メモリ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644659

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

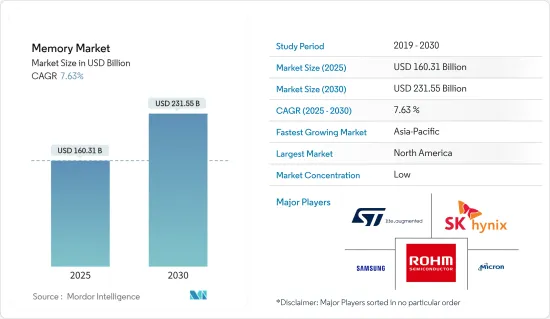

メモリ市場規模は2025年に1,603億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.63%で、2030年には2,315億5,000万米ドルに達すると予測されます。

世界のCOVID-19の大流行は、2020年の初期段階における市場調査のサプライチェーンと生産を大きく混乱させました。製造装置については、この影響はより深刻でした。人手不足のため、アジア太平洋の包装、組立、検査工場の多くが操業を縮小し、一時停止さえしました。これは半導体に依存するエンドユーザー企業にとってボトルネックとなりました。さらに最近では、中国でのCOVID-19関連のロックダウンが再び世界のメモリ市場のサプライチェーンを混乱させました。2021年12月、世界最大級のメモリチップメーカーであるSamsung ElectronicsとMicron Technologyは、中国の西安市におけるCOVID-19の厳格な規制とロックダウンにより、同地域のチップ製造拠点が混乱する可能性があると警告しました。Micron Technologyによると、ロックダウンはデータセンターで広く使用されているDRAMメモリチップの供給に遅れをもたらす可能性があるといいます。

メモリ市場は急速な成長を遂げており、半導体はほとんどの最新技術の基本コンポーネントとなっています。この市場における技術革新と進歩は、結果的にすべての下流技術に直接的な影響を及ぼしています。

全米ケーブル・通信協会は、2020年のコネクテッドデバイスの数は約501億台になると予測しています。すべてのIoTまたはIIoTデバイスには、デバイスの遠隔接続を可能にする先進的半導体メモリチップが搭載されています。さらに、IoTが大きく成長する見込みであることから、メモリ市場の成長にも影響を与えると予想されます。

2025年までに、自動車産業、接続性、通信、データセンターにおける継続的な開発と革新から、市場は大きな恩恵を受けることになります。安全、インフォテインメント、自動車のナビゲーションに使用される電子部品の消費の増加は、さらに市場の成長に寄与します。

半導体メモリ製品は、スマートフォン、薄型モニター、LEDテレビ、民間航空宇宙・軍事システムなどの電子機器全体で幅広く使用されています。メモリ産業は、生体認証機能の進歩からも恩恵を受ける可能性が高いです。また、スマートフォンやウェアラブルガジェットなど、技術的に先進的製品に対する需要の高まりも、調査対象市場の成長を加速させています。

さらに、複数のベンダーがこの技術に投資して優位に立とうとしています。例えば、2022年4月、先進的設計と検証ソリューションを提供する主要技術企業であるKeysight Technologies, Inc.は、SK Hynixが、膨大なデータを管理し、高速データをサポートできる先進的製品の設計に使用されるメモリ半導体の開発を加速するために、KeysightのPCIe(integrated peripheral component to interconnect express)5.0テストプラットフォームを採用したと発表しました。

メモリ市場動向

消費者向け製品が大きな市場シェアを占める見込み

デジタルカメラ、携帯電話、ノートパソコンなど、一般的な民生用電子機器に使用されている高価なシリコンチップよりも少ないコストで、より多くのデータを保存できるようになり、新たなメモリ技術がメモリの可能性を高めています。

世界の半導体鋳造メーカーである台湾のUnited Microelectronics Corporation(UMC)は、28nm CMOS製造プロセスによる組み込み型不揮発性STT-MRAMブロックを提供しており、これにより顧客は、モノのインターネット、ウェアラブル、民生用電子機器セグメントを対象に、低レイテンシ、超高性能、低消費電力の組み込み型MRAMメモリブロックをMCUやSoCに統合できるようになります。

このセグメントでの技術進歩が、調査対象市場の需要を牽引しています。Nanterohのような開発企業は、NRAMと呼ばれる高密度不揮発性メモリを開発しました。このメモリは驚くほど高速で、小さなスペースに大量のストレージを提供し、消費電力は極めて小さいです。NanteroのNRAMがあれば、民生用電子機器ベンダーは未来的とされる新しい消費者向け機器を開発できます。このような開発により、不揮発性メモリの採用は拡大すると予想されます。

このセグメントの新興メモリ技術は、主にウェアラブルデバイスやコネクテッドデバイスが牽引しており、予測期間中により速いペースで成長すると予想されます。Cisco Systems Inc.の予測によると、2022年までに世界で接続されるウェアラブルデバイスの台数は11億500万台に達する可能性があります。

デジタルカメラ、スマートフォン、ゲーム機器など、他の民生用電子機器にも効果的なメモリが必要とされるため、これらのメモリ技術に対する需要はさらに高まると予想されます。Ericssonは、スマートフォンの出荷台数が2022年までに15億7,440万台に達すると予測しています。

南北アメリカが最大の市場シェアを占める

急速に変化する技術と産業を横断する大量のデータ生成により、国内ではより効率的な処理システムのニーズが高まっています。モバイル機器や低消費電力機器、ハイエンドのデータセンターや大規模なオンチップ・キャッシュの出現により、不揮発性で高密度、低エネルギー消費のメモリという、もう一つの優先度の高い需要が出現しています。

メモリ半導体製造技術において、米国はここ数年でDRAMと3D-NANDで競合を取り戻し、米国企業はEUV(極端紫外線)を全面的に採用しています。

米国エネルギー省によると、米国には約300万のデータセンターがあります。データセンターはコンピューティングの新しい単位となっています。DPU(データプロセッシング・ユニット)は、GPU、CPU、DPUが完全にプログラム可能な単一のコンピューティング・ユニットに結合できる、安全で最新のアクセラレーション・データセンターに不可欠な要素です。Nvidiaは、データ管理がデータセンターの中央処理コアの最大30%を消耗していると推定しています。データセンターの需要の増加は、メモリ・コンポーネントの需要も押し上げています。現在、北米では大規模なデータセンタープロジェクトが進行しており、DRAMなどのメモリ需要が高まっています。

さらに、5Gによって膨大な通信データを短時間で伝送することが可能になると予想されており、デバイスはより多くのストレージを必要とすることになります。これはNANDフラッシュの採用を増やすと考えられます。

米国はファクトリーオートメーションと産業制御の主要市場です。FRAMは、高速ランダム・アクセス、高い読み取り・書き込み耐久性、低消費電力を記載しています。ファクトリーオートメーションでは、産業標準のアーキテクチャ、インターフェース、機能、包装により、シンプルなドロップインソリューションが可能になり、コストのかかるシステムの再設計が不要になります。

メモリ産業概要

メモリ市場は、複数のベンダーが国内外市場にメモリを供給しているため、競争が激しいです。市場は適度にセグメント化されているようで、主要ベンダーはM&Aや戦略的提携などの戦略を採用し、市場参入の拡大と市場競合の維持に努めています。同市場の主要企業には、Samsung Electronics、Micron Technology Inc.、SK Hynix Inc.、ROHMなどが挙げられます。市場の最近の動向としては、以下のようなものがあります。

2021年10月-米国のメモリメーカーであるMicron Technologyは、米国での工場拡大の可能性を含め、先進的なメモリ製造、研究開発に今後10年間で全世界で1,500億米ドル以上を投資します。

2021年12月-Micron TechnologyはUnited Microelectronics Corporationとの取引関係の拡大を発表し、将来にわたってモバイル、自動車、重要顧客向けの供給を確保する機会を記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 5GとIoTデバイスの普及拡大

- データセンターにおけるメモリ需要の増加

- コンシューマー・エレクトロニクスと自動車部門からの需要増加

- 市場課題

- パンデミックシナリオと米国と中国の貿易戦争シナリオによるサプライチェーンの短期的課題

第6章 市場セグメンテーション

- タイプ別

- DRAM

- SRAM

- NORフラッシュ

- NANDフラッシュ

- ROM & EPROM

- その他

- 用途別

- コンシューマー製品

- PC/ノートPC

- スマートフォン/タブレット

- データセンター

- 自動車

- その他

- 地域別

- 南北アメリカ

- 欧州

- 中国

- 日本

- アジア太平洋

第7章 競合情勢

- 企業プロファイル

- Samsung Electronics Co. Ltd

- Micron Technology Inc.

- SK Hynix Inc.

- ROHM Co. Ltd.

- STMicroelectronics NV

- Maxim Integrated Products Inc.

- IBM Corporation

- Cypress Semiconductor Corporation

- Intel Corporation

- Nvidia Corporation

- Kioxia Corporation

- Vendor Ranking

第8章 投資分析

第9章 市場の将来

目次

The Memory Market size is estimated at USD 160.31 billion in 2025, and is expected to reach USD 231.55 billion by 2030, at a CAGR of 7.63% during the forecast period (2025-2030).

The COVID-19 pandemic across the globe significantly disrupted the supply chain and production of the market studies in the initial phase of 2020. For fabrication units, this impact was more severe. Owing to the labor shortages, many of the package, assembly, and testing plants in the Asia Pacific region reduced and even suspended operations. This created a bottleneck for end-user companies that depend on semiconductors. More recently, COVID-19-related lockdowns in China again disrupted the Global Memory Market supply chain. In December 2021, Samsung Electronics and Micron Technology, two of the world's largest memory chip producers, warned that strict COVID-19 curbs and lockdowns in the Chinese city of Xian might disrupt their chip manufacturing bases in the area. According to Micron Technology, the lockdowns could cause delays in the supply of DRAM memory chips, widely used in data centers.

The memory market is witnessing rapid growth, with semiconductors emerging as the basic building blocks of most modern technologies. The innovations and advancements in this market are resulting in a direct impact on all downstream technologies.

The National Cable and Telecommunications Association projected that the number of connected devices in 2020 will be around 50.1 billion. Every IoT or IIoTdevice contains sophisticated semiconductor memory chips that permit devices to achieve remote connectivity. Moreover, as the IoT is poised to grow significantly, it is expected to impact the growth of the memory market as well.

By 2025, the market is set to experience significant benefits from the ongoing development and innovation in the automotive industry, connectivity, communications, and data centers. The rise in the consumption of electronic components used in the navigation of safety, infotainment, and automobiles further contributes to the market's growth.

Semiconductor memory products are used extensively across electronic devices, such as smartphones, flat-screen monitors, LED TVs, and civil aerospace and military systems. The memory industry is also likely to benefit from progress in biometrics capabilities. The growing demand for smartphones and technologically advanced products, such as wearable gadgets, etc., is also accelerating the growth of the market studied.

Further, several vendors are investing in this technology to gain an advantage. For instance, in April 2022, Keysight Technologies, Inc., a leading technology company that provides advanced design and validation solutions, announced that SK Hynix selected Keysight's integrated peripheral component to interconnect express (PCIe) 5.0 test platforms for speeding up the development of memory semiconductors used for designing advanced products capable of managing huge data and supporting high data speeds and.

Memory Market Trends

Consumer Products is Expected to Hold Significant Market Share

The emerging memory technologies have enhanced the potential of memory by allowing the storage of more data at a lesser cost than the expensive-to-build silicon chips used by popular consumer electronic gadgets, including digital cameras, cell phones, notebooks, etc.

Taiwan's United Microelectronics Corporation (UMC), a global semiconductor foundry, is providing embedded non-volatile STT-MRAM blocks based on a 28nm CMOS manufacturing process, which will enable customers to integrate low latency, very high performance, and low power embedded MRAM memory blocks into MCUs and SoCs, targeting the Internet of Things, wearable, and the consumer electronics sector.

The technological advancements in the field are driving the demand for the market studied. Companies like Nanterohave developed high-density non-volatile memory called NRAM, which is incredibly fast, offer huge amounts of storage in a small space, and consumes very little power. With Nantero'sNRAM, consumer electronics vendors can develop new consumer devices that are considered to be futuristic. With such developments, the adoption of non-volatile memory is expected to grow.

The emerging memory technologies in the sector are mainly driven by wearable and connected devices that are expected to grow at a faster pace during the forecast period. Cisco Systems estimates that the number of connected wearable devices worldwide could reach 1,105 million units by 2022.

The demand for these memory technologies is further expected to rise owing to the effective memory requirement for other consumer electronics devices such as digital cameras, smartphones, gaming devices, etc. Ericsson estimates that the shipment of smartphone units could reach 1574.4 million by 2022.

The Americas Account for the Largest Market Share

Rapidly changing technologies and high data generation across industries are creating a need for more efficient processing systems in the country. With the advent of mobile and low-power devices, as well as high-end data centers and large on-chip caches, another high-priority demand has emerged: non-volatile, dense, and low-energy-consuming memories.

In memory semiconductor manufacturing technology, the United States has regained its competitiveness in DRAM and 3D-NAND in the last few years, and US companies are fully embracing EUV (Extreme Ultraviolet).

According to the US Department of Energy, there are about 3 million data centers in the United States. The data center has become the new unit of computing. DPUs (Data Processing Units) are the essential elements of secure and modern accelerated data centers in which GPUs, CPUs, and DPUs are able to combine into a single computing unit that is fully programmable. Nvidia estimates that data management drains up to 30% of the central processing cores in data centers. The increasing demand for data centers is also boosting the demand for memory components. Currently, large data center projects in North America have contributed to the strong demand for memory, such as DRAM.

Furthermore, It is expected that 5G will enable the transmission of a huge amount of telecommunications data in a short time, which also means devices would need more storage. This would increase the adoption of NAND flash.

The US is a major market for factory automation and industrial control. FRAM offers fast random access, high read and write endurance, and low power consumption. In factory automation, the industry-standard architecture, interface, features, and packages can enable a simple drop-in solution that can eliminate the costly re-designs of the system.

Memory Industry Overview

The Memory Market is highly competitive owing to multiple vendors providing memory to the domestic and international markets. The market appears to be moderately fragmented, with the significant vendors adopting strategies for mergers and acquisitions and strategic partnerships, among others, to expand their reach and stay competitive in the market. Some major players in the market are Samsung Electronics Co. Ltd, Micron Technology Inc., SK Hynix Inc., and ROHM Co. Ltd., among others. Some of the recent developments in the market are:

October 2021 - Micron Technology, a US-based memory manufacturer, will invest more than USD 150 billion worldwide over the next decade in advanced memory manufacturing, research, and development, including potential United States-based fab expansion.

December 2021 - Micron Technology announced an expansion of its business relationship with United Microelectronics Corporation, providing Micron the opportunities to secure supply for mobile, automotive, and critical customers into the future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Penetration of 5G and IoT Devices

- 5.1.2 Growing Memory Requirement in Data Centers

- 5.1.3 Rising Demand from Consumer Electronics and Automotive Sectors

- 5.2 Market Challenges

- 5.2.1 Short term supply chain challenges due to the pandemic scenario and the US-China Trade war scenario

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 DRAM

- 6.1.2 SRAM

- 6.1.3 NOR Flash

- 6.1.4 NAND Flash

- 6.1.5 ROM & EPROM

- 6.1.6 Others

- 6.2 By Application

- 6.2.1 Consumer Products

- 6.2.2 PC/Laptop

- 6.2.3 Smartphone/Tablet

- 6.2.4 Data Center

- 6.2.5 Automotive

- 6.2.6 Other Applications

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 China

- 6.3.4 Japan

- 6.3.5 Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Samsung Electronics Co. Ltd

- 7.1.2 Micron Technology Inc.

- 7.1.3 SK Hynix Inc.

- 7.1.4 ROHM Co. Ltd.

- 7.1.5 STMicroelectronics NV

- 7.1.6 Maxim Integrated Products Inc.

- 7.1.7 IBM Corporation

- 7.1.8 Cypress Semiconductor Corporation

- 7.1.9 Intel Corporation

- 7.1.10 Nvidia Corporation

- 7.1.11 Kioxia Corporation

- 7.2 Vendor Ranking

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日