|

市場調査レポート

商品コード

1640334

北米の温度センサ:市場シェア分析、産業動向、成長予測(2025~2030年)North America Temperature Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の温度センサ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

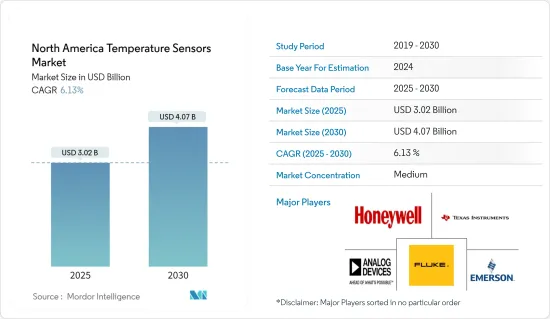

北米の温度センサ市場規模は2025年に30億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.13%で、2030年には40億7,000万米ドルに達すると予測されています。

温度センサは、環境の温度を測定し、入力データを電子データに変換して、温度変化をモニターまたは信号として記録します。このようなプロセスやモニタリングの自動化を産業や防衛業務に採用することが、資産モニタリング、セキュリティ、品質保証におけるワイヤレスセンサの需要を増大させる主要要因となっています。

主要ハイライト

- 航空宇宙、石油・ガス、鉱業などの産業は、過酷で複雑な動作環境を特徴としており、このような外部環境の極限に耐え、所望の精度、信頼性、精度、再現性で動作する適切なセンサの採用は、これらのエンドユーザーにとって極めて重要です。

- 温度モニタリングにおける急速な技術進歩は、ここ数年のワイヤレス温度センサの成長に重要な役割を果たしています。複数の大規模メーカーが、赤外線センサや熱センサといった先進的なコンセプトの実装に注力しています。先進的なコンセプトの使用は、今後数年間の市場成長の大きな可能性を開くと期待されています。

- 防衛費の増加に伴い、無線タイプのセンサは防衛産業内で複数の用途を持つ新興技術セグメントとなっています。防衛車両や航空宇宙車両の統合車両健全性モニタリング(IVHM)などの用途は、主に乗組員の安全と車両を確保するために必要です。

- センサネットワークの本質は、環境の物理的特性をモニタリングし、その物理的測定値を電気インパルスに変換することです。センサネットワークは主に温度などの特性を測定します。様々なケースで、ネットワークは環境を感知するだけでなく、感知されたデータに基づいて物理的環境に作用するように設計されています。

- 温度センサはIoT接続を採用し、COVID-19スクリーニングを高速化しています。スクリーニングプロセス機器に対する市場の需要は、新しい温度センサデバイスを発明するための様々な企業の協力が著しく高まっている温度センサの需要を可能にしています。例えば、ポリセンス・ Technologiesとセムテックは、セムテックの長距離(LoRa)低電力広域ネットワーク(LPWAN)による一連の人体温度モニタリングデバイスの開発で提携しました。このセンサは最前線の医療ワーカーにリアルタイムデータを提供し、COVID-19の最も一般的な症状の1つである高体温の個人を迅速にスクリーニングします。

北米の温度センサ市場動向

赤外線温度センサが市場成長を牽引

- 赤外線温度センサの用途は、光学対象照準や可変放射率測定など、さまざまな防衛用途で見られ、追跡活動に役立つことが多いです。しかし、これらの用途はすべて非常に高度であり、世界的に増加する軍事費により継続的な需要があります。

- 近年では、ペプシ社の人気部門である北米フリトレイ社のような一流スナックメーカーでさえ、揚げ物よりもむしろ焼き菓子の新商品を発売しています。このような動向は、世界的に厳しい食品安全規制と相まって、赤外線温度センサの大きな市場機会をまもなく生み出すと予想されます。

- FLIR(Forward-Looking Infrared)は、このような技術の著名なベンダーです。FLIRの技術は、港湾や国境、空港などで体温の上昇を調べるために使われてきました。FLIR Systemsはこの1ヶ月でその受注が大幅に増加しました。

- FLIR Systemsの製品を体温検査に使用している国の数は増え続けています。現在、中国、タイ、台湾、フィリピン、シンガポール、マレーシア、韓国、イタリア、米国が含まれています。

- 予知保全は赤外線(IR)温度センサの機能的用途の1つであり、企業は予知保全、自動化、IoTにますます注力しています。

米国が大きな市場シェアを占める

- 米国は、同国の様々な産業における進歩により、大きな市場シェアを占めています。さまざまな製品に組み込まれる複数タイプの温度センサの研究開発により、温度センサ市場は健全な成長を遂げると考えられます。

- 例えば、General Motorsなどの自動車メーカーは、2023年までに20種類の新型電気自動車を発売する予定です。また、Teslaは、信頼性が高く効率的な電気自動車を発表し、同国のEV市場セグメントの様相を一変させました。

- 米国の自動車産業は、直接的・間接的に数十万人の米国人を雇用し、数十億米ドルを投資しています。自動車産業は毎年、世界中で1,050億米ドル近くを研究開発に費やしていると推定され、そのうち180億米ドルは、より新しく先進的なセンサを自動車に組み込むために米国で費やされています。

- 米国内務省は、2019~2024年にかけての全国大陸棚外石油・ガスリース計画(全国OCS計画)のもと、大陸棚外(OCS)鉱区の約90%で海洋試掘を許可する計画であり、この地域の石油・ガス部門は市場に新たな機会を開くと予想されます。

- COVID-19パンデミックでは、温度スクリーニングのために職場で温度センサの需要が高まっていることが市場で確認されています。例えば、米国のCDC(疾病管理予防センター)やWHO(世界保健機関)は職場での温度チェックを推奨しています。

北米の温度センサ産業概要

北米の温度センサ市場は、Honeywell、Analog Devices、Texas Instrumentsなどの地域メーカーや地元メーカーをはじめ、多くの企業が参入しているため、適度にセグメント化されています。継続的な製品のアップグレードと産業の融合が、市場を高度に差別化された製品へと牽引しています。さらに、参入企業は市場での存在感を高めるために、M&Aやパートナーシップなどの戦略的イニシアチブを採用しています。最近の市場開拓の動向をいくつか発表します。

- 2020年7月-Maxim Integrated Products Inc.とAnalog Devices Inc.は正式契約を締結したと発表しました。Analog DevicesはMaximを全株式取引で買収し、統合後の企業価値は680億米ドルを超えます。この取引は2021年夏に完了する予定です。この取引により、Analog Devicesは強化され、複数の市場にまたがるリーチと規模が拡大します。

- 2021年5月-Honeywellは、ニューヨークのジョン・F・ケネディ国際空港の第1ターミナルに、乗客と従業員のための先進的皮膚温度スクリーニングシステム(Honeywell Thermo Rebellion)を設置。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- COVID-19の産業への影響評価

- 市場促進要因

- インダストリー4.0と高速ファクトリーオートメーションの成長

- 特に過酷な環境におけるワイヤレス技術の採用増加

- 市場抑制要因

- 高いセキュリティニーズとインフラ更新コスト

- バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 電気自動車センサ市場

- xEVセンサの市場予測

- EVへのセンサ採用に影響を与える動向と力学

- EVの2つの大分類による市場予測の内訳

- EVで使用される主要センサカテゴリーと主要用途

第6章 市場セグメンテーション

- タイプ別

- 有線

- ワイヤレス

- 技術別

- 赤外線

- 熱電対

- 抵抗温度検出器

- サーミスタ

- 温度トランスミッタ

- 光ファイバー

- その他

- エンドユーザー産業別

- 化学・石油化学

- 石油・ガス

- 金属・鉱業

- 発電

- 飲食品

- 自動車

- 医療

- 航空宇宙・軍事

- 民生用電子機器

- その他

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Siemens AG

- Texas Instruments Incorporated

- Honeywell International Inc.

- Analog Devices Inc.

- Fluke Process Instruments

- Emerson Electric Company

- Microchip Technology Incorporated

- Sensata Technologies

- FLIR Systems

- Maxim Integrated Products

第8章 投資分析

第9章 市場の将来

The North America Temperature Sensors Market size is estimated at USD 3.02 billion in 2025, and is expected to reach USD 4.07 billion by 2030, at a CAGR of 6.13% during the forecast period (2025-2030).

The temperature sensor measures the temperature of its environment and converts the input data into electronic data to record monitor or signal temperature changes. Adopting such process and monitoring automation in industrial and defense operations is the major driver augmenting the demand for wireless sensors in asset monitoring, security, and quality assurance.

Key Highlights

- Industries, such as aerospace, oil and gas, and mining, among others, are characterized by the harsh and complex operating environment and the adoption of a suitable sensor to withstand such external environment extremities and performing at the desired accuracy, reliability, precision, and repeatability are of crucial importance for these end-users.

- Rapid technological advancements in temperature monitoring have played a crucial role in the growth of wireless temperature sensors in the past few years. Multiple large-scale manufacturers have been focusing on implementing advanced concepts such as IR sensors and heat sensors. The usage of advanced concepts is further expected to open up significant potential for the market's growth in the coming years.

- With the increase in defense expenditure, wireless type sensors have been an emerging technology area with multiple applications within the defense industry. Applications such as integrated vehicle health monitoring (IVHM) of the defense and aerospace vehicles are primarily needed to ensure the crew's safety and the vehicle.

- At their essence, the sensor networks have been monitoring the physical characteristics of an environment and then translating those physical measurements to electrical impulses. The sensor networks primarily measure characteristics such as temperature, among others. In various cases, the network has been designed to not only sense the environment but also act on the physical environment based on the sensed data.

- Temperature sensors are employing IoT connectivity to speed COVID-19 screening. The market demand for screening process equipment has enabled the demand for temperature sensors where various firms' collaboration to invent new temperature sensor devices has raised significantly. For instance, Polysense Technologies and Semtech have joined forces in developing a series of human body temperature monitoring devices based on Semtech's Long Range (LoRa) Low-Power Wide-Area Network (LPWAN). The sensors offer real-time data to frontline healthcare workers and quickly screen individuals with high temperatures, one of the most common symptoms of COVID-19.

North America Temperature Sensors Market Trends

Infrared Temperature Sensors to Drive the Market Growth

- IR temperature sensor applications are found in various defense applications such as optical target sighting and variable emissivity measurements that are often helpful in tracking activities. However, all these applications are very advanced and have a continuous demand due to the globally increasing military spending.

- In recent years, even the top snack manufacturers like Frito-Lay North America, Inc, a popular division of Pepsi Co, have started a new range of products rather baked than fried. Such trends, coupled with stringent food safety regulations worldwide, are expected soon to create substantial market opportunities for IR temperature sensors.

- Forward-Looking Infrared (FLIR) has been a prominent vendor for such technology. FLIR technology has been used in ports and borders and airports, and other places to look for elevated body temperatures. The company has witnessed a significant increase in those orders in the past month.

- The list of countries using FLIR products for temperature screening continues to grow. It now includes China, Thailand, Taiwan, the Philippines, Singapore, Malaysia, South Korea, Italy, and the U.S. The company stated that its supply chain is continuing to keep up with demand.

- Predictive maintenance is one of the functional uses of Infrared (IR) temperature sensors in the market; enterprises are increasingly focusing on predictive maintenance, automation, and IoT.

United States Holds Significant Market Share

- The United States holds a significant market share due to advancements across various industries in the country. With the R & D of multiple types of temperature sensors being integrated into different products, the market for temperature sensors is set to grow at a healthy rate.

- For instance, automakers, such as General Motors, have planned to launch 20 new all-electric vehicles by 2023. The Tesla Company also changed the face of the EV market segment in the country by introducing reliable and efficient electric vehicles.

- The United States's automotive industry, directly and indirectly, employs hundreds of thousands of Americans and invest billions of dollars. It was estimated that the automotive industry annually spends nearly USD 105 billion on R&D worldwide, USD 18 billion of which is spent in the United States to incorporate newer and more advanced sensors into automobiles.

- With the US Department of the Interior planning to allow offshore exploratory drilling in about 90% of the Outer Continental Shelf (OCS) acreage, under the National Outer Continental Shelf Oil and Gas Leasing Program (National OCS Program) for 2019-2024, the oil and gas sector in the region is expected to open up new opportunities to the market.

- In the COVID-19 pandemic, the market is witnessing growing demand for temperature sensors at the workplace for temperature screening. For instance, the CDC (Centers for Disease Control and Prevention) in the United States and WHO (World Health Organization) recommended temperature checking at the workplace.

North America Temperature Sensors Industry Overview

The North America temperature sensor market is moderately fragmented due to many players operating in the market, such as Honeywell, Analog Devices Inc, and Texas Instruments, among other regional and local manufacturers. Continuous product up-gradation and industry convergence are driving the market towards highly differentiated offerings. Further, players adopt strategic initiatives such as mergers and acquisitions, partnerships, etc., to strengthen their market presence. Some of the recent developments in the market are:

- July 2020 - Maxim Integrated Products Inc. and Analog Devices Inc. announced that they entered into a definitive agreement. Analog Devices Inc. will acquire Maxim in an all-stock transaction that values the combined enterprise at over USD 68 billion. The transaction is expected to close in the summer of 2021. This transaction would strengthen Analog Devices Inc. and increase its reach and scale across multiple markets.

- May 2021 - Honeywell installed advanced skin temperature screening systems (Honeywell Thermo Rebellion) in Terminal One of New York's John F. Kennedy International Airport for passengers and employees

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Assessment of Impact of COVID-19 on the Industry

- 4.3 Market Drivers

- 4.3.1 Growth in Industry 4.0 & Rapid Factory Automation

- 4.3.2 Increasing Adoption of Wireless Technologies, especially in Harsh Environments

- 4.4 Market Restraints

- 4.4.1 Higher Security Needs and Infrastructure Updating Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 ELECTRIC VEHICLE SENSOR MARKET

- 5.1 Market Estimation for xEV Sensors

- 5.2 Trends and Dynamics Impacting the Adoption of Sensors in EV

- 5.3 Breakdown of the Market Estimates by Two Broader Classes of EV

- 5.4 Major Sensor Categories used in EV with Key Applications

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By Technology

- 6.2.1 Infrared

- 6.2.2 Thermocouple

- 6.2.3 Resistance Temperature Detector

- 6.2.4 Thermistor

- 6.2.5 Temperature Transmitter

- 6.2.6 Fiber Optic

- 6.2.7 Others

- 6.3 By End-user Industry

- 6.3.1 Chemical & Petrochemical

- 6.3.2 Oil and Gas

- 6.3.3 Metal and Mining

- 6.3.4 Power Generation

- 6.3.5 Food and Beverage

- 6.3.6 Automotive

- 6.3.7 Medical

- 6.3.8 Aerospace and Military

- 6.3.9 Consumer Electronics

- 6.3.10 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Texas Instruments Incorporated

- 7.1.3 Honeywell International Inc.

- 7.1.4 Analog Devices Inc.

- 7.1.5 Fluke Process Instruments

- 7.1.6 Emerson Electric Company

- 7.1.7 Microchip Technology Incorporated

- 7.1.8 Sensata Technologies

- 7.1.9 FLIR Systems

- 7.1.10 Maxim Integrated Products