牛乳包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Milk Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640378

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

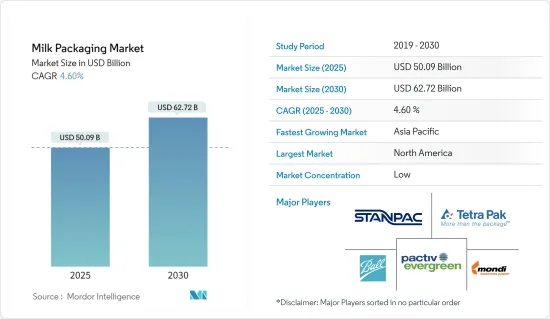

牛乳包装市場規模は2025年に500億9,000万米ドルと推定され、市場推定・予測期間中(2025~2030年)のCAGRは4.6%で、2030年には627億2,000万米ドルに達すると予測されます。

牛乳の包装は、光、空気、細菌を遮断することにより、汚染、腐敗、劣化から牛乳を保護し、保存期間を延ばすために不可欠です。適切な包装は、漏出や改ざんを防ぐことにより、牛乳が衛生的で安全に消費されることを保証します。環境への影響がますます重視される中、包装の技術革新は、廃棄物を減らすためにリサイクル可能な材料や生分解性材料を使用することに重点を置いています。

主要ハイライト

- 牛乳は世界で最も消費されている乳製品です。水分とミネラルを多く含むため、ベンダーは長期保存の課題に直面しています。この難しさが、牛乳がしばしば粉牛乳や加工品のような形で取引される主要理由です。現在、生乳の70%以上がHDPEボトルで包装されており、従来のガラス瓶包装の需要が減少しています。外出先での消費の増加、注ぎやすいという利便性、魅力的な包装の美観、大豆ベースの製品やサワー牛乳のような飲用可能な代替乳製品の人気に見られる健康意識の高まりといった要因が、総体として革新的な牛乳包装ソリューションの需要を煽っています。

- FAOによると、世界の牛乳生産量は2025年までに1億7,700万トン増加すると予測されています。また、NDDBが報告しているように、2023会計年度の生乳調達量では、インドの西部地域が1日平均3,100万kg以上でトップです。一方、南部地域は2位を確保し、1日の平均調達量は1,500万kgを超えました。ライフスタイルが進化し都市化が加速するにつれ、消費者は主要なタンパク質源として穀物よりも乳製品を好むようになっています。この変化は今後数年間、乳製品、特に牛乳の需要を高めると予測されます。その結果、これらの動向は牛乳包装市場力学を形成する態勢を整えています。

- さらに、バイオベースの包装は、標準的な牛乳パックよりも持続可能性が高く、裏地の化石ベースのポリエチレンプラスチックへのメーカーの依存を減らすことができます。環境への影響がますます重視される中、包装の革新は、廃棄物を減らすためにリサイクル可能な材料や生分解性材料を使用することに重点を置いています。例えば、2023年7月、Arla FoodsはBlue Ocean Closuresと提携し、牛乳パック用の繊維ベースのキャップを開発し、年間500トン以上のプラスチック消費量を削減しました。さらに、2023年11月には、プラスチック廃棄物をめぐる懸念に対応するため、フレッシュウェイズ社が、1リットル、500ml、1パイントのPure-Pakカートン入りのLoveMilkブランドを、新しい紐付きキャップ付きで発売しました。この取り組みは、外食産業と卸売産業で展開されています。

- しかし、プラスチックや生分解性のない包装材が与える有害な影響に対する懸念が消費者やメーカーの間で生じています。これを受け、企業は環境に優しい生分解性包装へとシフトしています。メーカーは環境に優しい包装方法を採用し、より軽い材料に焦点を当て、リサイクルを奨励しています。さらに、環境規制は生乳生産にも影響を与えると予想されます。というのも、牛乳の包装から排出される温室効果ガスは、特定の国では総排出量のかなりの部分を占めており、関連規制の変更の影響を受けやすいからです。

- 現在進行中のロシアとウクライナの紛争は、牛乳包装市場の成長に大きな影響を与えます。戦争によるインフラの損傷と輸送の障害は、原料と包装資材のサプライチェーンを混乱させています。この混乱により、供給不足とコスト高騰が懸念されます。さらに、紛争に起因するエネルギー価格の高騰とインフレは、生産と包装の経費をエスカレートさせる可能性があり、その結果、牛乳製品の価格設定と入手しやすさに影響を与えます。

牛乳包装市場の動向

板紙製牛乳包装が大きな需要を確認する

- 環境に優しい包装材料に対する世界の意識が高まるにつれ、牛乳包装産業は顕著な変化を目の当たりにしています。板紙はリサイクル可能な特性を持つため、牛乳包装で最も急成長している材料となります。板紙セグメントのこの急増は、環境意識の高まりと共鳴するその環境に優しい特徴に起因することができます。さらに、板紙包装の明確で目立つ情報は、その市場成長をさらに促進する態勢を整えています。

- 様々な政府や団体がプラスチック使用規制を強化し、企業に紙のような代替品への切り替えを促しています。例えば米国では、連邦政府のガイドラインにより、再生材を最低限含む紙製品の使用が義務付けられており、リサイクルインフラへの需要と投資を促進しています。また、欧州連合(EU)のエコラベル制度は、紙製品が厳しい環境基準を満たしていることを保証するもので、サステイナブル林業と透明性のある製品情報を奨励しています。

- さらに、技術の先進化と生産プロセスの改善により、紙製包装はメーカーにとって費用対効果が高く、効率的なものとなっています。自社製品を差別化し、環境意識の高い消費者の共感を得るために、紙包装を採用する企業が増えています。例えば、持続可能性へのコミットメントで有名なNestleは、現在複数の地域で紙ベースのカートンで牛乳を販売しています。

- さらに、世界の紙の生産事業は著しく成長しており、調査された市場を後押ししています。FAOの報告によると、米国では2023年に5,414万トンの包装・梱包用紙と板紙が生産されます。さらに、中国国家統計局のデータによると、2024年7月、中国の加工紙・段ボール生産量は約1,317万トンに達しました。紙の包装は、プラスチックのような代替品よりも環境に優しいと考えられることが多いです。持続可能性が消費者や企業にとってより重要な問題となるにつれ、牛乳用紙包装のような環境に優しい包装オプションのニーズは拡大すると考えられます。

大幅な市場成長が期待されるアジア太平洋

- アジア太平洋は、乳糖を含む製品に代わる健康的な代替品として無乳糖乳製品に対する高いポテンシャルを有しており、これが牛乳生産を補完し、市場の成長を促進する可能性が高いです。さらに、幼児の栄養に関する関心の高まりが牛乳の消費を押し上げ、市場の拡大にさらに拍車をかけると予想されます。Adani Wilmarによると、フレッシュパック乳製品の市場規模は、2025年度には1兆6,000億インドルピー(196億米ドル)にまで拡大する見込みです。新鮮包装乳製品には、牛乳、豆腐、パニール、ヨーグルトなどがあり、賞味期限は2~3日です。

- 乳製品の健康効果に対する意識の高まりと消費者の食生活の変化が、この地域における牛乳消費量の増加を促しています。また、USDAによると、2023年時点で、インド国内の牛乳消費量は2億700万トンを超えています。これは、消費量が約2億200万トンだった前年に比べ増加しました。

- さらに、都市部が拡大し、ライフスタイルのペースが速くなるにつれて、便利でレディトゥドリンク牛乳製品への嗜好が高まり、革新的な包装ソリューションへの需要を押し上げています。また、インドや中国などの新興諸国では可処分所得が増加しており、顧客の購買力が高まっています。したがって、消費者の加工食品、調理済み食品、パック詰め食品への依存度が高まる可能性が高いです。このような顧客の支出や嗜好の変化は、市場の成長に寄与すると予想されます。公式発表によると、2023年の中国における乳製品の小売販売額は4,950億6,000万人民元(694億9,000万米ドル)で、2022年の約4,738億9,000万人民元(665億2,000万米ドル)から増加しました。乳製品の小売販売額は着実な成長を維持し、2024年には約5,647億2,000万人民元(792億7,000万米ドル)に達すると推定されます。

- この地域の国々は紙の生産を大幅に拡大しており、予測期間中に調査された市場の成長をさらに促進する可能性があります。MOSPIによると、インドにおける紙と紙製品の製造による収益は、2024年までに約213億米ドルに達すると予測されています。さらに、IBEFの報告によると、インドには861の製紙工場があり、そのうち526工場が現在稼働中です。

- 環境に優しくリサイクル可能な包装が重視されるようになり、メーカーと消費者の双方がサステイナブル包装を選ぶようになっています。このように、こうした動向はアジア太平洋における牛乳包装市場の拡大を後押ししており、消費者ニーズの高まりに対応するために先進包装ソリューションへの投資が増加しています。

牛乳包装産業のセグメンテーション

牛乳包装市場は、未組織の参入企業が産業のローカルと世界参入企業の存在に直接影響を与えるため、セグメント化されています。地元の農場はeコマースを利用し、利便性と柔軟性を提供することで顧客を引き付けることができます。さらに、生乳生産の伸びは、より良い包装ソリューションを開発するために参入企業を駆り立てており、生乳包装市場を非常に競合ものにしています。市場の主要企業には、Evergreen Packaging LLC、Elopak AS、Tetra Pak International SA、Stanpac Inc.、Ball Corporationなどがあります。これらの企業は、市場の需要増に対応するため、常に製品の革新とアップグレードを行っています。

- 2024年3月ノルウェーの食品包装会社であるElopakは、リトルロック港湾局で米国初の生産施設の建設を開始しました。7,000万米ドルを投資し、牛乳、ジュース、植物性食品、液卵など様々な製品のカートンを製造します。生産設備の設置は2024年第4四半期を予定しており、2025年第1四半期までにフル稼働を目指します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 消費者の健康志向の高まり

- フレーバー牛乳消費の増加

- 市場抑制要因

- 酪農活動による温室効果ガス排出が法的問題に発展

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- ミクロ経済要因が市場に与える影響の評価

第5章 市場セグメンテーション

- 包装タイプ別

- 缶

- ボトル/容器

- カートン

- パウチ/袋

- その他

- 材料別

- プラスチック

- 板紙

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Stanpac Inc.

- Mondi PLC

- Tetra Pak International SA

- Ball Corporation

- Pactiv Evergreen Inc.

- Indevco Group

- CKS Packaging Inc.

- Elopak AS

- Consolidated Container Company LLC(Loews Corporation)

- SIG Combibloc Group Ltd

第7章 投資分析

第8章 市場の将来

目次

The Milk Packaging Market size is estimated at USD 50.09 billion in 2025, and is expected to reach USD 62.72 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Milk packaging is essential to protect milk from contamination, spoilage, and degradation by blocking out light, air, and bacteria, thereby extending its shelf life. Proper packaging ensures that milk remains hygienic and safe for consumption by preventing leaks and tampering. With increasing emphasis on environmental impact, packaging innovations focus on using recyclable or biodegradable materials to reduce waste.

Key Highlights

- Milk stands as the world's most consumed dairy product. Due to its high moisture and mineral content, vendors face challenges in long-term storage. This difficulty is a primary reason why milk is often traded in forms like milk powder or processed variants. Over 70% of fresh milk is currently packaged in HDPE bottles, diminishing the demand for traditional glass bottle packaging. Factors such as the rise of on-the-go consumption, the convenience of easy pouring, appealing packaging aesthetics, and heightened health awareness evident in the popularity of drinkable dairy alternatives such as soy-based products and sour milk have collectively fueled the demand for innovative milk packaging solutions.

- According to FAO, global milk production is projected to grow by 177 million metric tons by 2025. Also, as reported by NDDB, the western region of India topped the charts in milk procurement for the financial year 2023, averaging over 31 million kg daily. Meanwhile, the southern region secured the second spot, with an average daily procurement exceeding 15 million kg. As lifestyles evolve and urbanization accelerates, consumers are increasingly favoring dairy products over cereals as their primary protein source. This shift is projected to bolster the demand for dairy products, particularly milk, in the coming years. Consequently, these trends are poised to shape the dynamics of the milk packaging market.

- Furthermore, bio-based packages are more sustainable than standard milk cartons, reducing the manufacturer's reliance on fossil-based polyethylene plastic in the lining. With increasing emphasis on environmental impact, packaging innovations focus on using recyclable or biodegradable materials to reduce waste. For instance, in July 2023, Arla Foods partnered with Blue Ocean Closures to develop a fiber-based cap for its milk cartons to cut its plastic consumption by over 500 tonnes yearly. Further, in November 2023, addressing concerns surrounding plastic waste, Freshways launched its LoveMilk brand in 1 liter, 500 ml, and 1-pint Pure-Pak cartons with a new tethered cap. This initiative is being rolled out in the foodservice and wholesale industries.

- However, concerns over the harmful impacts of plastics and non-biodegradable packaging materials have arisen among consumers and manufacturers. In response, companies are shifting toward environmentally friendly biodegradable packaging. Manufacturers are adopting green packaging methods, focusing on lighter materials and encouraging recycling. Furthermore, environmental regulations are anticipated to affect milk production. This is because greenhouse gas emissions from milk packaging account for a notable portion of total emissions in certain countries, making them susceptible to changes in related regulations.

- The ongoing conflict between Russia and Ukraine significantly impacts the growth of the milk packaging market. Damaged infrastructure and transportation hurdles due to the war disrupt the supply chains for both raw and packaging materials. This disruption raises the specter of shortages and inflated costs. Furthermore, the conflict-induced surge in energy prices and inflation could escalate production and packaging expenses, subsequently affecting the pricing and accessibility of milk products.

Milk Packaging Market Trends

Paperboard Milk Packaging to Witness Significant Demand

- As global awareness of eco-friendly packaging materials rises, the milk packaging industry is witnessing a notable shift. Due to its recyclable properties, the paperboard segment is set to emerge as the fastest-growing material in milk packaging. This surge in the paperboard segment can be attributed to its eco-friendly features, which resonate with growing environmental consciousness. Additionally, the clear and prominent information on paperboard packaging is poised to drive its market growth further.

- Various governments and organizations are introducing stricter plastic-use regulations, encouraging companies to switch to alternatives like paper. For instance, in the United States, federal guidelines mandate paper products with minimum recycled content, driving demand and investment in recycling infrastructure. Also, the European Union's Ecolabel scheme ensures paper products meet stringent environmental standards, encouraging sustainable forestry and transparent product information.

- In addition, technological advancements and refined production processes have rendered paper packaging cost-effective and efficient for manufacturers. Firms are increasingly adopting paper packaging to distinguish their products and resonate with eco-conscious consumers. For instance, Nestle, renowned for its commitment to sustainability, now markets milk in paper-based cartons across multiple regions.

- Moreover, the worldwide paper production business is growing significantly, boosting the market studied. As reported by FAO, the United States produced 54.14 million metric tons of wrapping and packaging paper and paperboard in 2023. Furthermore, data from the National Bureau of Statistics of China indicates that in July 2024, China's processed paper and cardboard production reached around 13.17 million metric tons. Paper packaging is often considered more environmentally friendly than alternatives like plastics. The need for eco-friendly packaging options like milk paper packaging will expand as sustainability becomes a more significant issue for consumers and companies.

Asia-Pacific Expected to Witness Significant Market Growth

- Asia-Pacific has a high potential for lactose-free dairy products as healthy alternatives to lactose-containing products, which will likely complement milk production, propelling the market's growth. Additionally, heightened concerns regarding child nutrition are anticipated to boost milk consumption, further fueling the market's expansion. According to Adani Wilmar, the market size of freshly packaged dairy food is likely to increase to INR 1.6 trillion (USD 19.6 billion) in the financial year 2025. Freshly packaged dairy includes milk, curd, paneer, and yogurt, which have a shelf life of two to three days.

- Rising awareness about the health benefits of dairy products and changing dietary habits among consumers are driving higher milk consumption in the region. Also, as per USDA, as of 2023, the total domestic consumption volume of milk was over 207 million metric tons in India. This was an increase compared to the previous year, when the consumption volume was about 202 million metric tons.

- Furthermore, as urban areas expand and lifestyles become more fast-paced, there is a growing preference for convenient and ready-to-drink milk products, boosting the demand for innovative packaging solutions. Also, higher disposable incomes in developing countries such as India and China increase the purchasing power of customers. Hence, consumer dependence on processed, pre-cooked, and packed foods will likely increase. Such changes in customer spending and preferences are expected to contribute to market growth. According to an official source, in 2023, the retail sales value of dairy products in China totaled CNY 495.06 billion (USD 69.49 billion), increasing from around CNY 473.89 billion (USD 66.52 billion) in 2022. The retail sales value of dairy products was estimated to maintain steady growth and reach approximately CNY 564.72 billion (USD 79.27 billion) by 2024.

- Countries across the region are significantly expanding their paper production, which may further drive the growth of the market studied during the forecast period. According to MOSPI, the revenue from the manufacture of paper and paper products in India is projected to amount to approximately USD 21.3 billion by 2024. Furthermore, as reported by IBEF, India boasts 861 paper mills, of which 526 are currently operational, underscoring the country's substantial capabilities in paper and paperboard production.

- There is a rising emphasis on eco-friendly and recyclable packaging, influencing both manufacturers and consumers toward sustainable packaging options. Thus, these trends are driving the expansion of the milk packaging market in Asia-Pacific, with increasing investments in advanced packaging solutions to meet growing consumer needs.

Milk Packaging Industry Segmentation

The milk packaging market is fragmented as unorganized players directly impact the existence of local and global players in the industry. Local farms use e-commerce and can attract customers by providing convenience and flexibility. Moreover, the growth in milk production is driving the players to develop better packaging solutions, making the milk packaging market highly competitive. Some of the key players in the market are Evergreen Packaging LLC, Elopak AS, Tetra Pak International SA, Stanpac Inc., and Ball Corporation. These players constantly innovate and upgrade their product offerings to cater to the increasing market demand.

- March 2024: Elopak, a Norwegian food packaging company, commenced construction on its inaugural US production facility at the Little Rock Port Authority. With an investment of USD 70 million, the plant is set to manufacture cartons for various products, including milk, juices, plant-based items, and liquid eggs. Installation of production equipment is slated for the fourth quarter of 2024, with the facility aiming for full operational status by the first quarter of 2025.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Health Concerns Among Consumers

- 4.2.2 Increasing Consumption of Flavored Milk

- 4.3 Market Restraints

- 4.3.1 Greenhouse Gas Emissions due to Dairy Activities Leading to Legislative Issues

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET SEGMENTATION

- 5.1 By Packaging Type

- 5.1.1 Cans

- 5.1.2 Bottles/Containers

- 5.1.3 Cartons

- 5.1.4 Pouches/Bags

- 5.1.5 Other Packaging Types

- 5.2 By Material

- 5.2.1 Plastic

- 5.2.2 Paperboard

- 5.2.3 Other Materials

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Stanpac Inc.

- 6.1.2 Mondi PLC

- 6.1.3 Tetra Pak International SA

- 6.1.4 Ball Corporation

- 6.1.5 Pactiv Evergreen Inc.

- 6.1.6 Indevco Group

- 6.1.7 CKS Packaging Inc.

- 6.1.8 Elopak AS

- 6.1.9 Consolidated Container Company LLC ( Loews Corporation)

- 6.1.10 SIG Combibloc Group Ltd

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日