|

市場調査レポート

商品コード

1644902

米国のFTL貨物仲介:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)US FTL Freight Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のFTL貨物仲介:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

米国のFTL貨物仲介の市場規模は2025年に169億1,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは7.86%で、2030年には246億9,000万米ドルに達すると予測されます。

主なハイライト

- 米国ではパンデミック(世界的大流行病)の影響で貨物輸送・ロジスティクス産業が停滞し、国境を越えた貨物の輸送が閉鎖されました。パンデミックの影響は、貨物ヤードや倉庫に大規模な課題を生み出し、COVID-19の状況に苦しんでいる多くの施設では、人員削減や荷積み・荷受けドックの営業時間短縮が行われました。

- 近年、米国では、内陸貨物輸送と米国、カナダ、メキシコ間の国境を越えた貿易からの需要により、フルトラック積載(FTL)サービスが大幅に成長しています。米国の輸出入の前年比増加も、同国の貨物仲介業界の開発を支えています。貨物ブローカーの重要性は、ブローカーとしての役割と、荷送人と運送業者双方のビジネスを促進することによって高まっています。米国では、世界的にeコマース企業が台頭しているため、輸送・貨物輸送サービスが増加傾向にあります。

- トラック満載貨物の仲介はまだ成長段階にあり、国内市場への参入を目指す新規荷主にとって大きな魅力となっています。しかし、既存の荷送人は、国際貨物輸送業界で主導的な地位を得るために、仲介会社や輸送会社との長期契約を求めています。FTLブローカーは荷主のために船積みサービスを促進し、輸送会社の船積みを監視します。多くの貨物ブローカー会社はデジタルマーケットプレースを強化し、自動価格設定、アプリケーション・プログラミング・インターフェース(API)接続、データサイエンス、社内向け技術などのテクノロジーを導入しています。消費者の嗜好も変化しているため、企業はテクノロジーやイノベーションへの投資や支出を増やしています。技術の進歩が進むにつれ、従来の企業は新興企業との激しい競争に直面しています。例えば、北米最大級の貨物ブローカーであるC.H.ロビンソンは2019年、デジタル新興企業に対抗するため、2024年までの技術支出を倍増すると発表しました。

- 市場では、あるシナリオが繰り返し展開されています。トラック積載量に満たないサイズの荷物を持つ荷主は、より迅速な配送を確保するためにフルトラック積載(FTL)サービスに料金を支払っており、その結果、スペースと非効率性が生じています。新興企業は主にこの分野を攻撃してきました。これは、LTLや小包よりも複雑でなく、より大きなパイを含んでいるためです。Transfix、Convoy、Uber Freightのような最も資金を集めている新興企業は、貨物のマッチングに焦点を当てています。モバイルテクノロジーを活用し、手作業を自動化することで、従来のブローカーに取って代わりつつあります。

米国のFTL貨物仲介市場の動向

燃料価格の変動が市場の成長を妨げる

輸送会社(ロジスティクス会社)は、市況が保証する場合、または高い営業コストをカバーする場合、高い運賃を請求することがあります。その結果、仲介会社が顧客向けの価格設定を引き上げることができなければ、収入や営業利益が減少する可能性があります。FTLサービスに対する市場の需要の増加や、規制の変更待ちにより、利用可能なキャパシティが減少し、運送会社の価格設定が上昇する可能性があります。燃料価格は変動しやすく、予測が難しいです。過去5年間、燃料価格は劇的に変動しました。顧客は、価格の下落が燃料節約に転嫁されることを期待しています。輸送会社が燃料費の下落を反映して価格を下げない場合、顧客が代替輸送手段を求めるため、出荷量が減少する可能性があります。

この輸送量の減少は、仲介会社の売上総利益および営業利益に悪影響を及ぼします。燃料価格が上昇した場合、運送会社は営業費用の増加をカバーするため、より高い料金を請求することが予想されます。こうしたコスト増の総額を顧客に転嫁し続けることができなければ、仲介会社の売上総利益および営業利益は減少する可能性があります。燃料費の上昇はまた、顧客が代替輸送手段を利用することを選択する可能性があるため、輸送手段別の収入割合に重大な変化をもたらす可能性もあります。仲介会社がより低い粗利益率を実現する輸送手段への重大なシフトは、営業成績を悪化させる可能性があります。ウクライナ・ロシア戦争は、ロシアが第3位の原油生産国であることから、燃料価格の高騰も引き起こしました。

建設セクターは急成長するエンドユーザー・セグメント

一部の建設部門では目先の課題があるもの、米国の中長期的な成長ストーリーは変わっていないです。米国の建設業界は、今後4四半期にわたって安定した成長が見込まれます。米国では、いくつかのプロジェクトが計画段階を経ている一方、世界的流行病による1年間の遅れを経てようやく再開したプロジェクトもあります。原材料価格の上昇、建築資材の不足、熟練労働者の不足といった世界・サプライチェーンに関連する課題にもかかわらず、住宅建設セクターは4~8四半期にわたって安定した成長を続けると思われます。

住宅建設セクターは、低金利、大型住宅への旺盛な需要、米国内の住宅在庫の少なさに大きく支えられています。今後数四半期は、ヘルスケアと教育セクターが注目を集めると思われます。2021年11月、米国議会は1兆米ドルのインフラ支出法案を可決しました。

このインフラ法案では、道路、橋、高速道路のアップグレード、都市交通システムと旅客鉄道網の近代化のために、米国で今後8年間に新たに5,500億米ドルの連邦政府支出が提案されています。新たなインフラ支出法案は、当初の2兆3,000億米ドルの提案には及ばないもの、米国のさまざまなインフラ部門に対する1兆米ドルの支出は、今後4~8四半期にわたって同国の建設業界の成長を支え続けると思われます。

米国のFTL貨物仲介業界の概要

米国のFTL貨物仲介市場は比較的細分化されており、著名な地域企業、世界企業、様々な中小のローカル企業が存在します。業界の主要企業には、CH Robinson、Echo Global Logistics、Worldwide Express、Landstar System Inc.、Schneider、SunteckTTS、GlobalTranz、JB Hunt Transport Inc.、Hub Group、BNSF Logistics LLCなどがあります。Convoy、Uber Freight、uShipなどの新規参入企業は、価格の透明性、オンライン積荷ボード、モバイルアプリによる貨物予約のための貨物マーケットプレースを提供し、貨物予約と支払いプロセスにおける人的交流を排除することで、大きな市場シェアを獲得しようとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の背景

- 調査の前提条件と市場定義

第2章 調査と関与の枠組み

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の創出

- プロジェクトのプロセスと構造

- エンゲージメント・フレームワーク

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場力学

- 市場促進要因

- 効率的な輸送に対する需要の増加

- eコマース産業の成長

- 市場の課題/抑制要因

- 市場に影響を与える激しい競合

- 燃料価格の変動

- 市場機会

- 先端技術の採用

- ロジスティクスにおける持続可能性の重視

- 市場促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン/サプライチェーン分析

- 米国物流業界(概要、動向、研究開発、主要統計等)

- 主要な政府規制と取り組み

- 運賃に関する洞察

- 技術スナップショット

- 米国通関セクターに関する定性・定性的洞察

- シカゴとイリノイ-FTL貨物仲介業に関する洞察

- 貨物ブローカー市場の賃金と給与構造に関する洞察

- COVID-19が市場に与える影響に関する評価

第5章 市場セグメンテーション

- エンドユーザー別

- 製造業と自動車

- 石油・ガス、鉱業、採石業

- 農業、漁業、林業

- 建設業

- 流通・貿易

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- CH Robinson

- Total Quality Logistics

- XPO Logistics Inc.

- Echo Global Logistics

- Worldwide Express

- Coyote Logistics

- Landstar System Inc.

- Schneider

- Suntecktts

- Globaltranz

- J.B. Hunt Transport Inc.

- Hub Group

- BNSF Logistics LLC

- Kag Logistics Inc.

- Transplace*

第7章 市場の将来

第8章 付録

第9章 クレデンシャル

- クライアント一覧

- 業界内の類似案件

第10章 出版社について

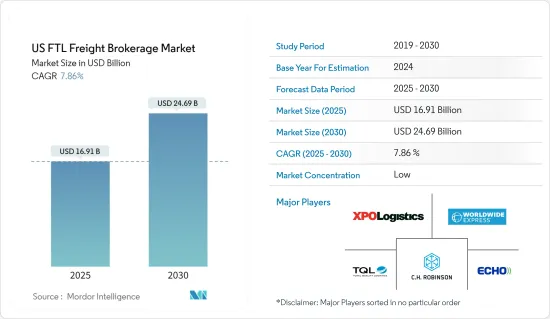

The US FTL Freight Brokerage Market size is estimated at USD 16.91 billion in 2025, and is expected to reach USD 24.69 billion by 2030, at a CAGR of 7.86% during the forecast period (2025-2030).

Key Highlights

- The full truckload freight brokerage market in the United States experienced a strong hit by the pandemic, as the freight transportation and logistics industry slowed down in the country due to pandemic restrictions and the closing of cross-border shipments. The impact of the pandemic has created massive challenges in freight yards and warehouses, where many facilities struggling with COVID-19 conditions have cut their staffing levels and reduced operating hours at loading and receiving docks.

- In recent years, the US has experienced substantial growth in full-truckload (FTL) services owing to the demand from inland freight movement and cross-border trade between the United States, Canada, and Mexico. The increase in year-on-year growth of the United States exports and imports also supports the development of the freight brokerage industry in the nation. The significance of freight brokers is growing owing to their role as intermediaries and facilitating the business of both shippers and carriers. Transport and freight forwarding services are on the rise in the United States due to the number of e-commerce companies emerging globally.

- Full truckload freight brokerage is still in a growth phase and is a major attraction for new shippers looking to penetrate the domestic market. However, established shippers seek long-term contracts with brokerage firms and carriers to gain a leading position in the international freight forwarding industry. FTL brokers facilitate the shipping service for shippers and monitor carriers' shipments. Many freight brokerage firms are strengthening their digital marketplace and are adopting technology, such as automated pricing, application programming interface (API) connectivity, data science, and internally facing technology. Companies are increasing their investments and spending on technologies and innovations as consumer preferences are also changing. With the increasing technological advancements, traditional players face intense competition from startups. For instance, C.H. Robinson, one of the largest freight brokers in North America, announced in 2019 that it would double its technology spending through 2024 to compete with digital startups.

- The market has seen one scenario play out repeatedly. Shippers with less-than-truckload-size loads are paying for full truckload (FTL) service to ensure faster delivery of goods, resulting in space and inefficiencies. Startups have mostly attacked this sector. This is because it is less complex than LTL and parcel and contains a larger piece of the pie. The most funded startups, like Transfix, Convoy, and Uber Freight, focus on freight matching. They are replacing traditional brokers by utilizing mobile technology and automating manual operations.

US FTL Freight Brokerage Market Trends

Fluctuating Fuel prices Hampering the Growth of the Market

Carriers (logistics companies) may charge higher rates if market conditions warrant or cover higher operating costs. As a result, if brokerage firms cannot increase pricing for their customers, revenues, and income from operations may decrease. The increased market demand for FTL services and pending regulatory changes may reduce available capacity and raise carrier pricing. Fuel prices can be volatile and challenging to forecast. Over the last five years, fuel prices have fluctuated dramatically. Clients anticipate that lower prices will pass them on to fuel savings. If carriers do not lower their prices to reflect decreases in fuel costs, shipment volume may suffer as customers seek alternative shipping options.

This volume decrease would harm the brokerage companies' gross profits and operating income. In the event of rising fuel prices, carriers can be expected to charge higher fees to cover higher operating expenses. The gross profit of brokerage firms and income from operations may decrease if they cannot continue to pass through to their clients the total amount of these increased costs. Higher fuel costs could also cause material shifts in the percentage of revenue by transportation mode, as clients may elect to utilize alternative transportation modes. Any material shifts to transportation modes concerning which brokerage firms realize lower gross profit margins could impair operating results. The Ukraine-Russia war also caused a spike in fuel prices as Russia is the third-largest producer of crude oil.

Construction Sector is the Fastest-growng End-user Segment

Despite near-term challenges in certain construction sectors, the medium to long-term growth story in the United States remains intact. The construction industry in the United States is expected to grow steadily over the next four quarters. In the United States, several projects are working their way through the planning phase, whereas others have finally resumed after a year of global pandemic-related delays. Despite the challenges associated with the global supply chain, such as rising raw material prices, shortage of building materials, and lack of skilled labor, the residential construction sector will continue its stable growth over the four to eight quarters.

The residential construction sector largely remains supported by low lending rates, strong demand for bigger homes, and low housing inventory in the United States. Over the next few quarters, the healthcare and education sectors will receive more attention. In November 2021, the US Congress passed a USD 1 trillion infrastructure spending bill.

The infrastructure legislation proposes USD 550 billion in new federal expenditure over the next eight years in the United States for the upgrade of roads, bridges, and highways and modernizing the city transit systems and passenger rail networks. While the new infrastructure spending bill falls short of the original USD 2.3 trillion proposals, the USD 1 trillion spending on various United States infrastructure sectors will keep supporting the growth of the construction industry over the next four to eight quarters in the country.

US FTL Freight Brokerage Industry Overview

The US FTL freight brokerage market is relatively fragmented, with prominent regional, global, and various small- and medium-sized local players. Major players in the industry include CH Robinson, Echo Global Logistics, Worldwide Express, Landstar System Inc., Schneider, SunteckTTS, GlobalTranz, JB Hunt Transport Inc., Hub Group, and BNSF Logistics LLC. New entrants such as Convoy, Uber Freight, uShip, etc., are trying to gain significant market share by offering price transparency, online load boards, and freight marketplaces for booking freight via mobile apps and removing human interaction in the freight booking and payment process.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Background

- 1.2 Study Assumptions and Market Definition

2 RESEARCH AND ENGAGEMENT FRAMEWORKS

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

- 2.5 Project Process and Structure

- 2.6 Engagement Frameworks

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increasing demand for efficient transportation

- 4.2.1.2 Growing eCommerce industry

- 4.2.2 Market Challenges/Restraints

- 4.2.2.1 Intense competition affecting the market

- 4.2.2.2 Fluctuating fuel prices

- 4.2.3 Market Opportunities

- 4.2.3.1 Adoption of advanced technologies

- 4.2.3.2 Focus on sustainability in logistics

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain / Supply Chain Analysis

- 4.5 US Logistics Industry (Overview, Trends, R&D, Key Statistics, etc.)

- 4.6 Key Government Regulations and Initiatives

- 4.7 Insights into Freight Rates

- 4.8 Technology Snapshot

- 4.9 Qualitative and Qualitative Insights into the US Customs Clearance Sector

- 4.10 Insights into Chicago and Illinois - FTL Freight Brokerage

- 4.11 Insights into Wages and Pay Structure in the Freight Brokerage Market

- 4.12 Assessment on the Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Manufacturing and Automotive

- 5.1.2 Oil and Gas, Mining, and Quarrying

- 5.1.3 Agriculture Fishing, and Forestry

- 5.1.4 Construction

- 5.1.5 Distributive Trade

- 5.1.6 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Overview

- 6.2 Company Profiles

- 6.2.1 CH Robinson

- 6.2.2 Total Quality Logistics

- 6.2.3 XPO Logistics Inc.

- 6.2.4 Echo Global Logistics

- 6.2.5 Worldwide Express

- 6.2.6 Coyote Logistics

- 6.2.7 Landstar System Inc.

- 6.2.8 Schneider

- 6.2.9 Suntecktts

- 6.2.10 Globaltranz

- 6.2.11 J.B. Hunt Transport Inc.

- 6.2.12 Hub Group

- 6.2.13 BNSF Logistics LLC

- 6.2.14 Kag Logistics Inc.

- 6.2.15 Transplace*

7 FUTURE OF THE MARKET

8 APPENDIX

9 CREDENTIALS

- 9.1 Illustrative List of Clients

- 9.2 Similar Engagements Within the Industry