北米の決済市場:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644649

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

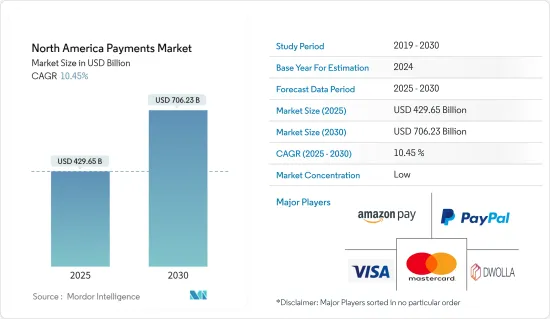

北米の決済市場規模は2025年に4,296億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.45%で、2030年には7,062億3,000万米ドルに達すると予測されます。

米国では、American Expressは重要なクレジットカード会社です。American Expressは、卓越した顧客サービスと最高のインセンティブを提供することで知られています。American Expressは、超エリートの法人向け旅行カードから日常的な特典まで、あらゆるカード会員に適したクレジットカードを用意しています。クレジットカード発行会社(または提供銀行)とは、クレジットカードを発行する機関(銀行または信用組合)のことです。米国最大の銀行はチェースとシティであり、カナダ最大の銀行はTDとRBCです。発行銀行は、金利、限度額、国際手数料などを設定する権限を持っています。

主要ハイライト

- バイオメトリクス認証技術を取引に利用することは、決済産業で大きな潮流となっています。バイオメトリクス認証は、正確性、有効性、安全性を一体化して提供する不可欠な決済技術です。例えば、2023年 12月、FortressPayはエンタープライズ対応のバイオメトリクス決済プラットフォームを発表しました。新しいPayment Identityプラットフォームにより、FortressPayは決済詐欺を排除しながら、摩擦のない顧客体験を提供することを目指しています。

- 決済産業は、消費者部門とビジネス部門の両方で大きく変化しています。リアルタイム決済の台頭、顧客データへのアクセスと活用の拡大、デジタル決済と従来型決済の間での消費者の選択肢の増加、インターネット巨大企業と伝統的銀行との間の競争と協力の激化は、いずれも注目のテーマです。こうした新たな、現在進行中の動向は、イノベーションと顧客の受容性を促進するため、企業に事業戦略の見直しを求めています。

- 北米のデジタル決済セグメントにおける技術的進歩により、市場の魅力的な開拓が見込まれます。このプラットフォームでは、デビットカードとクレジットカードを併用することで、金利や追加手数料なしでオンライン購入の決済を分割できます。その結果、このプラットフォームは、個々のカードにかかるコスト負担を軽減し、財務上のプライバシーを高め、信用格付けを高める上でユーザーを支援すると期待されています。

- COVID-19の流行は北米の決済産業に大きな影響を与えました。ロックダウンや事業所の閉鎖により、人々は対面での買い物ができなくなり、流行前の取引方法も変化しました。景気や個人金融への懸念から全体的な支出は減少したもの、人々はオンラインでより多くの金額を消費し、現金からデジタル決済への移行を早めました。カード、スマートフォン、ウェアラブル端末などの非接触型決済ソリューションが大幅に増加したようです。

北米の決済市場の動向

デジタルウォレット決済の利用増加

- 北米におけるデジタルウォレット決済の利用増加は、消費者行動の大きな変化と、金融サービスの広範なデジタル変革を反映しています。技術が人々の財務管理方法を形成し続ける中、デジタルウォレットは従来の決済方法に代わる便利で安全、かつ汎用性の高い選択肢として台頭しています。

- また、北米の規制環境はデジタルウォレットの台頭に対応し、これらの決済方法が既存の金融規制と整合するようになりました。各国政府が金融サービスにおけるイノベーションを促進することの重要性を認識する中、規制の枠組みはデジタル決済技術の成長を支援する環境を提供するように進化してきました。

- さらに、eコマースプラットフォームはさまざまな支払方法に対応できるため、主要クレジットカードやギフトカードなど、より多くのユーザーがビジネスにアクセスしやすくなっています。Amazon、eBay、Shopifyなどのeコマースプラットフォームは、オンライン決済処理手数料を賄うため、月額手数料や取引手数料を頻繁に請求します。

- 米国におけるeコマースの売上は、デジタル決済の体験が向上するにつれて増加しています。この増加は、消費者がオンラインショッピングをより快適に利用するようになり、モバイルやハンドヘルド機器の利用が増えたことを反映しています。

- 北米の消費者の間では、BNPL(buy-now-pay-later)サービスが代替決済ソリューションとして人気を集めています。米国の消費者がBNPLを利用する理由はさまざまで、通常なら手が届かないような商品を購入したり、クレジットカードの利息を避けたり、信用調査なしでお金を借りたりするためです。市場参入企業はBNPLの普及拡大のために様々な戦術を実施しています。例えば、スプリットは2023年5月、加盟店にBNPL(Buy Now, Pay Later)ソリューションを提供するため、ビザとの提携を発表しました。両社は、Splititが提供する分割払いをVisa Instalmentsと組み合わせてBNPLソリューションとする契約を締結し、今年下半期に一部の市場で検査的に導入する予定です。

米国が市場シェアの過半数を占める

- 米国とカナダでは、オフラインでもオンラインでも、クレジットカードが最もよく使われる決済手段であり、デビットカードはその次です。デジタル決済体験の充実により、同国のeコマース売上は拡大しています。この成長は、顧客がオンライン購入に慣れてきたこと、モバイル機器やハンドヘルド機器の利用が増えたことを反映しています。

- さらに、米連邦準備制度理事会(FRB)は米国のACHシステムをカナダ、英国、ユーロ圏、メキシコ、パナマの現地決済システムに統合し、個人や企業が米国の銀行口座から他国の銀行口座に現金を直接移動できるようにしました。金融技術企業はクロスボーダー決済、特にピアツーピア決済に急速に参入しています。例えば、金融技術企業は送金セグメントに参入し、ユーザーが銀行口座やデビットカード、クレジットカードを使ってオンラインで「モバイルウォレット」に資金を供給し、そのまま海外のモバイルウォレットに送金できるようにしています。

- さらに、リテール即時決済システムは少額の銀行間送金を実行するため、従来の銀行決済システムではリテール送金の決済に数日かかる場合もあったが、これとは対照的に、ほぼ即時に送金が可能になります。他のリテール決済システムと同様、即時決済システムも銀行預金を利用することが多いが、最終的には中央銀行の準備金残高で決済されます。2017年に始まったクリアリングハウスのRTPネットワーク(RTP)や、連邦準備制度理事会(FRB)が2023年の導入を目指すFedNowサービスなどがあります。

- デジタル決済市場の成長により、モバイルコマースは、特にキャッシュレス決済の受け入れという点で、実店舗型ビジネスのあり方も変えてきました。例えば、Apple Pay、Samsungペイ、Googleペイは、それぞれの国の市場リーダーと競合する主要な競争相手です。数カ国でモバイル決済が一貫して増加していることから、北米のデジタル決済市場は急速に拡大しています。

北米の決済産業概要

北米の決済市場は競争が激しく、Apple Pay、Samsung Pay、Amazon Pay、Google Payのような主要企業が参入しています。企業もまた、事業拡大と自国民への電子商取引プラットフォームの提供を目的に、アフリカ大陸への投資やパートナーシップの締結を行っています。

- 2023年6月-Amazon PayはBNPLアウトレットAffirmとの提携を発表。この提携により、Amazon Payはオンラインストアを利用する中小企業オーナーにBNPL(buy-now-pay-later)サービスを記載しています。

- 2023年3月-Apple Inc.が米国でApple Pay Laterを発表。利用者の財務の健全性を考慮して設計されており、利用者は購入した商品を4回に分けて6週間にわたって無利息・手数料なしで支払うことができます。ユーザーは、Apple Walletの便利な1つの場所で、Apple Pay Laterのローンを簡単に追跡、管理、返済することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 北米における決済環境の進化

- 北米におけるキャッシュレス取引の拡大に関連する主要市場動向

- COVID-19が北米の決済市場に与える影響

第5章 市場力学

- 市場促進要因

- Mコマースの台頭を含むeコマースの高い普及率

- 決済市場におけるスマートフォンの成長と電子化への取り組み

- リアルタイム決済の増加

- 市場課題

- データセキュリティリスク

- 市場機会

- キャッシュレス社会への転換

- 決済市場における新たな参入企業の登場が、普及拡大につながるイノベーションを促進する可能性があります。

- デジタル決済産業における主要規制と基準

- 主要事例と使用事例の分析

- 北米の決済産業に関する主要な人口動向とパターンの分析(人口、インターネット普及率、銀行普及率/非銀行人口、年齢・所得などを網羅)

- 北米における顧客満足度重視の高まりと世界の動向の融合に関する分析

- 北米における現金離れと非接触決済の台頭に関する分析

第6章 市場セグメンテーション

- 決済モード別

- 販売時点情報管理(POS)

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- 現金

- その他

- オンライン販売

- カード決済(デビットカード、クレジットカード、銀行融資プリペイドカードを含む)

- デジタルウォレット(モバイルウォレットを含む)

- その他(代金引換、銀行振込、Buy Now, Pay Laterを含む)

- 販売時点情報管理(POS)

- エンドユーザー産業別

- 小売

- エンターテインメント

- 医療

- ホスピタリティ

- その他

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- PayPal Holdings Inc.

- MasterCard Incorporated(MasterCard)

- Dwolla

- Amazon.com Inc.

- Visa Inc.

- Alipay.com Co. Ltd

- Alphabet Inc.(Apple Pay)

- Google Pay(Google LLC)

- Beacon Payments LLC

- Interac Corp.

第8章 投資分析

第9章 市場の将来展望

目次

The North America Payments Market size is estimated at USD 429.65 billion in 2025, and is expected to reach USD 706.23 billion by 2030, at a CAGR of 10.45% during the forecast period (2025-2030).

In the United States, American Express is a significant credit card corporation. It is well-known for offering exceptional customer service as well as some of the greatest incentives. From ultra-elite corporate travel cards to daily rewards, American Express has a credit card to fit every cardholder. Credit card issuers (or providing banks) are the institutions (banks or credit unions) from whom credit cards are obtained. The largest banks in the United States are Chase and Citi, while the largest in Canada are TD and RBC. The issuing bank has the authority to set the interest rate, the limit, international fees, and so on.

Key Highlights

- Using biometric authentication technologies in transactions is a major trend that is gaining traction in the payments industry. Biometric authentication is an essential payment technique that combines and provides accuracy, effectiveness, and security in a single package. For instance, in December 2023, FortressPay announced the launch of an enterprise-ready biometric payment platform. With its new Payment Identity platform, FortressPay aims to provide a frictionless customer experience while eliminating payment fraud.

- The payments industry is significantly shifting in both the consumer and business sectors. The rise of real-time payments, more access to and use of customer data, increasing consumer choice among digital and conventional payment methods, and growing rivalry and collaboration between internet behemoths and traditional banks are all hot subjects. These new and ongoing trends are requiring firms to reassess their business strategies in order to foster innovation and client acceptability.

- Technical advancements in the North American digital payment sector are projected to generate attractive development prospects for the market. This platform allows you to divide payments for online purchases using a combination of debit and credit cards with no interest or additional fees. As a result, the platform is expected to assist users in reducing the cost load on individual cards, increasing financial privacy, and building credit ratings.

- The COVID-19 pandemic significantly impacted the payment industry in North America. Lockdowns and business closures prevented people from making in-person purchases and altered how they transacted before the outbreak. While overall spending fell due to concerns about the economy and personal finances, people spent more money online, hastening the transition from cash to digital payments. There appears to have been a significant increase in contactless payment solutions, such as cards, smartphones, and wearable devices.

North America Payments Market Trends

Increasing use of digital wallets payments

- The increasing use of digital wallet payments in North America reflects a significant shift in consumer behavior and the broader digital transformation of financial services. As technology continues shaping how people manage their finances, digital wallets have emerged as a convenient, secure, and versatile alternative to traditional payment methods.

- Also, the regulatory environment in North America has adapted to accommodate the rise of digital wallets, ensuring that these payment methods align with existing financial regulations. As governments recognize the importance of fostering innovation in financial services, regulatory frameworks have evolved to provide a supportive environment for the growth of digital payment technologies.

- Furthermore, the e-commerce platforms can accept various payment methods, making it easier for more users to access the business, such as major credit cards, gift cards, etc. E-commerce platforms such as Amazon, eBay, and Shopify frequently charge monthly and transaction fees to cover online payment processing fees.

- E-commerce sales in the United States are increasing as digital payment experiences improve. This rise reflects consumers' growing comfort with online shopping and their increased use of mobile and handheld devices.

- The buy-now-pay-later (BNPL) service is gaining popularity among North American consumers as an alternative payment solution. Consumers in the United States utilize BNPL for a variety of reasons, including purchasing items that would otherwise be beyond reach, avoiding interest on credit cards, and borrowing money without a credit check. Market participants are implementing various tactics to expand the adoption of BNPL. For example, in May 2023, Splitit announced its partnership with visa to offer merchants a buy now, pay later (BNPL) solution. Both the companies had signed an agreement in which Splitit's installments-as-a-service offering is combined with Visa Instalments to form a BNPL solution that will be piloted in select markets during the second half of the year

United States to hold a majority market share

- Credit cards are the most commonly used payment method in the United States and Canada, both offline and online, with debit cards coming in second. With the enhancement of digital payment experiences, the country's e-commerce sales are expanding. This growth reflects customers' growing comfort with online buying and their increased usage of mobile and handheld devices.

- Additionally, the Federal Reserve has integrated the United States' ACH system into local settling systems in Canada, the United Kingdom, the Eurozone, Mexico, and Panama, allowing individuals and companies to move cash directly from U.S. bank accounts to bank accounts in other countries. Financial technology firms are rapidly venturing into cross-border payments, notably peer-to-peer payments. Financial technology firms, for example, are joining the remittance sector, allowing users to fund "mobile wallets" online using their bank accounts and debit or credit cards and sending money straight to overseas mobile wallets.

- Moreover, retail instant payment systems execute small-value interbank transfers such that money is available almost quickly, as contrast to the possibly multiday settlement wait for retail transfers on some traditional bank payment systems. Like other retail payment systems, immediate payment systems often employ bank deposit money but eventually settle in central bank reserve balances. include the Clearing House's RTP Network (RTP), which began in 2017, and the FedNow Service, which the Federal Reserve aims to implement in 2023.

- Due to the growth of the digital payment market, mobile commerce has also changed the way brick-and-mortar businesses operate, particularly in terms of accepting cashless payments. Apple Pay, Samsung Pay, and Google Pay, for example, are among the leading competitors competing with market leaders in their respective countries. With consistent increases in mobile payment in several countries, the North American digital payment market is expanding rapidly.

North America Payments Industry Overview

The North American Payments market is highly competitive, with key players such as Apple Pay, Samsung Pay, Amazon Pay, Google Pay, and many others in the region developing new e-commerce solutions for a wide range of end-user applications. Companies are also investing and forming partnerships in the continent to expand their businesses and provide e-commerce platforms to the country's people.

- June 2023 - Amazon Pay announced its partnership with BNPL outlet Affirm. With this partnership, Amazon Pay offers buy-now-pay-later (BNPL) services to small business owners using its online store.

- March 2023 - Apple Inc. introduced Apple Pay Later in the U.S. designed with users' financial health, It also allows users to split purchases into four payments, spread over six weeks with no interest and no fees. Users can easily track, manage, and repay their Apple Pay later loans in one convenient location in Apple Wallet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in North America

- 4.5 Key market trends pertaining to the growth of cashless transaction in North America

- 4.6 Impact of COVID-19 on the payments market in North America

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, Including the Rise of M-commerce

- 5.1.2 Smartphone Growth and Electronic Initiatives in the payment market

- 5.1.3 Increase in Real-Time Payments

- 5.2 Market Challenges

- 5.2.1 Data security risks

- 5.3 Market Opportunities

- 5.3.1 Transformation to a Cashless Society

- 5.3.2 New players in the payment market may drive innovation leading to greater adoption.

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in North America (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in North America

- 5.8 Analysis of cash displacement and rise of contactless payment modes in North America

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Others

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 PayPal Holdings Inc.

- 7.1.2 MasterCard Incorporated (MasterCard)

- 7.1.3 Dwolla

- 7.1.4 Amazon.com Inc.

- 7.1.5 Visa Inc.

- 7.1.6 Alipay.com Co. Ltd

- 7.1.7 Alphabet Inc. (Apple Pay)

- 7.1.8 Google Pay (Google LLC)

- 7.1.9 Beacon Payments LLC

- 7.1.10 Interac Corp.

8 Investment Analysis

9 Future Outlook of the Market

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日