|

|

市場調査レポート

商品コード

1640355

インドのプラスチック包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)India Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのプラスチック包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

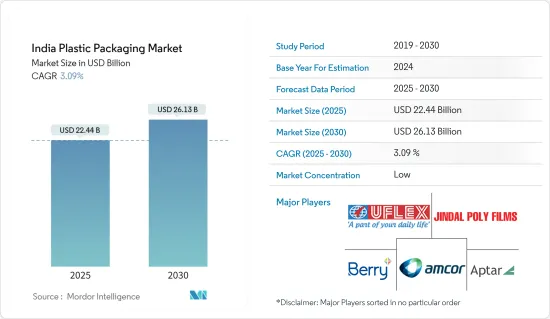

インドのプラスチック包装市場規模は2025年に224億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.09%で、2030年には261億3,000万米ドルに達すると予測されています。

プラスチックは最も著名な包装材料のひとつです。この材料は軽量で低コストであるため、あらゆるエンドユーザーの間で即座に差別化されます。

主要ハイライト

- プラスチック包装はインド包装産業の新時代の中心にあります。その多目的な用途は、多くの産業で製品包装の基盤になりつつあります。他の包装タイプに比べ、プラスチック包装容器は高い衝撃強度、剛性、バリア性といった独自の利点を備えており、これが近年のプラスチック包装市場を拡大しています。

- ポリエチレンは主にポリ袋、プラスチックフィルム、ジオメンブレンなどの包装に使用されます。軽量で部分結晶性の熱可塑性樹脂であり、高耐久性、低吸湿性、遮音性を持っています。低密度ポリエチレン(LDPE)は主にプラスチック袋の製造に使用されます。LDPEポリエチレン袋は柔らかく柔軟性があり、天然カラーがあります。これらの袋の需要は、柔軟性、透明性、高い衝撃強度、水とアルコール蒸気を除く弱いバリア性などの既知の特徴によるものです。耐熱性は弱いが、優れた電気特性と優れた耐薬品性があります。環境応力割れの傾向があります。

- パウチ包装は、非常に便利で持ち運びに便利なソリューションであるため、人気が高まっています。多くの買い物客は、従来の硬い包装よりも、柔軟性のあるスタンドアップパウチを好みます。消費者は過去10年間にスタンドアップパウチ(スナック、飲食品、ベビーフード、工業用オイルや潤滑油用)の需要を飛躍的に伸ばしました。包装タイプ特有のイノベーションが、市場の持続可能性をさらに後押ししています。

- インドではここ数年、飲料用包装市場が大きく成長しています。国全体の飲料包装動向の急速な変化は、市場の成長にとって極めて重要です。飲料包装の新たな動向は、構造の変化に加え、ポストコンシューマーリサイクルのようなリサイクル材料の開発、顧客の受容性、安全性、新たな充填技術に焦点を当てています。耐熱性PETボトルの開発により、いくつかの飲料の保存性が向上しました。

- しかし、インドのプラスチック包装市場は、主に環境問題の高まりによる規制基準のダイナミックな変化により、大きな課題に直面することが予想されます。政府はプラスチック包装廃棄物に関する国民の懸念に対応し、環境廃棄物を最小限に抑え、廃棄物管理プロセスを改善するための規制を実施しています。

インドのプラスチック包装市場の動向

食品セグメントが大きなシェアを占める

- 食品産業におけるプラスチック包装の需要は、便利でコンパクトなソリューションの必要性、特に調理済み食品の人気の高まりによって牽引されています。丸型容器やサラダパックなど、さまざまな形態の密封トレイに包装されることが多いこれらの食事は、現在、持続可能で環境に優しい材料を使用する方向へと顕著にシフトしています。この戦略的な動きは、環境に配慮した包装ソリューションを求める消費者の嗜好に沿ったものであり、産業の中で市場の需要に応え、環境への影響を減らすことに取り組んでいることを示しています。

- 軟質包装には、パウチ、袋、フィルム、ラップなど様々な形態があり、食肉、鶏肉、魚類産業において、様々なカット、ポーションサイズ、包装形態に対応する多用途の包装ソリューションを可能にしています。これにより、ホールカットからソーセージやフィレのような加工品まで、幅広い製品の効率的な包装が可能になります。

- 高い栄養価を実現するため、チーズ、牛乳、ヨーグルトなど、栄養価の高い乳製品への消費者のシフトが進んでいることも、成長を後押ししていると考えられます。その上、乳製品はビタミン、タンパク質、高吸収性カルシウムなどと長い間関連付けられてきました。これらの乳製品に含まれる数多くの生物学的に機能的な成分は、予測期間中に乳製品セグメントを強化すると予想されます。

- さらに、プラスチックトレイや容器は、食堂、レストラン、家庭、オフィスなどの食品容器として数多くの産業で使用されています。レストランのような外食産業は、食品包装トレイをテイクアウトやデリバリーサービスに利用し、食品の安全性と見栄えを保証しています。また、カフェやベーカリーのような他のセグメントでは、製品の包装や陳列のためにこれらのトレイに依存し、顧客の利便性と魅力を向上させます。

- トレイは主に、食品産業では一次包装、二次包装に、医薬品や消費財では二次包装に使用されています。トレイと容器は、主に食品、飲食品、ホスピタリティ産業における使い捨て市場の一部です。これらの製品は広く入手可能で、価格も安く、使い捨て市場の大部分を占めています。

- 「メイク・イン・インディア」構想の一環として、インド政府は食品加工セグメントへの投資を優先・促進しました。政府は、食品加工のサプライチェーンを改善するため、134のコールドチェーンプロジェクトと18のメガフードパークを創設しました。食品加工セグメントもまた、産業振興のために開始された1,000億インドルピー(13億5,000万米ドル)プログラムなどの最近の政府の施策により、堅調な開発軌道に乗っており、最終的には国内の軟質プラスチック包装の需要を高めています。

- インドにおけるeコマースの成長は、さまざまな食品に対する需要を生み出しています。同国におけるオンライン小売売上高は、2022年の8,700万米ドルから大幅に増加し、2027年には1億7,300万米ドルに達すると予測されています。オンライン小売販売の増加は、食品包装の需要がインドで増加していることを示しています。さらに、プラスチックボトルと容器は、包装された食品に長い保存期間を提供する能力により、食品産業で重要性を増しています。

インドで力強い成長を遂げるボトル

- 市場でボトルが広く使用されている産業には、食品、飲食品、化粧品、工業、医療などがあります。飲料セグメントのプラスチックボトル市場は、ボトル入り飲料水とノンアルコール飲料の需要増により成長が見込まれています。

- PepsiCo Indiaは、同社の製品「ペプシ・ブラック」が、炭酸飲料カテゴリーで初めてインドで製造される100%リサイクルPETペットボトルを導入すると発表しました。この取り組みには、完全リサイクルボトルのペプシブラックのラベルとキャップは含まれていないです。

- ペットボトル入り飲料水市場は、他の包装方法よりもコスト効率が良く、賞味期限が長く、使いやすいため、消費者の間で包装入り飲料水に対する需要が高まっていることが背景にあります。純粋な飲料水の必要性に対する一般消費者の意識が高まるにつれ、包装飲料水やボトル入り飲料水の包装産業は急速な成長を遂げています。

- ペットボトルは、炭酸飲料、ジュース飲料、フルーツジュース、スポーツドリンク、エナジードリンクなど様々なカテゴリーで大きな需要があり、その中でも水ボトルはインドで潜在的なシェアを示し、ペットボトル市場の成長を助けています。Indian Railways Catering and Tourism Corporation Limitedは、ペットボトル入り飲料水ブランド "Rail Neer "を立ち上げ、列車や駅で販売しています。2021年の生産量は7,520万本で、2023年には3億5,770万本に増加し、この地域におけるペットボトル入り飲料水需要の有機的動向を示しています。

- ペットボトルは形を作るのが簡単です。清涼飲料水のような加圧商品の入った箱は、強い内圧下でその形態を維持するのが難しいです。しかし、技術の進歩、製造方法、材料の開発により、プラスチックは圧力がかかってもどんな形にも成形できるようになりました。ペットボトルは落としても安全性が高く、軽量で透明、詰め替え可能です。回収の必要性がプラスチックのリサイクルを制約することもあります。しかし、新しい技術によって、より多くのプラスチックをリサイクルすることが可能になりつつあります。

競合情勢

インドではプラスチック包装の需要が大幅に増加しているため、市場はセグメント化しています。市場を独占している大手企業には、Aptar Group Inc.、Uflex Limited、Berry Global、Sealed Air Corporation、Constantia Flexiblesなどがあります。これらの企業は、市場シェアを維持するために技術革新を続け、戦略的パートナーシップを結んでいます。例えば

- 2024年4月、Manjushree Technopack Limitedは、Oricon Enterprises Ltd.のプラスチック包装事業を企業価値52億インドルピー(629万米ドル)で買収する最終契約を締結しました。買収された企業には、主に飲料に使用されるプラスチック容器とクロージャーのメーカーであるオリエンタルコンテナーズが含まれます。年間150億個近くの設備能力を持つこの買収により、キャップ・クロージャーセグメントにおけるMTLの現在の市場シェアは倍増することになります。

- 2023年12月、米国のAptar Corporationの完全子会社であるAptar Pharmaは、東南アジア市場向けの生産能力を増強するため、インドのムンバイに新しい製造施設を設立しました。その生産能力は、東南アジアの医薬品顧客の製造能力を向上させ、より革新的な製品ソリューションを提供するためにさらに強化されました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 軽量包装の採用増加

- 環境に優しい包装と再生プラスチックの増加

- eコマース産業の成長が成長を牽引する見込み

- 市場抑制要因

- 原料(プラスチック樹脂)価格の高騰

- 政府の規制と環境問題

- プラスチック包装の世界市場概要

第6章 市場セグメンテーション

- 包装タイプ別

- 軟質プラスチック包装

- 硬質プラスチック包装

- エンドユーザー別

- 食品

- 飲料

- 医療

- パーソナルケアと家庭用品

- その他

- 製品タイプ別

- ボトルとジャー

- トレイ・容器

- パウチ

- バッグ

- フィルム・ラップ

- その他

第7章 競合情勢

- 企業プロファイル

- Hitech Plast(Hitech Group)

- Mondi Group

- Sealed Air Corporation

- Berry Global Inc.

- Polyplex Corporation Limited

- TCPL Packaging Ltd

- Manjushree Tecnopack Ltd

- Aptar Group Inc.

- Amcor PLC

- Jindal Poly Films Limited

- Cosmo Films Ltd(Cosmo First Limited)

- Constantia Flexibles

第8章 投資分析

第9章 市場の将来

The India Plastic Packaging Market size is estimated at USD 22.44 billion in 2025, and is expected to reach USD 26.13 billion by 2030, at a CAGR of 3.09% during the forecast period (2025-2030).

Plastic is one of the most prominent packaging materials. The material's lightweight and low-cost nature instantly distinguished it among all the end-users.

Key Highlights

- Plastic packaging is at the center of a new era in the Indian packaging industry. Its versatile usage is becoming the foundation for many industries for product packaging. Compared to other packaging types, plastic packaging containers provide unique benefits, such as high impact strength, stiffness, and barrier properties, which have expanded the market for plastic packaging in recent years.

- Polyethylene is primarily used for packaging plastic bags, plastic films, geomembranes, etc. It is a lightweight, partially crystalline, thermoplastic resin with high resistance, low moisture absorption, and sound-insulating properties. Low-density polyethylene (LDPE) is mainly used to manufacture plastic bags. LDPE polyethylene bags are soft and flexible and are available in natural colors. The demand for these bags is due to their known features, such as flexibility, transparency, high impact strength, and weak barrier, except for water and alcohol vapor. These bags have weak temperature resistance but outstanding electrical properties and excellent chemical resistance. They show a tendency for environmental stress cracking.

- Pouch packaging is gaining popularity as it is a highly convenient and portable solution. Many shoppers prefer flexible, stand-up pouches over traditional, rigid packaging. Consumers drove the demand for stand-up pouches (for snacks, beverages, baby food, or industrial oils and lubricants) exponentially over the past decade. Specific innovations in the packaging type further drive the market's sustainability.

- The market for beverage packaging has grown significantly over the last few years in India. Rapid changes in beverage packaging trends across the country are critical for the market's growth. The new trends in the packaging of beverages focus on structural changes, as well as the development of recycled materials like post-consumer recycling, customer acceptance, safety, and new filling technologies. The development of heat-resistant PET bottles improved the preservation of several drinks.

- However, the plastic packaging market in India is expected to be significantly challenged due to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. The government is responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

India Plastic Packaging Market Trends

Food Segment to Hold a Significant Share

- The food industry's demand for plastic packaging is driven by the need for convenient, compact solutions, particularly with the increasing popularity of ready-to-eat meals. These meals, often packaged in sealed trays of various shapes, including round containers and salad packs, are now seeing a notable shift toward using sustainable and environmentally friendly materials. This strategic move aligns with consumer preferences for eco-conscious packaging solutions, indicating a commitment to meeting market demands and reducing environmental impact within the industry.

- Flexible packaging comes in various forms, such as pouches, bags, films, and wraps, allowing for versatile packaging solutions to accommodate different cuts, portion sizes, and packaging formats within the meat, poultry, and fish industries. This enables efficient packaging of a wide range of products, from whole cuts to processed items like sausages and fillets.

- The increasing shift of consumers toward nutrient-dense dairy products such as cheese, milk, yogurt, and more to achieve high nutrition is likely to aid growth. Besides, dairy products have been long associated with vitamins, proteins, highly absorbable calcium, and more. Numerous biologically functional components in these dairy products are expected to strengthen the dairy products segment over the forecast period.

- Furthermore, plastic trays and containers are used in numerous industries as food containers in cafeterias, restaurants, homes, offices, etc. Food services businesses like restaurants utilize food packaging trays for takeout and delivery services, assuring food remains secure and presentable. Besides, other sectors like cafes and bakeries depend on these trays for packaging and displaying their products, improving customer convenience and appeal.

- Trays are mainly used for primary and secondary packaging in the food industry and secondary packaging in pharmaceutical and consumer goods. Trays and containers are part of the disposables market, mainly in the food, beverage, and hospitality industries. These products are widely available, cost less, and are a large part of the disposables market.

- As part of the "Make in India" initiative, the Indian government prioritized and promoted investments in the food processing sector. The government created 134 cold chain projects and 18 mega food parks to improve the food processing supply chain. The food processing sector is also on a solid development trajectory due to recent government measures, such as the INR 10,000 crore (USD 1.35 billion) program launched to promote the industry, eventually enhancing the demand for flexible plastic packaging in the country.

- The growth of e-commerce in India creates the demand for different food products. The rise of online retail sales in the county grew significantly from USD 87 million in 2022, and it is forecasted to reach USD 173 million by 2027. Growing retail online sales show that the demand for food packaging is increasing in India. Moreover, plastic bottles and containers have gained importance in the food industry due to their ability to provide longer shelf life to packaged food items.

Bottles to Witness Strong Growth in the Country

- The industries where bottles are widely used in the market include food, beverage, cosmetics, industrial, healthcare, and more. The beverage sector's plastic bottle market is anticipated to witness growth owing to the increased demand for bottled water and non-alcoholic beverages.

- PepsiCo India announced that its product Pepsi Black will introduce the first 100% recycled PET plastic bottles in the carbonated beverages category to be manufactured in India. The manufacturer does not include the Pepsi Black label and cap for a completely recycled bottle in this initiative.

- The market for bottled water packaging in plastic bottles is driven by the rising demand for packaged drinking water among consumers because they are more cost-effective than other packaging options, have a longer shelf life, and are easier to use. The packaged and bottled water packaging industries are experiencing rapid growth as public awareness of the need for pure drinking water increases.

- Plastic bottles have a significant demand in India in various categories, such as carbonated soft drinks, juice drinks, fruit juices, and sports and energy drinks, out of which water bottles show a potential share in the country, aiding the growth of the plastic bottle market. Indian Railways Catering and Tourism Corporation Limited launched a pet bottled water brand, "Rail Neer," which is sold on trains and railway stations. It produced 75.20 million bottles in 2021, which increased to 357.70 million bottles in 2023, indicating the organic trend in demand for plastic bottled water in the region.

- A plastic bottle is simple to shape. It can be difficult for a box containing pressurized goods like soft drinks to keep its shape under intense internal pressure. However, with technological advancements, manufacturing methods, and material development, plastic can be molded into any shape, even under pressure. If dropped, a plastic bottle has a high safety factor and is lightweight, transparent, and refillable. The need for collection can constrain plastic recycling. However, new technologies are making it possible for more plastic to be recycled.

Competitive Landscape

As the demand for plastic packaging is increasing significantly in India, the market is fragmented. Large, dominant players in the market include Aptar Group Inc., Uflex Limited, Berry Global, Sealed Air Corporation, and Constantia Flexibles. These companies keep innovating and entering into strategic partnerships to retain their market share. For instance,

- In April 2024, Manjushree Technopack Limited entered into definitive agreements to acquire Oricon Enterprises Ltd's plastic packaging business for an enterprise value of INR 520 crores (USD 6.29 million). The acquired company included Oriental Containers, a manufacturer of plastic containers and closures used primarily in beverages. With an installed capacity of nearly 15 billion pieces per year, this transaction will double MTL's current market share in the cap and closure sector.

- In December 2023, Aptar Pharma, a wholly owned subsidiary of the US-based Aptar Corporation, established its new manufacturing facility in Mumbai, India, to increase production capacity for Southeast Asian markets. Its production capabilities have been further enhanced to improve the manufacturing capacity of pharmaceutical customers in Southeast Asia and to offer more innovative product solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight-packaging Methods

- 5.1.2 Increased Eco-friendly Packaging and Recycled Plastic

- 5.1.3 Growing E-commerc Industry is Expected to Drive Growth

- 5.2 Market Restraints

- 5.2.1 High Price of Raw Material (Plastic Resin)

- 5.2.2 Government Regulations and Environmental Concerns

- 5.3 Global Plastic Packaging Market Overview

6 MARKET SEGMENTATION

- 6.1 By Packaging Type

- 6.1.1 Flexible Plastic Packaging

- 6.1.2 Rigid Plastic Pacakaging

- 6.2 By End User

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Personal Care and Household

- 6.2.5 Other End Users

- 6.3 By Product Type

- 6.3.1 Bottles and Jars

- 6.3.2 Trays and Containers

- 6.3.3 Pouches

- 6.3.4 Bags

- 6.3.5 Films and Wraps

- 6.3.6 Other Product Types

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hitech Plast (Hitech Group)

- 7.1.2 Mondi Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 Berry Global Inc.

- 7.1.5 Polyplex Corporation Limited

- 7.1.6 TCPL Packaging Ltd

- 7.1.7 Manjushree Tecnopack Ltd

- 7.1.8 Aptar Group Inc.

- 7.1.9 Amcor PLC

- 7.1.10 Jindal Poly Films Limited

- 7.1.11 Cosmo Films Ltd (Cosmo First Limited)

- 7.1.12 Constantia Flexibles