantly boosted the country's renewable installations and are likely to expand its transmission and distribution system to supply power.

- In 2021, China's total renewable energy installation capacity was 1160.7 gigawatts (GW), more than the installed capacity in 2021, 1020.2gigawatts (GW). With the increasing growth in renewable power generation, particularly from wind and solar PV, and connecting those to the country's grid, the demand for transformers is expected to remain high in the country.

- Moreover, the government's subsidies support large-scale solar PV development in the country. China has adopted a feed-in tariff subsidy policy for renewable energy, which has been marked as one of the most effective renewable energy support policies globally for solar PV developments.

- The upgradation of the aging infrastructure is further anticipated to power the market's growth. The upgradation of equipment concerning extending the life span would drive the market for switchgear. Another significant factor fueling the switchgear market growth is the rising construction activities worldwide, owing to the increasing focus on infrastructure.

- In March 2022, State Grid Corp of China started the construction of two ultrahigh voltage power transmission projects with a total investment of USD 1.7 billion. It comprises an ultrahigh voltage (UHV) power transmission line linking Fuzhou with Xiamen in Fujian province and a line connecting Zhumadian in Henan province with Wuhan in Hubei province. The project is likely to come online by 2023. Further, the planned investment by the State Grid Corporation of China in the country's electricity network infrastructure is likely to exceed CNY 500 billion in 2022, which is 25% more than the state-owned firm spent in 2021. Such increasing investments are anticipated to create a massive demand for switchgear (GIS).

- According to BP statical review 2022, the electricity generation of China accounted for 8848.7 terawatt-hours in 2022. With an annual growth rate of 10%, energy generation is expected to increase due to the increasing power demand, which, in turn, will drive the switchgear market in the forecast period.

China Switchgear Industry Overview

The China switchgear market is semi-consolidated. Some of the key players in this market (not in a particular order) include ABB Ltd, Schneider Electric SE, General Electric Company, Toshiba International Corporation, and Mitsubishi Electric Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Electricity Generation and Consumption

- 4.5.1.2 Rising Emphasis on Renewable Energy Generation

- 4.5.2 Restraints

- 4.5.2.1 Stringent Environmental and Safety Regulations

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Voltage

- 5.1.1.1 Low-Voltage

- 5.1.1.2 Medium-Voltage

- 5.1.1.3 High-Voltage

- 5.1.2 Insulation

- 5.1.2.1 Gas Insulated Switchgear (GIS)

- 5.1.2.2 Air Insulated Switchgear (AIS)

- 5.1.2.3 Other Insulation Types

- 5.1.3 Installation

- 5.1.3.1 Indoor

- 5.1.3.2 Outdoor

- 5.1.1 Voltage

- 5.2 End-user Industry

- 5.2.1 Commertial

- 5.2.2 Residential

- 5.2.3 Industrial

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 General Electric Company

- 6.3.3 Siemens AG

- 6.3.4 Toshiba International Corporation

- 6.3.5 Mitsubishi Electric Corporation

- 6.3.6 SGC SwitchGear Company

- 6.3.7 Larson & Turbo Limited

- 6.3.8 KOHL Gmbh

- 6.3.9 Hyosung Heavy Industries Corp.

- 6.3.10 Hitachi Energy Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of Power Transmission and Distribution (T&D) Infrastructure