|

市場調査レポート

商品コード

1642066

フランスの包装:市場シェア分析、産業動向、成長予測(2025~2030年)France Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

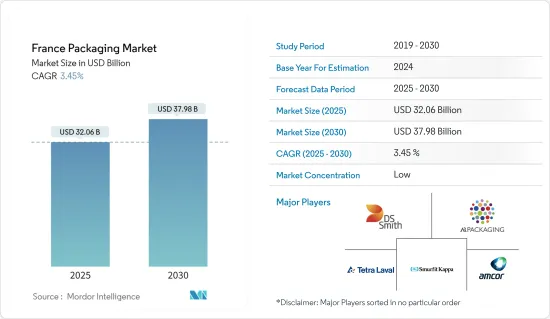

フランスの包装市場規模は2025年に320億6,000万米ドルと推定・予測され、市場推定・予測期間中(2025~2030年)のCAGRは3.45%で、2030年には379億8,000万米ドルに達すると予測されています。

フランスにおける飲食品産業向け包装需要の拡大は、利便性、レディトゥイート、高価格の食品を重視する観光客の増加に起因しています。

主要ハイライト

- 米国農務省(USDA)によると、2023年の国内総生産(GDP)は2兆8,090億米ドルと推定されています。フランスは世界第7位、EUでは第2位の経済大国です。フランスは食品材料産業が盛んで、国内で使用されるだけでなく世界中に輸出される幅広い材料を生産しています。

- さらに、フランスへの観光客の増加が、豊かな風味と独特の製法が融合したフランス料理への需要をかき立てています。同国におけるフランス料理の選択肢の絶え間ない開発と拡大は、同国の食品産業を大きく牽引しています。

- フランスの包装メーカーは、サステイナブル新製品を革新することにより、包装廃棄物の削減に焦点を当てています。環境に優しい製品に対する消費者の需要は、サステイナブル包装ソリューションへの顕著なシフトを推進しています。生分解性、堆肥化可能、リサイクル可能な材料がますます好まれるようになっています。同時に、企業はプラスチック使用量の削減を優先し、循環型経済に沿ったプラクティスを取り入れています。

- しかし、国内ではプラスチック使用に対する規制が強まっており、同国のプラスチック包装市場に影響を及ぼすと予想されます。例えば、フランス議会下院は2020年12月、再利用とリサイクルを増やすためのいくつかの取り組みに加え、2040年以降すべての使い捨てプラスチック製品と包装を禁止する法律を可決しました。

フランスの包装市場の動向

軟質包装が大きなシェアを占める

- 軟質包装は、非硬質材料を使用して製品を包装する手段であり、フランスではより経済的でカスタマイズ可能なオプションを可能にします。同国では安価で軽量な包装が人気を集めているため、メーカーは食品、化粧品、パーソナルケア、eコマースなどの用途にパウチ、バッグ、ラップなどの軟包装を使用するよう奨励されています。したがって、これらの要因が市場の成長を後押ししています。

- パウチ包装は非常に便利で持ち運びしやすいソリューションであるため、フランスでは急速に人気が高まっています。パウチ包装は、他の容器に比べて使用する材料が大幅に少なく、食品廃棄物を減らすことができるため、人気が高まっており、市場成長の原動力となっています。消費者は過去10年間でスタンドアップパウチ(スナック、飲食品、ベビーフード、工業用油脂・潤滑油用)の需要を飛躍的に伸ばしました。

- Amcor Groupなどのフランスの軟質包装メーカーは、生鮮食品の賞味期限を延ばすのに役立つ軟質紙包装ソリューションを提供しています。2023年12月、スイスを拠点とするAmcor Groupは、フランスを拠点とするチーズ製造会社Fromagerie Milleretに、同社の高級チーズ「Le Baron Brie」と「l'Ortolan Bio」用のリサイクル可能な紙製軟質包装を供給しました。AmcorのAmFiber Matrix包装により、ソフトチーズ生産者は製品内の水分レベルと熟成プロセスをコントロールすることができます。

- フランスの消費者は、包装が環境に与える影響をますます意識するようになっています。彼らは、機能性と環境配慮のバランスが取れた包装ソリューションを求めています。フランス板紙・紙・セルロース工業連合(COPACEL)によると、フランスにおける紙・板紙生産のうち、包装向けは2020年に64.3%、2023年には70%まで増加しています。

- そのため、消費者の嗜好の変化により、持続可能でリサイクル可能な軟包装材への需要が高まっています。これに応えるべく、軟包装材メーカーはこうした進化する需要に軸足を置き、環境への配慮を優先した革新的なソリューションを生み出しています。

市場を独占すると予想される食品セグメント

- フランスでは食品と外食産業が急成長しており、同国の包装市場を牽引しています。こうした変化の結果、マルチパックや、より小型で便利なシングルサーブパックなど、新しい包装スタイルがますます必要となってきています。軟包装と硬質プラスチックは、フランスの包装市場で最も人気のある材料です。

- フランスのメーカーは、この地域の紙製包装の需要増に対応するため、紙製造施設の拡大に力を入れています。2024年5月、英国の多国籍企業であるDS Smithは、フランスのラ・シュヴロリエール施設に600万ユーロ(645万米ドル)を投資すると発表しました。

- フランスの有機農業開発推進機関Agence Bioによると、レストランなどの外食施設を除くフランスの有機食品市場の年間売上高は、2019年に114億ユーロ(123億3,000万米ドル)、2023年には120億8,000万ユーロ(130億7,000万米ドル)に達しました。有機食品市場の台頭は、国全体の包装産業市場も促進します。

- フランスの消費者は、品質を感じさせるクリーンで魅力的なデザインを好みます。機能性と美的アピールを融合させた包装は注目を集めています。この動向はミニマリズムに傾き、ラベルの乱雑さを減らし、高級材料を強調することを提唱しています。

- 消費者は、食品の原産地や製造方法についてこれまで以上に関心を寄せています。ブランドはトレーサビリティを強調する包装ソリューションを採用し、シングルサーブ包装、リシーラブルバッグ、ポーションコントロール用にデザインされた製品など、成分ラベルや調達先の詳細を特徴としています。

フランスの包装産業概要

フランスの包装市場の競合情勢はセグメント化されており、DS Smith PLC、AR Packaging Group AB、Smurfit Kappa Group PLC、Tetra Pak International SAのような大手企業が参入しています。さらに、各社がさまざまな技術革新や投資を行っているため、ベンダー間の競争レベルも高くなっています。また、各社は製品ポートフォリオを強化し、市場シェアを拡大するために買収も行っています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 人口動態の変化や消費者の嗜好の変化などのマクロ経済要因

- 観光産業の増加

- 市場課題

- 国内におけるプラスチック使用規制の強化

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 材料

- プラスチック

- ガラス

- 金属

- その他

- 包装タイプ

- 軟包装

- 硬質包装

- エンドユーザー産業別

- 食品

- 飲料

- 医療と医薬品

- 美容・パーソナルケア

- その他のエンドユーザーセグメント

第6章 競合情勢

- 企業プロファイル

- AR Packaging Group AB

- DS Smith PLC

- Smurfit Kappa Group PLC

- Tetra Pak International SA

- Amcor PLC

- Ball Corporation(Rexam PLC)

- RPC Group PLC

- Owens Illinois Inc.

- Ardagh Group

- Mondi PLC

- Ametek Inc.

- Crown Holding Inc.

- Constantia Flexibles GmbH

第7章 投資分析

第8章 市場機会と今後の動向

The France Packaging Market size is estimated at USD 32.06 billion in 2025, and is expected to reach USD 37.98 billion by 2030, at a CAGR of 3.45% during the forecast period (2025-2030).

The growing demand for packaging in France for the food and beverage industry is attributable to increasing tourism with increased emphasis on convenience, ready-to-eat, and value-priced foods.

Key Highlights

- According to the United States Department of Agriculture (USDA), the gross domestic product (GDP) in 2023 is estimated at USD 2.809 trillion. France is the world's seventh-largest economy and the second-largest in the EU. France has a flourishing food ingredient industry, producing a wide range of ingredients used domestically and exported worldwide, which signifies the demand for packaging in the country.

- Additionally, the growth in the number of tourists in France has stirred the demand for French food, an amalgamation of rich flavors and unique processes. The constant development and expansion of French food options in the country significantly drive the food industry in the country.

- French packaging manufacturers focus on reducing packaging waste by innovating new sustainable products. Consumer demand for eco-friendly products propels a notable shift towards sustainable packaging solutions. Materials that are biodegradable, compostable, and recyclable are becoming increasingly favored. In tandem, companies are prioritizing reducing plastic usage and embracing practices aligned with the circular economy.

- However, increasing regulations in the country against the use of plastic are anticipated to affect the market for plastic packaging in the country. For instance, the French Parliament's lower chamber passed a law in December 2020 that banned all single-use plastic products and packaging after 2040, in addition to several initiatives to increase reuse and recycling.

France Packaging Market Trends

Flexible Packaging to Have a Significant Share

- Flexible packaging is a means of packaging products using non-rigid materials, which allows for more economical and customizable options in France. As cheap and lightweight packaging is gaining popularity in the country, manufacturers are encouraged to use flexible packaging such as pouches, bags, and wraps for food, cosmetics, personal care, and E-commerce applications. Hence, these factors are responsible for boosting the market's growth.

- Pouch packaging is rapidly gaining popularity in France, as it is a highly convenient and portable solution. The growing popularity of pouch packaging, as it significantly uses less material than other containers and reduces food waste, drives the market growth. Consumers drove the demand for stand-up pouches (for snacks, beverages, baby food, or industrial oils and lubricants) exponentially over the past decade.

- French flexible packaging manufacturers, such as Amcor Group, provide flexible paper packaging solutions that help extend the shelf life of perishable food products. In December 2023, Amcor Group, a Swiss-based brand, supplied France-based cheese producer Fromagerie Milleret with recycle-ready paper flexible packaging for the company's Le Baron Brie and l'Ortolan Bio premium cheeses. Amcor's AmFiber Matrix packaging allows soft cheese producers to control the level of moisture within the product and the ripening process.

- French consumers are increasingly aware of the environmental implications of packaging. They are on the lookout for packaging solutions that strike a balance between functionality and eco-friendliness. According to the French Union of Carboard, Paper and Cellulose Industries (COPACEL), the distribution of paper and paperboard production in France for packaging, in 2020 was 64.3% and it has increased to 70% in 2023.

- Therefore, this shift in consumer preference has led to a heightened demand for sustainable and recyclable flexible packaging materials. In response, manufacturers of flexible packaging are pivoting towards these evolving demands, crafting innovative solutions that prioritize environmental consciousness.

Food Segment Expected to Dominate the Market

- France's rapidly growing food and food service industry drives the country's packaging market. As a result of these changes, new packaging styles, such as multi-packs and more miniature and more convenient single-serve packs, are becoming increasingly necessary. Flexible packaging and rigid plastics are the most popular materials in the French packaging market.

- French manufacturers are focusing on expanding paper manufacturing facilities to cater to the region's increasing demand for paper packaging. In May 2024, DS Smith, a British multinational company, announced an investment of EUR 6 million (USD 6.45 million) in its La Chevroliere facility in France.

- According to Agence Bio, the French Agency for the Development and Promotion of Organic Agriculture, the annual turnover of the organic food market in France, excluding restaurants and other food service facilities, was EUR 11.4 billion (USD 12.33 billion) in 2019 and reached EUR 12.08 billion (USD 13.07 billion) in 2023. The rise in the organic food market also promotes the packaging industry market across the country.

- French consumers have a penchant for clean, attractive designs that exude quality. Packaging that marries functionality with aesthetic appeal captures attention. This trend leans towards minimalism, advocating for less clutter on labels and emphasizing premium materials.

- Consumers are more curious than ever about their food's origins and production methods. Brands adopt packaging solutions that underscore traceability, featuring ingredient labels and sourcing details, including single-serve packages, resealable bags, and products designed for portion control.

France Packaging Industry Overview

The competitive landscape of the French packaging market is fragmented, with major players such as DS Smith PLC, AR Packaging Group AB, Smurfit Kappa Group PLC, and Tetra Pak International SA vying for larger market share. Moreover, the competition level among these vendors is high due to the various innovations and investments made by the companies. Companies are also undergoing acquisitions to strengthen their product portfolios and increase their market shares.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Macroeconomic Factors, such as Demographic Changes and Changing Consumer Preferences

- 4.2.2 Increasing Tourism in the Industry

- 4.3 Market Challenges

- 4.3.1 Increasing Regulations in the Country against the Use of Plastic

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Plastic

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Other Materials

- 5.2 Packaging Type

- 5.2.1 Flexible Packaging

- 5.2.2 Rigid Packaging

- 5.3 End-user Verticals

- 5.3.1 Food

- 5.3.2 Beverages

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Beauty and Personal Care

- 5.3.5 Other End-user Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AR Packaging Group AB

- 6.1.2 DS Smith PLC

- 6.1.3 Smurfit Kappa Group PLC

- 6.1.4 Tetra Pak International SA

- 6.1.5 Amcor PLC

- 6.1.6 Ball Corporation (Rexam PLC )

- 6.1.7 RPC Group PLC

- 6.1.8 Owens Illinois Inc.

- 6.1.9 Ardagh Group

- 6.1.10 Mondi PLC

- 6.1.11 Ametek Inc.

- 6.1.12 Crown Holding Inc.

- 6.1.13 Constantia Flexibles GmbH