|

市場調査レポート

商品コード

1644323

計器用変圧器:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Instrument Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 計器用変圧器:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

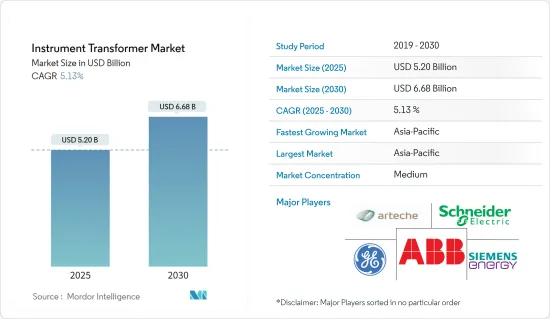

計器用変圧器の市場規模は2025年に52億米ドルと推定され、予測期間(2025~2030年)のCAGRは5.13%で、2030年には66億8,000万米ドルに達すると予測されます。

中期的には、送電や配電網の拡大、再生可能エネルギー発電設備の増加といった要因が市場を牽引するとみられます。

一方、高圧直流(HVDC)ネットワークの拡大は、予測期間中の市場成長を妨げると予想されます。

AIやIoTなどの先進技術と計器用変圧器との統合が進むことで、将来的には市場にいくつかの機会が生まれると予想されます。

計器用変圧器の市場動向

電力公益事業産業が市場を独占する可能性が高い

- 電力公益事業産業には、電気エネルギーの発電、送電、配電が含まれます。電力公益事業機器は電力品質の変動によるダメージを受けやすいため、計器用変圧器は主に計測、機器の保護、保護リレーへのエネルギー供給のために、このようなシステムで使用されています。計測用途では、計器用変圧器は収入計測に使用されます。計器用変圧器は、計器、保護リレー、ベイコンピュータなどの二次装置に、正確で信頼性の高い電流と電圧の測定を記載しています。

- 計器用変圧器は、幅広い電圧範囲を含む用途で使用されます。高電圧アプリケーションの場合、計器用変圧器は高圧ラインの電流と電圧をメーターや保護装置で測定可能な値に変換します。これらの変圧器は、主に72.5kVから1200kV以上の電圧に使用されます。送電網では、主に電流トランス、変圧器、複合変圧器、メータリングユニット、コンデンサ変圧器、電力変圧器、GIS用計器用変圧器、ライントラップとして使用されます。

- 今後、2022年には、中国の完成した電力供給プロジェクトへの投資は1兆718億2,000万米ドル、完成した送電網プロジェクト建設への投資は1,108億2,000万米ドルとなります。投資の大部分は風力エネルギープロジェクトに投じられ、風力発電所の資産管理は、適切な計測器と変圧器を使用して発電電力と送電電力をモニタリングすることで効率化できます。このため、全国で計器用変圧器の使用が増加しています。

- さらに、中電圧計器用変圧器は主に1~72.5kVの電圧範囲で作動します。これらは主に屋内用途で使用され、その主要目的はスペースの節約です。これらの変圧器は金属で密閉されたキュービクル内に設置され、一次端子は顧客の要求に応じて変更されます。低圧計器用変圧器は、1kV以下の電圧範囲で動作するため、限られた絶縁を必要とし、紙やポリマーのシートで形成されます。これらはサイズが小さく、主に制御盤や計測盤で使用されます。

- 送電や配電システムでは、一般に高圧計器用変圧器が使用されます。これらの機器は主に高電圧用途で使用され、HVACシステムの重要な部分を形成しています。このため、これらの変圧器の需要は、新規の大規模HV送電プロジェクトの大半が開発中である南米とアジア太平洋が主に牽引すると予想されます。

- 2022年11月、Power Grid Corporation of India Limitedは、チャッティースガル州ライガルから南部地域への余剰電力の送電を促進するため、約24億3,000万米ドル相当の送電回廊を実施する計画を発表しました。これはまた、再生可能エネルギーを南部の州からインドの他の地域に送るためのグリーンエネルギー回廊の一部でもあります。アジア太平洋などの成長市場における新たな送電プロジェクトは、予測期間中に計器用変圧器の需要を促進すると予想されています。

- したがって、上記の要因から、予測期間中は電力事業部門が市場を独占すると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、電力消費の増加、再生可能エネルギー源を利用した発電能力の増強に向けた政府の取り組み、老朽化した送電網インフラの拡大・強化などにより、2020年の計器用変圧器市場で大きなシェアを占めました。インド、中国、日本、韓国、オーストラリアなどの国々が、この地域の主要貢献国です。

- アジア太平洋の2022年の一次エネルギー消費量は277.60エクサジュールで、前年から2%以上増加しました。さらに、電力インフラは大きく成長し、2022年の発電量は1,4546.4 TWhとなります。

- この地域の多くの国々が、予測期間中に電力網インフラの開発に投資しています。中国では、2022年の総電力消費量は約8兆6,372億キロワット時でした。これは2021年から3.6%の成長です。

- 増加する電力需要に対応するため、中国政府は2020年半ばに、今後5年間で約9,000億米ドルを投資し、電力網インフラを開発する計画を立てた。また、同国最大の電力会社である中国国民生用電子機器網公司によると、送電網インフラと関連産業への投資は、送電、電気自動車充電器、新しいデジタルインフラを中心に、2021~2025年に8,960億米ドルを超えると予想されています。

- 2023年2月、インドの国営電力網公社は、競争入札によって5つの州間送電プロジェクトを落札したと発表しました。同社はBOOT(建設・所有・運営・譲渡)方式でプロジェクトの送電システムを構築します。グジャラート州における最初の送電網拡大プロジェクトは、Khavda潜在的REゾーンからの再生可能プロジェクトを統合し、同州を通過する765kV D/C送電線を確立するものです。Khavda RE ParkプロジェクトにおけるKhavda Pooling Station-2の設立は、新しい765/400kV GISの設立からなります。このようなプロジェクトでは、電力サージを最小限に抑えるために絶縁変圧器が使用されます。

- したがって、上記の要因により、アジア太平洋が予測期間中に計器用変圧器市場を独占すると予想されます。

計器用変圧器産業概要

計器用変圧器市場は半固体化しています。市場の主要企業(順不同)には、ABB Ltd、Siemens Energy AG、General Electric Company、Schneider Electric SE、Arteche Groupなどがあります。

2023年11月、Siemensはアメリカのデータセンターと重要インフラをサポートするため、ダラス・フォートワースの新しいハイテク製造工場に1億5,000万米ドルを投資すると発表しました。この工場は、最先端の効率的で信頼性の高い電気機器を提供する予定です。この工場は、生成AIの急激な普及によって加速する米国データセンターの成長を促進します。また、重要インフラの安全な運用も保証します。この投資は、2030年まで毎年約10%の需要増加が見込まれるデータセンターセグメントの長期的な顧客を明確に支援するものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- T&Dグリッドの近代化に向けた大幅な投資と取り組み

- 抑制要因

- 高電圧直流(HVDC)ネットワークの拡大

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 現行変圧器

- 計器用変圧器

- 複合変圧器

- エンドユーザー

- 電力会社

- 産業部門

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- Siemens Energy AG

- General Electric Company

- Schneider Electric SE

- Arteche Group

- PFIFFNER Instrument Transformers Ltd

- Crompton Greaves Ltd

- Mitsubishi Electric Corporation

- Nissin Electric Co. Ltd

- Amran Inc.

第7章 市場機会と今後の動向

- AIやIoTなどの先進技術と計器用変圧器との統合の増加

The Instrument Transformer Market size is estimated at USD 5.20 billion in 2025, and is expected to reach USD 6.68 billion by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

Over the medium term, factors like expansion in the transmission and distribution network and growth in renewable power generation facilities are likely to drive the market.

On the other hand, the expansion of high voltage direct current (HVDC) networks is expected to hinder the market growth during the forecast period.

Nevertheless, the increasing integration of advanced technologies such as AI and IoT with instrument transformers is expected to create several opportunities for the market in the future.

Instrument Transformer Market Trends

Power Utility Sector Likely to Dominate the Market

- The power utility industry includes the generation, transmission, and distribution of electrical energy. As power utility devices are vulnerable to damage from power quality fluctuations, instrument transformers are used in such systems mainly for measurement, protection of equipment, and providing energy to protective relays. In measurement applications, instrument transformers are used for revenue metering. They provide accurate and reliable current and voltage measurements for secondary equipment such as meters, protection relays, bay computers, and other devices.

- Instrument transformers are used in applications involving a wide range of voltages. For high-voltage applications, instrument transformers convert the currents and voltages of high voltage lines to values that are measurable by meters and protections. These transformers are mainly used for voltages over 72.5 kV to 1200 kV. They are used in transmission networks primarily as current transformers, voltage transformers, combined transformers, metering units, capacitor voltage transformers, power voltage transformers, instrument transformers for GIS applications, and line traps.

- Going ahead, in the year 2022, the China's investments for completed power supply projects was USD 1,071.82 billion and investment in power grid project construction completed was USD 110.82 billion. Majortity of investment got in wind energy projects, managing wind farm assets can be efficient by using the proper metering instrument and transformer to monitor produced and transmitted power. This, in turn, increases the use of instrument transformers across the country.

- Moreover, medium-voltage instrument transformers operate primarily between 1 and 72.5 kV voltage ranges. These are mainly used in indoor applications, with the primary target of saving space. These transformers are placed in metal-enclosed cubicles, and the primary terminals are modified according to customer requirements. Low-voltage instrument transformers operate in voltage ranges below 1 kV and, hence, require limited insulation and are formed by sheets of paper or polymers. These are smaller in size and are primarily used in control and measurement panels.

- In transmission and distribution systems, high-voltage instrument transformers are generally used. These devices are primarily used in high-voltage applications and form a critical part of HVAC systems. Due to this, the demand for these transformers is expected to be mainly driven by South America and Asia-Pacific, where most new large-scale HV transmission projects are under development.

- In November 2022, the Power Grid Corporation of India Limited announced its plan to implement a transmission corridor worth about USD 2.43 billion to facilitate the transfer of surplus power from Raigarh in Chhattisgarh to the southern region. It is also part of the green energy corridor for transferring renewable energy from the southern states to the rest of India. New transmission projects in growing markets such as Asia-Pacific are expected to drive demand for instrument transformers during the forecast period.

- Therefore, owing to the above factors, the power utility sector is expected to dominate the market during the forecast period.

Asia-Pacific Likely to Dominate the Market

- The Asia-Pacific region accounted for a significant share of the instrument transformer market in 2020, owing to increasing power consumption, government initiatives to increase power generation capacity using renewable energy sources, and the expansion and enhancement of aging grid infrastructure. Countries such as India, China, Japan, Korea, and Australia are the key contributing nations in the region.

- The Asia-Pacific region consumed 277.60 exajoules of primary energy in total in 2022, up more than two percent from the previous year. Further, power infrastructure grew significantly, with an electricity generation of 14546.4 TWh in 2022.

- Many countries in the region are investing in developing their power grid infrastructure during the forecast period. In China, the total power consumption in 2022 was about 86, 372 billion kilowatt-hours. It represented 3.6 percent growth from 2021.

- To cater to the increasing power demand, in mid-2020, the Chinese government planned to invest nearly USD 900 billion in the next five years to develop the country's power grid infrastructure. In addition, according to the State Grid Corp. of China, the country's biggest power utility, investments in power grid infrastructure and related industries are expected to surpass USD 896 billion in 2021-2025, focusing on power transmission, electric vehicle chargers, and new digital infrastructure.

- In February 2023, India's state-owned Power Grid Corporation announced that it had bagged five inter-state electricity transmission projects through competitive bidding. The company will establish the project's transmission system on a build, own, operate, and transfer (BOOT) basis. The first transmission network expansion project in Gujarat is associated with integrating renewable projects from the Khavda potential REzone to establish 765 kV D/C transmission lines passing through the state. The establishment of Khavda Pooling Station-2 in the Khavda RE Park project comprises the establishment of a new 765/400 kV GIS. In turn, this kind of project will culminate in the utilization of isolation transformers to minimize power surges.

- Therefore, owing to the above factors, the Asia-Pacific region is expected to dominate the instrument transformer market during the forecast period.

Instrument Transformer Industry Overview

The instrument transformer market is semi-consolidated. Some of the key players in the market (in no particular order) include ABB Ltd, Siemens Energy AG, General Electric Company, Schneider Electric SE, and Arteche Group, among others.

In November 2023, Siemens announced an investment of USD 150 million in a new high-tech manufacturing plant in Dallas-Fort Worth to support power American data centers and critical infrastructure. This plant is going to deliver state-of-the-art, efficient, and reliable electrical equipment. It is going to facilitate accelerated growth of United States data centers, which is being driven by the exponential adoption of generative AI. It will also ensure the secure operation of critical infrastructure. This investment explicitly helps long-term customers in the data center sector, where demand is expected to grow by about 10% annually through 2030.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Substantial Investments and Efforts to Modernize the T&D Grid

- 4.5.2 Restraints

- 4.5.2.1 Expansion of High Voltage Direct Current (HVDC) Networks

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Current Transformer

- 5.1.2 Potential Transformer

- 5.1.3 Combined Transformer

- 5.2 End User

- 5.2.1 Power Utilities

- 5.2.2 Industrial Sector

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 Spain

- 5.3.2.4 United Kingdom

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Siemens Energy AG

- 6.3.3 General Electric Company

- 6.3.4 Schneider Electric SE

- 6.3.5 Arteche Group

- 6.3.6 PFIFFNER Instrument Transformers Ltd

- 6.3.7 Crompton Greaves Ltd

- 6.3.8 Mitsubishi Electric Corporation

- 6.3.9 Nissin Electric Co. Ltd

- 6.3.10 Amran Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Integration of Advanced Technologies such as AI and IoT with Instrument Transformers