|

市場調査レポート

商品コード

1644312

アフリカの包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Africa Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 108 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

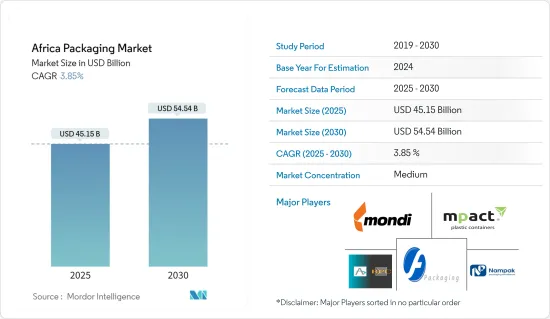

アフリカの包装市場規模は2025年に451億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.85%で、2030年には545億4,000万米ドルに達すると予測されます。

主要ハイライト

- 若い消費者の増加が市場を牽引しており、特に東アフリカと西アフリカでは消費財需要の増加、個人所得の上昇、国内経済の拡大が見られます。

- 都市化と移動の増加に伴い、アフリカの消費者はバルク、割引、小分けパックなど、お得感のある商品を求めています。ベンダーにとって、魅力的な包装を採用することは、販売を促進し、押し上げる上で有利となります。さらに、飲食品、医薬品、その他の家庭用製品の包装に関する関心の高まりが、人々に美的魅力を提供し、リサイクル可能であることから、ガラス容器とガラス瓶市場を牽引しています。

- さらに、企業はより優れた技術や専門知識を持ち込み、忍耐強く現地のパートナーを見つけようとしています。例えば、2022年10月、オーストリアを拠点とする国際的なプラスチック包装、リサイクルのスペシャリストであるAlpla Groupは、ヨハネスブルグ近郊のハウテン州ランセリアに新施設を建設し、南アフリカでの拠点を拡大しました。

- 包装市場の成長を妨げる大きな課題のひとつは、包装製造コストの高さです。紙パルプは、紙包装製造に使用される主原料です。段ボール箱、ダンボール箱、紙パック、紙袋など、さまざまな包装の製造に広く使われています。紙パルプの価格は常に変動しています。同様に、プラスチック包装産業も原油に依存しており、原油価格も不安定です。さらに、ロシア・ウクライナ戦争は包装エコシステム全体に影響を与えています。

- COVID-19の発生により、包装メーカーはアフリカの多くの地域で、現場での製造の減少とともにサプライチェーンの混乱に直面しました。例えば、製紙包装会社のモンディは、年間27万トンの生産能力を持つ南アフリカのMerebank工場での生産を一時停止すると発表しました。

アフリカの包装市場の動向

ガラス瓶が市場成長を牽引

- ガラス容器やガラス瓶は、医薬品、飲食品、ワインなどのエンドユーザー産業で広く使用されています。同地域では、より多くの人口が環境に優しいソリューションに目を向け、その貢献度を高めているため、ガラス製容器包装は同地域での成長が見込まれています。さらに、ガラス包装はプラスチック包装に代わる無限のリサイクル可能な代替品と見なされています。ガラスは100%リサイクル可能で、品質を損なうことなく再利用できます。

- 南アフリカはワイン消費国です。国際的な動向は缶入りワインにシフトしつつあるが、同国が追随できるようになるには、相当な期間、強力なガラス市場であり続けると予想されます。

- アフリカのガラス容器やガラス瓶市場は競争が激しく、合理化に失敗した参入企業は事業から撤退しています。南アフリカを拠点とする多角的包装メーカーであるNampakは、固定費と経費が高く、財務的リターンが不十分であったため、ガラス事業の売却を余儀なくされました。同事業はIsanti Glass(Kwande Capital所有)に15億ZAR(1億2,500万米ドル)で売却されました。

- ガラス瓶の大きな原動力のひとつは、地元の観光産業がペット瓶の使用をやめようという動きを強めていることです。これは、この地域でガラスを生産する企業にとって大きな機会になると期待されています。さらに、Glass Recycling Company(TGRC)によると、南アフリカのガラスリサイクル率は現在44%であり、これが市場の成長にさらに拍車をかけています。

- さらに、南アフリカのワイン産業は複数の栽培地域にまたがっています。産業団体SAWIS(South African Wine Industry Information &Systems)によると、2022年のワイン用ブドウの収穫量は137万8,737トンと推定されています。2021年の収穫量より5.5%少ないが、5年平均の134万6,024トンよりは多いです。

- 南アフリカのワイン・ブランデー産業は、国内販売禁止と世界の貿易障壁による2年間の深刻な混乱の後、再建を続けています。同産業は、2025年に向けた戦略計画(WISE)を改訂し、世界と国内の市場アクセス、変革、持続可能性に特に焦点を当てました。このフレームワークと主要業績評価指標は、最近署名されたAgriculture and Agro-processing Master Plan(AAMP)にも含まれています。これにより、より広範な農業セクターの中で、ワインにとってはるかに有利な生産・取引環境を確保することができます。Vinproが発表したデータによると、南アフリカのワイン輸出総量は2021年に22%増の3億8,800万リットルに達します。

市場成長をリードする飲料産業

- 飲料は調査対象市場で最大のシェアを占めています。消費者が消費するものや包装される材料にますます気を配るようになったことで、包装への注目度が高まり、市場成長をさらに後押ししています。

- 世界保健機関(WHO)によると、この地域のアルコール消費者は世界でも有数の大量飲酒者であり、これが市場成長を後押ししています。また、清涼飲料ベンダーからの需要の増加は、瓶包装ソリューションプロバイダーや包装ベンダーの同地域での能力増強に役立っています。

- さらに、同地域の市場参入企業は、飲料包装に関するさまざまなイノベーションを試みています。例えば、2022年9月、Coca-Cola Beverages Africa(CCBA)の子会社であるVoltic Ltdは、ガーナでHollandia's Choco Maltブランドを発売しました。牛乳を含むモルト飲料は無菌カートンで販売されているが、同社はモダンなグラフィックとブランディングを施した缶での販売も計画しています。

- エナジードリンクの売上は、炭酸飲料よりも大幅に伸びています。低アルコール飲料やノンアルコール飲料の代替品、低カロリー・低糖質飲料、健康飲料、サステイナブル包装に対する需要が高まっており、その結果、リターナブルのガラス瓶入りフルーツジュースブレンドや缶入り飲料水が発売されています。

- 広大な飲食品小売市場では、数多くの企業がトップの座を争っています。飲食品小売市場の参入企業は、ライフスタイルの変化、進化する飲料の嗜好、特定地域の人々の嗜好など、さまざまな側面を研究し、それに応じて食品や飲料アイテムを開発しています。この側面により、参入企業は多くの収入を得ることができます。

アフリカの包装産業概要

アフリカの包装市場の競争は中程度です。同市場の参入企業は、市場シェアを拡大し収益性を高めるために、アフリカ諸国全域での顧客基盤の拡大に継続的に注力し、戦略的な共同イニシアティブを活用しています。市場の主要開発には次のようなものがあります。

2022年7月、Ardagh Glass Packaging Africaは、南アフリカのハウテン州にあるナイジェル生産施設の15億ZAR(9,500万米ドル)の拡大工事を開始したと発表しました。この投資は、同社の顧客の現在と予測される需要増加をサポートするサステイナブルガラス包装を提供するための施設の能力を倍増させ、新しい炉と生産ラインを組み込みました。

2022年3月、Elopak ASAはGulf Industrial Groupの100%子会社であるNaturepak LimitedとPactiv Evergreen Inc.の100%子会社であるEvergreen Packaging International LLCから、中東・北アフリカ地域の主要なゲーブルトップ液体カートンと包装システムサプライヤーであるNaturepak Beverageの買収を完了しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の市場への影響評価

- 世界の包装市場概要

第5章 市場力学

- 市場促進要因

- ガラス瓶が市場成長を牽引

- 飲料産業が市場成長を牽引

- 市場抑制要因

- 原料価格の変動が市場成長の妨げになる可能性

第6章 市場セグメンテーション

- 材料別

- 紙・板紙

- プラスチック

- 金属

- ガラス

- 製品タイプ別

- プラスチック瓶

- ガラス瓶

- 段ボール箱

- 金属缶

- その他

- エンドユーザー産業別

- 飲料

- 食品

- 医薬品

- 家庭用品・パーソナルケア

- その他

- 国別

- エジプト

- ナイジェリア

- ケニア

- 南アフリカ

- その他のアフリカ

第7章 競合情勢

- 企業プロファイル

- Astrapak Ltd(RPC Group)

- Nampak Limited

- Mondi Group

- Mpact Pty Ltd

- Foster Packaging

- Consol Glass(Pty)Ltd.

- East African Packaging Industries Ltd(EAPI)

- Constantia Afripack(Pty)Ltd

- Tetra Pak SA

- Bonpak(Pty)Ltd.

- Frigoglass South Africa(Pty)Ltd.

第8章 投資分析

第9章 市場の将来

The Africa Packaging Market size is estimated at USD 45.15 billion in 2025, and is expected to reach USD 54.54 billion by 2030, at a CAGR of 3.85% during the forecast period (2025-2030).

Key Highlights

- An increasing number of young consumers is driving the market, increasing demand for consumer goods, rising individual incomes, and expanding domestic economies, particularly in East and West Africa.

- With increasing urbanization and mobility, African consumers are looking for products that offer the best value for money, such as bulk, discounted, and smaller packs. It can be an advantage for vendors to go for attractive packaging to encourage and boost sales. Moreover, the growing concern regarding the packaging of food, beverages, pharmaceuticals, and other household products is driving the market for glass containers and bottles as they offer an aesthetic charm to people and are recyclable.

- Furthermore, companies are willing to bring better technology, technical expertise, and patience to find local partners. For instance, in October 2022, Austria-based Alpla Group, an international plastic packaging, and recycling specialist, expanded its footprint in South Africa by building a new facility in Lanseria, Gauteng Province, near Johannesburg.

- One of the significant challenges impeding packaging market growth is high packaging manufacturing costs. Paper pulp is a primary raw material used in paper packaging manufacturing. It is widely used in manufacturing corrugated boxes, cardboard boxes, folding cartons, and paper bags, among other types of packaging. The price of paper pulp has constantly been fluctuating. Similarly, the plastic packaging industry is also dependent on crude oil, and crude oil prices are also volatile. Furthermore, the Russia-Ukraine war has an impact on the overall packaging ecosystem.

- With the outbreak of COVID-19, packaging manufacturers faced supply chain disruption along with decreasing manufacturing at the site in many parts of Africa. For instance, paper and packaging company Mondi announced the temporary suspension of production at its Merebank mill in South Africa, which has a production capacity of 270,000 tonnes annually.

Africa Packaging Market Trends

Glass Bottles to Drive the Market Growth

- Glass containers and bottles are widely used by end-user industries like pharmaceuticals, food and beverage, and wine. As more and more population of the region is turning toward eco-friendly solutions to increase their contribution, glass packaging is expected to grow in the region. Moreover, glass packaging is seen as an endless recyclable alternative to plastic packaging. Glass can be 100% recycled and reusable without losing quality.

- South Africa is a wine-consuming country. Although the international trend is shifting toward wine in cans, the country is expected to continue to be a strong glass market for a significant amount of time before it can follow.

- The African glass bottles and container market is highly competitive, and the players who fail to streamline their operations are exiting the business. Nampak, a South Africa-based diversified packaging manufacturer, has been forced to sell its glass business due to high fixed costs and expenditures, leading to inadequate financial returns. It was sold to Isanti Glass (Kwande Capital-owned) for ZAR 1.5 billion (USD 125 million).

- One of the significant drivers of glass bottles is the growing drive by the local tourism industry to stop using plastic bottles. This is expected to create a massive opportunity for companies to produce Glass in the region. Moreover, according to Glass Recycling Company (TGRC), the current glass recycling rate in South Africa is 44%, which further adds to the market's growth.

- Furthermore, the wine industry in South Africa is spread across several cultivation areas. According to the industry body, South African Wine Industry Information & Systems (SAWIS), the wine grape crop is estimated to be 1,378,737 tonnes 2022. It is 5.5% lower than the crop for 2021, but it is higher than the fi)ve-year average of 1,346,024 tonnes.

- The South African wine and brandy industry is continuing to rebuild after two years of severe disruptions due to domestic sales bans and global trade barriers; the industry has revised its strategic plan (WISE) towards 2025, which includes a specific focus on global and local market access, transformation, and sustainability. The framework and key performance indicators are also included in the recently signed Agriculture and Agro-processing Master Plan (AAMP). This can ensure a far more favorable production and trading environment for wine within the broader agricultural sector. According to data published by Vinpro, South Africa's total wine export volume grew by 22% to 388 million liters in 2021.

Beverage Industry to Lead the Market Growth

- Beverages hold the maximum market share in the market studied. With consumers getting increasingly careful about what they consume and what material is packaged, the focus on packaging is increased, further driving the market growth.

- According to the World Health Organization (WHO), the consumers of alcohol in the region are some of the heaviest drinkers globally, which boosts the market growth. Also, the increase in demand from soft-drink vendors is helping bottle packaging solution providers and packaging vendors increase their capacities in the region.

- Moreover, market players in the region are trying out various innovations for beverage packaging. For instance, in September 2022, Voltic Ltd, Coca-Cola Beverages Africa's (CCBA) subsidiary, launched Hollandia's Choco Malt brand in Ghana. Malted drinks containing milk are sold in aseptic cartons, and the company is also planning to sell them in cans with modern graphics and branding.

- Sales of energy drinks are growing significantly faster than carbonated drinks. There is increasing demand for low or no-alcohol drink substitutes, low-calorie and low-sugar options, health drinks, and sustainable packaging resulting in the launch of fruit juice blends in returnable glass bottles and canned water.

- Numerous players compete for the top spot in the vast food and beverage retail market. Food and beverage retail market players research various aspects such as lifestyle changes, evolving drink preferences, and the preferences of people in a specific area and develop food and beverage items accordingly. This aspect allows the players to earn a lot of money.

Africa Packaging Industry Overview

The Africa Packaging Market is moderately competitive. The players in the market are continuously focusing on expanding their customer base across the countries of Africa and leveraging strategic collaborative initiatives to increase their market share and increase their profitability. Some of the key developments in the market are:

In July 2022, Ardagh Glass Packaging Africa announced the commissioning of a ZAR 1.5 billion (USD 95 million) extension of its Nigel production facility in Gauteng, South Africa. The investment doubled the facility's capacity to provide sustainable glass packaging to support the company's customers' current and projected demand growth and incorporates a new furnace and production lines.

In March 2022, Elopak ASA completed the acquisition of Naturepak Beverage, a leading gable top fresh liquid carton and packaging systems supplier in the MENA region, from Naturepak Limited, a wholly owned subsidiary of Gulf Industrial Group, and Evergreen Packaging International LLC, a wholly owned subsidiary of Pactiv Evergreen Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Overview of the Global Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Glass Bottles to Drive the Market Growth

- 5.1.2 Beverage Industry to Lead the Market Growth

- 5.2 Market Restraints

- 5.2.1 Fluctuation in Raw Material Price can Hinder the Growth of the Market.

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Paper and Paperboard

- 6.1.2 Plastic

- 6.1.3 Metal

- 6.1.4 Glass

- 6.2 By Product Type

- 6.2.1 Plastic Bottles

- 6.2.2 Glass Bottles

- 6.2.3 Corrugated Boxes

- 6.2.4 Metal Cans

- 6.2.5 Other Applications

- 6.3 By End-user Industry

- 6.3.1 Beverage

- 6.3.2 Food

- 6.3.3 Pharmaceuticals

- 6.3.4 Household and Personal Care

- 6.3.5 Other

- 6.4 By Country

- 6.4.1 Egypt

- 6.4.2 Nigeria

- 6.4.3 Kenya

- 6.4.4 South Africa

- 6.4.5 Rest of Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Astrapak Ltd (RPC Group)

- 7.1.2 Nampak Limited

- 7.1.3 Mondi Group

- 7.1.4 Mpact Pty Ltd

- 7.1.5 Foster Packaging

- 7.1.6 Consol Glass (Pty) Ltd.

- 7.1.7 East African Packaging Industries Ltd (EAPI)

- 7.1.8 Constantia Afripack (Pty) Ltd

- 7.1.9 Tetra Pak SA

- 7.1.10 Bonpak (Pty) Ltd.

- 7.1.11 Frigoglass South Africa (Pty) Ltd.