アジア・アフリカの食品缶詰-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Asia and Africa Food Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 133 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644459

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

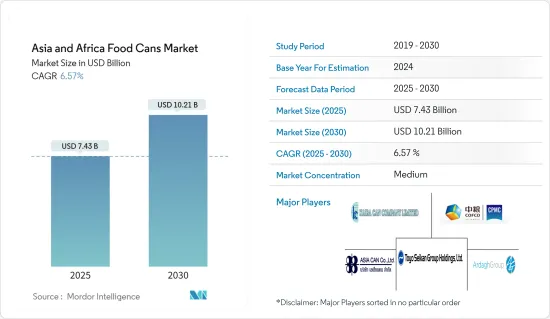

アジア・アフリカの食品缶詰市場規模は2025年に74億3,000万米ドルと推定・予測され、2030年には102億1,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.57%です。

COVID-19は食品消費に多くの変化をもたらしました。食品と食料品の購入パターンは消費者の嗜好の変化を浮き彫りにし、保存のきく食品や缶詰は食料品の買い物リストの上位に位置づけられました。さらに、免疫系を高める成分や栄養価の高い新製品が並びました。冷凍食品は、COVID-19が大流行する中、アジアの消費者の間で、ロックダウンと経済引き締めの中で成長を集めました。

主要ハイライト

- 金属缶詰の優れた防腐特性と構造的完全性は、より高い保存可能期間を提供し、アジア・アフリカ全域の食品包装産業で金属缶詰の高い使用率につながっています。多忙なライフスタイルや仕事のスケジュールにより、包装食品やコンビニエンスフードは多くの消費者にとって主食となっています。例えば人口問題ラボによると、2019年の世界の都市化の度合い(総人口に占める都市人口の割合)は約54%でした。

- IIEDによると、アジア諸国では、2020年に世界の都市人口のうち53.9%がこの地域に住むと推定されています。また、アフリカの都市成長率は世界最速で、2050年までに9億5,000万人がアフリカの都市で暮らすようになると予測されています。

- 各地域の金属産業は純増傾向を示しています。アフリカでは、錫メッキのスチール缶詰からアルミ缶詰への転換により、年間1億ZARから2億ZARが金属くずとリサイクル産業に流入すると予想されます。また、有名な飲料缶詰メーカーであるNampak Bevcanによれば、この産業は、使用済み缶詰の回収・販売により、さらに2,000~3,000人の人々に収入源を提供する可能性があります。

- アジアの動向は、東南アジアの成長と混在しています。中国や日本の複数のメーカーが、この地域に進出しています。例えば、昭和アルミ缶詰は「プロジェクト2020+」を通じて、東南アジアを対象に中期的な事業の成長加速に注力しています。

- 2020年10月現在、東南アジアに立地する複数の大型鉄鋼プロジェクトが中国の投資によって下支えされています。同時に、プラスチック容器からよりリサイクル性の高い缶詰にシフトする食品企業が増え、東南アジアが注目されるようになったと報じられています。東京に本社を置くUACJ株式会社は、2021年までに東南アジア工場のアルミ板生産能力を増強する見込みです。

アジア・アフリカの食品缶詰市場の動向

果物・野菜が市場成長を牽引

- 野菜と果物の缶詰は、冷凍代替品や生鮮代替品と比較すると、栄養面で妥協することなくコストが安いです。野菜缶詰の唯一の欠点はナトリウム含有量だが、消費者はナトリウム含有量の少ないものを選んだり、野菜を洗ったりすることができます。

- 2021年1月に発表された国連機関の報告書によると、13億人の南アジア人が健康的な食生活を送る余裕がなかった。さらに、パンデミックによって果物、野菜、乳製品の価格が上昇し、野菜や果物の缶詰がより良い選択肢となっています。

- 生産面では、インドと中国が野菜と果物の主要生産国です。国連食糧農業機関によると、2019年の生鮮野菜の生産量は中国が5億8,826万トン、次いでインドが1億3,203万トンでした。野菜の大量生産は、保存性を高めるために缶詰にする機会を生み出します。

- 輸出はまた、野菜や果物の缶詰輸出の品質向上の引き金にもなっています。例えば、中国とカナダが署名した覚書によると、中国の缶詰野菜には特定の輸出要件があります。

著しい成長率を示す韓国

- 韓国では、食肉加工品、野菜、野菜加工品などの品目が伸びています。韓国国家統計データベース(KOSIS)によると、1世帯当たりの加工肉に対する月平均支出は、12,190ウォンから2020年には1万4,470ウォンへと増加しました。

- 同様に、野菜と野菜加工品への支出は、2019年の3万3,580ウォンから2020年には4万1,370ウォンに増加しました。このように、国内における食肉と野菜の加工品の成長は、缶詰のような適切な包装の必要性を生み出しています。

- 政府は、2030年までにプラスチック廃棄物の排出量を半減させ、リサイクル率を34%から70%に倍増させる努力をしています。

- また、政府は2020年5月に食品接触材料の規格・基準を改定しました。今回の改定は、食品用器具、容器、包装の製造方法やレイアウトの改善など、共通の製造基準や仕様が対象となっています。

- この基準には、再生プラスチック樹脂の使用に関する明確化も含まれています。したがって、政府のイニシアティブは、プラスチックやスチールやアルミなどの他の材料からの脱却を促し、国の食品缶詰を牽引しています。

- COVID-19の大流行は、缶詰食品へのシフトに重要な役割を果たしており、その結果、食品缶詰の市場を牽引しています。例えば、新世界の調査によると、2020年2月現在、缶詰のオンライン販売は268%と大幅に増加し、米(187%)、即席麺(175%)、惣菜(168%)と続いています。

アジア・アフリカの食品缶詰産業概要

アジア・アフリカの食品缶詰市場は、主要市場参入企業間の適度な競合と新規参入者の増加が特徴です。市場開拓企業は、メディア参入企業に先進的機能と性能を統合するための研究開発にさらに注力しています。各社は市場シェアを維持するために技術革新を続け、戦略的パートナーシップを結んでいます。

- 2021年2月-Ardagh Groupは、金属包装事業部門をGores Holdings Vと合併し、公開会社を設立することで合意しました。この合意により、特別目的買収会社であるGores Holdings Vが、Ardaghの金属包装(AMP)部門と合併し、新たにArdagh Metalが設立されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 金属缶詰の代替品に対するリサイクル可能性の高さ

- コストと利便性に関する優位性が缶詰需要を牽引

- 賞味期限延長につながる製品革新

- 市場課題

- 各地域でプラスチックは依然として信頼性の高い代替品である

- 市場機会

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係の強さ

- 代替品の脅威

- 産業サプライチェーン分析

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 材料

- アルミ缶詰

- スチール/錫缶詰

- 缶詰タイプ

- 2ピース

- 3ピース

- 用途

- 魚介類

- 果物・野菜

- 加工食品

- ペットフード

- その他

- 地域

- アジア

- 中国

- インド

- 韓国

- 東南アジア

- アフリカ

- 南アフリカ

- アジア

第6章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- ORG Packaging Co. Limited

- Kian Joo Can Factory(Can One)

- Silgan Holdings Inc.

- CPMC Holdings Limited

- Kaira Can Private Limited

- Toyo Seikan Group Holdings Ltd

- Ardagh Group

- Asia Can Co. Ltd

- Royal Cans Industries Company

- CanSmart Group

- MC Packaging(Pte)Ltd

- Dongwon Systems

- Can It

- Nampak Ltd

第7章 投資分析

第8章 市場の将来

目次

The Asia and Africa Food Cans Market size is estimated at USD 7.43 billion in 2025, and is expected to reach USD 10.21 billion by 2030, at a CAGR of 6.57% during the forecast period (2025-2030).

COVID-19 has brought a slew of changes to food consumption. Food and grocery purchase patterns highlighted the changing consumer preferences; shelf-stable foods and canned goods were positioned on top of the grocery shopping list. Moreover, newer products were aligned to have immune system boosting ingredients and nutritional aspects. Frozen foods, among Asian consumers amid the COVID-19 pandemic, garnered growth during lockdowns and tightening economics.

Key Highlights

- The excellent preservative properties and structural integrity of the metal cans, offering higher shelf life, have resulted in the high usage of metal cans in the food packaging industry across Asia and Africa. Packaged and convenience foods have become a staple diet for many consumers, owing to their hectic lifestyles and work schedules. For instance, according to the Population Reference Bureau, in 2019, the degree of urbanization (percentage of the urban population in total population) across the world was around 54%.

- According to IIED, across the Asian counterparts, the percentage of the world's urban population living in the region was estimated at 53.9% in 2020. Also, Africa is projected to have the fastest urban growth rate in the world, i.e., by 2050, African cities may be home to an additional 950 million people.

- Metal industries in the respective regions demonstrate a net flourishing trend. In Africa, between ZAR 100 million and ZAR 200 million per year is expected to flow into the scrap metals and recycling industry due to the conversion from tin-plated steel cans to aluminum cans. Also, the industry may provide an additional 2,000-3,000 people a source of income from collecting and selling used cans, as per a reputed beverage can manufacturer, Nampak Bevcan.

- Asian trends are mixed with Southeast Asia's growth. Multiple manufacturers from China and Japan have expanded their footprint in the region. For instance, via its Project 2020+, Showa Aluminum Can Corporation has focused on the growth acceleration of its business in the medium-term by targeting Southeast Asia.

- Then, as of October 2020, multiple large steel projects located in Southeast Asia were underpinned by Chinese investment. At the same time, Southeast Asia reportedly gained attention as more food companies shifted away from plastic containers for more recyclable cans. UACJ Corporation, a Tokyo-based company, is expected to boost the output capacity of aluminum sheets at its Southeast Asian plants by 2021.

Asia & Africa Food Cans Market Trends

Fruits and Vegetables to Drive the Market Growth

- Canned fruits and vegetables cost less when compared to frozen alternatives or fresh alternatives without compromising nutrition. The only drawback for canned vegetables is the sodium content, but consumers can choose lower sodium versions or rinse the vegetables.

- According to the United Nations agency report published in January 2021, 1.3 billion South Asians could not afford a healthy diet. Further, the pandemic has increased the prices of fruits, vegetables, and dairy products, making canned fruits and vegetables a better option.

- From the production point of view, India and China are the primary producers of vegetables and fruits. According to the Food and Agriculture Organization, in 2019, China produced 588.26 million metric ton of fresh vegetables, followed by India at 132.03 million metric ton. The massive production of vegetables creates opportunities for canning to increase the shelf life.

- The exports are also triggering the quality improvement of the canned vegetable and fruit exports. For instance, according to a memorandum signed by China and Canada, the Chinese canned vegetables have specific export requirements.

South Korea to Witness Significant Growth Rate

- South Korea has seen growth in items such as processed meat, vegetables, and processed vegetables. According to the National Statistics database of Korea (KOSIS), the average monthly expenditure on processed meat per household increased from KRW 12,190 to KRW 14,470 in 2020.

- Similarly, the expenditure on vegetables and processed vegetables increased from KRW 33,580 in 2019 to KRW 41,370 in 2020. Thus, the growth in the processed meat and vegetables in the country creates the need for appropriate packaging, such as cans.

- The government is making efforts to reduce its plastic waste production by half and more than double recycling rates from 34% to 70% by 2030.

- Also, in May 2020, the government revised the standards and specifications for food contact materials. The revision is for common manufacturing standards and specifications, including improved methods and layouts for food utensils, containers, and packaging.

- The standards also include clarification on the use of recycled plastic resins. Hence, government initiatives encourage the push away from plastics and other materials such as steel and aluminum, thus driving the country's food cans.

- The COVID-19 pandemic has played a significant role in the shift toward canned food, thus driving the market for food cans. For instance, according to a survey by Shinsegae, as of February 2020, the online sales of canned food increased by a significant 268%, followed by rice (187%), instant noodles (175%), and prepared meals (168%).

Asia & Africa Food Cans Industry Overview

The Asian and African food cans market is characterized by moderate competitiveness among key market players and an increase in the number of new entrants. Market players are further focusing on research and development to integrate advanced functions and capabilities into media players. The companies keep on innovating and entering strategic partnerships to retain their market share.

- February 2021 - Ardagh Group entered an agreement to merge its Metal Packaging business segment with Gores Holdings V, thereby creating a public listed company. The agreement would see Gores Holdings V, a special purpose acquisition company, merge with Ardagh's Metal Packaging (AMP) division to form the newly created Ardagh Metal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Recyclable Score of Metal Cans over Alternatives

- 4.2.2 Demand for Canned Foods Driven by Cost and Convenience-related Advantages

- 4.2.3 Product Innovations Leading to Increased Shelf Life

- 4.3 Market Challenges

- 4.3.1 Plastic Remains a Highly Credible Alternative in the Regions

- 4.4 Market Opportunities

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Intensity of Competitive Rivalry

- 4.5.5 Threat of Substitutes

- 4.6 Industry Supply Chain Analysis

- 4.7 Impact of COVID-19 on the Market

5 Market Segmentation

- 5.1 Material

- 5.1.1 Aluminum Cans

- 5.1.2 Steel/Tin Cans

- 5.2 Can Type

- 5.2.1 2-piece

- 5.2.2 3-piece

- 5.3 Application

- 5.3.1 Fish and Seafood

- 5.3.2 Fruits and Vegetables

- 5.3.3 Processed Food

- 5.3.4 Pet Food

- 5.3.5 Other Applications

- 5.4 Geography

- 5.4.1 Asia

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 South Korea

- 5.4.1.4 Southeast Asia

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.1 Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Crown Holdings Inc.

- 6.1.2 ORG Packaging Co. Limited

- 6.1.3 Kian Joo Can Factory (Can One)

- 6.1.4 Silgan Holdings Inc.

- 6.1.5 CPMC Holdings Limited

- 6.1.6 Kaira Can Private Limited

- 6.1.7 Toyo Seikan Group Holdings Ltd

- 6.1.8 Ardagh Group

- 6.1.9 Asia Can Co. Ltd

- 6.1.10 Royal Cans Industries Company

- 6.1.11 CanSmart Group

- 6.1.12 MC Packaging (Pte) Ltd

- 6.1.13 Dongwon Systems

- 6.1.14 Can It

- 6.1.15 Nampak Ltd

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 133 Pages

- 納期

- 2~3営業日