|

市場調査レポート

商品コード

1640375

中国のファクトリーオートメーションと産業制御:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のファクトリーオートメーションと産業制御:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

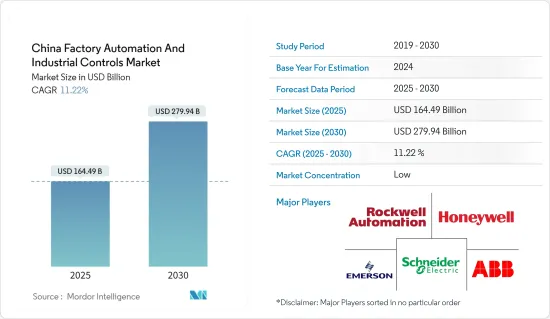

中国のファクトリーオートメーションと産業制御市場規模は2025年に1,644億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.22%で、2030年には2,799億4,000万米ドルに達すると予測されます。

主要ハイライト

- さまざまな製造装置における技術の進歩と革新の進化が、自動化技術の採用を後押ししています。

- 中国のデジタル化とインダストリー4.0イニシアチブは、生産プロセスを改善するためにロボット工学や制御システムなど、より革新的で自動化されたソリューションを必要とすることによって、産業間の自動化の成長を大幅に刺激しています。中国経済は、その製造能力と政府による工場、インフラ、機械への投資によって目覚ましい成長を遂げました。

- 中国は産業用ロボット市場をリードし、この地域の工場自動化への道を推進してきました。また、同国はアジア太平洋でも世界有数の製造国です。同国における産業用ロボットの出荷台数の増加と、同国全体における様々な産業用制御システムソフトウェアの採用が、大規模な工場の自動化を促進しています。

- 中国におけるオートメーションは、インテリジェントマニュファクチャリングの導入により拡大知能が期待されています。工業情報化省によると、中国では過去数年間に100を超える知的生産のパイロットプロジェクトが開始されています。また、2022年6月には深セン市が「知的ロボット産業クラスター育成・開発行動計画」を発表しました。2023年6月、北京市政府は「北京ロボット産業革新開発行動計画(2023~2025年)」を発表しました。

- 政府のインセンティブと目標は、中国市場がファクトリーオートメーションに飛び込む可能性を前進させました。メイド・イン・チャイナ2025計画は、国内参入企業が海外参入企業への依存度を下げることを奨励しています。中国における人件費の急激な高騰と製造業の労働力供給の減少も、産業用ロボットとファクトリーオートメーションの普及を後押ししています。

- 買収計画における政府の強力な支援も、インダストリー4.0への移行を後押ししています。例えば、中国を拠点とする産業用ロボットメーカーのSiasunは、中国科学院と提携しており、同院はさらに政府と連携しています。

- 中国での生産コストが上昇し、人民元が対ドルで上昇したことで、投資家たちはによる生産地に目を向けています。しかし、製造業者は高品質生産と環境に優しい製造規制に焦点を当てる必要があります。技術の発展に伴い、完全自動化された施設は調整と進化に何年もかかります。一方、積極的な自動化適応に関する取り組みが不利または遅れているため、地域ベースでの成長は限られています。

中国のファクトリーオートメーションと産業制御市場の動向

分散型制御システムセグメントが大きな市場シェアを占める見込み

- DCSは、相互接続されたセンサ、コントローラ、ターミナル、アクチュエータに依存するプロセス指向のプラットフォームであり、施設の生産オペレーションの集中マスターコントローラとして機能します。そのため、DCSはプロセスの制御とモニタリングに重点を置き、設備オペレータが1つの場所からすべての設備オペレーションを確認できるようにします。

- DCSシステムの大きな利点のひとつは、分散したコントローラ、ワークステーション、その他のコンピューティング要素間のデジタル通信がピアツーピアアクセスの原則に従っていることです。石油化学、原子力、石油・ガス産業などのプロセス産業において、より高い精度と制御を実現するために、特定されたセットポイントを中心に、指定されたプロセス公差を提供するコントローラへの需要が高まっている

- さらに、多くの要件がDCSの採用を後押ししています。これらのシステムは、操作の複雑さ、プロジェクトのリスクを低減し、要求の厳しい用途で俊敏な製造のための柔軟性などの機能性を提供するからです。PLC、ターボ機械制御、安全システム、サードパーティ制御、熱交換器、給水加熱器、水質などの各種プラントプロセス制御を統合するDCSの能力は、エネルギーセグメントでのDCS採用をさらに後押ししています。

- 中国における発電量の開発は、分散型制御システム(DCS)の需要を伸ばしています。CECが発表した2023年の国民生用電子機器力産業統計によると、2023年の中国の総設備発電容量は2919.6ギガワットでした。

- 2022年1月、中国はエネルギー消費を制御するための二重制御システムの使用を発表しました。今後、エネルギー消費量と原単位は、二酸化炭素排出量と電力の「二重制御システム」へと変化していく。こうした取り組みにより、2024~2029年にかけて、主要製造施設におけるDCSシステムの採用が加速すると考えられます。

石油・ガスセクターは大幅な成長が見込まれる

- 石油・ガスプラットフォームは地理的に分散しているため、適切な通信システムが必要です。PLC、SCADA、DCS、セーフティオートメーションなどのソリューションの開発は、中国における産業の巨大な発展に起因しています。また、DCSシステムを含むオートメーション製品に対する大規模な需要も見込まれています。

- 2023年3月、Aramcoは深センに上場している栄盛石油化学の株式10%を246億人民元(36億米ドル)で取得する最終合意に調印しました。この戦略的合意に基づき、栄盛の子会社である浙江石油化工との継続的な長期販売契約の一環として、Aramcoは同社に毎日48万バレルのアラビア原油を供給することになります。

- さらに、石油・ガス産業は、安全性、プラントの信頼性、効率性に関するいくつかの政府規制の対象となっています。ICSは、リモート・ターミナル・ユニット(RTU)やポンプ・圧縮ステーションに応用され、安全性を確保しています。

- 生産効率を損なうことなく安全性と環境保全性を維持するため、産業ではICSソリューションの採用が増加しています。オートメーションは、手頃な価格のエネルギーと厳しい政府規制の要件を満たすために、情報と制御、電力、安全ソリューションを統合するのに役立ちます。

- さらに、石油・ガス産業におけるオートメーションへの高い需要により、SeeqはCygNetエンタープライズモニタリング制御・データ収集(SCADA)ウェルサイト情報転送マークアップ言語(WITSML)データストレージシステムに新しいコネクタを導入することで、石油・ガス産業へのサポートを拡大しました。これにより、現在の厳しい産業環境において、先進的分析とデータによる迅速な意思決定が可能になります。

- ここ数年、石油・ガス企業は、インシデント・レスポンスソリューションや、ICS環境のログ収集が可能なソフトウェアなど、サイバーセキュリティ技術に多額の投資を行っており、ネットワークの可視化とセグメント化を強化し、横の動きを防止し、差し迫った脅威を排除しています。

- 産業では、生産効率を損なうことなく安全性と環境保全性を維持するために、ICSソリューションの採用が進んでいます。オートメーションは、手頃なエネルギーと厳しい政府規制の要件を満たすために、情報と制御、電力、安全ソリューションを統合するのに役立ちます。

中国のファクトリーオートメーションと産業制御産業概要

中国のファクトリーオートメーションと産業制御市場は非常にセグメント化されており、著名な企業が複数存在しています。各社は市場シェアを獲得するため、戦略的パートナーシップや製品開拓に継続的に投資しています。最近の市場開拓の動向をいくつか発表します。

- 2024年3月-Rockwell Automationは、次世代産業用アーキテクチャを加速するためにNvidiaと協業すると発表しました。オートメーションの顧客が産業プロセスをデジタル化しやすくするため、Rockwellは未来の工場を構築することで産業を進化させる計画です。

- 2024年2月-ABBは、自動車、消費財、教育、医療、小売、新エネルギーなどの新興セグメントで、このAIとロボティクスの統合を活用する計画を発表。この戦略的な動きは、中国全土のロボット用途に新たなレベルの自律性を導入することで、顧客にさらなる価値を生み出すことを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 労働人口の減少による自動化技術の台頭

- 市場課題

- 産業の規制と施策

第6章 市場セグメンテーション

- タイプ別

- 産業用制御システム

- 分散型制御システム(DCS)

- PLC(プログラマブル・ロジック・コントローラ)

- SCADA(モニタリング制御・データ収集)

- 製品ライフサイクル管理(PLM)

- ヒューマンマシンインターフェース(HMI)

- 製造実行システム(MES)

- 統合基幹業務システム(ERP)

- その他の産業用制御システム

- フィールド機器

- センサとトランスミッター

- 電気モーターとドライブ

- 産業用ロボット

- マシンビジョンシステム

- その他のフィールドデバイス

- 産業用制御システム

- エンドユーザー産業別

- 石油・ガス

- 化学・石油化学

- 電力・公益事業

- 自動車・運輸

- 医薬品

- 飲食品

- その他

第7章 競合情勢

- 企業プロファイル

- General Electric Company

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Company

- ABB Ltd

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

第8章 投資分析

第9章 市場の将来

The China Factory Automation And Industrial Controls Market size is estimated at USD 164.49 billion in 2025, and is expected to reach USD 279.94 billion by 2030, at a CAGR of 11.22% during the forecast period (2025-2030).

Key Highlights

- The evolution of technological advancements and innovations across various manufacturing units has encouraged the adoption of automation technologies.

- Digitization and Industry 4.0 initiatives in China have significantly stimulated the growth of automation among industries by necessitating more innovative and automated solutions, such as robotics and control systems, to improve production processes. China's economy witnessed impressive growth due to its manufacturing capabilities and the government's investments in factories, infrastructure, and machinery.

- China has led the industrial robot market, driving its way to factory automation in the region. The country is also one of the leading manufacturing countries globally in Asia-Pacific. The increase in the shipment of industrial robots in the country and the adoption of various industrial control system software across the country facilitates factory automation at scale.

- Automation in China is expected to be augmented by the uptake of intelligent manufacturing. According to the Ministry of Industry and Information Technology, the country has initiated over 100 pilot projects for intellectual manufacturing in the past few years. Also, in June 2022, Shenzhen announced the Action Plan for Cultivating and Developing Intelligent Robot Industry Clusters. In June 2023, the Beijing Municipal government announced the Beijing Robot Industry Innovation and Development Action Plan (2023-2025).

- Government incentives and targets have advanced the potential of the Chinese market to dive into factory automation. Made in China 2025 plan encourages domestic players to decrease their dependency on foreign players. The rapidly soaring labor costs and declining manufacturing labor force supply in China are also helping in the penetration of industrial robots and factory automation.

- The government's strong support in the acquisition program has helped the country move towards Industry 4.0. For instance, Siasun, a China-based industrial robot maker, is affiliated with the Chinese Academy of Sciences, which is further linked to the government.

- With the rising cost of production in China and the strengthening of the Yuan against the Dollar, investors have been looking at alternate manufacturing destinations. However, manufacturers need to focus on quality production and environment-friendly manufacturing regulations. With the growing technology, a fully automated facility takes years to adjust and evolve. Meanwhile, unfavorable or delayed initiatives on active automation adaptation have limited growth on a regional basis.

China Factory Automation And Industrial Controls Market Trends

The Distributed Control System Segment is Expected to Hold a Significant Market Share

- DCS are process-oriented platforms that depend on interconnected sensors, controllers, terminals, and actuators to act as a centralized master controller for a facility's production operations. Thus, a DCS focuses on controlling and monitoring processes and allowing facility operators to see all facility operations from one place.

- One of the significant benefits of the DCS system is that the digital communication between distributed controllers, workstations, and other computing elements follows the peer-to-peer access principle. To achieve greater precision and control in process industries, like the petrochemical, nuclear, and oil and gas industries, there is an increasing demand for controllers that offer specified process tolerance around an identified set point.

- Moreover, many requirements have driven the adoption of DCS, as these systems provide lower operational complexity, project risk, and functionalities like flexibility for agile manufacturing in highly demanding applications. The ability of DCS to integrate PLCs, turbomachinery controls, safety systems, third-party controls, and various other plant process controls for heat exchangers, feedwater heaters, and water quality further drives the adoption of DCS in the energy sector.

- The growth in electric power generation in China is developing demand for distributed control systems (DCS). According to the national power industry statistics for the 2023 report published by CEC, the total installed electricity generation capacity in China in 2023 was 2919.6 gigawatts.

- In January 2022, China announced the use of dual control systems to control energy consumption. In the future, energy consumption and intensity will be transformed into a "dual control system" for carbon emissions and power. These initiatives will accelerate the adoption of the DCS system in the major manufacturing facilities between 2024 and 2029.

The Oil and Gas Sector is Expected to Register a Significant Growth

- The geographically dispersed oil and gas platforms require proper communication systems. Growth in solutions like PLC, SCADA, DCS, and safety automation is attributed to the enormous development of industries in China. It is also expected to create a massive demand for automation products that include DCS systems.

- In March 2023, Aramco signed definitive agreements to acquire a 10% shareholding in Shenzhen-listed Rongsheng Petrochemical Co. Ltd for CNY 24.6 billion (USD 3.6 billion); this would significantly expand its downstream presence in China. Under the strategic agreement, as part of an ongoing long-term sales arrangement with Rongsheng's subsidiary Zhejiang Petroleum and Chemical Co. Ltd, Aramco would supply this company with 480,000 barrels of Arabian crude oil daily.

- Moreover, the oil and gas industry is subject to several government regulations for safety, plant reliability, and efficiency. ICS finds applications in remote terminal units (RTU) and pumping and compression stations to ensure safety.

- The industry increasingly adopts ICS solutions to maintain safety and environmental integrity without compromising production efficiency. Automation helps integrate information and control, power, and safety solutions to meet the requirements of affordable energy and stringent government regulations.

- Moreover, owing to the high demand for automation in the oil and gas industry, Seeq expanded its support for the oil and gas industry by introducing new connectors to CygNet enterprise Supervisory Control and Data Acquisition (SCADA) Wellsite Information Transfer Markup Language (WITSML) data storage systems. This enables advanced analytics and faster data-based decision-making in the current challenging industry environment.

- Over the past few years, oil and gas companies have invested heavily in cybersecurity technologies, such as incident response solutions and software capable of collecting logs in ICS environments to enhance visibility and segmenting networks, prevent lateral movement, and eliminate imminent threats.

- The industry increasingly adopts ICS solutions to maintain safety and environmental integrity without compromising production efficiency. Automation helps integrate information and control, power, and safety solutions to meet the requirements of affordable energy and stringent government regulations.

China Factory Automation And Industrial Controls Industry Overview

The Chinese factory automation and industrial controls market is highly fragmented, with the presence of several prominent companies. Companies continuously invest in strategic partnerships and product developments to gain market share. Some of the recent developments in the market are:

- March 2024 - Rockwell Automation announced that it is collaborating with NVIDIA to accelerate the next-generation industrial architecture. To make it easier for automation customers to digitalize industrial processes, Rockwell plans to evolve the industry by building a future factory.

- February 2024 - ABB announced that it plans to leverage this integration of AI with robotics in sectors such as automotive, consumer goods, education, and emerging areas like healthcare, retail, and new energy. This strategic move aims to create additional value for customers by introducing new levels of autonomy in robotic applications across China.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Prominence of Automation Technologies Due to Declining Workforce

- 5.2 Market Challenges

- 5.2.1 Industry Policies and Regulations

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 PLC (Programmable Logic Controller)

- 6.1.1.3 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.4 Product Lifecycle Management (PLM)

- 6.1.1.5 Human Machine Interface (HMI)

- 6.1.1.6 Manufacturing Execution System (MES)

- 6.1.1.7 Enterprise Resource Planning (ERP)

- 6.1.1.8 Other Industrial Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Sensors and Transmitters

- 6.1.2.2 Electric Motors and Drives

- 6.1.2.3 Industrial Robotics

- 6.1.2.4 Machine Vision Systems

- 6.1.2.5 Other Field Devices

- 6.1.1 Industrial Control Systems

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Power and Utilities

- 6.2.4 Automotive and Transportation

- 6.2.5 Pharmaceuticals

- 6.2.6 Food and Beverage

- 6.2.7 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 General Electric Company

- 7.1.2 Schneider Electric SE

- 7.1.3 Rockwell Automation Inc.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Emerson Electric Company

- 7.1.6 ABB Ltd

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 Siemens AG

- 7.1.9 Omron Corporation

- 7.1.10 Yokogawa Electric Corporation