|

市場調査レポート

商品コード

1644948

英国の住宅建設:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)UK Residential Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の住宅建設:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

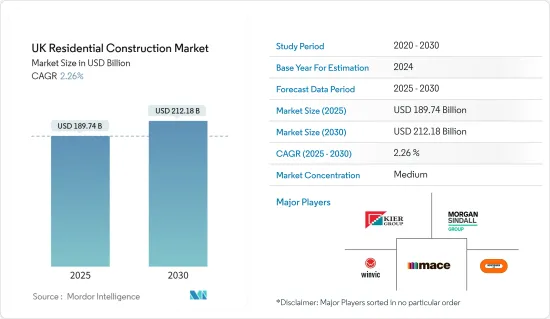

英国の住宅建設の市場規模は2025年に1,897億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.26%で、2030年には2,121億8,000万米ドルに達すると予測されます。

この市場拡大の大きな要因は、年間30万戸の新築住宅建設という政府の野心的な目標です。この目標が大胆であることは否定できないが、英国に根強く残る住宅課題に対処するためには不可欠です。こうした野心的な目標を達成するためには、建設会社は急速に事業を拡大しなければならないです。そのためには、オフサイト・プレハブなどの現代的な建設技術を採用し、プロセスを迅速化し、経費を削減し、生産性を高めるために最先端技術を活用する必要があります。

しかし、この道のりにはハードルがないわけではないです。英国政府は、いくつかの新しい建築規制や基準を導入し、プロジェクトにさらなる複雑さをもたらしています。例えば、建築安全法やフューチャー・ホームズ・スタンダードは、住宅の安全性とエネルギー効率を高めることを目的としているが、同時に建設作業を複雑化し、長期化させるものでもあります。建設業者は、潜在的な遅れを回避するために、こうした規制の変化を巧みに操らなければならないです。

さらに、不動産価格の高騰は両刃の課題となっています。住宅所有者は借り換えの恩恵を受けるが、不動産価格の上昇は建設コストの上昇につながります。持続的なインフレや資材価格に影響するサプライチェーンの混乱も相まって、住宅建設にかかる経済的負担は増大しています。しかし、こうしたコスト上昇にもかかわらず、住宅需要は、特に都心部や人口が増加している地域で堅調を維持しています。

パンデミック(世界的大流行)は、デジタルツールや適応性の高い作業手法の採用を早め、このセクターを大きく変貌させました。多くの建設会社がロックダウンに起因する課題に取り組む一方で、デジタル・プロジェクト管理、ビルディング・インフォメーション・モデリング(BIM)からオートメーションに至るまで、テクノロジーを迅速に統合した建設会社は勢いを維持しました。

今後は、AI、ドローン、ロボティクス、その他の先端技術の統合により、効率性の向上、無駄の最小化、急増する需要への対応が期待され、業界のデジタル進化は続くとみられます。

まとめると、無数の課題に直面しているにもかかわらず、英国の住宅建設市場は今後数年間で力強い成長を遂げようとしています。持続可能でエネルギー効率の高い住宅を目指す業界の動きは、技術革新に拍車をかけることが期待されます。しかし、規制の強化、コストの高騰、技能不足に悩む労働力など、建設会社は機敏さと創意工夫を怠らず、前途に備えなければならないです。

英国の住宅建設市場の動向

エネルギー効率に関する政府の義務化

英国の住宅建設業界は、2050年までに温室効果ガス排出量ネットゼロを達成するという政府のコミットメントによって大きく形作られています。この野心的な目標は、新たな規制の策定を推進するだけでなく、建設における持続可能な材料の採用を促進しています。このグリーン転換を強化するため、政府はグリーン産業革命のために約300億英ポンド(約364億米ドル)を確保しています。さらに政府は、持続可能な建築慣行と環境に優しい技術への投資を拡大することを目指しています。予測によると、2030年までに、こうした取り組みによって、最大900億英ポンド(1,090億米ドル)の民間投資が行われ、グリーン産業で44万人の雇用が創出される可能性があります。このような持続可能性の重視の高まりは、特に低炭素材料やエネルギー効率の高い建築技術の分野において、住宅建設市場に新たなチャンスをもたらすことになります。

この動向を受け、政府は2022~2023年の住宅プロジェクトに115億英ポンド(~140億米ドル)を割り当てています。この投資のかなりの部分は、ロンドン、マンチェスター、バーミンガムといった活気ある都市に焦点を当て、住宅価格の危機をターゲットにしています。総予算のうち、約84億英ポンド(~100億米ドル)が地方自治体の住宅強化に充てられます。政府は、新築住宅への資金提供だけでなく、既存住宅の改修にも資源を投入し、厳しいエネルギー効率基準に適合するようにしています。手頃な価格でエネルギー効率の高い住宅へのこうした堅実な投資は、英国の住宅建設市場の成長を推進する上で極めて重要です。

英国の住宅建設市場におけるアパート建設への注目の高まり

英国の住宅建設市場では、都市部における手頃な価格の住宅需要の高まりに対応するため、アパート開発を優先する傾向が強まっています。マンチェスター、ロンドン、バーミンガムなどの都市は、スペースの制約と人口の増加に直面しています。その結果、賃貸住宅(BTR)プロジェクトを含む高密度住宅ソリューションが重要になってきています。例えば、2024年2月、リーガル&ジェネラルはマンチェスターで500戸のBTRマンションを開発する計画を発表し、このセクターの成長の可能性を示しました。しかし、原材料やエネルギーコストの上昇により、こうしたプロジェクトは複雑さを増しています。リーガル&ジェネラルのような開発会社は、効率性を高めコストを削減するモジュール建設技術を採用することで、こうした課題に対処しています。

政府の資金援助イニシアティブも、アパート建設へのシフトを後押ししています。2024年4月、英国政府は18億ユーロ(19億4,000万米ドル)を「アフォーダブル・ハウジング・プログラム」に割り当て、都市部の住宅不足を緩和する集合住宅の役割を強調しました。これらのプロジェクトは、ロンドンやバーミンガムのような人口密集都市で土地利用効率を最大化することに重点を置き、土地不足に対処しながら必要不可欠な住宅ソリューションを提供するものです。このような対策は、財政が逼迫し、プロジェクト費用が高騰する中、建設の勢いを維持し、十分なサービスを受けていない人々にとって手頃な価格の住宅が利用しやすい状態を維持するために不可欠です。

このような進歩にもかかわらず、建設コストの上昇は引き続き課題となっています。業界の報告によると、2024年3月のアパートプロジェクトの資材価格は前年同月比で8%上昇しました。Barratt Developments社を含む開発会社は、こうしたコスト上昇に対処するため、プロジェクトの予算とスケジュールを見直しています。さらに、開発業者は手頃な価格と品質の両立を目指しているため、代替資材やサプライチェーン戦略の改善の必要性も高まっています。このような需要主導型のアパート建設とコスト管理の二重焦点は、2024年の英国の住宅建設市場を形成する複雑性を浮き彫りにしています。

英国の住宅建設業界の概要

英国の住宅建設市場は、Barratt Developments、Taylor Wimpey、Persimmon Homesといった業界大手が主導する競争の激化を目の当たりにしています。これらの大手企業は、政府の住宅目標達成に努めるだけでなく、手頃な価格の住宅危機に取り組み、高品質でエネルギー効率の高い住宅を供給しています。ポートフォリオを拡大するにつれ、サステナビリティとグリーンビルディングの実践を優先し、ネット・ゼロの目標との整合性を確保しています。

こうした大手企業以外にも、バークレー・グループやキアー・グループのような企業が、持続可能な開発に重点を置きながら、高級住宅や都市再生プロジェクトでニッチを開拓しています。同時に、ウィンビック・グループ(Winvic Group)のような新進気鋭の企業も、モジュール建築やオフサイト製造など、より迅速で経済的なプロジェクト完成を約束する最先端の建設技術で躍進しています。革新と持続可能性に向けたこの集団的な軸足は、市場全体の水準を高めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 市場促進要因

- 都市化と手頃な価格の住宅需要

- モジュラー方式と持続可能な建設技術の採用

- 市場抑制要因

- 建設コストの上昇

- 建設部門における労働力不足

- 市場機会

- エネルギー効率の高い持続可能なアパートへの投資

- 市場促進要因

- 住宅不動産セクターにおける技術革新への洞察

- 政府の規制と取り組み

- サプライチェーン/バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- コンドミニアムとアパート

- ヴィラと土地付き住宅

- 主要都市別

- ロンドン

- バーミンガム

- グラスゴー

- リバプール

- その他の地域

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Kier Group

- Morgan Sindall Group

- Mace

- Winvic Group

- Bouygues UK

- Lendlease

- Balfour Beatty

- Willmott Dixon Holdings

- Skanska UK

- Laing O'Rourke

- Galliford Try

- その他の企業

第7章 市場の将来

第8章 付録

The UK Residential Construction Market size is estimated at USD 189.74 billion in 2025, and is expected to reach USD 212.18 billion by 2030, at a CAGR of 2.26% during the forecast period (2025-2030).

A significant driver of this market expansion is the government's ambitious target of constructing 300,000 new homes annually. While this goal is undeniably bold, it's essential for addressing the persistent housing challenges in the UK. To achieve these ambitious targets, construction firms must rapidly scale operations. This necessitates the adoption of contemporary construction techniques, such as off-site prefabrication, and harnessing cutting-edge technologies to expedite processes, curtail expenses, and boost productivity.

However, the journey isn't without hurdles. The UK government has rolled out several new building regulations and standards, introducing additional complexities to projects. For instance, the Building Safety Act and the Future Homes Standard aim to enhance home safety and energy efficiency, but they also complicate and prolong construction endeavors. Builders must adeptly navigate these regulatory shifts to sidestep potential delays.

Furthermore, surging property prices present a dual-edged challenge. While homeowners benefit from refinancing opportunities, these elevated property values translate to escalating construction costs. Coupled with persistent inflation and supply chain disruptions affecting material prices, the financial burden of home construction is rising. Yet, despite these escalating costs, housing demand remains robust, particularly in urban centers and regions witnessing population growth.

The pandemic significantly reshaped the sector, hastening the adoption of digital tools and adaptable work methodologies. While numerous construction firms grappled with lockdown-induced challenges, those that swiftly integrated technologies-ranging from digital project management and Building Information Modeling (BIM) to automation-managed to maintain momentum.

Looking forward, the industry's digital evolution is poised to continue, with the integration of AI, drones, robotics, and other advanced technologies promising enhanced efficiency, minimized waste, and the ability to cater to surging demand.

In summary, despite facing a myriad of challenges, the UK residential construction market is on track for robust growth in the coming years. The industry's push towards sustainable and energy-efficient homes promises to spur innovation. Yet, with tightening regulations, escalating costs, and a workforce grappling with skill shortages, construction firms must remain agile, inventive, and prepared for the road ahead.

UK Residential Construction Market Trends

Government mandates pertaining to Energy Efficiency

The UK residential construction industry is being significantly shaped by the government's commitment to achieving Net Zero greenhouse gas emissions by 2050. This ambitious goal is not only driving the formulation of new regulations but also promoting the adoption of sustainable materials in construction. To bolster this green transition, the government has set aside approximately GBP 30 billion (USD 36.4 billion) for its green industrial revolution. Furthermore, the government aims to amplify investments in sustainable building practices and eco-friendly technologies. Projections indicate that by 2030, these initiatives could draw in private investments of up to GBP 90 billion (USD 109 billion) and generate 440,000 jobs in green industries. This heightened emphasis on sustainability is poised to unlock fresh opportunities in the residential construction market, especially in the realms of low-carbon materials and energy-efficient building techniques.

Continuing its trend, the government has allocated GBP 11.5 billion (~USD 14 billion) for housing projects in the 2022-2023 period. A substantial chunk of this investment targets the affordability crisis, with a keen focus on bustling cities like London, Manchester, and Birmingham. Out of the total budget, around GBP 8.4 billion (~USD 10 billion) is channeled to bolster local authority housing. Beyond funding new constructions, the government is also channeling resources into retrofitting existing homes, ensuring they align with stringent energy efficiency standards. Such steadfast investments in affordable and energy-efficient housing are set to be pivotal in propelling the growth of the UK's residential construction market.

Rising Focus on Apartment Construction in the UK Residential Construction Market

The UK residential construction market is increasingly prioritizing apartment developments to address the growing demand for affordable housing in urban areas. Cities such as Manchester, London, and Birmingham are facing space constraints and rising populations. As a result, high-density housing solutions, including build-to-rent (BTR) projects, are becoming critical. For example, in February 2024, Legal & General announced plans to develop 500 BTR apartments in Manchester, showcasing the sector's growth potential. However, rising costs for raw materials and energy have added complexity to these projects. Developers like Legal & General are addressing these challenges by adopting modular construction techniques, which enhance efficiency and reduce costs.

Government funding initiatives are also driving the shift toward apartment construction. In April 2024, the UK government allocated EUR 1.8 billion (USD 1.94 billion) to its Affordable Housing Programme, emphasizing the role of apartment complexes in mitigating urban housing shortages. These projects focus on maximizing land use efficiency in densely populated cities like London and Birmingham, delivering essential housing solutions while addressing land scarcity. Such measures are vital for sustaining construction momentum amid financial pressures and rising project costs, ensuring affordable housing remains accessible to underserved populations.

Despite these advancements, rising construction costs continue to pose challenges. According to industry reports, material prices for apartment projects increased by 8% year-on-year in March 2024. Developers, including Barratt Developments, are revising project budgets and timelines to manage these rising costs. Additionally, the need for alternative materials and improved supply chain strategies has become more pressing, as developers aim to balance affordability with quality. This dual focus on demand-driven apartment construction and cost management highlights the complexities shaping the UK residential construction market in 2024.

UK Residential Construction Industry Overview

The UK residential construction market is witnessing heightened competition, spearheaded by industry giants such as Barratt Developments, Taylor Wimpey, and Persimmon Homes. These leading firms are not only striving to meet government housing targets but are also tackling the affordable housing crisis and delivering high-quality, energy-efficient homes. As they broaden their portfolios, they prioritize sustainability and green building practices, ensuring alignment with Net Zero objectives.

Beyond these major players, firms like Berkeley Group and Kier Group are carving out niches in premium residential and urban regeneration projects, placing a pronounced focus on sustainable development. At the same time, up-and-coming entities like Winvic Group are making strides with cutting-edge construction techniques, including modular building and off-site manufacturing, which promise quicker and more economical project completions. This collective pivot towards innovation and sustainability is elevating standards across the board in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Urbanization and Demand for Affordable Housing

- 4.2.1.2 Adoption of Modular and Sustainable Construction Techniques

- 4.2.2 Market Restraints

- 4.2.2.1 Rising Construction Costs

- 4.2.2.2 Labor Shortages in the Construction Sector

- 4.2.3 Market Opportunities

- 4.2.3.1 Investment in Energy-Efficient and Sustainable Apartments

- 4.2.1 Market Drivers

- 4.3 Insights into Technological Innovation in the Residential Real Estate Sector

- 4.4 Government Regulations and Initiatives

- 4.5 Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porters' Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Geopolitics and Pandemics on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Condominiums and Apartments

- 5.1.2 Villas and Landed Houses

- 5.2 By Key Cities

- 5.2.1 London

- 5.2.2 Birmingham

- 5.2.3 Glasgow

- 5.2.4 Liverpool

- 5.2.5 Rest of the UK

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Kier Group

- 6.2.2 Morgan Sindall Group

- 6.2.3 Mace

- 6.2.4 Winvic Group

- 6.2.5 Bouygues UK

- 6.2.6 Lendlease

- 6.2.7 Balfour Beatty

- 6.2.8 Willmott Dixon Holdings

- 6.2.9 Skanska UK

- 6.2.10 Laing O'Rourke

- 6.2.11 Galliford Try*

- 6.3 Other Companies