|

市場調査レポート

商品コード

1644638

欧州の倉庫自動化-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の倉庫自動化-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

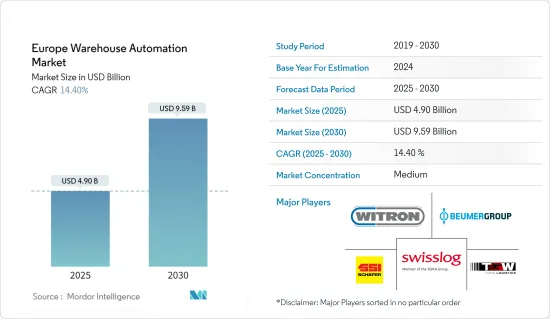

欧州の倉庫自動化市場規模は2025年に49億米ドルと推定され、予測期間中(2025~2030年)のCAGRは14.4%で、2030年には95億9,000万米ドルに達すると予測されます。

さらに、倉庫用ロボットはこれまで膨大な配備が行われてきたが、COVID-19は配備速度を大幅に向上させる可能性が高いです。COVID-19の発生により、倉庫所有者は自動化とロボットの導入スケジュールを早めることを検討しています。自動化の導入に成功した企業はまた、eコマースのニーズの高まりに対応するために生産性を高めつつ、作業員の相互作用を制限することによって、より安全な職場を確立することを実証しています。最近のeコマースの増加により、何千もの実店舗が閉店しています。

主要ハイライト

- 欧州では、パンデミック以降、倉庫自動化の伸びが拡大しました。これは、eコマースの増加が止まらないように見えることと、労働力不足が続き人件費が高騰していることという、相互に関連し合った2つの動向によるものです。欧州の倉庫ロボット市場は、倉庫数の増加と倉庫自動化への支出の増加、人件費の上昇、拡大可能な技術ソリューションの利用可能性によって牽引されてきました。

- 需要とOEMとシステムインテグレーターの存在に関して、ドイツは倉庫自動化の主要国のひとつです。OEMは欧州に多く、ドイツ、イタリア、フランス、オランダ、スペインに拠点があります。中・東欧は、欧州の中でも急速に成長している地域で、ポーランドとチェコ共和国は、有望な経済ポテンシャルを持つ物流ハブとして台頭してきています。しかし、ロシア・ウクライナ紛争を含む現在の地政学的状況により、拡大や投資計画は保留されています。

- モノのインターネットは、在庫と倉庫の自動化開発を推進しています。モノのインターネットは、倉庫を接続された協調システムへと変貌させることに貢献しています。2021年以降、低コスト化とIoTセンサの強化により、倉庫でのIoT利用が促進されると予想されます。例えば、2020年5月、ドイツの物流会社DHLは、米国の技術企業であるシスコと提携し、欧州の3つの大規模倉庫業務にIoTを導入したと発表しました。

- しかし、倉庫管理の自動化は、事業全体の支出を削減し、製品配送の不具合をなくすという点では非常に有益です。このような利点があるにもかかわらず、注目すべき3PL事業者であり、倉庫自動化技術の主要なエンドユーザーであるDHLによれば、倉庫の80%は、いまだに自動化を支援することなく手作業で運営されています。さらに、コンベア・ベース、ソーター・ベース、ピック・アンド・プレイス倉庫は、全倉庫の15%を占めています。これに対し、自動化されている倉庫は全体の5%に過ぎないです。

欧州の倉庫自動化市場動向

自律移動ロボット(AMR)が欧州で人気を集める

- 欧州の倉庫自動化開発には、満杯の棚を移動できる自律型ロボットの使用と、繁忙期の自動化を支援するフォークリフトの更新の2つがあります。従来、移動ロボットによって処理されていた作業を移し、引き継ぐために、コンベア、手動フォークリフト、カート、牽引装置などを使用することができます。その他の用途としては、梱包、運搬、仕分けなどがあります。

- 欧州各地の物流用途では、自律移動ロボット(AMR)が自動搬送車(AGV)に取って代わりつつあります。AMRはAGVとは異なり、慣性測定装置(IMU)、レーザー走査距離計、2Dと3Dカラーカメラ、モーター・コントローラとリンクした、より先進的オンボード・コンピューターを備えています。AMRはまた、在庫管理に新たな可能性をもたらしています。これらのデバイスは、RFIDタグが付けられた製品や機器と組み合わせることで、倉庫で決められたスケジュールで自律的に在庫掃討を実行することができます。

- 例えば、英国を拠点とするIconsysは、iAM-R(Iconsys Autonomous Mobile Robot)を発表し、自律移動ソリューションに進出しました。これは同社の顧客に自律型ロボットソリューションを提供するためのものです。

- 2022年5月、IFOYにノミネートされ、フルフィルメント倉庫向け自律移動ロボット(AMR)のリーダーであるLocus Roboticsは、倉庫用AMRラインの拡充を発表しました。これらの新しい形態ファクターはLocus Originロボットに加わり、eコマース、ケースピッキング、パレットピッキングから、より大きく重いペイロードを必要とするシナリオまで、今日のフルフィルメントや流通施設におけるあらゆる製品移動のニーズに対応するAMRの包括的なファミリーを形成します。

- 2022年6月、シュトゥットガルトで開催されたLogiMATで、生産・倉庫ロジスティクス向けハイテク無人搬送車(AGV)のリーディング・メーカーでありインテグレーターであるek roboticsは、柔軟でインテリジェントな自律移動ロボット(AMR)の世界のリーディング・カンパニーであるOTTO Motorsとの世界の技術提携を発表しました。両社が提供するAGVハードウェアとAMRソフトウェアの組み合わせにより、世界中の製造・倉庫産業の顧客は恩恵を受けることになります。

自動車産業における自動化保管・検索システム(AS/RS)の高い採用率

- Mercedes-Benz、Volvo、Aston Martin、Bentley, Porsche、Porsche、ランボルギーニ、フェラーリなど、多くの有名自動車ブランドが欧州に拠点を置いています。ドイツ、フランス、英国にある数多くの自動車生産工場は、競合を維持するためにAS/RSシステムに大きく依存しています。英国にあるExmac Automationは、アストンマーチン、ベントレイ、ジャガー、IBCの車両にストレージソリューションを提供しています。

- 例えば、英国の大手AS/RSソリューション・プロバイダーであるIndustoreは、倉庫や大小の保管庫で利用される製品を幅広く取り揃えています。AS/RSのもう一つの主要企業であるExMac Automationは、国内の様々な産業に自動保管・検索クレーンシステム(大容量のミニロードクレーンやラッキングからハイベイ倉庫クレーンまで)を提供しています。

- 欧州委員会は世界の技術調和を支援し、自動車産業が競合と技術的リーダーシップを維持できるよう、研究開発への資金提供を申し出ています。さらに、ACEAの調査によると、欧州連合(EU)の人口1,000人当たりの自動車保有台数は569台。ルクセンブルクの自動車密度はEUで最も高く(人口1,000人当たり694台)、ラトビアは最も低いです。OICAによると、欧州の乗用車総販売台数は2020年に1,416万台に達します。

- 英国の自動車サプライチェーンは需要主導型であるため(自動車内のカスタマイズレベルの向上を含む)、OEMサプライヤーはより柔軟性の高い倉庫自動化を選択せざるを得ないです。自動車製造プロセスにおけるAS/RSシステムと自動化の採用の増加、デジタル化とAIの出現は、オランダの自動車セクターにおけるデジタル化の需要を促進する主要要因の一部です。

- さらに、ドイツは自動マテリアルハンドリングシステムの世界最大のユーザーの1つです。国際ロボット連盟(IFR)によると、ドイツのロボット密度は韓国、日本に次いで最も高い(労働者1万人当たり294台)。これらの要因により、欧州全体で倉庫自動化の需要が高まると考えられます。

欧州の倉庫自動化産業概要

欧州の倉庫自動化市場は、競合情勢によって細分化されています。Dematic Group、Swisslog Holding AG、Swisslog Holding AG(KUKA AG) WITRON、Logistik+Informatik GmbH SSI Schaefer AG BEUMER Group GmbH &Co.KG、TGW Logistics Group GmbH、ユングハインリッヒAGなどが、このセグメントにおける地域の重要な競争相手です。

市場のかなりのシェアを占めるこれらの主要な競合他社は、新しい国々での消費者基盤の拡大に集中しています。さらに、倉庫オートメーションセグメントの市場参入企業は、製品発売、買収、提携などの主要戦略を駆使しています。以下は最近の動向です。

- 2022年2月-DHL Supply Chainは、ドイツのブラウンシュヴァイクにあるオムニチャネルオークションサイト1-2-3.tvに、ロボットピッキングを備えた初の完全自動化オートストアロジスティクスシステムを導入しました。オートストアシステムは、ロジスティクス技術企業であるエレメント・ロジックによって構築され、ロボット・ピッキングとソフトウェアソリューションを使用して、各注文の処理速度を向上させ、業務効率を改善し、その場所の保管容量を最大化します。

- 2021年11月-Honeywell Intelligrated warehouse automationは、より迅速で正確なサプライチェーンを可能にする技術に対する需要の高まりに応えるため、新たな高度研究開発(R&D)検査センターを設立する計画を発表しました。Honeywellのハードウェアとソフトウェアのエンジニアは、この拠点で物流企業が利用する斬新な倉庫自動化システムを作成、試作、テストできるようになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- 倉庫投資のシナリオ

- 倉庫自動化市場に対するマクロ経済要因の影響

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- eコマース産業の急成長と顧客の期待

- 製造の複雑化と技術の利用可能性の増加

- 自動化とマテリアルハンドリングの需要を促進するインダストリー4.0投資

- 市場課題

- 高額な設備投資

- 厳しい規制要件

第6章 市場セグメンテーション

- コンポーネント

- ハードウェア

- 移動ロボット(AGV、AMR)

- 自動保管・検索システム(AS/RS)

- 自動コンベア・仕分けシステム

- デパレタイジング/パレタイジングシステム

- 自動認識・データ収集(AIDC)

- ピースピッキングロボット

- ソフトウェア(倉庫管理システム(WMS)、倉庫実行システム(WES))

- サービス(付加価値サービス、メンテナンスなど)

- ハードウェア

- エンドユーザー

- 飲食品(製造施設、配送センターを含む)

- 郵便・小包

- 食料品

- 一般商品

- アパレル

- 製造業(耐久性と非耐久性)

- その他

- 国名

- 英国

- ドイツ

- フランス

- その他の欧州

第7章 競合情勢

- 企業プロファイル

- Swisslog Holding AG(KUKA AG)

- WITRON Logistik+Informatik GmbH

- SSI Schaefer AG

- BEUMER Group GmbH & Co. KG

- TGW Logistics Group GmbH

- Kion Group AG(Dematic Group)

- Knapp AG

- Jungheinrich AG

- Vanderlande Industries BV

- Mecalux SA

第8章 投資分析

第9章 今後の市場展望

The Europe Warehouse Automation Market size is estimated at USD 4.90 billion in 2025, and is expected to reach USD 9.59 billion by 2030, at a CAGR of 14.4% during the forecast period (2025-2030).

Furthermore, whereas warehouse robots have had enormous deployments, COVID-19 is likely to significantly increase deployment speed. The COVID-19 outbreak has prompted warehouse owners to explore expediting their automation and robotics implementation timelines. Those who have successfully adopted automation have also demonstrated the establishment of safer workplaces by limiting worker interactions while raising productivity to meet rising e-commerce needs. Thousands of brick-and-mortar stores have closed their doors due to the recent increase in e-commerce.

Key Highlights

- In Europe, the warehouse automation growth increased post-pandemic. This results from two interconnected trends: a seemingly unstoppable rise in e-commerce and a persistent labor shortage resulting in rising labor prices. The market for warehouse robots in Europe has been driven by the growing number of warehouses and increased expenditures on warehouse automation, rising labor costs, and the availability of scalable technical solutions.

- Regarding demand and the presence of OEMs and System Integrators, Germany is one of the leading countries in warehouse automation. OEMs are well-represented in Europe, with strongholds in Germany, Italy, France, the Netherlands, and Spain. Central and Eastern Europe is a rapidly growing region within Europe, with Poland and the Czech Republic emerging as logistical hubs with promising economic potential. However, expansion and investment plans have been put on hold due to the present geopolitical circumstances, including the Russia-Ukraine conflict.

- The Internet of Things is driving inventory and warehouse automation developments. It's contributing to the transformation of the warehouse into a connected and coordinated system. In 2021 and beyond, lower costs and enhanced IoT sensors are expected to boost the use of IoT in warehouses. For Instance, In May 2020, DHL, a German logistics company, said that it had partnered with Cisco, a US technology company, to introduce IoT to three large warehouse operations across Europe.

- However, warehousing automation is extremely beneficial when it comes to lowering overall business expenditures and eliminating product delivery faults. Despite the benefits, 80 percent of warehouses are "still manually operated with no supporting automation," according to DHL, a notable 3PL business and a major end-user of warehouse automation technologies. Furthermore, conveyor-based, sorter-based, and pick-and-place warehouses account for 15% of all warehouses. In comparison, only 5% of today's warehouses are automated.

Europe Warehouse Automation Market Trends

Autonomous Mobile Robots (AMRs) are Gaining Popularity Throughout Europe

- Two European warehouse automation developments include using autonomous robots capable of transferring filled shelves and updating forklifts to help automation during busy periods. To transfer and take over activities traditionally handled by mobile robots, conveyors, manual forklifts, carts, and towing devices can all be used. Other applications include packing, transportation, and sorting.

- Autonomous mobile robots (AMRs) in logistical applications across Europe are displacing automatic guided vehicles (AGVs). AMRs, unlike AGVs, have more advanced onboard computers linked to inertial measuring units (IMU), laser scanning range finders, 2D and 3D color cameras, and motor controllers. AMR also opens up new possibilities for inventory management. These devices may now execute inventory sweeps autonomously at warehouse-determined schedules when paired with RFID-tagged products and equipment.

- For instance, the United Kingdom-based Iconsys expanded into autonomous mobile solutions with the launch of its iAM-R (Iconsys Autonomous Mobile Robot). It is designed to provide autonomous robotic solutions to the company's customers.

- In May 2022, Locus Robotics, a 2022 IFOY nominee and leader in autonomous mobile robots (AMRs) for fulfillment warehouses, announced the expansion of its warehouse AMR line. These new form factors join the Locus Origin robot to form a comprehensive family of AMRs that handle the full range of product movement needs in today's fulfillment and distribution facilities, from e-commerce, case-picking, and pallet-picking to scenarios needing larger, heavier payloads.

- In June 2022, At LogiMAT in Stuttgart, ek robotics, the leading manufacturer and integrator of high-tech automated guided vehicles (AGVs) for production and warehouse logistics, announced a global technology partnership with OTTO Motors, the world's leading developer of flexible and intelligent autonomous mobile robots (AMR). Customers in the manufacturing and warehousing industries worldwide will benefit from the combination of AGV hardware and AMR software offered by the two firms.

High Adoption of Automated Storage and Retrieval Systems (AS/RS) in Automotive Sector

- Many well-known vehicle brands are based in Europe, including Mercedes-Benz, Volvo, Aston Martin, Bentley, Porsche, Lamborghini, Ferrari, and others. Numerous vehicle production facilities in Germany, France, and the United Kingdom rely heavily on AS/RS systems to stay competitive. Exmac Automation, situated in the United Kingdom, provides storage solutions for Aston Martin, Bentley, Jaguar, and IBC vehicles.

- For instance, Industore, a major AS/RS solution provider in the UK, has a wide range of products utilized in warehouses and small and large storage units. ExMac Automation, another key player in AS/RS, provides automated storage and retrieval crane systems (ranging from high-capacity mini-load cranes and racking to high-bay warehouse cranes) to various industries across the country.

- The European Commission supports worldwide technical harmonization and offers to fund R&D to help the automotive industry maintain its competitiveness and technological leadership. Furthermore, according to ACEA research, 569 automobiles per 1,000 people in the European Union. Luxembourg has the highest car density in the EU (694 cars per 1,000 people), while Latvia has the lowest. According to the OICA, total European passenger car sales reached 14.16 million in 2020.

- The demand-driven nature of the UK automotive supply chain (including increasing levels of customization within a car) is compelling OEM suppliers to choose warehouse automation with greater flexibility. The increasing adoption of AS/RS systems and automation in the automotive manufacturing process and the advent of digitization and AI are some of the primary factors driving the demand for digitalization in the automotive sector of the Netherlands.

- Moreover, Germany is one of the world's largest users of automated material handling systems. According to the International Federation of Robotics (IFR), Germany has the highest robot density (294 units per 10,000 workers), behind South Korea and Japan. These factors will increase the demand for warehouse automation throughout Europe.

Europe Warehouse Automation Industry Overview

The European warehouse automation market is fragmented by its competitive landscape. Dematic Group, Swisslog Holding AG, and Swisslog Holding AG (KUKA AG) WITRON, Logistik + Informatik GmbH SSI Schaefer AG BEUMER Group GmbH & Co. KG TGW Logistics Group GmbH, and Jungheinrich AG are some of the regional significant competitors in this sector.

These major competitors, which hold a considerable share of the market, are concentrating on growing their consumer base in new countries. Furthermore, market participants in the warehouse automation sector use major strategies, including product launches, acquisitions, and collaborations. The following are some of the most recent developments:

- February 2022 -DHL Supply Chain has deployed the first fully automated auto store logistics system with robot picking for the omnichannel auction site 1-2-3.tv in Braunschweig, Germany. The Autostore system was created by Element Logic, a logistics technology company, and it uses robot picking and a software solution to increase the processing speed of each order, improve operational efficiency, and maximize the location's storage capacity.

- November 2021 - Honeywell Intelligrated warehouse automation announced plans to create a new advanced research and development (R&D) testing center to fulfill the growing demand for technologies that enable speedier, more accurate supply chains. Honeywell hardware and software engineers will be able to create, prototype, and test novel warehouse automation systems utilized by logistics companies at the site.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study assumptions and market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Industry Attractiveness -Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain Analysis

- 4.5 Warehouse Investment Scenario

- 4.6 Impact of Macro-economic Factors on the Warehouse Automation Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Exponential Growth of the E-commerce Industry and Customer Expectation

- 5.1.2 Increasing Manufacturing Complexity and Technology Availability

- 5.1.3 Industry 4.0 Investments Driving The Demand For Automation & Material Handling

- 5.2 Market Challenges

- 5.2.1 High Capital Investment

- 5.2.2 Stringent Regulatory Requirements

6 MARKET SEGMENTATION

- 6.1 Component

- 6.1.1 Hardware

- 6.1.1.1 Mobile Robots (AGV, AMR)

- 6.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3 Automated Conveyor & Sorting Systems

- 6.1.1.4 De-palletizing/Palletizing Systems

- 6.1.1.5 Automatic Identification and Data Collection (AIDC)

- 6.1.1.6 Piece Picking Robots

- 6.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

- 6.1.3 Services (Value Added Services, Maintenance, etc.)

- 6.1.1 Hardware

- 6.2 End-User

- 6.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

- 6.2.2 Post and Parcel

- 6.2.3 Groceries

- 6.2.4 General Merchandise

- 6.2.5 Apparel

- 6.2.6 Manufacturing (Durable and Non-Durable)

- 6.2.7 Other End-user Industries

- 6.3 Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Swisslog Holding AG (KUKA AG)

- 7.1.2 WITRON Logistik + Informatik GmbH

- 7.1.3 SSI Schaefer AG

- 7.1.4 BEUMER Group GmbH & Co. KG

- 7.1.5 TGW Logistics Group GmbH

- 7.1.6 Kion Group AG (Dematic Group)

- 7.1.7 Knapp AG

- 7.1.8 Jungheinrich AG

- 7.1.9 Vanderlande Industries BV

- 7.1.10 Mecalux SA