エンドユーザーコンピューティング-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

End User Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644285

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

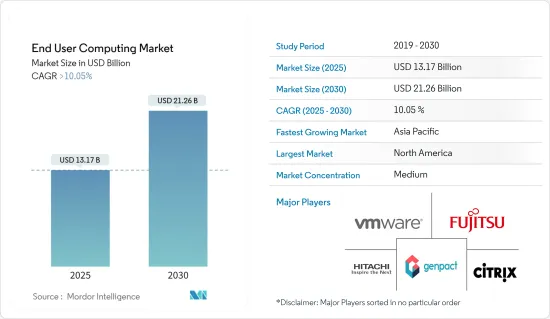

エンドユーザーコンピューティング市場規模は、2025年に131億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは10.05%を超え、2030年には212億6,000万米ドルに達すると予測されます。

エンドユーザーコンピューティング市場の成長には、急速に進歩する技術とソフトウェアのアップデート、BYOD(Bring Your Device)デバイスの増加傾向、従業員の生産性重視の高まり、ワークスペースを近代化しながらITインフラコストを削減する取り組みなどが寄与しています。

主要ハイライト

- インスタントクローン、ユーザー環境管理、アプリボリュームなどの革新的な技術により、企業はデスクトップとアプリケーションの管理を合理化し、従業員に明確でステートレスなデスクトップを提供しています。これにより、企業はコストを削減し、セキュリティを向上させ、従業員にパーソナライズされたデスクトップ体験を提供できます。

- ビジネスの継続性を維持し、従業員の安全を確保するために、多くのワークスペースが在宅勤務にシフトしているため、エンドユーザーコンピューティングソリューションの需要が急増しています。これに対応するため、企業はさまざまな事業規模やITリソースに合わせたソリューションやサービスを提供しています。

- さらに2023年7月、genpactは、プランニングと意思決定を変革するための主要企業向け人工知能(AI)ソフトウェアプラットフォーム・プロバイダであるo9 Solutionsとの提携を拡大し、企業が生成的AIを活用することで、進行中のサプライチェーンの混乱を乗り切るのを支援すると発表しました。

- ITリソースが限られている中小企業向けに、エンドユーザーコンピューティング・プロバイダーは、市場をリードするソリューションの低価格エントリーバージョンや無料トライアルを提供しています。しかし、データやファイルにリモートでアクセスする人の増加は、サーバーやネットワークインフラなどの物理的リソースを圧迫しており、長期的にはコスト増につながる可能性があります。

- COVID-19の流行は、エンドユーザーコンピューティング部門に悪影響を与えました。社会的距離を置く措置や制限の実施により、重要な中核組立拠点での業務が停止し、サプライチェーンや製造業務に混乱が生じた。これは短期的にも長期的にも産業に影響を及ぼし、アジア太平洋と欧州の数多くの企業が、従業員と活動の減少により操業停止を余儀なくされました。

エンドユーザーコンピューティング市場の動向

クラウド利用の増加がエンドユーザーコンピューティング市場の成長を牽引する見込み

- エンドユーザーコンピューティング・プロバイダーは、企業がクラウドサービスを利用し、一時的に必要なリソースに対してのみ料金を支払うことを可能にする、ライセンシングとサブスクリプションベースのソリューションを提供しています。これにより、企業は、長期間アイドル状態のリソースや機器を追加購入、プログラム、保守する必要がなくなるため、収益を生まないコストを削減し、クラウドベースのエンドユーザーコンピューティング市場の成長を促進することができます。

- エンドユーザーの多様な要件を満たすため、企業はエンドユーザーコンピューティングソリューションをオンプレミス、クラウド、またはその両方を組み合わせたハイブリッド・アプローチで提供することができます。このアプローチは、オンプレミスのサービスから完全なクラウドホスト型サービスまたはハイブリッドクラウド管理型サービスに移行するための低リスクな方法を企業に記載しています。

- オンプレミスでホスト可能なクラウドベースの管理、デスクトップ、インフラ、先進的仮想C、Nvidia Gridなどの技術、まったく新しいBlast Extremeプロトコルにより、企業は、最も要求の厳しいグラフィックを多用するワークロードであっても、エンドユーザーが期待するすべての機能を備えた優れたユーザー体験を提供することができます。

- 例えば、VMwareはMicrosoftと提携し、VMware Workspace ONE for Microsoft Endpoint Managerという新しいソリューションを開発しました。このソリューションにより、Windows 10デバイスの最新の管理が可能になり、企業はWorkspace OneコンソールからWindows 10デバイスを管理できるようになります。VMwareはまた、Workspace ONEを介してMicrosoft 365のアプリケーションとサービスへのアクセスを提供し、BYoD(Bring-your-own-devices)全体でMicrosoft Endpoint ManagerとAzure Active Directory Premiumとの統合を実現します。

北米が大きな市場シェアを占める見込み

- 北米は、さまざまな要因からエンドユーザーコンピューティング市場で重要な位置を占めています。同地域では、ネットワーク技術の急速な成長、先進的モバイルプラットフォームの利用可能性、SaaSの柔軟性が確認されています。その結果、労働力の流動性が高まり、エンドユーザーコンピューティングの成長を牽引しています。さらに、5Gネットワークの登場により、エンドユーザーコンピューティング・プロバイダーは近い将来、より多くの帯域幅とより高速なインターネット速度を利用して、より先進的サービスを開発できるようになります。

- 北米はまた、BYOD(Bring-your-own-device)文化の先駆者としても知られており、これがエンドユーザーコンピューティングの広範な導入につながっています。この地域の多くの会社は、パブリッククラウドにとどまらず、パブリッククラウド、プライベートクラウド、従来のITを組み合わせたハイブリッドITアプローチを採用しています。このアプローチにより、従業員はいつでもどこからでも企業のデータやアプリケーションにアクセスできるようになります。クラウドベースのソリューションやサービスの採用と開発が、エンドユーザーコンピューティング市場の成長をさらに促進しています。

- さらに、データセンターの導入がプロフェッショナルクラウドサービス市場の成長を加速させています。バージニア州北部は、2022年に米国の主要データセンター市場の中で最もデータセンターの純吸収量が多く、303.3メガワットに達しました。コンピューティング・ニーズを満たすためにクラウドベースのソリューションやサービスを採用する企業が増えるにつれ、この動向は続くと考えられます。全体として、北米の技術進歩、BYOD文化の採用、クラウドベースのソリューションとサービスの成長により、エンドユーザーコンピューティング市場における北米の優位性は今後も続くと予想されます。

エンドユーザーコンピューティング産業概要

エンドユーザーコンピューティング市場は、地域的な参入企業と世界の参入企業の両方がその技術的専門知識で市場を独占しており、半固体化が予想されます。多くの企業が戦略的パートナーシップを採用し、共通の利益を得て市場での地位を強化しています。

- 2023年4月-IGELは、新しいCOSMOSエンドポイントプラットフォームの発売を発表しました。このプラットフォームは、従業員があらゆるデバイスからあらゆるクラウドへあらゆるデジタルワークスペースにアクセスできるようにすることで、素晴らしいワークスペース体験を可能にし、EUC管理者は、新しいオペレーティングシステム、更新された管理コンソール、多数の新しいクラウドサービスを通じて、より高いセキュリティ、管理、制御を提供できるようになります。

- 2022年11月-XenTegraとMindcentricは、XenTegraの広範な技術的ノウハウを活用する新会社XenTegra ONEを設立。これにより、エンドユーザーコンピューティング、クラウドコンピューティング、データセンターインフラソリューションの改善を企業顧客に提供。Mindcentricは独立系事業として存続しますが、XenTegraのSMB販売とサポート部門として、XenTegraを代表することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場促進要因

- 技術による従業員の生産性向上の推進

- クラウド利用の増加

- 市場抑制要因

- 組織によるプロセスの変革と統合に伴う問題

- COVID-19が産業に与える影響の評価

第5章 市場セグメンテーション

- タイプ

- ソリューション

- 仮想デスクトップインフラ

- デバイス管理

- その他のソリューション(ユニファイドコミュニケーション、ソフトウェア資産管理)

- サービス内容

- ソリューション

- 組織規模

- 大企業

- 中小企業

- 導入形態

- オンプレミス

- クラウド

- エンドユーザー業種

- ITと電気通信

- 銀行、金融サービス、保険

- 医療

- 小売

- その他のエンドユーザー産業(メディア&エンターテインメント、政府、教育、運輸&物流)

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Nutanix, Inc.

- Fujitsu Ltd.

- Genpact

- HCL Infosystems Limited

- IGEL Technology

- Infosys Limited

- Mindtree Limited

- NetApp, Inc.

- Nucleus Software Exports Limited

- Citrix Systems, Inc.

- Tech Mahindra Limited

- Vmware, Inc.

- Hitachi Systems Micro Clinic

- Dell Technologies

- Amazon Web Services

第7章 投資分析

第8章 市場機会と今後の動向

目次

The End User Computing Market size is estimated at USD 13.17 billion in 2025, and is expected to reach USD 21.26 billion by 2030, at a CAGR of greater than 10.05% during the forecast period (2025-2030).

The growth of the end-user computing market is fueled by rapidly advancing technology and software updates, a rising trend of BYOD (bring your device) devices, an increased focus on employee productivity, and efforts to lower IT infrastructure costs while modernizing workspaces.

Key Highlights

- Innovative technologies such as instant clones, user environment management, and app volumes are helping organizations streamline desktop and application management, providing employees with clear and stateless desktops that can be easily destroyed or delivered as needed. This allows organizations to reduce costs, improve security, and provide personalized desktop experiences for their employees.

- The demand for end-user computing solutions has skyrocketed as many workspaces have shifted to work-from-home setups to maintain business continuity and ensure employee safety. In response, companies offer solutions and services tailored to different business sizes and IT resources.

- Furthermore, in July 2023, genpact has announced it is expanding its partnership with o9 Solutions, a leading enterprise artificial intelligence (AI) software platform provider for transforming planning and decision-making, to help companies navigate ongoing supply chain disruptions by leveraging generative AI.

- For small to medium-sized organizations with limited IT resources, end-user computing providers offer low-cost entry-level versions and free trials of their market-leading solutions. However, the growing number of people accessing data and files remotely is straining physical resources such as servers and network infrastructure, which may increase costs in the long run.

- The COVID-19 pandemic negatively impacted the end-user computing sector. Implementing social distancing measures and restrictions halted duties at critical core assembly sites, leading to disruptions in the supply chain and manufacturing operations. This had short-term and long-term effects on the industry, with numerous companies in Asia-Pacific and Europe having to shut down operations due to reduced employees and activity.

End User Computing Market Trends

Increasing Use of Cloud is Expected to Drive the End User Computing Market Growth

- End-user computing providers offer licensing and subscription-based solutions that allow companies to use cloud services and pay only for the resources they temporarily require. This eliminates the need for companies to purchase, program, and maintain additional resources and equipment that remain idle for extended periods of time, thus reducing costs that do not generate revenue and promoting market growth in the cloud-based end-user computing market.

- To meet the diverse requirements of end-users, companies can deliver end-user computing solutions from on-premises, in the cloud, or through a hybrid approach that combines both. This approach provides businesses a low-risk way to move from an on-premises service to a fully cloud-hosted or hybrid cloud-managed service.

- With cloud-based management, desktops, and infrastructure that can be hosted on-premises, advanced virtual c, technologies such as Nvidia Grid, and brand new blast extreme protocol, companies can deliver great user experiences with all the features end-users expect, even for the most demanding graphic-intensive workloads.

- For example, VMware partnered with Microsoft to develop a new solution named VMware Workspace ONE for Microsoft Endpoint Manager. This solution enables modern management for Windows 10 devices and allows enterprises to manage their Windows 10 devices from their Workspace One console. VMware will also provide access to Microsoft 365 apps and services via Workspace ONE and integration with Microsoft endpoint manager and Azure active directory premium across bring-your-own-devices (BYoDs).

North America is Expected to Hold Significant Market Share

- North America is a significant player in the end-user computing market due to various factors. The region has witnessed rapid growth in network technologies, the availability of advanced mobile platforms, and the flexibility of SaaS. This has resulted in increased workforce mobility, driving the growth of end-user computing. Additionally, with the onset of 5G networks, end-user computing providers can utilize more bandwidth and faster internet speeds to develop more advanced services in the near future.

- North America is also known for being a pioneer in the bring-your-own-device (BYOD) culture, which has led to the widespread incorporation of end-user computing. Many companies in the region are moving beyond the public cloud and adopting a hybrid IT approach that combines public cloud, private cloud, and traditional IT. This approach allows employees to access corporate data and applications from anywhere and anytime. The adoption and development of cloud-based solutions and services are further fueling the growth of the end-user computing market.

- Moreover, the adoption of data centers is accelerating the growth of the professional cloud services market. Northern Virginia had the highest data center net absorption among the leading data center markets in the United States in 2022, amounting to 303.3 megawatts. This trend will continue as more companies adopt cloud-based solutions and services to meet their computing needs. Overall, North America's dominance in the end-user computing market is expected to continue due to its technological advancements, adoption of BYOD culture, and growth in cloud-based solutions and services.

End User Computing Industry Overview

The end-user computing market is expected to be semi-consolidated, with both regional and global players dominating the market with their technological expertise. Many companies are adopting strategic partnerships to gain shared benefits and strengthen their position in the market.

- April 2023 - IGEL has announced the launch of the new COSMOS endpoint platform, which allows employees to have an incredible workspace experience by enabling them to access any digital workspace from any device into any cloud and gives EUC administrators the ability to provide greater security, management, and control through its new Operating System, updated administrative console and a number of new cloud services.

- November 2022 - XenTegra and Mindcentric formed a new company called XenTegra ONE, which leverages XenTegra's extensive technological know-how. This has provided enterprise clients with improved end-user computing, cloud computing, and data center infrastructure solutions. While Mindcentric will remain a separate business, it will represent XenTegra as its SMB sales and support division.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Drive to Increase the Productivity of Employees with Technology

- 4.4.2 Increasing Use of Cloud

- 4.5 Market Restraints

- 4.5.1 Issues Associated with Transformation and Integration of Processes By Organizations

- 4.6 Assessment of Impact of Covid-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Solution

- 5.1.1.1 Virtual Desktop Infrastructure

- 5.1.1.2 Device Management

- 5.1.1.3 Other Solutions (Unified Communication, Software Asset Management)

- 5.1.2 Services

- 5.1.1 Solution

- 5.2 Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small & Medium Enterprises

- 5.3 Deployment Mode

- 5.3.1 On Premise

- 5.3.2 Cloud

- 5.4 End user Industry

- 5.4.1 IT and Telecom

- 5.4.2 Banking, Financial Services, and Insurance

- 5.4.3 Healthcare

- 5.4.4 Retail

- 5.4.5 Other End user Industries (Media & Entertainment, Government, Education, Transportation and Logistics)

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Nutanix, Inc.

- 6.1.2 Fujitsu Ltd.

- 6.1.3 Genpact

- 6.1.4 HCL Infosystems Limited

- 6.1.5 IGEL Technology

- 6.1.6 Infosys Limited

- 6.1.7 Mindtree Limited

- 6.1.8 NetApp, Inc.

- 6.1.9 Nucleus Software Exports Limited

- 6.1.10 Citrix Systems, Inc.

- 6.1.11 Tech Mahindra Limited

- 6.1.12 Vmware, Inc.

- 6.1.13 Hitachi Systems Micro Clinic

- 6.1.14 Dell Technologies

- 6.1.15 Amazon Web Services

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日