|

市場調査レポート

商品コード

1640565

塩化ナトリウム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Sodium Chloride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 塩化ナトリウム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

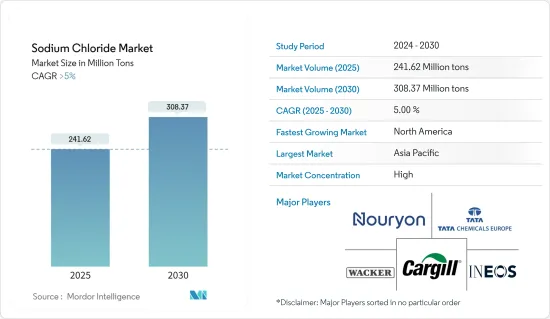

塩化ナトリウム市場規模は2025年に2億4,162万トンと推定され、予測期間(2025~2030年)のCAGRは5%を超え、2030年には3億837万トンに達すると予測されます。

2020年に発生したCOVID-19は、建設作業の一時的な停止や化学製造施設の世界の操業停止により、市場に悪影響を及ぼしました。しかし、市場は回復し、予測期間中も同様の予測をたどることが予想されます。

主要ハイライト

- 北米と欧州では、飲食品産業における塩化ナトリウムの需要増加と医薬品グレードの塩化ナトリウムの需要が市場拡大の原動力となる見込みです。

- しかし、防腐剤や解氷剤として利用できる、特性が改善された代替化学品が数多く出現していることが、市場の成長を阻害する可能性があります。

- ナトリウム系電池の使用増加と塩素アルカリ製品の生産は、将来の市場成長にさまざまな機会を提供すると予想されます。

- アジア太平洋が市場を独占し、北米は予測期間を通じて急速に発展すると予測されます。

塩化ナトリウム市場の動向

市場を独占する化学品生産セグメント

- 塩化ナトリウムは、塩素、ソーダ灰、苛性ソーダなどの有機、無機、塩素アルカリ化合物を含む多くの化学品を生産します。これらの材料は、ポリ塩化ビニル(PVC)、洗剤、ガラス、染料、石鹸など、さまざまな製品の製造に使用されます。

- 炭酸ナトリウム(ソーダ灰)は、洗剤の製造や冶金産業で利用されるほか、リン酸塩、ケイ酸塩、ガラスなどの重化学品の製造にも使用されます。安価で広く入手可能な石灰石と塩化ナトリウムは、ソルベープロセスで使用されます。アンモニアと二酸化炭素が塩と石灰石を炭酸ナトリウムに変えます。

- 2023年上半期には、EU27カ国、ノルウェー、スイス、英国で約362万8,468トンの塩素が生産されました。しかし、これは2022年上半期に比べ生産量が19.4%減少しました。2023年9月の塩素生産量は、2022年9月と比較して2%の増加が観察されました。

- 報告書によると、生産された塩素の大半はPVC、EDC/VCM用途で使用され、約31.6%を占め、次いでイソシアネートと酸素酸塩(30.8%)、無機物(12.7%)となっています。

- 米国国勢調査局によると、2023年の建設額は1兆9,787億米ドルで、2022年の1兆8,487億米ドルを7%上回りました。その結果、硬質発泡断熱パネルなどのPVC製品やポリウレタン系建設産業資材の需要が高まった。

- さらに、苛性ソーダは木材を木材パルプに変換するクラフトプロセスで使用され、製紙プロセスでは現在も主流となっています。Chlor-Alkali Industry Reviewによると、2023年9月までEU-27諸国、ノルウェー、スイス、英国で2,422.5キロトンの苛性ソーダが生産され、有機物が主要シェアを占めています。

- したがって、上記の要因から、今後数年間は化学製品セグメントが市場を独占すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、化学産業からの需要増加により、世界市場シェアを独占しています。中国は化学加工の中心地であり、世界的に生産される化学製品の大半を占めています。

- 中国国家統計局によると、同国では3,900万トンを超える水酸化ナトリウムが生産され、化学品、水処理、金属加工に使用されています。工業用に加え、水酸化ナトリウムは家庭用洗剤にもよく使われています。

- Invest Indiaが発表した統計によると、インドの主要化学品の生産量は2023~24年(2023年8月まで)には53.54トンに減少し、2022~2023年の同期間には54.32トンを超えていました。しかし、2023年8月までの有機化学品の生産量は、前年同期比で4.52%の増加を記録しました。

- 塩化ナトリウムは、製薬産業の様々な用途にも使用されています。透析液や輸液、注射液、生理食塩水点滴、経口補水塩など、原薬やその他の製品の製造に使用されます。

- India Brand Equity Foundation(IBEF)によると、インドの医薬品産業は2030年までに1,300億米ドルに達すると予想されています。同国は世界最大のワクチン生産国で、世界のワクチン総量の約60%を占めています。また、医薬品生産量では世界第3位となっています。

- 塩化ナトリウム市場に関連するさまざまなセグメントでの需要が何らかの形で増え続けていることから、同市場はアジア太平洋が独占すると予想されます。

塩化ナトリウム産業概要

塩化ナトリウム市場は主要企業で固められています。主要企業(順不同)には、Nouryon、Cargill Incorporated、Wacker Chemie AG、INEOS、Tata Chemicals Europeが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 飲食品産業からの塩化ナトリウム需要の増加

- 北米と欧州における医薬品グレードの塩化ナトリウム需要の増加

- 抑制要因

- 防腐剤と解氷剤として利用可能な代替化学品の出現

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- グレード

- 岩塩

- ソーラーソルト

- 真空塩

- 用途

- 化学品製造

- 解氷

- 水質調整

- 農業

- 食品加工

- 製薬

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ベトナム

- マレーシア

- インドネシア

- タイ

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- トルコ

- イタリア

- ノルディック

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- ナイジェリア

- アラブ首長国連邦

- エジプト

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Cargill, Incorporated.

- CK Life Sciences Int'l.(Holdings)Inc.

- Compass Minerals

- INEOS

- K+S Aktiengesellschaft

- Nouryon

- Pon Pure Chemicals Group

- Rio Tinto

- Sudwestdeutsche Salzwerke AG

- Swiss Salt Works AG

- Tata Chemicals Europe

- Wacker Chemie AG

第7章 市場機会と今後の動向

- ナトリウム系電池の使用増加

- クロールアルカリ製品の生産増加

The Sodium Chloride Market size is estimated at 241.62 million tons in 2025, and is expected to reach 308.37 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 outbreak in 2020 had a detrimental influence on the market due to the temporary halt in construction operations and the worldwide shutdown of chemical manufacturing facilities. However, the market picked up and is expected to follow a similar projection during the forecast period.

Key Highlights

- The increasing demand for sodium chloride in the food and beverage industry and the demand for pharmaceutical-grade sodium chloride in North America and Europe are expected to fuel the market expansion.

- However, the emergence of numerous alternative chemicals with improved properties that can be utilized as preservatives and deicing agents may stifle market growth.

- The increasing usage of sodium-based batteries and the production of chlor alkali products are expected to offer various opportunities for future market growth.

- Asia-Pacific dominates the market, and North America is predicted to develop quickly throughout the forecast period.

Sodium Chloride Market Trends

The Chemical Production Segment to Dominate the Market

- Sodium chloride produces many chemicals, including organic and inorganic, and chlor alkali compounds, such as chlorine, soda ash, and caustic soda. These materials are then used to make various products, including polyvinyl chloride (PVC), detergents, glass, dyes, and soaps.

- In addition to being utilized in the production of detergents and the metallurgical industry, sodium carbonate (soda ash) is employed in producing heavy chemicals, including phosphates, silicates, and glass. Limestone and sodium chloride, both of which are inexpensive and widely accessible, are used in the Solvay process. Ammonia and carbon dioxide turn salt and limestone into sodium carbonate.

- In the first half of 2023, about 3,628,468 tonnes of chlorine were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom. However, this was a 19.4% decrease in production volume compared to the first half of 2022. In September 2023, an increase of 2% was observed in chlorine production volume over September 2022.

- According to the report, most chlorine produced was used in the PVC, EDC/VCM application, accounting for approximately 31.6%, followed by isocyanates and oxygenates (30.8%) and inorganics (12.7%).

- According to the US Census Bureau, the value of construction in 2023 was USD 1,978.7 billion, 7% above the USD 1,848.7 billion spent in 2022. It, in turn, enhanced the demand for PVC products and polyurethane-based construction industry materials, such as rigid foam insulation panels.

- Furthermore, caustic soda is used in the Kraft process, which converts wood into wood pulp and is still the dominant method in paper manufacturing. According to the Chlor-Alkali Industry Review, 2,422.5 kilotons of caustic soda were produced in EU-27 countries, Norway, Switzerland, and the United Kingdom till September 2023, with organics accounting for the major share.

- Therefore, based on the factors mentioned above, the chemical products segment is expected to dominate the market in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global market share, with rising demand from the chemical industry. China is a hub for chemical processing, accounting for most chemicals produced globally.

- According to the National Bureau of Statistics of China, the country generated over 39 million metric tons of sodium hydroxide, which is used to make chemicals, water treatment, and metal processing. In addition to industrial use, sodium hydroxide is commonly found in domestic cleaning detergents.

- According to the statistics presented by Invest India, the production of major chemicals in India decreased to 53.54 lakh tonnes during 2023-24 (up to August 2023), with over 54.32 lakh tonnes produced during the corresponding period of 2022-2023. However, the production of organic chemicals up to August 2023, as compared to the corresponding period of the previous year, recorded an increase of 4.52%.

- Sodium chloride also serves its purpose in various applications in the pharmaceutical industry. It is used in manufacturing APIs and other products, such as dialysis and infusion solutions, injections, saline drips, and oral rehydration salts.

- According to the India Brand Equity Foundation (IBEF), the Indian pharmaceutical industry is expected to reach ~USD 130 billion by 2030. The country is the largest producer of vaccines worldwide, accounting for around 60% of the total vaccines globally. Additionally, the country ranks third across the globe for pharmaceutical production by volume.

- With the ever-increasing demands in the different sectors related to the sodium chloride market in one way or another, the market for the same is expected to be dominated by Asia-Pacific.

Sodium Chloride Industry Overview

The sodium chloride market is consolidated among the top players. The key players (not in a particular order) include Nouryon, Cargill Incorporated, Wacker Chemie AG, INEOS, and Tata Chemicals Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Sodium Chloride from Food and Beverage Industry

- 4.1.2 Increasing Demand for Pharmaceutical-grade Sodium Chloride in North America and Europe

- 4.2 Restraints

- 4.2.1 Emergence of Numerous Alternative Chemicals that can be Utilized as Preservatives and Deicing Agents

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Rock Salt

- 5.1.2 Solar Salt

- 5.1.3 Vacuum Salt

- 5.2 Application

- 5.2.1 Chemical Production

- 5.2.2 Deicing

- 5.2.3 Water Conditioning

- 5.2.4 Agriculture

- 5.2.5 Food Processing

- 5.2.6 Pharmaceutical

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Vietnam

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Thailand

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 Italy

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Cargill, Incorporated.

- 6.4.2 CK Life Sciences Int'l. (Holdings) Inc.

- 6.4.3 Compass Minerals

- 6.4.4 INEOS

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Nouryon

- 6.4.7 Pon Pure Chemicals Group

- 6.4.8 Rio Tinto

- 6.4.9 Sudwestdeutsche Salzwerke AG

- 6.4.10 Swiss Salt Works AG

- 6.4.11 Tata Chemicals Europe

- 6.4.12 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Sodium-based Batteries

- 7.2 Increasing Production of Chlor-alkali Products