|

市場調査レポート

商品コード

1642184

欧州のマネージドサービス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Europe Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のマネージドサービス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

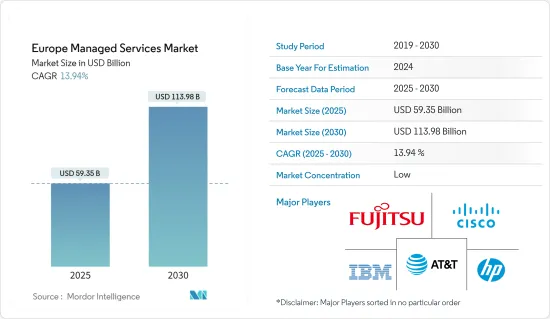

欧州のマネージドサービス市場規模は、2025年に593億5,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは13.94%で、2030年には1,139億8,000万米ドルに達すると予測されます。

主なハイライト

- クラウドサービスの採用拡大、クラウドの多様化、設備投資を最小限に抑えIT予算を最大限に活用しようとするIT企業の意欲などの要因が、調査対象市場の成長を引き続き後押ししています。

- 人工技術とクラウド管理は、さまざまな機能的ビジネス要件とマネージドサービスに対応し、生み出される仕事の質を犠牲にすることなく、低コストで組織の効率的な運営を支援します。主要な市場参入企業は、新しいアイテムの創出や製品の多様化に投資を行っています。また、信頼性が高く手頃な価格のサービスを提供するための研究開発も行っています。例えば、2022年8月、野村総合研究所(NRI)は、「NRIの製品開発への投資」を発表しました。(NRI)は、欧州におけるマネージドサービスの提供体制を強化するため、NRI欧州デンマーク支店にマネージドサービス専用ルームを開設しました。

- 欧州地域は、主要な自動車製造市場の一つです。近年、自動車産業は激変の時代を迎えており、生産される自動車はコネクテッド化、自律走行化、オンデマンド共有化、電動化が見込まれています。自律走行の出現には、AIやリアルタイムの意思決定システムの学習に必要な膨大なデータ量などの課題があります。富士通のようなサービス・プロバイダーは、データ量を減らし、関連するデータのみを収集する分散型で管理するソリューションを提供しています。

- さらに、大手企業はビジネスを強化するため、欧州でパブリック・クラウドのセットアップを進めています。例えば、マイクロソフトは最近、ドイツに2つの新しいクラウド地域を提供する計画を発表し、欧州および世界中のより多くの組織や会社がパブリッククラウド・ソリューションでデジタル変革できるようにしました。これらの新しいリージョンは、Microsoft Azure、Office 365、Dynamics 365の全機能、エンタープライズグレードのセキュリティ、および顧客がコンプライアンスや規制要件を満たすためのその他の機能を提供します。

- さらに、IoTによって企業は、顧客が情報にアクセスする方法を再評価し、顧客に最適な戦略を策定する必要に迫られています。毎年何百万という新しいガジェットがインターネットに接続し、すでに複雑な状況や、多くのチャネルが提供する統合の課題やサイバー脅威を理解することは事実上不可能になっています。したがって、マネージドサービス・プロバイダーは、この時点でIoTエコシステムの各階層のセキュリティを向上させることができ、企業がIoTをイノベーションに活用し、資格のあるリソースと24時間体制のサポート・サービスを提供することでテクノロジーの最先端にとどまることを可能にします。

- しかし、マネージドサービスは優れたメリットを提供するもの、信頼性への懸念など特有の課題があり、予測期間中の市場の成長を阻害する可能性があります。重要なビジネス・インフラのホスティングをMSPに依頼するプロセスでは、プロバイダーのビジネスが彼らとの関係に耐えられるかもしれないという確信が伴う。プロバイダーが市場での競争を維持できなくなった場合、プロバイダーに依存している企業は、ウェブホスティング、電子メール、カレンダー、その他の重要なインフラを全面的に交換しなければならなくなる可能性があります。

- さらに、パンデミックによって、組織の災害復旧計画(DRP)や事業継続計画(BCP)のギャップも明らかになった。これらの計画のほとんどはパンデミックに対応できず、組織は分散した遠隔地の従業員に対応するためにITインフラの移行に奔走することを余儀なくされました。パンデミックは、運用リスクを引き起こす前にセキュリティ・インシデントを検出するために、テクノロジーとサービスを監視することの重要性を浮き彫りにしました。したがって、COVID後の期間は、欧州のマネージドサービス市場の成長機会を促進すると予想されます。

欧州のマネージドサービス市場の動向

クラウド分野は高い成長ペースが見込まれる

- 同地域におけるデジタルトランスフォーメーションに伴い、組織はITが提供する創造的なアプリケーションや拡張機能の成功に依存するようになっています。これは、ほとんどの組織にとって重要な競争力となっています。さらに、ITアウトソーシングは、クラウド移行やクラウドサービスオプションによって、単なるコスト削減手法以上のものとなっています。したがって、この新しい形態は、ビジネスの成長、顧客経験、競合の混乱に関する組織の動機によって推進されています。

- クラウド・アウトソーシングの需要が高まっていることは、欧州の会社がデータ保存の目的で公開ソースのクラウドプラットフォームを好んでいることを示しています。また、クラウド上で事業を展開する企業は、セキュリティ上の脅威を懸念し、ITセキュリティ・サービスをアウトソーシングすることであらゆる脅威を排除する可能性が高いです。このように、ベンダーの専門知識が要求されるとともに、責任の委譲が容易になります。

- ユーロスタットによると、EU企業におけるクラウド・コンピューティングの利用は近年大幅に増加しています。業界筋はさらに、欧州地域ではIaaSとSaaSの導入が進んでおり、ハイブリッド・クラウドの需要が高まっていることを示唆しています。さらに、2030年までに欧州企業のクラウド先端技術の利用を75%に拡大するというEUの「デジタルの10年(Digital Decade)」など、いくつかの地域的な取り組みも、同市場の成長を後押ししています。

- BYOD(Bring-your-own-device)とIoT(Internet of things)がクラウド導入の成長を後押ししています。クラウドベースのソリューションは主に、IoTによって生成されたデータから価値を引き出すために活用されているからです。これは、パブリック、プライベート、ハイブリッドのクラウドモデルによって支えられています。さらに、企業のレガシーITインフラは、IoTデバイスと接続するためにクラウドに依存しなければならない可能性があります。さらに、企業はパブリック・クラウドやプライベート・クラウド・サービスのいくつかの欠点を認識しています。企業は、それぞれのモデルの欠点を最小限に抑えながら、両方のアーキテクチャの利点を提供するハイブリッド・アプローチを模索しています。その結果、プライベート・システムとパブリック・システムで動作する2つ以上のアプリケーションを統合する、すなわちハイブリッド・クラウド・ホスティング・サービスという新たな動向が生まれつつあります。

- さらに、欧州でクラウドとハイブリッドITインフラの採用が拡大していることは、欧州各国でICT専門家を雇用する企業の割合が増加していることからも明らかです。例えば、デンマーク統計局によると、デンマークでは、ICT専門家を雇用する企業の割合は、2016年の25%から2022年には34%に増加しています。

マネージドセキュリティが大きな市場シェアを占める

- 競争力を維持するため、欧州全域の企業はその規模にかかわらず、マネージドサービス・プロバイダーにますます依存するようになっています。マネージドセキュリティ・サービス・プロバイダーは、適切な専門知識、ソリューション、価格モデルを提供することで、提供するサービスのポートフォリオに付加価値を与えています。マネージドセキュリティ・サービスは、この地域のダイナミックなビジネス空間における新興分野です。サービス・プロバイダーは、セキュリティとサポート・サービスを提供するために、マネージドセキュリティ・オペレーション・センター(SOC)を設立しています。ほとんどのサービス・プロバイダーは、顧客向けに独自の統合セキュリティ管理プラットフォームを展開し、セキュリティ情報・イベント管理(SIEM)やその他のモニタリング・ソリューション(SIEM)を提供しています。

- 技術の発展によるサイバーセキュリティの脅威の増大により、政府はサイバーセキュリティとMSSPに投資しています。例えば、AAG IT Services &Cyber Securityによると、2022年には欧州の企業の約39%がサイバー攻撃を受けたと報告しています。

- サーバーのインストールとセットアップ、顧客の要件に応じた承認済みソフトウェアのインストール、セキュリティ監視、ソフトウェアの更新と管理、データのバックアップと保護、その他多数のサービスを含む、フルマネージドのホストサービス。ドイツの多くの企業、特に新興企業や中小企業は、このようなソリューションを求めています。こうしたサービスは、サーバーをオンサイトで維持・管理するために多くの資金を必要とする中小企業や、適切なITチームを必要とする中小企業、あるいは業務上の要求のために時間的制約のある中小企業にとって、ビジネスチャンスを提供するものです。

- 同地域におけるデータ漏えいの増加は、マネージドセキュリティ・サービスを促進し、マネージドセキュリティ・ベンダーが市場シェアを獲得するために新製品を開発することを可能にすると予想されます。例えば、ツアーシャークによると、今年第3四半期のデータ漏洩件数は2,230万件を超え、ロシアが中東欧(CEE)諸国をリードしています。2位はウクライナ、3位はモンテネグロだった。

- ダッソー・システムズのような多くのフランス大手企業は、国内の新興企業エコシステムを強化するため、新興企業向けにカスタマイズされたサービスを簡単に導入できるパッケージ・ソリューション(SaaS、PaaS、IaaS)を提供しています。フランス政府は、Orange Business Servicesが提供する外部クラウドに非重要データをアウトソーシングするサービスの利用を決定しました。これは、容量の変動に完璧に対応するクラウドを利用するメリットを実感したためである(これにより、政府は新しいサービスをより迅速に導入するために必要な柔軟性を得ることができる)。

欧州のマネージドサービス業界の概要

欧州のマネージドサービス市場は、強力な顧客基盤を持つ国際的なプレーヤーによって支配されているため、断片化されています。また、各社は市場での地位を維持し、顧客を維持するために強力な競争戦略を採用しており、競争企業間の敵対関係が激化しています。主なプレーヤーは、富士通、IBM、シスコシステムズなどです。

- 2024年1月ビジネスISPおよびマネージドサービス・プロバイダーのEvolveは、イングランド北部でMS3の新しい10Gbps対応Fiber-to-the-Premisesブロードバンド・ネットワークに乗り込む最新のプロバイダーとなり、2025年末までに英国の535,000の施設に接続することを目指します。アステリオンからの不特定多数の投資がMS3を支援しており、158,779の敷地をカバーし(119,139のRFS)、急速に増加しています。EvolveはMS3との新たな提携により、MS3のXGS-PONネットワークを活用し、イースト・ライディングとリンカンシャー地域の企業に初めて新たなソリューションを提供します。

- 2023年12月BTとセキュア・アクセス・サービス・エッジ(SASE)のプレーヤーであるネットスコープは、ネットスコープの市場をリードするセキュリティ・サービス・エッジ(SSE)機能をBTの世界顧客に提供するための提携を発表しました。このパートナーシップは、両社が大企業のセキュリティとアクセスのニーズを満たすために協力してきたいくつかの大規模な顧客導入に続くものです。BTのデータによると、ハイブリッド・ワーキングは現在、世界・ワーカーの76%に求められており、より俊敏でセキュアな接続性が求められています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- ハイブリッドITへのシフトの増加

- コストと業務効率の改善

- 市場抑制要因

- 統合と規制の問題、信頼性への懸念

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- タイプ別

- マネージドデータセンター

- マネージドセキュリティ

- マネージドコミュニケーション

- マネージドネットワーク

- マネージドインフラストラクチャ

- マネージドモビリティ

- 企業規模別

- 中小企業

- 大企業

- 業界別

- BFSI

- 製造業

- ヘルスケア

- 小売

- その他業界別

- 国別

- 英国

- ドイツ

- フランス

- その他欧州

第7章 競合情勢

- 企業プロファイル

- Fujitsu Ltd

- Cisco Systems Inc.

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Nokia Solutions and Networks

- Deutsche Telekom AG

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Ltd

- NSC Global Ltd

- Telefonica Europe PLC

第8章 投資分析

第9章 市場機会と今後の動向

The Europe Managed Services Market size is estimated at USD 59.35 billion in 2025, and is expected to reach USD 113.98 billion by 2030, at a CAGR of 13.94% during the forecast period (2025-2030).

Key Highlights

- Factors such as the growing adoption of cloud services, growth in cloud diversification, and the willingness of IT companies to minimize capital expenditure and make the most of their IT budgets continue to drive the growth of the studied market.

- Artificial technology and cloud management address various functional business requirements and managed services and assist with the efficient operation of the organization at a low cost without sacrificing the caliber of the work produced. The key market participants are making investments in the creation of new items and the diversification of their product offerings. They are also conducting research and development efforts to provide dependable and affordable services. For instance, in August 2022, Nomura Research Institute, Ltd. (NRI), a leading provider of system solutions and consulting services and system solutions, launched a dedicated managed services room at the NRI Europe Denmark Branch in order to enhance its system for providing managed services in Europe.

- The European region is among the leading automotive manufacturing markets. In recent years, the automotive industry has entered into a period of radical change, with the vehicles being produced expected to be connected, autonomous, shared on-demand, and electric. The emergence of autonomous driving will have challenges, including huge data volumes required for training AI and real-time decision-making systems. Service providers, like Fujitsu, offer solutions that will decrease data volumes and manage them in a distributed fashion, where only the relevant data is collected.

- Furthermore, major players are setting up public cloud setups in Europe to empower businesses. For instance, Microsoft recently announced its plans to deliver two new cloud regions in Germany to equip more organizations and companies in Europe and worldwide to transform them digitally with public cloud solutions. These new regions will offer Microsoft Azure, Office 365, and Dynamics 365 full functionality features, enterprise-grade security, and other features to help customers meet compliance and regulatory requirements.

- Additionally, IoT has forced companies to re-evaluate how customers access information and develop a strategy to best reach them. Millions of new gadgets connect to the Internet every year, making it practically impossible to understand the already complex landscape and the integration challenges and cyber threats provided by many channels. Hence, managed service providers can improve security for each tier of the IoT ecosystem at this point, enabling firms to harness IoT for innovation and stay on the cutting edge of technology by providing qualified resources and round-the-clock support services.

- However, despite the managed services providing excellent benefits, the specific challenges, like reliability concerns, may obstruct the market's growth over the forecast period. The process of hiring an MSP to host critical business infrastructure involves the belief that the providers' business may endure the relationship with them. In case of any failure by the providers to sustain the competition in the market, the enterprises relying upon them may have to entirely replace web hosting, emails, calendars, and other critical pieces of infrastructure, without which it is not possible to conduct business.

- Moreover, the pandemic has also revealed gaps in organizations' disaster recovery plans (DRP) and business continuity plans (BCP). Most of these plans could not address the pandemic, forcing organizations to scramble to transition their IT infrastructure to accommodate a distributed and remote workforce. The pandemic highlighted the importance of monitoring technology and services in detecting security incidents before they cause operational risk. Hence, the post-COVID period is anticipated to drive growth opportunities in the European managed services market.

Europe Managed Services Market Trends

Cloud segment is expected to grow at a higher pace

- With digital transformation in the region, organizations have become dependent on the success of creative applications and extensions that IT could provide. It has become a critical competitive edge for most organizations. Moreover, IT outsourcing has become more than a simple cost-reduction technique with cloud migrations and cloud service options. Therefore, this new form is driven by organizational motivations regarding business growth, customer experience, and competitive disruption.

- The increasing demand for cloud outsourcing indicates that European companies prefer cloud platforms from public sources for data storage purposes. Also, businesses operating over the cloud will likely be concerned about security threats and will eliminate all possible threats by outsourcing IT security services. This way, the demand for expert knowledge of the vendor will be required, along with an easy delegation of responsibilities.

- According to Eurostat, the use of cloud computing among EU enterprises increased significantly in recent years. Industry sources further suggest the increasing adoption of IaaS and SaaS in the European region, which in turn would increase the demand for hybrid cloud in the market. Furthermore, several regional initiatives such as EU's Digital Decade which to expand the use fo cloud-edge technologies among European businesses to 75% by 2030 also favors the studied market's growth.

- Bring-your-own-device (BYOD) and the Internet of things (IoT) have pushed the growth of cloud adoption, as cloud-based solutions are being leveraged primarily to derive value from the data generated by IoT. This is supported by the public, private, and hybrid cloud models. In addition, the legacy IT infrastructure of enterprises may have to rely on the cloud to connect with IoT devices. Besides, organizations realize several drawbacks of public and private cloud services. They are looking for a hybrid approach that provides advantages of both architectures, minimizing the drawbacks in each model. As a result, there is an emerging trend of integrating two or more applications running on private and public systems, i.e., hybrid cloud hosting services.

- Furthermore, the growing adoption of cloud and hybrid IT infrastructure in the European is also evident from the fact that the share of enterprises employing ICT specialists has been growing across various European countries. For instance, according to Statistics Denmark, in Denmark, the share of enterprises employing ICT specialists increased to 34% in 2022, compared to 25% in 2016.

Managed Security Account for Significant Market Share

- To maintain a competitive edge, organizations across Europe, irrespective of their sizes, increasingly rely on managed service providers to ensure technology usage to transform and scale businesses. Managed security service providers are adding value to their portfolio of offerings by providing the right expertise, solutions, and pricing models. Managed security service is an emerging field in the dynamic business space of the region. Service providers are setting up managed security operations centers (SOC) to deliver security and support services. Most service providers deploy their own unified security management platform for customers to provide security information and event management) and other monitoring solutions (SIEM).

- The growing cyber security threats due to the increase in the development of technologies have led the government to invest in cyber security and MSSP. For instance, according to AAG IT Services & Cyber Security, in 2022, about 39% of enterprises in Europe reported suffering a cyberattack.

- Fully managed to host services, including server installations and setup, approved software installations according to customer requirements, security monitoring, software updates and management, data backup and protection, and a slew of other services. Many enterprises in Germany, especially startups and SMEs, are looking for such solutions. These services offer the opportunity for SMEs that need more capital to keep and maintain their servers on-site, need an appropriate IT team, or are time-constrained due to the demands of their business operations.

- The rise in data breaches in the region is expected to drive the managed security services and enable managed security vendors to develop new products to capture the market share. For instance, according to tour shark, with over 22.3 million data breaches in the third quarter of the current year, Russia led all of Central and Eastern Europe (CEE) countries. Ukraine and Montenegro came in second and third, respectively.

- To empower the thriving startup ecosystem in the country, many French majors, like Dassault Systems, are offering packaged solutions (software-as-a-service (SaaS), platform-as-a-service, PaaS, and infrastructure-as-a-service (Iaas)) that can be easily deployed with tailored offerings for startups to augment growth. The French government decided to use the services of outsourcing non-critical data to an external cloud provided by Orange Business Services after realizing the benefits of using the cloud, which is perfectly suited to capacity fluctuations (thereby empowering the government with the flexibility required to implement new services more quickly).

Europe Managed Services Industry Overview

The Europe managed services market is fragmented as the market studied is dominated by international players with a strong client base. Additionally, companies are employing powerful competitive strategies to sustain themselves in the market and retain their clients, intensifying competitive rivalry. Key players are Fujitsu Ltd, IBM Corporation, Cisco Systems, etc.

- January 2024: Business ISP and managed service provider Evolve has become the latest provider to hop onto MS3's new 10Gbps capable Fibre-to-the-Premises broadband network in the North of England, aiming to reach 535,000 UK premises by the end of 2025. An unspecified investment from Asterion is backing MS3 and has covered 158,779 premises passed (119,139 RFS) and is rising fast. Evolve's new partnership with MS3 allows them to leverage MS3's XGS-PON network to bring new solutions to businesses in the East Riding and Lincolnshire regions for the first time.

- December 2023: BT and Netskope, a player in Secure Access Service Edge (SASE), announced a partnership to bring Netskope's market-leading Security Service Edge (SSE) capabilities to BT's global customers. The partnership follows several large customer implementations where the two companies have collaborated to meet the security and access needs of large enterprises successfully. BT's data shows that hybrid working is now a requirement for 76% of global workers, driving a requirement for more agile, secure connectivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Restraints

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 Manufacturing

- 6.4.3 Healthcare

- 6.4.4 Retail

- 6.4.5 Other End-user Verticals

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Nokia Solutions and Networks

- 7.1.10 Deutsche Telekom AG

- 7.1.11 Tata Consultancy Services Limited

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Wipro Ltd

- 7.1.14 NSC Global Ltd

- 7.1.15 Telefonica Europe PLC