FPSO:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

FPSO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640476

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

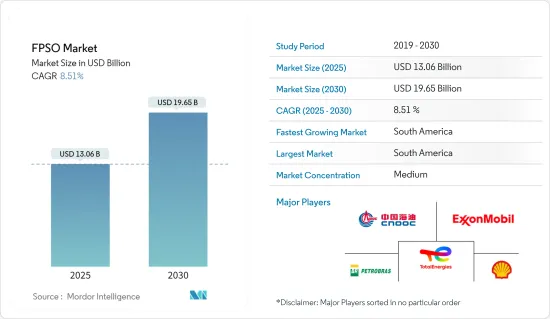

FPSOの市場規模は2025年に130億6,000万米ドルと推計され、予測期間中(2025-2030年)のCAGRは8.51%で、2030年には196億5,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、深海や超深海での探査・生産活動の増加が予測期間中のFPSO市場を牽引するとみられます。

- 一方、初期費用が高いことが予測期間中の市場成長の妨げになると予想されます。

- とはいえ、FPSOシステムの技術的進歩と革新は、FPSO市場に大きなチャンスをもたらすと期待されています。

- 南米は、オフショア活動の増加により、FPSO市場の支配的な地域になると予想されます。

FPSO市場動向

コントラクター所有のセグメントが市場を独占する見込み

- FPSOの調達方法には、主に新造、既存船の改造、既存ユニットの再配置の3つがあります。これらの選択肢のうち、FPSOの再展開は、特定分野向けに高度にカスタマイズされるため、いくつかの課題があります。その結果、オペレーターは主に新造と改造のアプローチを好んでおり、過去20年間、これらのサービスを専門知識を持つ第三者請負業者に頼ることが多かった。

- コントラクター所有のFPSOは、オペレーター所有のFPSOや固定プラットフォームよりもコスト面で有利です。FPSOの設計、建設、操業を専門とする請負業者は、規模の経済を実現し、船隊利用率を最適化することで、オペレーターのコストを削減することができます。このため、請負業者が所有するFPSOは、費用対効果の高いソリューションを求めるオペレーターにとって魅力的な選択肢となります。

- コントラクター所有のFPSOは通常リース可能で、オペレーターに油田開発の柔軟性を提供します。リースにより、オペレーターは最小限の先行資本投資でFPSOにアクセスし、配備することができるため、小規模なオペレーターや生産プロファイルが不確かなプロジェクトに有利です。

- オフショア活動の活発化に伴い、探鉱・生産活動にかかるコストは増加しており、FPSO関連業務は請負業者に委託されるようになっています。これによりオペレーターは、FPSOのオペレーションを専門業者に任せることで、最も価値を生み出せる分野に資源と注意を振り向けることができます。

- 例えば、Baker Hughes Rig Countによると、2023年末のオフショア・リグ数は約246基で、前年比約6.4%増となり、オフショアでの探鉱・生産活動が増加し、FPSOの需要が高まっています。

- 2023年5月、日本のFPSOサプライヤーであるMODECは、ブラジル沖カンポス海盆のBM-C-33ブロック向けにFPSO船を供給する契約をEquinorから獲得しました。MODECは、2027年の完成を目指すFPSOの納入に加え、FPSOの原油生産開始初年度の操業・保守サービスをEquinorに提供します。その後、EquinorはFPSOの操業責任を引き継ぐ予定です。

- 世界には、まだ発見されていない、あるいは探査段階にある未開発の海洋埋蔵物がいくつかあります。石油・ガス会社は今後、こうした未開発の石油・ガス埋蔵量の発見に注力するため、FPSOの需要は増加すると予想されます。

- FPSOに対する需要の増加と他のタイプのFPSOに対する優位性から、コントラクター所有のFPSOが予測期間中に市場を独占すると予想されます。

南米が市場を独占する見込み

- 南米は世界のFPSO市場に最も大きな影響を与えると予想されます。特に、ブラジルとガイアナがこの市場の主要企業として台頭し、近年FPSOの需要が大幅に急増しています。

- 南米は、特にブラジルとガイアナにおいて海洋石油・ガスの埋蔵量が多いです。これらの埋蔵量は深海や超深海に位置しており、効率的な生産・貯蔵・積出のためにFPSOが必要とされています。これらの地域で大規模な発見と生産が行われる可能性があるため、FPSOの需要が高まっています。

- 例えば、2024年1月、Offshore Frontier Solution Pte Ltdは、南米ウアル油田向けのエクソンモービル製浮体式生産貯蔵積出設備(FPSO)の電気システムと関連デジタルソリューションを受注しました。同船はガイアナ沖約200キロで操業します。

- また、南米には、特にブラジルのサントス盆地とカンポス盆地に広大なプレソルト層が埋蔵されています。これらの埋蔵物は厚い塩の層の下にあり、探査と生産に技術的な課題をもたらしています。FPSOは、深海で安全に操業でき、プレソルト油田の複雑な処理要件を処理できるため、こうした厳しい環境に適しています。したがって、今後、この地域で深海や超深海の石油・ガス・プロジェクトが探査・生産されるにつれて、FPSOの需要は伸びると予想されます。

- 以上のことから、予測期間中、南米がFPSO市場を独占すると予想されます。

FPSO産業の概要

FPSO市場は適度に統合されています。同市場の主なプレーヤーとしては、Petroleo Brasileiro SA(ペトロブラス)、CNOOC Ltd、TotalEnergies SE、Exxon Mobil Corp.、Shell PLCなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- FPSO稼動状況(地域別・オペレーター別):2023年

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 海洋石油・ガス探査・生産活動の増加

- エネルギー需要の増加

- 抑制要因

- 高い初期費用

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 所有別

- 事業者所有

- 業者所有

- 水深別

- 浅水

- 深水

- 超深水

- 地域別市場分析{2028年までの市場規模および需要予測(地域別のみ)}:日本

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ノルウェー

- 英国

- ロシア

- オランダ

- フランス

- イタリア

- ノルディック

- ドイツ

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- インドネシア

- マレーシア

- タイ

- 日本

- ベトナム

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- ベネズエラ

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- アルジェリア

- カタール

- 南アフリカ

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- FPSO請負業者

- Modec Inc.

- SBM Offshore NV

- BW Offshore Limited

- Teekay Offshore Partners LP

- Bluewater Holding BV

- Saipem SpA

- Petrofac Limited

- FPSOオペレーター

- Petroleo Brasileiro SA(Petrobras)

- CNOOC Ltd

- TotalEnergies SE

- ExxonMobil Corp.

- Chevron Corporation

- Shell PLC

- BP PLC

- 市場ランキング/シェア(%)分析

- FPSO請負業者

第7章 市場機会と今後の動向

- 技術の進歩と革新

目次

Product Code: 53453

The FPSO Market size is estimated at USD 13.06 billion in 2025, and is expected to reach USD 19.65 billion by 2030, at a CAGR of 8.51% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the increasing exploration and production activities in deep and ultradeep water depths are expected to drive the FPSO market during the forecast period.

- On the other hand, the high upfront cost is expected to hinder the market's growth during the forecast period.

- Nevertheless, the technological advancements and innovation in FPSO systems are expected to create huge opportunities for the FPSO market.

- South America is expected to be a dominant region for the FPSO market due to increasing offshore activities in the region.

FPSO Market Trends

The Contractor-owned Segment is Expected to Dominate the Market

- There are three primary methods for procuring FPSOs: new build, conversion of an existing vessel, and redeployment of an existing unit. Among these options, redeployment poses several challenges due to the highly customized nature of the FPSO for a specific field. As a result, operators have predominantly favored the new build and conversion approaches, often relying on third-party contractors with specialized expertise for these services over the past two decades.

- Contractor-owned FPSOs offer cost advantages over operator-owned FPSOs or fixed platforms. Contractors specializing in designing, constructing, and operating FPSOs can achieve economies of scale and optimize their fleet utilization, reducing operator costs. This makes contractor-owned FPSOs an attractive option for operators seeking cost-effective solutions.

- Contractor-owned FPSOs are typically available for lease, providing operators greater flexibility in field development. Leasing allows operators to access and deploy FPSOs with minimal upfront capital investments, benefiting smaller operators or projects with uncertain production profiles.

- With increasing offshore activities, the cost of exploration and production activities is increasing, and FPSO-related activities are being outsourced to contractors. This allows operators to allocate their resources and attention to areas where they can create the most value, leaving the FPSO operations to specialized contractors.

- For instance, according to Baker Hughes Rig Count, at the end of 2023, there were around 246 offshore rigs, which witnessed about 6.4% compared to the previous year, signifying an increase in offshore exploration and production activities, consequently driving the demand for FPSOs.

- In May 2023, MODEC, a Japanese FPSO supplier, secured a contract from Equinor to supply an FPSO vessel for the BM-C-33 block in the Campos Basin offshore Brazil. In addition to delivering the FPSO, which is expected to be completed by 2027, MODEC will provide Equinor with operations and maintenance services for the first year of the FPSO's oil production. Subsequently, Equinor plans to take over the operational responsibilities of the FPSO.

- There are several untapped offshore reserves globally that have not been discovered yet or are in the process of exploration. As oil and gas companies are focusing on discovering these untapped oil and gas reserves in the future, the demand for FPSO is expected to increase.

- With increasing demand for FPSO and its advantages over other types of FPSO, the Contractor-owned FPSO is expected to dominate the market during the forecast period.

South America is Expected to Dominate the Market

- South America is anticipated to exert the highest influence on the global FPSO market. Particularly, Brazil and Guyana have emerged as key players in this market, experiencing a significant surge in demand for FPSOs in recent years.

- South America has significant offshore oil and gas reserves, particularly in Brazil and Guyana. These reserves are located in deepwater and ultra-deepwater areas, requiring FPSOs for efficient production, storage, and offloading. The potential for large-scale discoveries and production in these regions drives the demand for FPSOs.

- For instance, in January 2024, Offshore Frontier Solution Pte Ltd awarded a contract for an electrical system and associated digital solutions on an ExxonMobil floating production storage and offloading (FPSO) vessel for the South American Uaru oil field. The unit will perform operations approximately 200 kilometers off the coast of Guyana.

- Moreover, South America has extensive pre-salt reserves, especially in Brazil's Santos and Campos Basins. These reserves are located beneath thick layers of salt, presenting technical challenges for exploration and production. FPSOs are well-suited for these challenging environments, as they can safely operate in deepwater and handle the complex processing requirements of pre-salt fields. Thus, in the future, with the upcoming deep and ultra-deep oil and gas projects' exploration and production in the region, demand for the FPSO is expected to grow.

- Therefore, as per the above points, South America is expected to dominate the FPSO market during the forecast period.

FPSO Industry Overview

The FPSO market is moderately consolidated. Some of the major players in the market are Petroleo Brasileiro SA (Petrobras), CNOOC Ltd, TotalEnergies SE, Exxon Mobil Corp., and Shell PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 FPSOs in Operation, by Region and Operator, 2023

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Offshore Oil and Gas Exploration and Production Activities

- 4.6.1.2 Increasing Demand for Energy

- 4.6.2 Restraints

- 4.6.2.1 High Upfront Costs

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ownership

- 5.1.1 Operator-owned

- 5.1.2 Contractor-owned

- 5.2 Water Depth

- 5.2.1 Shallow Water

- 5.2.2 Deep Water

- 5.2.3 Ultra-deep Water

- 5.3 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Norway

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Netherland

- 5.3.2.5 France

- 5.3.2.6 Italy

- 5.3.2.7 NORDIC

- 5.3.2.8 Germany

- 5.3.2.9 Spain

- 5.3.2.10 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Indonesia

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Japan

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Venezuela

- 5.3.4.4 Colombia

- 5.3.4.5 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Algeria

- 5.3.5.5 Qatar

- 5.3.5.6 South Africa

- 5.3.5.7 Egypt

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FPSO Contractors

- 6.3.1.1 Modec Inc.

- 6.3.1.2 SBM Offshore NV

- 6.3.1.3 BW Offshore Limited

- 6.3.1.4 Teekay Offshore Partners LP

- 6.3.1.5 Bluewater Holding BV

- 6.3.1.6 Saipem SpA

- 6.3.1.7 Petrofac Limited

- 6.3.2 FPSO Operators

- 6.3.2.1 Petroleo Brasileiro SA (Petrobras)

- 6.3.2.2 CNOOC Ltd

- 6.3.2.3 TotalEnergies SE

- 6.3.2.4 ExxonMobil Corp.

- 6.3.2.5 Chevron Corporation

- 6.3.2.6 Shell PLC

- 6.3.2.7 BP PLC

- 6.3.3 Market Ranking/Share (%) Analysis

- 6.3.1 FPSO Contractors

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Innovations

FPSO:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日