中東・アフリカのプロセスオートメーション:市場シェア分析、産業動向、成長予測(2025年~2030年)

Middle East And Africa Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1640347

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

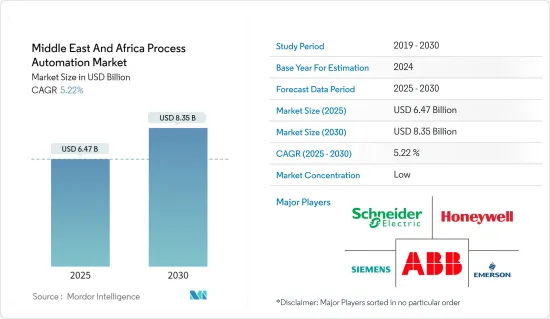

中東・アフリカのプロセスオートメーション市場規模は2025年に64億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.22%で、2030年には83億5,000万米ドルに達すると予測されます。

自動化は、近代的な製造・産業プロセスにとって不可欠なものとなっています。それは、企業が優先順位を実現するのに役立っています。この地域の企業は、SCADA、DCS、MES、PLCなどのさまざまな技術の助けを借りて業務を自動化しています。これらの技術に対する需要は高まっており、多くのベンダーが、企業が製造プロセスでより高い効率を達成できるよう支援するソリューションを製造しています。

主なハイライト

- 製造プロセスの自動化は、モニタリングの容易化、無駄の削減、生産スピードの向上など、さまざまなメリットをもたらします。この技術は、標準化による品質の向上と、信頼性の高い製品を時間内かつ低コストで顧客に提供します。

- SCADA、HMI、PLCシステム、および可視化を提供するソフトウェアの採用において、産業機械と設備を接続し、リアルタイムデータを取得することが重要な役割を果たし、その結果、製品の不具合を減らし、ダウンタイムを削減し、メンテナンスをスケジューリングし、意思決定のために反応的な状態から予測的・規定的な段階へと切り替えることが可能になりました。

- インダストリアル・モノのインターネット(IIoT)とインダストリアル4.0は、スマート・ファクトリー・オートメーションとして知られるロジスティクス・チェーン全体の開発、生産、管理のための新しい技術的アプローチの中心にあります。これらは産業部門の動向を支配しており、機械やデバイスはインターネットを介して接続されています。

- さらに、自動化によって内部プロセスを近代化し、オペレーションやメンテナンスに関する情報へのアクセスを改善することで、この地域の産業は生産と流通を合理化し、より高い歩留まりを実現できるようになります。

- 新技術に対する政府支出の増加により、サウジアラビアはファクトリーオートメーションと産業用制御システム産業において中東の主要国のひとつになると予想されます。その結果、国のオートメーションと製造業の将来にとってインダストリー4.0が重要になります。

- サウジアラビアの2030年ビジョンは、国の地位、戦略的パートナーシップ、エネルギー資源、物流を活用することで、産業とオートメーションの新たな段階を目指しています。また、2030年までに再生可能エネルギーと産業製造部門を自動化し、国内需要の50%を国内で製造することを目指しています。

中東・アフリカのプロセスオートメーション市場動向

石油・ガスエンドユーザー産業が大きな市場シェアを占める見込み

- 石油・ガスエンドユーザー業界では、自動化が大きな原動力であり動向です。デジタル化、自動化、先端技術により、オペレーターや技術者は重要なパフォーマンス、資産状況、技術情報に即座にアクセスできるようになります。この地域の石油・ガス企業は、意思決定、トラブルシューティング、パフォーマンス効率を高めるために、プロセスオートメーションツールの採用を増やしています。

- 石油・ガスのエンドユーザー産業の上流部門では、厳しい政府規制を満たす必要があり、運用コストを削減するための綿密な計画を必要とする掘削活動がいくつか行われています。多くの場合、エンドユーザー業界は膨大な空間データセットを扱い、いくつかの意思決定を行います。空間データのパワーを最大限に活用するために、いくつかのプロセスオートメーションツールや分析エンジンが採用されています。

- 中東の石油・ガス会社は、より多くの再生可能エネルギーに移行する際、しばしば課題に直面します。多様な状況での需要に対応するため、エネルギー企業はビジネスモデルの中でプロセスオートメーションのような革新的な技術に焦点を当て、イノベーションを取り入れ、効率を高める必要があります。

- 2024年2月現在、同地域には296基の陸上リグがあり、さらに中東のオフショアに53基、同地域に95基の陸上リグが配置されています。アフリカのオフショアには16基のリグが配置されています。

- 石油・ガス産業のプロセスでは、安全性と信頼性に対する需要が急増しています。サプライチェーンは、自動化、業界の専門知識、広範なパートナーネットワークに対する大きなニーズを生み出しています。プロセスオートメーションは、石油・ガス生産者が情報を統合し、動力を制御し、ダイナミックな世界的需要に対応するための安全ソリューションを提供するのに役立ちます。

- 原油価格の変動に伴い、複数の石油・ガス会社は、流通チェーン全体でコストを最小限に抑え、効率を最大化することに注力しています。競争環境の激化と小売マージンの減少の中で持続していくためには、複数の部門における複数のプロセスを最適化する必要があります。

アラブ首長国連邦が大きな市場シェアを占める見込み

- インダストリー4.0に後押しされ、アラブ首長国連邦(UAE)はファクトリーオートメーションと産業用制御システム業界において革新を続け、その地位を固めています。同市場におけるスマート技術の採用は、国民経済にプラスの影響を与えています。

- アラブ首長国連邦では、建設産業が経済の向上と開発に不可欠な役割を果たしています。SCADAは建設業界でますます使用されています。SCADA(Supervisory Control and Data Acquisition:監視制御およびデータ収集)により、ユーザーは現場や遠隔から産業オペレーションを制御することができます。建設業界におけるSCADAの利点は、リアルタイムでデータを監視・収集し、それを産業用に処理できる点にあります。

- 世界の製造業の統合が進むにつれ、自動化投資に対するプレッシャーが高まっています。

- アラブ首長国連邦(UAE)のスマート工場ではサイバー攻撃が増加しており、産業用制御システムの使用に対する懸念が高まっています。政府もこのような犯罪の増加を抑制する計画を持っています。これは、サイバーセキュリティ侵害のリスクを回避するために、スマート工場のために国内で製造される産業用制御システムの増加傾向と一致しています。

- プロセスディスカバリー、プロセス最適化、プロセスインテリジェンス、プロセスオーケストレーションなどの技術は、ロボティック・プロセスオートメーション(RPA)の重要な部分を占めるようになってきています。今後、ビジネスプロセス管理(BPM)とRPAの関係がより緊密になる傾向が続いています。

- パンデミックの影響からUAE経済を復活させるための政府による投資展開では、中小企業の成長とともに、インフラとエレクトロニクス産業が主な受益者として注目されました。インフラとエレクトロニクス産業は、産業用制御システムのハードウェア製品とソフトウェア・ソリューションのヘビーユーザーであり、直接的なプラス効果が期待されます。

中東・アフリカのプロセスオートメーション産業概要

中東・アフリカのプロセスオートメーション市場は、世界プレイヤーと中小企業の両方が存在するため、非常に断片化されています。同市場の主要プレイヤーには、ABB Ltd、Siemens AG、Schneider Electric、Emerson Electric Co.、Honeywell International Inc.などがいます。市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2024年2月エネルギー管理とオートメーションのデジタル変革におけるリーダーの一人であるシュナイダーエレクトリックは、テクノロジー企業のインテルとレッドハットと協力し、分散制御ノード(DCN)ソフトウェアフレームワークのリリースを発表しました。シュナイダーエレクトリックのEcoStruxure Automationの拡張であるこの新しいフレームワークにより、産業企業はソフトウェア定義のプラグアンドプロデュースソリューションに移行し、運用の強化、品質の確保、複雑性の軽減、コストの最適化を図ることができます。

- 2023年10月エマソンは、現場、エッジ、クラウドからのデータを接続するソフトウェア中心の産業用オートメーションプラットフォームであるBoundless Automationビジョンをサポートする新技術を発表。より安全で柔軟かつスケーラブルなソリューションを消費者に提供し、業務の最適化と自動化を支援します。エマソンのイノベーションには、DeltaV Edge Environment、Ethernet APL、DeltaV PK Flex Controllerなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 中東・アフリカのプロセスオートメーション市場へのマクロ動向の影響

第5章 市場力学

- 市場促進要因

- エネルギー効率とコスト削減の重視の高まり

- 安全オートメーションシステムへの需要

- IIoTの出現

- 市場の課題

- コストと実装の課題

第6章 市場セグメンテーション

- 通信プロトコル別

- 有線

- 無線

- システムタイプ別

- システムハードウェア別

- 監視制御・データ収集システム(SCADA)

- 分散型制御システム(DCS)

- プログラマブルロジックコントローラ(PLC)

- 製造実行システム(MES)

- バルブおよびアクチュエーター

- 電動モーター

- ヒューマン・マシン・インターフェース(HMI)

- プロセス安全システム

- センサーとトランスミッター

- システムソフトウェア

- APC(スタンドアロンおよびカスタマイズソリューション)

- 高度な規制制御

- 多変数モデル

- 推論および逐次

- データ分析およびレポートベースのソフトウェア

- その他のソフトウェアとサービス

- システムハードウェア別

- エンドユーザー産業別

- 石油・ガス

- 化学・石油化学

- 電力・公益事業

- 上下水道

- 飲食品

- 製紙・パルプ

- 製薬

- その他エンドユーザー産業

- 国別

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第7章 競合情勢

- 企業プロファイル

- ABB Ltd

- Siemens AG

- Schneider Electric

- Emerson Electric Co.

- Honeywell International Inc.

- General Electric

- Mitsubishi Electric

- Fuji Electric

- Eaton Corporation

- Delta Electronics Inc.

第8章 投資分析

第9章 市場の将来

目次

The Middle East And Africa Process Automation Market size is estimated at USD 6.47 billion in 2025, and is expected to reach USD 8.35 billion by 2030, at a CAGR of 5.22% during the forecast period (2025-2030).

Automation has become an essential part of modern manufacturing and industrial processes. It helps enterprises to realize priorities. Companies in the region are automating their operations with the help of different technologies like SCADA, DCS, MES, and PLC. The demand for these technologies is escalating, and many vendors are manufacturing solutions to help enterprises achieve higher efficiency in their manufacturing processes.

Key Highlights

- Automation of manufacturing processes offers various benefits, such as effortless monitoring, reduction of waste, and production speed. This technology provides customers with improved quality with standardization and dependable products within time and at a much lower cost.

- Connecting the industrial machinery and equipment and obtaining real-time data have played a vital role in the adoption of SCADA, HMI, PLC systems, and software that offer visualization, thus enabling reducing the faults in the product, reducing downtime, scheduling maintenance, and switching from being in the reactive state to predictive and prescriptive stages for decision-making.

- The Industrial Internet of Things (IIoT) and Industrial 4.0 are at the center of new technological approaches for the development, production, and management of the entire logistics chain, otherwise known as smart factory automation. They dominate industrial sector trends, with machinery and devices being connected via the internet.

- Further, modernizing internal processes with automation and better access to information about operations and maintenance will help the industry streamline production and distribution and allow for a higher yield in the region.

- Increased government spending on new technologies is expected to make Saudi Arabia one of the major countries in the Middle East in the factory automation and industrial control system industry. As a result, Industry 4.0 is important for the future of national automation and manufacturing.

- Saudi Arabia's 2030 vision aims for a new phase of industry and automation by exploiting the country's position, strategic partnerships, energy resources, and logistics. It also seeks to automate the country's renewable energy and industrial manufacturing sectors by 2030 and manufacture 50% of its needs within the country.

Middle East And Africa Process Automation Market Trends

The Oil and Gas End-user Industry is Expected to Hold a Significant Market Share

- Automation is a significant driver and trend in the oil and gas end-user industry. Digitization, automation, and advanced technologies give operators and technicians immediate access to critical performance, asset conditions, and technical information. Oil and Gas companies in the region are increasingly adopting process automation tools to enhance decision-making, troubleshooting, and performance efficiency.

- The upstream sector of the oil and gas end-user industry involves several drilling activities that must meet stringent government regulations and require intense planning to cut operational costs. Often, the end-user industry deals with vast sets of spatial data to make several decisions. Several process automation tools and analytical engines are employed to harness the full power of spatial data.

- Middle Eastern oil and gas companies often face challenges when transitioning to more renewable sources. To meet the demand in diverse situations, energy companies must focus on innovative technologies like process automation within their business models to embrace innovation and increase efficiency.

- As of February 2024, there were 296 land rigs in the region, with a further 53 rigs located offshore in the Middle East and 95 land rigs in that region; 16 rigs were located offshore in Africa.

- There is a surging demand for safety and reliability in the oil and gas industry processes. The supply chain creates a significant need for automation, industry expertise, and an extensive partner network. Process automation helps oil and gas producers integrate information, control power, and provide safety solutions to respond to the dynamic global demand.

- With the fluctuation in crude oil prices, several oil and gas companies focus on minimizing costs and maximizing efficiency throughout the distribution chain. To sustain itself in the rising competitive environment and decrease retail margins, the company needs to optimize several processes in multiple sectors.

The United Arab Emirates is Expected to Account For a Significant Market Share

- Fueled by Industry 4.0, the UAE continues to innovate and consolidate its position in the factory automation and industrial control systems industry. The adoption of smart technologies in the market has positively impacted the national economy.

- In the United Arab Emirates, the construction industry plays an essential role in economic upliftment and development. SCADA is being increasingly used in the construction industry. Supervisory Control and Data Acquisition (SCADA) allows users to control industrial operations on-site and remotely. The advantage of SCADA in the construction industry lies in the ability to monitor and gather data in real-time and then process it for industrial usage.

- Increasing global manufacturing integration is raising the pressure for automation investment, as cost minimization with quality maximization looms ever more significantly as an operating paradigm for Arab manufacturers.

- With cyber-attacks increasing in smart factories in the UAE, there is growing concern about using Industrial Control Systems. The government also has plans to curb the rise of such crimes. This aligns with the growing trend of industrial control systems manufactured in the country for smart factories to avoid the risk of cybersecurity breaches.

- Technologies such as process discovery, process optimization, process intelligence, and process orchestration are becoming a more significant part of Robotic Process Automation (RPA). There is an ongoing trend of increasing a closer relationship between business process management (BPM) and RPA in the future.

- With investment roll-outs by the government to revive the UAE economy from the effects of the pandemic, the infrastructure and electronics industry were marked as the primary beneficiaries, alongside the growth of small and medium-sized enterprises. The infrastructure and electronics industry are heavy users of industrial control systems' hardware products and software solutions and are expected to have a direct positive effect.

Middle East And Africa Process Automation Industry Overview

The Middle East and African process automation market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are ABB Ltd, Siemens AG, Schneider Electric, Emerson Electric Co., and Honeywell International Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2024: Schneider Electric, one of the leaders in the digital transformation of energy management and automation, collaborated with the technology companies Intel and Red Hat and announced the release of a Distributed Control Node (DCN) software framework. An extension of Schneider Electric's EcoStruxure Automation, this new framework enables industrial companies to move to a software-defined, plug-and-produce solution to enhance their operations, ensure quality, reduce complexity, and optimize costs.

- October 2023: Emerson introduced new technologies to support its Boundless Automation vision, a software-centric industrial automation platform that connects data from the field, the edge, and the cloud. More secure, flexible and scalable solutions are provided to consumers to help optimize and automate their operations. Emerson's innovations include DeltaV Edge Environment, Ethernet APL and DeltaV PK Flex Controller.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macro Trends on the Middle East and Africa Process Automation Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Energy Efficiency & Cost Reduction

- 5.1.2 Demand for Safety Automation Systems

- 5.1.3 Emergence of IIoT

- 5.2 Market Challenges

- 5.2.1 Cost and Implementation Challenges

6 MARKET SEGMENTATION

- 6.1 By Communication Protocol

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By System Type

- 6.2.1 By System Hardware

- 6.2.1.1 Supervisory Control and Data Acquisition System (SCADA)

- 6.2.1.2 Distributed Control System (DCS)

- 6.2.1.3 Programmable Logic Controller (PLC)

- 6.2.1.4 Manufacturing Execution System (MES)

- 6.2.1.5 Valves and Actuators

- 6.2.1.6 Electric Motors

- 6.2.1.7 Human Machine Interface (HMI)

- 6.2.1.8 Process Safety Systems

- 6.2.1.9 Sensors and Transmitters

- 6.2.2 By System Software

- 6.2.2.1 APC (Standalone and Customized Solutions)

- 6.2.2.1.1 Advanced Regulatory Control

- 6.2.2.1.2 Multivariable Model

- 6.2.2.1.3 Inferential and Sequential

- 6.2.2.2 Data Analytics and Reporting-based Software

- 6.2.2.3 Other Software and Services

- 6.2.1 By System Hardware

- 6.3 By End-user Industry

- 6.3.1 Oil and Gas

- 6.3.2 Chemical and Petrochemical

- 6.3.3 Power and Utilities

- 6.3.4 Water and Wastewater

- 6.3.5 Food and Beverage

- 6.3.6 Paper and Pulp

- 6.3.7 Pharmaceutical

- 6.3.8 Other End-user Industries

- 6.4 By Country

- 6.4.1 United Arab Emirates

- 6.4.2 Saudi Arabia

- 6.4.3 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Siemens AG

- 7.1.3 Schneider Electric

- 7.1.4 Emerson Electric Co.

- 7.1.5 Honeywell International Inc.

- 7.1.6 General Electric

- 7.1.7 Mitsubishi Electric

- 7.1.8 Fuji Electric

- 7.1.9 Eaton Corporation

- 7.1.10 Delta Electronics Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日