|

市場調査レポート

商品コード

1643238

中東・アフリカの発電機セット:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East And Africa Generator Sets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの発電機セット:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

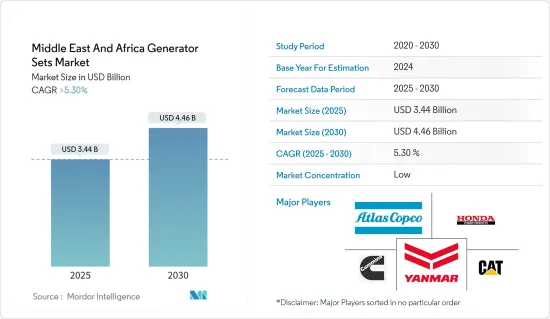

中東・アフリカの発電機セットの市場規模は2025年に34億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.3%以上で、2030年には44億6,000万米ドルに達すると予測されます。

主なハイライト

- 中断のない信頼性の高い電力供給に対する需要の増加などの要因が市場を牽引すると予想されます。

- 逆に、よりクリーンな代替品の入手可能性やバッテリー技術の進歩は、予測期間中の市場成長を抑制すると予想されます。

- とはいえ、ハイブリッド発電機の普及が進み、ハイブリッド・システムの信頼性が高まっていることは、様々な資源を利用することでコストを下げ、単一の燃料への依存を減らすことができるため、業界にとって好機となる可能性があります。

- ナイジェリアは、その人口の多さと経済成長の増加により、最大の市場になると予想されます。人口の増加に伴い、電力需要も増加すると予想されます。

中東・アフリカ発電機セット市場動向

市場を独占するバックアップ発電機

- アフリカのいくつかの国、特に西アフリカでは、毎日の電力使用量を満たすためにバックアップ発電機に大きく依存しています。バックアップ発電機は、ユーティリティ・グリッドからの電力供給に直面している消費者に、中断のない信頼性の高い電力供給を提供します。ユーティリティ・グリッドのトランスミッション・ネットワークと信頼性は、バックアップ発電機によって発電された電力と直接相関する可能性があります。送電網へのアクセスが高い北アフリカでは、サハラ以南の国々に比べてバックアップ発電機の使用は少ないです。

- 中東諸国では、Project Neom、住宅用ツインタワーElitz、ドバイ・クリーク・タワー、Res-Seaプロジェクト、複数のデータセンター・プロジェクトなど、停電につながる不測の事態に備えてバックアップ発電機を必要とするメガプロジェクトの建設が進んでいます。例えば、2022年、アル・マサウド・パワー社は、カズナ・データセンターにバックアップ電源として2000/2200KWのディーゼル発電機を供給しました。これは、同地域における発電機セットの市場規模を示すものです。

- また、2023年現在、サウジアラビアの建設業界は中東・アフリカ地域をリードし続けています。サウジアラビアはここ数年、プロジェクト受注額が最も高く、ビジョン2030に沿った国の変革が進んでいます。

- Arab Petroleum Investments Corporationによると、2021年から2025年にかけて、中東・北アフリカ(MENA)地域の電力セクターで計画されているエネルギー投資プロジェクトの割合は31%だった。次いでガス部門が27%、石油部門が20%、化学部門が22%となっています。これらのセクターで新たなプロジェクトが始まれば、バックアップ用発電機の需要は長期的に増加し、同地域の発電機市場の成長に寄与する可能性が高いです。

- そのため、バックアップ用発電機セットは、その柔軟な使用方法と、他の市場セグメントに比べて発電量に占める割合が大きいことから、今後も市場を独占し続けると予想されます。

市場を独占するナイジェリア

- ナイジェリアは、この地域でバックアップ発電機によって発電されたエネルギーの消費量が最も多い国のひとつです。これは、化石燃料の入手が容易であること、政府の政策が不十分でトランスミッション能力が低いこと、人口が増加して電力需要が増加していることなど、いくつかの要因によるものです。これらすべての要因が、消費者に小型のバックアップ発電機を使った発電を促し、市場の成長を後押ししています。

- ナイジェリア国家統計局によると、ナイジェリアで2022年に発電された電力は約2万1,243GWhで、前年の約3万5,654GWhから減少しました。電力会社の業績不振、送電網の崩壊、非効率な訓練を受けた人材、現地製造業者の不足、送電網設備の盗難、不確実な気象現象などの要因により、ナイジェリアの電力供給は大幅に減少しています。このため、ナイジェリアでは発電機セットの需要が必要となり、市場開拓に有利に働くと思われます。

- ガソリン発電機セットは、基本的な電力需要(3~5キロワット)しか供給できず、ディーゼル発電機よりもはるかに効率が低いが、ナイジェリアではバックアップ発電能力の大きな割合を占めています。これは主に、初期投資コストが低いためです。

- 2022年9月、ナイジェリア政府は、2020年と2021年に発電機セット、変圧器、掃除機、バリカン、その他の電気機械器具の輸入に52億6,000万米ドルを費やしたと発表しました。また、国家統計局は、ナイジェリアが必要とする電力の48.6%をガソリン、ディーゼル、ガスを燃料とする発電機から得ていることを明らかにしました。

- 世界銀行によると、ナイジェリアの電力アクセスは2021年時点で59.5%です。分散型発電やマイクログリッドなどのプロジェクトを展開する政府の努力にもかかわらず、ラストワンマイルのグリッド接続は今後も続くと思われます。このようなシナリオでは、発電機セットが電力供給の主役であり続けると思われます。

- そのため、ナイジェリアは人口の増加とトランスミッション能力の低さから、発電機セットの需要増につながり、市場を独占すると予想されます。

中東・アフリカの発電機セット産業の概要

中東・アフリカの発電機セット市場は、部分的に断片化されています。この市場の主要企業(順不同)には、Caterpillar Inc.、Cummins Ltd.、Yanmar Holdings、Atlas Copco AB、Honda Siel Power Products Limitedなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 中断のない信頼性の高い電力供給に対する需要の増加

- 発電機セット技術への技術介入

- 抑制要因

- よりクリーンな代替品の入手可能性とバッテリー技術の進歩

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 燃料タイプ別

- 天然ガス

- ディーゼル

- その他の燃料タイプ

- 定格別

- 0-75 kVA

- 75-375 kVA

- 375kVA以上

- 用途別

- 主電源

- バックアップ電力

- ピークカット

- 地域別

- ナイジェリア

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- カタール

- その他中東とアフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Cummins Inc.

- Kirloskar Oil Engines Limited

- Honda Siel Power Products Limited

- Yanmar Holdings Co. Ltd

- Caterpillar Inc.

- Mitsubishi Heavy Industries Ltd

- Perkins Engines Company Limited

- Atlas Copco AB

- 市場シェア

第7章 市場機会と今後の動向

目次

Product Code: 70388

The Middle East And Africa Generator Sets Market size is estimated at USD 3.44 billion in 2025, and is expected to reach USD 4.46 billion by 2030, at a CAGR of greater than 5.3% during the forecast period (2025-2030).

Key Highlights

- Factors such as increasing demand for uninterrupted and reliable power supply are expected to drive the market.

- Conversely, the availability of cleaner alternatives and advancement in battery technologies are expected to restrain market growth during the forecast period.

- Nevertheless, the increasing popularity of hybrid generators and the rising reliability of the hybrid system may be an opportunity for the industry due to its usage of various resources, driving down the cost and reducing dependence on a single fuel.

- Nigeria is expected to be the largest market due to its large population and increasing economic growth. The demand for electricity is expected to rise with an increase in the size of its population.

MEA Generator Sets Market Trends

Backup Power Generators to Dominate the Market

- Several African countries, especially Western Africa, heavily rely on backup power generators to meet daily electricity usage. The backup power generators provide an uninterrupted and reliable power supply to consumers facing load shedding from the utility grid supply. The transmission network and reliability of the utility grid may directly correlate with the power generated by the backup generators. North Africa, which includes higher grid access, uses backup generators less than the Sub-Saharan countries.

- The Middle-East countries are witnessing the construction of mega projects such as Project Neom, the residential twin-tower Elitz, the Dubai Creek Tower, the Res-Sea projects, and multiple Data Centre projects that would require back-power generators in unforeseen events leading to blackouts. For instance, in 2022, Al Masaood Power facilitated a 2000/2200-KW diesel generator to Khazna Data Centers for backup power. This represents a broad scope of generator sets market in the region.

- Also, as of 2023, Saudi Arabia's construction industry continued to lead the Middle-East and African region. The Kingdom witnessed the highest value of project awards in recent years, transforming the country in line with its Vision 2030.

- According to Arab Petroleum Investments Corporation, during 2021-2025, the share of planned energy investment projects in the power sector in the Middle-East and North Africa (MENA) region was 31%. The gas sector followed it with a share of 27%, the oil sector with 20%, and the chemical sector with 22%. With the onset of new projects in these sectors, the demand for backup power generators would likely increase in the longer term, benefitting the growth of the generator market in the region.

- Therefore, backup power generator sets are expected to continue to dominate the market due to their flexible use and significant share in electricity generation relative to other market segments.

Nigeria to Dominate the Market

- Nigeria is among the highest consumers of energy generated by backup generators in the region. It is due to several factors, including easy fossil fuel availability, poor governmental policies leading to low transmission capabilities, and an increasing population, leading to increased electricity demand. All these factors push consumers to produce their electricity using small backup generators, aiding the market's growth.

- According to the National Bureau of Statistics of Nigeria, nearly 21,243 GWh of electricity was generated in Nigeria in 2022, a decline from around 35,654 GWh in the previous year. Factors such as poor utility performance, grid collapse, inefficient trained personnel, shortage of local manufacturing, theft of grid equipment, and uncertain weather events have significantly decreased the electricity supply in Nigeria. This would necessitate demand for generator sets in the country and benefit its market development.

- Although gasoline generator sets can provide only basic electricity needs (3 - 5 KW) and contain much lower efficiency than diesel generators, they make up a large share of backup generation capacity in the country. This is primarily due to their lower initial investment costs.

- In September 2022, the government of Nigeria announced that it had spent USD 5.26 billion importing electric generator sets, transformers, vacuum cleaners, hair clippers, and other electrical machinery and equipment in 2020 and 2021. Also, the National Bureau of Statistics disclosed that Nigeria gets 48.6% of its electricity needs from generators powered by petrol, diesel, and gas.

- As per the World Bank, electricity access in Nigeria stood at 59.5% as of 2021. The last-mile grid connectivity will persist in the future despite government efforts to roll out projects such as distributed electricity generation and microgrids. In such a scenario, the generator sets will remain the mainstay to deliver electricity.

- Hence, Nigeria is expected to dominate the market due to its growing population and low transmission capabilities, leading to increased demand for generator sets.

MEA Generator Sets Industry Overview

The Middle-East and African generator sets market is partially fragmented. Some key players in this market (in no particular order) include Caterpillar Inc., Cummins Ltd, Yanmar Holdings Co. Ltd, Atlas Copco AB, and Honda Siel Power Products Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing demand for uninterrupted and reliable power supply

- 4.5.1.2 Technological Interventions in generator set technologies

- 4.5.2 Restraints

- 4.5.2.1 Availability of Cleaner Alternatives and Advancement in Battery Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Natural Gas

- 5.1.2 Diesel

- 5.1.3 Other Fuel Types

- 5.2 Ratings

- 5.2.1 0 - 75 kVA

- 5.2.2 75 - 375 kVA

- 5.2.3 Above 375 kVA

- 5.3 Application

- 5.3.1 Prime Power

- 5.3.2 Backup Power

- 5.3.3 Peak Shaving

- 5.4 Geography

- 5.4.1 Nigeria

- 5.4.2 Saudi Arabia

- 5.4.3 South Africa

- 5.4.4 United Arab Emirates

- 5.4.5 Qatar

- 5.4.6 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cummins Inc.

- 6.3.2 Kirloskar Oil Engines Limited

- 6.3.3 Honda Siel Power Products Limited

- 6.3.4 Yanmar Holdings Co. Ltd

- 6.3.5 Caterpillar Inc.

- 6.3.6 Mitsubishi Heavy Industries Ltd

- 6.3.7 Perkins Engines Company Limited

- 6.3.8 Atlas Copco AB

- 6.4 Market Share