クラウドインフラサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Cloud Infrastructure Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644268

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

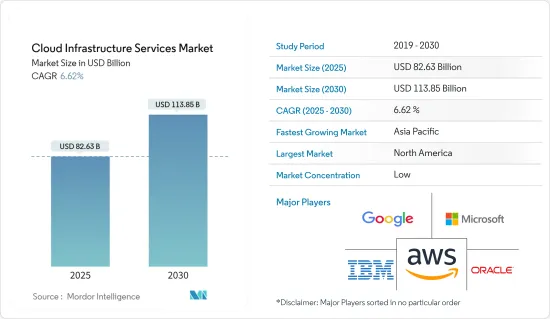

クラウドインフラサービス市場規模は、2025年に826億3,000万米ドルと推定され、2030年には1,138億5,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.62%です。

市場の主な成長促進要因は、低コスト、拡張性、柔軟性、セキュリティなどです。クラウドインフラサービスは、市場投入までの時間(TTM)を短縮し、迅速なアプリケーション開発と実行プロセスを実現します。さらに、ITインフラの運用コストとメンテナンスを削減するニーズの拡大も、クラウドインフラサービスの採用を後押ししています。

主なハイライト

- クラウドインフラサービス市場の成長を促す主な要因の1つは、世界のデータ量の増加です。データの安全性、完全性、サービス提供の向上を目的とした顧客によるクラウドベースの技術採用の増加や、世界のインターネットの普及率およびスマートフォンの普及率の上昇が、市場成長の要因となっています。

- サービスタイプ別に見ると、サービスとしてのストレージは、予測期間中により大きな市場規模を維持すると予想されます。Eurostatによると、EUにおけるクラウドコンピューティングの主な用途は電子メールサービスとファイルストレージで、それぞれ66%と53%を占めています。電子メール管理は安定しているが、ファイル・ストレージの用途は15%も増加しています。その他の最近のニーズとしては、企業のデータベースのホスティング、特に仮想専用サーバー(VPS)のホスティングが挙げられます。

- IaaSのメリットも増加しており、市場の成長機会となっています。マイクロソフトを含む主要プロバイダーは、Dynamics 365やOffice 365、Windows as a Serviceなど、自社のソリューションをクラウド関連モデルに急速に移行させています。Office 365、Windows as a Serviceなどです。全体として、クラウドの成長はIaaSの開発によって推進されているだけでなく、グーグル、マイクロソフト、IBMといった3つの有能なクラウドプレーヤーによって後押しされています。

- しかし、世界なクラウドインフラサービスは、高い帯域幅コスト、頻繁な監視と制御、セキュリティへの懸念、制御を後退させたくないという姿勢、クラウドプロバイダのネットワークが遅い場合のパフォーマンス管理など、いくつかの課題に直面しています。

- COVID-19により、クラウドインフラサービスとサポート・サービスは世界的に影響を受けています。パンデミックによる現在の危機は、企業が在宅勤務の手配をサポートするためにサービスパートナーを利用する必要があるため、短期的には多くの契約で業務量が増加し、市場を押し上げる可能性があります。

クラウドインフラサービス市場の動向

パブリッククラウドが圧倒的な市場シェアを占める

- パブリッククラウドベースの展開モデルは、その費用対効果と容易な可用性から需要が拡大しています。パブリッククラウドはクラウドコンピューティング・モデルに基づいており、需要に応じて複数の企業間でリソース(CPU、サーバー、ラックなど)を共有します。

- パブリッククラウドベースのソリューションは、物理的なセットアップやメンテナンスが少なくて済み、いつでもどこからでも24時間365日アクセスできます。スケーラビリティ、信頼性、柔軟性、ユーティリティ・スタイルのコスト、場所に依存しないサービスなど、パブリッククラウドのさまざまな利点により、パブリッククラウドベースの導入は高い成長率を記録すると予想されます。

- パブリッククラウドインフラサービス・プロバイダーのうち、Visual Capitalistによると、AWSは190カ国に100万人以上のアクティブ・ユーザーを抱えており、パブリッククラウド市場全体の41.5%をカバーしているといいます。

- 市場ベンダーは、パブリッククラウドインフラに対する需要の高まりに対応するため、常に製品やサービスを強化しています。例えば、Oracle Cloud Infrastructure(OCI)は昨年6月、パブリッククラウドサービスを自社内の顧客に提供するための新サービス「OCI Dedicated Region」を発表しました。

北米がクラウドインフラサービス市場を牽引

- 現在、北米はクラウドベースのITサービスの導入が加速していること、ITインフラ関連企業がクラウドインフラの研究開発に莫大な投資を行っていることから、世界のクラウドインフラサービス市場シェアを独占しています。

- 米国は、主要ベンダーの参入と、データセンターのコスト削減と事業継続性の向上を目的としたクラウドベースのサービス導入率の急上昇により、クラウドインフラサービス業界を支配しています。市場の成長には、グーグル、アマゾン、マイクロソフトといった大手テクノロジー企業の存在も関係しています。

- また、この地域はテクノロジー新興企業の主要拠点でもあります。有利な事業環境と政府の支援政策が、先進的なクラウドプラットフォームを開発する企業を後押ししています。さらに、著名な技術企業がクラウド技術へのベンチャー投資を増やしていることも、市場の成長を後押ししています。

- 北米では、熟練した労働力が確保できること、中小企業や大企業がクラウドインフラサービスへの参入と成長に熱心に取り組んでいることも、同地域でクラウドインフラサービスを採用する主な促進要因となっています。

- また、高度なアプリケーション開発技術の採用とデータ量の増加も、予測期間中の市場成長の大きな原動力となると思われます。パブリッククラウドは、低コスト、オンデマンドの可用性、セキュリティの向上により、この地域で大きな支持を得ています。

クラウドインフラサービス産業の概要

クラウドインフラサービス市場は競争が激しく、複数の大手企業が参入しています。市場競争は激化しており、企業は市場投入までの時間を短縮するためにより高度なビジネスモデルを模索し、ビジネスの俊敏性を高めるためにクラウドインフラストラクチャへの移行を進めています。注目すべき企業は、費用対効果の高い製品ポートフォリオを提供するため、常に技術革新を続け、研究開発に費やしています。クラウドインフラサービス市場で事業を展開している主な企業は、AT&T、アリババ、ディメンション・データ、AWS、IBM、インタービジョン、オラクル、マイクロソフト、グーグルなどです。

2022年12月、マイクロソフトとLSEGは、株式取得を通じてLSEGに出資することで、次世代データ・アナリティクスとクラウドインフラ・ソリューションのための1年間の戦略的協業を発表しました。この取り決めにより、LSEGのデータプラットフォームやその他の主要技術インフラはマイクロソフトのAzureクラウド環境に移行します。

2022年10月、オラクルは、システムインテグレーターや通信事業者などのパートナーがクラウドサービスを販売し、顧客に提供できるようにするクラウドインフラストラクチャ・ポートフォリオの拡充を発表しました。クラウドインフラストラクチャ・プラットフォームは、特定の市場や業界のニーズに合わせたクラウドインフラストラクチャとプラットフォーム・サービスのフルセットを提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 産業バリューチェーン分析

- COVID-19がクラウドインフラサービス市場に与える影響分析

第5章 市場力学

- 市場促進要因

- 拡大するIaaSのメリット

- コスト削減と投資収益率(ROI)の向上

- エッジコンピューティングの利用拡大

- 市場の課題

- データ損失に対する懸念の高まり

- 高い帯域幅コストと頻繁な監視と制御

第6章 市場セグメンテーション

- サービスタイプ別

- Compute as a Service

- Storage as a Service

- Networking as a Service

- その他のサービスタイプ(Desktop as a Service、マネージドホスティング)

- 展開モデル別

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

- 組織規模別

- 中小企業(SMEs)

- 大企業

- 業界別

- BFSI

- IT・通信

- 小売

- ヘルスケア&ライフサイエンス

- 政府機関

- その他の業界別(エネルギー&公益事業、メディア&エンターテインメント)

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- IBM Corporation

- Oracle Corporation

- Alibaba Cloud

- Rackspace Inc.

- Fujitsu Limited

- CenturyLink, Inc.

- VMware, Inc.

- DXC Technology

- Dimension Data

- Verizon Wireless

- Tencent Holdings Ltd.

- AT&T Mobility LLC

- NEC Corporation

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Cloud Infrastructure Services Market size is estimated at USD 82.63 billion in 2025, and is expected to reach USD 113.85 billion by 2030, at a CAGR of 6.62% during the forecast period (2025-2030).

The primary growth drivers for the market include low costs, scalability, flexibility, and security. The cloud infrastructure service offerings accelerate Time-to-Market (TTM) and rapid application development and running processes. Moreover, the expanding need to decrease the operational costs and maintenance of the IT infrastructure also boosts several organizations' adoption of cloud infrastructure services.

Key Highlights

- One of the primary factors fueling the growth of the cloud infrastructure services market is the increase in data quantities worldwide. The increased adoption of cloud-based technologies by customers to improve data security, integrity, and service delivery, as well as increasing internet penetration and smartphone adoption rates worldwide, all contribute to market growth.

- Based on the service type, storage as a service, service type is expected to hold a larger market size during the forecast period. According to Eurostat, email services and file storage are the predominant uses for cloud computing in the EU, with 66% and 53%, respectively. Email management remains steady, while file storage purposes have increased by a whopping 15%. Other recent needs include hosting company databases, specifically virtual private server (VPS) hosting.

- Increasing IaaS benefits are also providing ample opportunities for the growth of the market. Principal providers, including Microsoft, are quickly moving their solutions to cloud-associated models such as Dynamics 365. Office 365, and Windows as a Service, to name a few. Overall, cloud growth is propelled not only by the development of IaaS but is also being encouraged by three talented cloud players, including Google, Microsoft, and IBM.

- However, global cloud infrastructure services face a few challenges, including high bandwidth costs, frequent monitoring and control, security concerns, unwillingness to retreat controls, and performance management in case of a slow cloud provider network.

- Due to COVID-19, cloud infrastructure services and support services have been affected globally. The current crisis due to the pandemic may see work volume increase for many of the contracts in the short term as firms need to use service partners to support home working arrangements, which could boost the market.

Cloud Infrastructure Services Market Trends

Public Cloud Holds a Dominant Market Share

- The public cloud-based deployment model sees growing demand due to its cost-effectiveness and easy availability. The public cloud is based on the cloud computing model, which shares resources (such as CPU, servers, and racks) among several businesses depending on their demand.

- Public cloud-based solutions need fewer physical setups and low maintenance and provide 24/7 accessibility from any time, anywhere. Due to various benefits of public clouds, such as scalability, reliability, flexibility, utility-style costing, and location independence services, public cloud-based deployments are expected to record a high growth rate.

- Among the public cloud infrastructure service providers, Visual Capitalist states that AWS has over a million active users spread across 190 countries, supporting that AWS covers 41.5% of the entire public cloud market.

- Market vendors are constantly enhancing their products and services to meet the rising demand for public cloud infrastructure. For instance, in June last year, Oracle Cloud Infrastructure (OCI) announced the launch of a new offering - OCI Dedicated Region - that would enable it to offer public cloud services to customers on its premises.

North America to Drive the Cloud Infrastructure Services Market

- At present, North America is commanding the global cloud infrastructure services market share due to an escalation in the adoption of cloud-based IT services and huge investments by organizations in IT infrastructure in the research and development of cloud infrastructure.

- The U.S. dominates the cloud infrastructure services industry due to the attendance of principal vendors and the soaring adoption rate of cloud-based services to decrease costs for data centers and improve business continuity. The market growth is also connected to the presence of major technology players such as Google, Amazon, and Microsoft.

- This area is also a principal center for technology start-ups. Favorable business conditions and supportive government policies have encouraged businesses to develop advanced cloud platforms. Moreover, prominent tech players' increasing venture capital in cloud technology has also driven market growth.

- The availability of skilled labor and the keen focus of SMEs and large enterprises to enter and grow in North America are also primary driving factors for adopting cloud infrastructure services in the region.

- The increasing adoption of advanced application development technologies and data volumes will also drive significant market growth during the forecast period. The public cloud is gaining massive approval in this region due to its low costs, on-demand availability, and improved security.

Cloud Infrastructure Services Industry Overview

The Cloud Infrastructure Services Market is highly competitive and consists of several major players. As the competition among market players increases, organizations are looking for more advanced business models to reduce their time to market and switching to cloud infrastructure to improve business agility. The notable members keep innovating and spending on research and development to present a cost-effective product portfolio. The major companies operating in the cloud infrastructure services market are AT&T, Alibaba, Dimension Data, AWS, IBM, InterVision, Oracle, Microsoft, and Google, among others.

In December 2022, Microsoft and LSEG announced a 1-year strategic collaboration for next-generation data and analytics and cloud infrastructure solutions by making equity investments in LSEG through the acquisition of shares. Under the arrangements, LSEG's data platform and other key technology infrastructure will migrate into Microsoft's Azure cloud environment.

In October 2022, Oracle announced the expansion of its cloud infrastructure portfolio that will allow partners such as system integrators and telcos to sell and deliver cloud services to their customers. The cloud infrastructure platform will offer the full set of cloud infrastructure and platform services tailored to the needs of specific markets and industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Analysis on the impact of COVID-19 on the Cloud Infrastructure Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing IaaS Benefits

- 5.1.2 Increased Cost-Savings and Return on Investments (ROI)

- 5.1.3 Growing Use of Edge Computing

- 5.2 Market Challenges

- 5.2.1 Rising Concerns of Data Losses

- 5.2.2 High Bandwidth Costs & Frequent Monitoring and Control

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Compute as a Service

- 6.1.2 Storage as a Service

- 6.1.3 Networking as a Service

- 6.1.4 Other Service Types (Desktop as a Service, Managed Hosting)

- 6.2 By Deployment Model

- 6.2.1 Public Cloud

- 6.2.2 Private Cloud

- 6.2.3 Hybrid Cloud

- 6.3 By Organization Size

- 6.3.1 Small and Medium-Sized Enterprises (SMEs)

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT & Telecommunications

- 6.4.3 Retail

- 6.4.4 Healthcare & Life Sciences

- 6.4.5 Government

- 6.4.6 Other End-user Verticals (Energy & Utilities, Media & Entertainment)

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amazon Web Services, Inc.

- 7.1.2 Google LLC

- 7.1.3 Microsoft Corporation

- 7.1.4 IBM Corporation

- 7.1.5 Oracle Corporation

- 7.1.6 Alibaba Cloud

- 7.1.7 Rackspace Inc.

- 7.1.8 Fujitsu Limited

- 7.1.9 CenturyLink, Inc.

- 7.1.10 VMware, Inc.

- 7.1.11 DXC Technology

- 7.1.12 Dimension Data

- 7.1.13 Verizon Wireless

- 7.1.14 Tencent Holdings Ltd.

- 7.1.15 AT&T Mobility LLC

- 7.1.16 NEC Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日