光インターコネクト:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Optical Interconnect - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643138

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

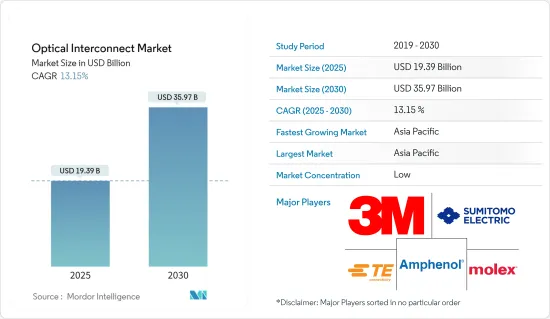

光インターコネクトの市場規模は、2025年に193億9,000万米ドルと推定され、2030年には359億7,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは13.15%です。

産業界全体でCOVID-19が悪影響を及ぼしているため、3Mのような企業は現在、COVID-19対策として、世界のさまざまな利害関係者を支援する医療用製品を製造しています。3Mは、米国、アジア、欧州を含む世界各地の製造施設で、N95レスピレーターの生産量を年間11億個に倍増させました。これにより、光インターコネクトケーブルの製造は減少しました。

しかし、在宅勤務が絶対的な必需品となったため、ネクスコム(台湾)のような市場プレーヤーは、世界中の通信プロバイダーやデータセンターの仮想化と容量拡大を支援する計画です。より高速なネットワーク需要に対応するため、NC 220FMS3モジュールはPCIe3.0 x16インターフェースと2つのQSFP28ポートを提供し、それぞれが100Gb/秒イーサネット接続をサポートします。このモジュールは、パケットロスのない高速接続を提供します。100G光トランシーバ(100Gb/秒イーサネットを提供)、そのフォームファクタタイプ、および規格は、相互接続市場開拓の主な原動力と見なされるコストと消費電力に応じて開発されており、光相互接続の需要を潜在的に牽引しています。

主なハイライト

- さらに、直接変調VCSELアレイ、パラレルファイバーリボン、ディテクタアレイは、光バックプレーンの容量問題に高度に適用されています。今後、光インターコネクトの新たな動向として、クロスコネクト・スイッチや光領域でのデータパケットルーティングなどの機能を含む、さらなる高機能化が大いに期待されています。

- 通信帯域幅の需要増が市場を牽引すると予想されます。さまざまな種類の通信における多数の新サービスとその付加価値事業体の出現により、帯域幅に対する需要はかつてないほど高まっています。光インターコネクトは、電気インターコネクトと比較して、より多くの帯域幅を提供することが可能で、コンピューティング性能に大きな利点をもたらします。

- 今後10年間で、クロスチップ通信に必要なエネルギーは0.5 pJ b1未満に、オフチップ通信技術などの通信に必要なエネルギーは0.1 pJ b1未満になると考えられています。データを安価に移動させる能力を活用することで、このような将来のマルチコア・プロセッサ・システムの消費電力と総コストの両方が、帯域幅の向上とともに削減されることが期待されます。

- 2020年の初めから、Ciena、Infinera、Huawei、Nokiaなどのベンダーは、最新のオプティクスの限界に課題してきました。ファーウェイのCloudFabric EVNレイヤー2 DCIソリューションは、IP WAN全体で最大32のデータセンターを拡張できる、拡張性の高い効率的なレイヤー2相互接続を提供します。ファーウェイと同様に、CienaやInfineraなどの競合ベンダーも800G対応のコヒレントソリューションに取り組んでおり、次世代光DCIプラットフォームの動力源となる可能性があります。

- 2020年第2四半期までに、何百万人もの人々が在宅勤務に切り替え、ビデオ消費量(世界のデータトラフィックの60%に相当)は史上最高を記録しました。クリティカルなサービスが影響を受け、Wi-Fiアクセスポイントは輻輳に直面し、FWAは制限を受け、相互接続ポイントは負担を強いられていました。

- このようなシナリオは、クラウド・コンピューティング活動にも波及し、産業・企業セグメントからの投資も大幅に増加しました。これらすべての要因が、データセンターの機能を拡張するために組み込まれた技術とともに、データセンター市場に大きなブームをもたらしました。このような動向は、この市場の成長をさらに刺激するものと期待されています。

光インターコネクト市場動向

データ通信が光インターコネクトの需要に拍車をかける見通し

- 光相互接続の主な用途の1つは、データセンターネットワーク、無線アクセスネットワーク、有線アクセスネットワークなどのデータ通信ネットワークです。電子パケットスイッチをベースとする現在のデータセンターネットワークは、クラウドコンピューティングの発展によりネットワークトラフィックが急激に増加しています。光インターコネクトは、高スループット、低遅延、低消費電力を実現する有望な代替手段として登場しました。

- IEEE Communicationsによると、全光ネットワークはデータセンターで最大75%の省エネを実現できるといいます。特に企業で使用される大規模データセンターでは、電力効率が高く、高帯域幅で低遅延の相互接続を使用することが最も重要であり、このようなデータセンターへの光相互接続の導入に大きな関心が寄せられています。

- 現在、データセンターで利用されている光技術はポイント・ツー・ポイントのリンクに限られており、これは旧来の通信ネットワーク(不透明なネットワーク)で利用されていたポイント・ツー・ポイントの光リンクと同じです。しかし、光スイッチ相互接続はまだ研究段階にあります。

北米が高い市場成長を遂げる

- インターネットの急速な普及が、この地域の市場成長を高めると予想されています。また、シスコシステムズによると、2021年の北米のクラウドトラフィックは年間6844エクサバイト程度になると推定されており、これは他の地域と比較して最も高いです。エリクソン・モビリティ・レポートの2020年11月版によると、北米では2020年末にモバイル契約の約4%が5Gになると予想されています。したがって、このような動向は、セルタワーやその他のアプリケーションが5Gトランスミッションに対応できるようにするための強力な相互接続が必要となるため、市場に余地をもたらします。

- また、北米には、光インターコネクト製品やソリューションを提供する様々なプレーヤーがおり、10倍程度の低電力でインターコネクト帯域密度を向上させる新しいソリューションの革新にも熱心なプレーヤーもいます。例えば、2020年3月、Ayar Labsは、Lockheed Martin Venturesから戦略的投資を受けたと発表しました。この資金は、高帯域幅、低レイテンシ、電力効率の高いショートリーチ相互接続を必要とするアプリケーション向けに、Ayar Labsの特許取得済みモノリシックインパッケージ光I/O(MIPO)ソリューションの商用化を加速するために使用されます。

- さらに、データセンター内のデータ移動は重要な機能になりつつあり、米国やカナダではデータセンターサービスを活用する新規事業が増加しているため、M2M(マシン・ツー・マシン)トラフィックがより多く活用されることになります。この問題を解決する鍵として、IBMはデータセンターに光スイッチを提供することに注力しています。IBMは、シリコンフォトニック技術を使った再構成可能な光スイッチの構築に取り組んでいます。実現すれば、この光ソリューションは光インターコネクト市場の新たな動向となります。

- 2020年6月、相互接続とデータセンターの世界的企業であるエクイニクスは、カナダ全土にある13のデータセンターのポートフォリオを、BCE Inc.から7億5,000万米ドルで全額現金取引により購入することで合意したと発表しました。ベル・データセンター25施設に相当する13のデータセンターは、年間約1億500万米ドルの収益を生み出す見込みです。

光相互接続業界の概要

光相互接続市場は細分化された市場であり、複数の主要ベンダーやその他の有力ベンダーが存在するのが特徴です。主要ベンダーは、新たな技術革新や買収とともに、光インターコネクトの開発コースやそのメリットに関する認知度向上にますます注力しています。さらに、世界のベンダーは、戦略的提携や投資を通じて、市場での安定化を図っています。主なプレーヤーは、3M、住友電気工業など。

- 2020年12月コーニング社が4億5,000万米ドルを投じてノースカロライナ州コンコードにあるCabarrus Countyの光ファイバーケーブル工場を拡張、475人の新規雇用を創出し、このような施設としては世界最大となります。

- 2020年11月光ネットワークプリンシパルのアーキテクチャに基づくチップソリューションを製造するAyar LabsがシリーズBラウンドで3,500万米ドルを調達。同社のCEOによると、この資金調達は製品の開発を継続し、さらなる商業化に取り組むために使用されます。同社の技術の主な応用分野は、航空宇宙や政府機関への応用、人工知能や高性能コンピューティング、通信やクラウドアプリケーション、自動運転車やその他の自律走行システム用のライダーなど、大量のデータが移動するあらゆる場所での次世代コンピューティングです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドコンピューティング、AI、HPC需要による通信帯域幅需要の増加

- データセンターの相互接続と光ファイバー通信への投資の増加

- 市場抑制要因

- 光インターコネクション関連技術の商用化の遅れ

- 産業バリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- タイプ別

- 光トランシーバー

- アクティブ光ケーブル(AOC)

- 組み込み型光モジュール(EOMs)

- 用途別

- 電気通信

- データ通信

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M Company

- Sumitomo Electric Industries Ltd

- Molex LLC

- Amphenol Corporation

- TE Connectivity Ltd.

- Go!Foton Inc.

- II-VI Incorporated

- Corning Incorporated

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Optical Interconnect Market size is estimated at USD 19.39 billion in 2025, and is expected to reach USD 35.97 billion by 2030, at a CAGR of 13.15% during the forecast period (2025-2030).

Due to the adverse effects of COVID 19 across industries, players such as 3M are currently manufacturing medical products to assist various stakeholders globally, to combat Covid-19. 3M has doubled production of N95 respirators to 1.1 billion per year at its global manufacturing facilities, including in the U.S., Asia, and Europe. This has led to reduced manufacturing for optical interconnect cables.

However, as the ability to work from home has become an absolute necessity, market players such as Nexcom (Taiwan) plans to help telecom providers and data centers across the world to virtualize and expand capacity. For meeting current network demands for faster speeds, the NC 220FMS3 module provides a PCIe3.0 x16 interface and two QSFP28 ports, each supporting 100Gb/s Ethernet connectivity. The module provides high-speed connectivity without any packet loss. The 100 G optical transceivers (providing 100Gb/s ethernet), their form factor type, and standard are developed according to the cost and power consumption, which are regarded as the main drive in the development for interconnect market, which potentially drives the demand of optical interconnect.

Key Highlights

- Moreover, directly modulated VCSEL arrays, parallel fiber ribbons, along with detector arrays, are highly being applied to optical backplane capacity issues. In the future, additional higher functionality is highly expected as an emerging trend for optical interconnects, which includes features such as cross-connect switches and data packet routing in the optical domain.

- The increasing demand for communication bandwidth is expected to drive the market. Due to the emergence of a large number of new services in different types of communications and their value-added entities, the demand for bandwidth has gone up more than ever before. Optical interconnect drive it possible in providing more bandwidth and bring great advantage to computing performance, compared to electrical interconnects.

- With optics, over the next decade, it is believed that the energy-requiring for cross-chip communication would approach less than 0.5 pJ b1 and to 0.1 pJ b1 for communication, such as off-chip communication technology. By utilizing the ability to move data affordably, both the power consumption and the total cost for such future multicore processor systems are expected to be reduced with improving bandwidth.

- Since the beginning of 2020, vendors, like Ciena, Infinera, Huawei, and Nokia, have been pushing the limits of modern optics. Huawei CloudFabric EVN Layer 2 DCI solution provides highly permits scalable, efficient layer 2 interconnection that allows expansion of up to 32 data centers across IP WANs. Like Huawei, competing vendors, like Ciena or Infinera, are also working on their 800G-capable coherent solutions, which may power next-generation optical DCI platforms.

- By the second quarter of 2020, millions of people switched to work from home, and video consumption (which amounts to 60% of the global data traffic) was at an all-time high. Critical services were being impacted, and Wi-Fi access points were facing congestion; FWA witnessed limitations, and interconnect points were burdened.

- These scenarios also surge the cloud computing activities, along with significantly increasing investments from the industrial and enterprises segment. All these factors made a massive boom in the data center market along with technologies incorporated to expand the capabilities of data centers. Such trends are expected to further stimulate the growth of the market studied.

Optical Interconnect Market Trends

Data Communication is Expected to Spur the Demand for Optical Interconnects

- One of the major applications of optical interconnectivity is within data communication networks which include datacenter networks, wireless access networks, and wired access networks. Current data center networks, which are based on electronic packet switches, experiences an exponential increase in network traffic due to cloud computing development. Optical interconnects emerged as a promising alternative that offers high throughput, low latency, and reduced power consumption.

- According to IEEE Communications, all-optical networks could provide up to 75% energy savings in the data centers. Especially in large data centers used in enterprises, the use of power efficient, high bandwidth, and low latency interconnects is of paramount importance, and there is significant interest in the deployment of optical interconnects in these data centers.

- Currently, optical technology is utilized in data centers is only for point-to-point links, which is in the same way as point-to-point optical links that were used in older telecommunication networks (opaque networks). However, optically switched interconnects are still in the research phase.

North America To Witness High Market Growth

- The rapid penetration of the internet is expected to raise the growth of the market in this region. Moreover, according to Cisco Systems, the cloud traffic in 2021 is estimated to be around 6844 exabytes per year in North America, which is highest in comparison to other regions. According to the November 2020 edition of the Ericsson Mobility Report, North America was expected to end 2020 with about 4% of its mobile subscriptions being 5G. Hence, such trends create scope for the market, as a powerful interconnect is required to enable cell towers and other applications to handle 5G transmissions.

- Also, North America has various players that provide optical interconnect products and solutions, along with players who are also keen to innovate new solutions for the improvement in interconnect bandwidth density at around 10x lower power. For instance, in March 2020, Ayar Labs announced that it had received a strategic investment from Lockheed Martin Ventures, where the funds will be used to accelerate the commercialization of Ayar Labs' patented monolithic in-package optical I/O (MIPO) solution for applications that require high bandwidth, low latency, and power-efficient short-reach interconnects.

- Moreover, data movement within the data center is becoming a critical feature, and the rise in the ample of new businesses leveraging data center services in the United States, and Canada will leverage more machine-to-machine (M2M) traffic. To overcome this problem, IBM focuses on providing optical switches in the data center as a key to resolve the problem. IBM is undertaking to build reconfigurable optical switches using silicon-photonic technology. If implemented, this optical solution becomes a new trend in the optical interconnect market.

- In June 2020, Equinix Inc., the global interconnection and data center company, announced its agreement to purchase a portfolio of 13 data centers across Canada from BCE Inc for USD 750 million in an all-cash transaction. The 13 data center sites representing 25 Bell data center facilities are likely to generate approximately USD 105 million annualized revenue.

Optical Interconnect Industry Overview

The Optical Interconnect Market is fragmented in nature and is characterized by the presence of several key vendors and other prominent vendors. The key vendors are increasingly focusing on creating awareness about the optical Interconnect development courses and their benefits, along with new innovation and acquisitions. Further, global vendors are trying to stabilize themselves in the market, through strategic collaborations and investements. Key players are 3M, Sumitomo Electric Industries, etc.

- December 2020 - Corning Inc. spent USD 450 million to expand its Cabarrus County fiber optic cable plant in Concord, N.C., generating 475 new jobs and making it the largest such facility in the world.

- November 2020 - Ayar Labs, which makes chip solutions based on optical networking principal's architecture raised USD 35 million in a Series B round of funding. According to the company's CEO, the funding will be used to continue developing its product and working on further commercialization. The main application area for the company's technology is next-generation computing, anywhere that there is a massive movement of data, including aerospace and government applications, artificial intelligence and high-performance computing, telecoms and cloud applications, and lidar for self-driving car and other autonomous systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Communication Bandwidth Owing to Demand for Cloud Computing, AI, and HPC

- 4.2.2 Increasing Investment in Data Centers Interconnect and Fiber Optic Communication

- 4.3 Market Restraints

- 4.3.1 Slow Commercialization of Optical Interconnection Related Technologies

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Impact of Covid-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Optical Transceivers

- 5.1.2 Active Optical Cables (AOCs)

- 5.1.3 Embedded Optical Modules (EOMs)

- 5.2 Application

- 5.2.1 Telecommunication

- 5.2.2 Data Communication

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M Company

- 6.1.2 Sumitomo Electric Industries Ltd

- 6.1.3 Molex LLC

- 6.1.4 Amphenol Corporation

- 6.1.5 TE Connectivity Ltd.

- 6.1.6 Go!Foton Inc.

- 6.1.7 II-VI Incorporated

- 6.1.8 Corning Incorporated

- 6.1.9 Cisco Systems Inc.

- 6.1.10 Huawei Technologies Co. Ltd

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日