ミルク包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Milk Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740890

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

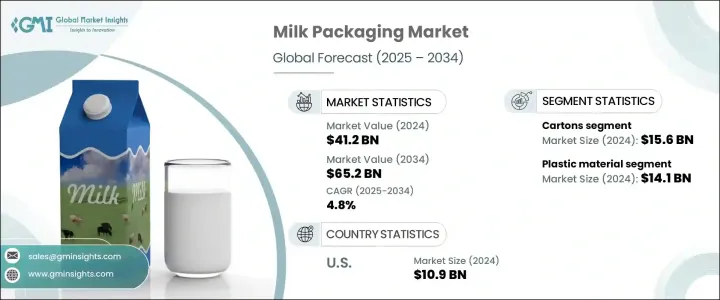

世界のミルク包装市場は、2024年には412億米ドルとなり、CAGR 4.8%で成長し、2034年には652億米ドルに達すると推定されます。

同市場は、乳製品消費の増加、組織小売業の急成長、eコマースの爆発的拡大により、力強い勢いを見せています。消費者が新鮮で包装された乳製品のオンラインショッピングをますます選ぶようになるにつれ、包装は耐久性、漏れにくさ、輸送のしやすさといった新たな基準を満たすように進化しています。製品の安全性を確保すると同時に、ブランドの認知度を高め、消費者の関心を高めるパッケージへのニーズは、今やかつてないほど高まっています。利便性、持続可能性、透明性を中心に嗜好が変化する消費者主導の環境において、包装は購買決定を形成する上で重要な役割を果たしています。企業は、物理的な棚でもデジタル店頭でも目立つことができる革新的な包装形態に投資しています。

持続可能で軽量、リサイクルしやすい素材への需要の高まりは、競合情勢を再構築しており、パッケージはもはやコスト要因としてではなく、戦略的なブランド資産と見なされています。食品の安全性、トレーサビリティ、原材料の原産地に対する意識の高まりは、包装の役割をさらに高めています。このシフトはまた、QRコードやスマートラベルなどの機能を提供し、消費者がより良い情報に基づいた選択ができるようにするスマートパッケージング技術の機会を生み出しています。小売業者やeコマース・プラットフォームが、視覚的に魅力的で、機能的で、環境に配慮した包装を求めているため、テトラパックや環境に優しいカートンのような形態が、オンラインとオフラインの両方のチャネルで広く支持されるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 412億米ドル |

| 予測金額 | 652億米ドル |

| CAGR | 4.8% |

ミルク包装市場は、包装タイプ別にボトル、カートン、パウチ、缶、その他に区分されます。カートン分野は依然として最大で、2024年の市場規模は156億米ドルです。その成長の原動力となっているのは、再生可能な板紙などの持続可能な素材を利用しながら賞味期限を延ばす無菌包装ソリューションに対する消費者の需要の高まりです。カートンはスペース効率も高く、輸送コストと排出量を削減し、従来のプラスチック製に代わる環境に優しい選択肢となっています。特に、光と酸素のバリア性が重要な、無乳糖牛乳や強化牛乳のようなプレミアムで付加価値の高い乳製品に好まれています。

市場は素材別に、プラスチック、ガラス、金属、板紙、その他に区分されます。素材別ではプラスチックが優勢で、2024年の市場規模は141億米ドルです。HDPEやPETのような素材は、その軽量構造、耐衝撃性、長距離物流やeコマース流通における優れた扱いやすさから、依然としてトップの選択肢となっています。リシーラブルキャップや人間工学に基づいたデザインなどの特徴は、ユーザーの利便性を高め、腐敗を最小限に抑えます。リサイクルへの注目が高まる中、メーカーは再生プラスチック(rPET)の使用を推進し、機能性を維持しながら環境問題に取り組んでいます。

ドイツミルク包装2024年の市場規模は23億米ドルであり、これは強力な規制基準とリサイクル可能で生分解性のある包装に対する消費者の嗜好の高まりを反映しています。オーガニック乳製品の消費動向は、プレミアムで持続可能なパッケージング・ソリューションの需要をさらに高める。スマートラベルや強化されたバリア素材などの技術革新は、賞味期限やトレーサビリティに具体的な影響を及ぼしています。

世界市場の主要企業には、Tetra Pak、SIG、Smurfit Kappa、WestRock、Sonoco Products、Elopak、Ecolean、Berry Global、CDF Corporation、Alfipaなどがあります。競争力を維持するため、これらの企業は持続可能なパッケージング革新に多額の投資を行っており、生分解性複合材、リサイクル可能な板紙、eコマース物流に合わせたソリューションなどを開発しています。研究開発の焦点は、賞味期限の延長、環境フットプリントの削減、有機乳製品や高級乳製品といったニッチ市場向けのカスタマイズ包装の提供であり、最終的にはブランド・ロイヤルティの強化にあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 乳製品の消費量の増加

- 組織化された小売業とeコマースの拡大

- 植物由来の代替ミルクの人気が高まっている

- 便利で使いやすいパッケージの需要

- 包装技術の進歩

- 業界の潜在的リスク&課題

- 環境問題と規制圧力

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:包装形態別、2021 –2034

- 主要動向

- ボトル

- カートン

- ポーチ

- 缶

- その他

第6章 市場推計・予測:材料別、2021 –2034

- 主要動向

- ガラス

- プラスチック

- 金属

- 板紙

- その他

第7章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第8章 企業プロファイル

- Alfipa

- Berry Global

- CDF Corporation

- CKS Packaging

- Ecolean

- Elopak

- Global Polybags Industries

- IPI

- Jagannath Polymers

- Nippon Paper Industries

- Parksons Packaging

- SIG

- Smurfit Kappa

- Sonoco Products

- Stanpac

- Stora Enso

- Tetra Pak

- WestRock

目次

The Global Milk Packaging Market was valued at USD 41.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 65.2 billion by 2034. The market is witnessing strong momentum driven by rising dairy product consumption, rapid growth in organized retail, and the explosive expansion of e-commerce. As consumers increasingly opt for online shopping for fresh and packaged dairy goods, packaging is evolving to meet new standards of durability, leak resistance, and ease of transport. The need for packaging that ensures product safety while enhancing brand visibility and consumer engagement is now at an all-time high. In a consumer-driven environment where preferences revolve around convenience, sustainability, and transparency, packaging plays a critical role in shaping purchasing decisions. Companies are investing in innovative packaging formats that can stand out on physical shelves and in digital storefronts alike.

The growing demand for sustainable, lightweight, and easily recyclable materials is reshaping the competitive landscape, with packaging no longer seen as a cost factor but as a strategic brand asset. Increasing awareness around food safety, traceability, and the origin of ingredients further elevates the role of packaging. This shift has also created opportunities for smart packaging technologies, offering features such as QR codes and smart labels that empower consumers to make better-informed choices. As retailers and e-commerce platforms seek packaging that is visually appealing, functional, and environmentally responsible, formats like tetra packs and eco-friendly cartons are gaining widespread traction across both online and offline channels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41.2 Billion |

| Forecast Value | $65.2 Billion |

| CAGR | 4.8% |

The milk packaging market is segmented by packaging type into bottles, cartons, pouches, cans, and others. The cartons segment remains the largest, valued at USD 15.6 billion in 2024. Its growth is fueled by rising consumer demand for aseptic packaging solutions that extend shelf life while utilizing sustainable materials such as renewable paperboard. Cartons are also space-efficient, cutting down on transportation costs and emissions, making them a greener alternative to traditional plastic options. They are especially preferred for premium and value-added milk products like lactose-free and fortified milk, where strong light and oxygen barrier properties are critical.

Based on material, the market is segmented into plastic, glass, metal, paperboard, and others. Plastic dominates the material segment, with a market value of USD 14.1 billion in 2024. Materials like HDPE and PET remain top choices for their lightweight structure, impact resistance, and superior ease of handling across long-distance logistics and e-commerce distribution. Features such as resealable caps and ergonomic designs enhance user convenience and minimize spoilage. A growing focus on recycling is pushing manufacturers toward using recycled plastics (rPET), addressing environmental concerns while maintaining functionality.

Germany Milk Packaging Market was valued at USD 2.3 billion in 2024, reflecting strong regulatory standards and heightened consumer preference for recyclable and biodegradable packaging. The growing trend of organic dairy consumption further drives demand for premium, sustainable packaging solutions. Technological innovations such as smart labels and enhanced barrier materials are making a tangible impact on shelf life and traceability.

Key players in the global market include Tetra Pak, SIG, Smurfit Kappa, WestRock, Sonoco Products, Elopak, Ecolean, Berry Global, CDF Corporation, and Alfipa. To stay competitive, these companies are heavily investing in sustainable packaging innovations, developing biodegradable composites, recyclable paperboards, and solutions tailored for e-commerce logistics. Research and development efforts are focused on extending shelf life, reducing environmental footprint, and offering customized packaging for niche markets such as organic and premium dairy segments, ultimately strengthening brand loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Selling Price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing consumption of dairy products

- 3.3.1.2 Expansion of organized retail and e-commerce

- 3.3.1.3 Rising popularity of plant-based milk alternatives

- 3.3.1.4 Demand for convenient and user-friendly packaging

- 3.3.1.5 Advancements in packaging technology

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Environmental concerns and regulatory pressures

- 3.3.2.2 Fluctuating raw material prices

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Bottles

- 5.3 Cartons

- 5.4 Pouches

- 5.5 Cans

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Glass

- 6.3 Plastic

- 6.4 Metal

- 6.5 Paperboard

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 ANZ

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 Middle East and Africa

- 7.6.1 UAE

- 7.6.2 Saudi Arabia

- 7.6.3 South Africa

Chapter 8 Company Profiles

- 8.1 Alfipa

- 8.2 Berry Global

- 8.3 CDF Corporation

- 8.4 CKS Packaging

- 8.5 Ecolean

- 8.6 Elopak

- 8.7 Global Polybags Industries

- 8.8 IPI

- 8.9 Jagannath Polymers

- 8.10 Nippon Paper Industries

- 8.11 Parksons Packaging

- 8.12 SIG

- 8.13 Smurfit Kappa

- 8.14 Sonoco Products

- 8.15 Stanpac

- 8.16 Stora Enso

- 8.17 Tetra Pak

- 8.18 WestRock

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日