|

市場調査レポート

商品コード

1851369

産業用制御システム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Industrial Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用制御システム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月11日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

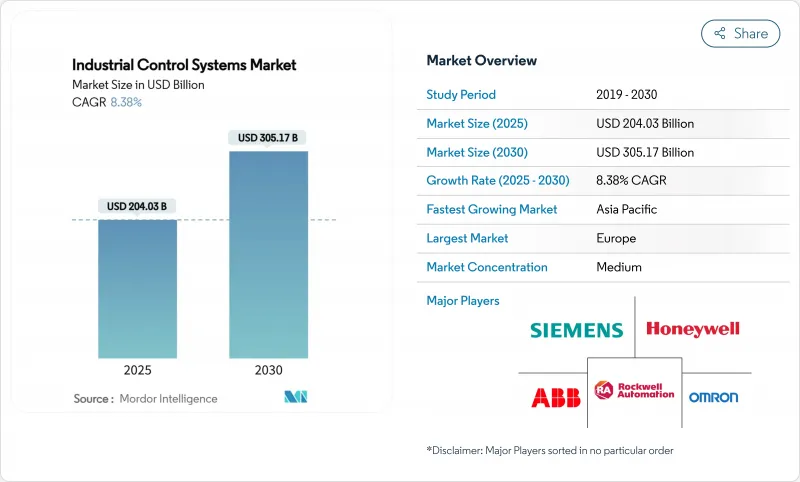

産業用制御システムの市場規模は、2025年に2,040億3,000万米ドルに達し、2030年には3,051億7,000万米ドルに達すると予測され、CAGRは8.38%で推移します。

インダストリー4.0の下で加速するデジタル化、サイバーセキュリティの義務化、オープンでベンダーニュートラルなアーキテクチャの魅力の高まりにより、自動化は効率化のためのアドオンではなく、オペレーションの要として強化されています。2024年の半導体不況でサプライチェーンリスクが高まったことで、専用ハードウェアから機能を切り離すソフトウェア定義制御プラットフォームの価値が浮き彫りになり、一方、欧州と北米では政府の優遇措置により、改修プロジェクトの資本プールが拡大した。クラウド、エッジ、オンプレミスが共存するようになったのは、メーカーが低レイテンシのプロセス制御を放棄することなく、スケールの大きな分析を求めるようになったからです。特にエレクトロニクスやライフサイエンスなどの高精度分野では、相互運用可能なハードウェアにAI対応ソフトウェアや統合セキュリティを組み合わせたベンダーが競争上有利になっています。

世界の産業用制御システム市場の動向と洞察

工場全体の自動化を加速するインダストリー4.0の展開

製造業者は、自動化を孤立したラインから、オペレーション、エンジニアリング、ビジネスデータを統合する企業規模のネットワークへと拡張しています。シーメンスSINUMERIK ONEのようなAI対応のエッジノードは、現在、機械フロアで直接、予知保全と適応フィードレート制御を実行し、意思決定の待ち時間を短縮しています。より広範な接続性は複合的な価値を生み出し、マクロ的な逆風にもかかわらず、2025年にOT予算の平均が30%増加した理由を説明しています。その結果、相互運用可能な製品が独自のポイント製品を凌駕し、市場競争力学を再構築しています。

産業安全と機能安全コンプライアンス重視の高まり

産業界の規制は、安全性の完全性(IEC 61508/61511)とサイバーセキュリティの回復力(IEC 62443)という二重の義務に集約されつつあります。シーメンスのSIBERprotectのようなツールは、安全ループを無傷に保ちながら、危険な資産をミリ秒単位で隔離するため、認証された安全PLCと安全な通信プロトコルが不可欠です。CISAは2024年にOTの脆弱性に関する24の勧告を発表しており、バイヤーは現在、サイバーセーフティ資格を資本計画に織り込んでおり、産業用制御システム市場はネイティブに統合された機能を提供するベンダーへと誘導されています。

熟練したOT/ICSエンジニアの不足

Deloitteは、2033年までに米国の製造業で190万人が未就職になる可能性があり、その多くがITとOTのハイブリッドスキルを必要とすると予測しています。そのためベンダーは、マネージドサービスとローコード設定をバンドルすることで、導入時の摩擦を和らげようとしています。

セグメント分析

SCADAプラットフォームは2024年に産業用制御システム市場の28.7%を占めるが、その集中型アプローチはエッジ対応PLCによって争われつつあり、2030年までのCAGRは11.46%となっています。マイクロAIチップの流入により、PLCは状態監視と品質検査のワークロードをローカルで処理できるようになり、データのバックホールとネットワークの混雑が緩和されます。石油・ガスと化学業界では、分散型制御システムが依然として連続プロセスを管理しているが、顧客は資産の寿命を延ばすために、従来のDCSに予測アルゴリズムを重ねようとしています。ヒューマン・マシン・インターフェースは、現場でのトラブルシューティングのためにARオーバーレイを組み込んだ意思決定支援コンソールへと進化しています。インテリジェント電子デバイスは、グリッドオペレーターがより迅速な故障切り分けを追求する中で、ユーティリティ企業で支持を集めています。これらの使用事例において、オープンAPIを組み込んだサプライヤーは産業用制御システム市場で高く評価され、プラント管理者はベンダーに縛られることなくベスト・オブ・ブリードのコンポーネントを組み合わせることができます。

SCADAが2025年の産業用制御システム市場規模にまだ585億米ドル貢献していることから、アップグレードサイクルの中心は、アナリティクスを注入しながら監視レイヤーをそのまま維持するコンテナベースのマイクロサービスです。一方、ディスクリート製造業のパイロット・プログラムでは、エッジPLCクラスタが計画外ダウンタイムを最大20%削減し、投資回収を加速しています。集中型アーキテクチャと分散型アーキテクチャの両方でライフサイクルサービスを調和させることができるベンダーは、不釣り合いなシェアを獲得すると予想されます。

アセット・パフォーマンス・マネジメントは、プラントが設備全体の有効性とスケジュール不要のメンテナンスを追い求める中、2024年の売上高の23.6%を生み出しました。今後、サイバーセキュリティ・スイートは、OT資産を標的としたランサムウェアの増加への反動から、CAGR12.75%で他のすべてのカテゴリーを上回るとみられています。脆弱性スキャン、ゼロトラスト・セグメンテーション、安全PLCのハードニングを融合させた統合型製品は、製薬会社などのリスクを嫌う部門に支持されています。製造実行システムは現在、品質分析と電子バッチ記録をバンドルしており、製品ライフサイクル管理ツールはデジタル・ツインと連携して設計と製造を橋渡ししています。ERPベンダーは、REST APIを通じてOTデータモデルを公開し、需要主導型の計画アルゴリズムに供給しています。そのため、産業用制御システム市場は、個別のモジュールではなく、クロスドメインデータをオーケストレーションするプラットフォームに傾斜しています。

2030年までに産業用制御システムの市場規模が140億米ドルを超えると予測される産業用サイバー・プラットフォームは、ベンチャー資金を集め、既存ベンダーにニッチな専門家の買収を促しています。APM、MES、サイバーレイヤーを同期させることに長けているサプライヤーは、デジタルトランスフォーメーションのロードマップを一気通貫で実現するパートナーとして自らを位置づけています。

地域分析

欧州は2024年の売上高の28.5%を占めており、厳格な機能安全規制と持続可能性の義務化により、高効率オートメーションが評価されています。Manufacturing-Xのような資金調達スキームは、データ主権を重視するプロジェクトに1億5,000万ユーロ(1億6,100万米ドル)を分配し、国内ベンダーに早期参入の優位性を与えています。資本プロジェクトは、EUのグリーン・ディール報告に合わせて、カーボン・フットプリント・ダッシュボードをバンドルすることが増えています。東欧のクラスターは、欧米OEMのニアショア・キャパシティとして機能し、中位の制御機器に対する需要の増加を刺激しています。

アジア太平洋はCAGR 10.24%で成長し、エレクトロニクス、EV用バッテリー、再生可能部品の大規模な生産能力拡大から恩恵を受ける。中国の人口動態の逆風と賃金インフレが工場の自動化を加速させ、東南アジア諸国は税制優遇措置を活用してリショアリング・プロジェクトを誘致します。国内のPLCとロボットのサプライヤーがシェアを伸ばしているが、ハイエンドの安全性とモーション・ソリューションでは多国籍の既存企業が優位を保っています。中国の重要情報インフラ法を筆頭とする政府のサイバー規制は、バイヤーを検証可能なセキュリティ系統の製品に向かわせ、調達候補リストを形成しています。

北米は、リショアリング・イニシアチブとCHIPS法の2億米ドルのデジタルツイン・プログラムを通じて勢いを維持します。米国メキシコ湾岸におけるエネルギー転換への支出は、LNG、水素、CCS施設を改修するためのオープン・プロセス・オートメーションへの需要を生み出しています。カナダのNGenの3,500万米ドルの持続可能な製造の課題は、モジュラー制御キットの中小企業の採用を推進しています。CISAによるサイバー指令の強化により調達仕様が向上し、IEC 62443認証を持つサプライヤーが有利になります。これらの動向を総合すると、産業用制御システム市場は地域的に多様な成長を続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インダストリー4.0の展開が工場全体の自動化を加速させる

- 産業安全と機能安全コンプライアンス重視の高まり

- リアルタイム・データ主導のマス・カスタマイゼーションに対する需要の急増

- スマート工場の改修に対する政府のインセンティブ

- オープン・プロセス・オートメーション(O-PAS)アーキテクチャの普及(アンダーザレーダー)

- OT-as-a-Service」エッジプラットフォームへのシフト(アンダーザレーダー)

- 市場抑制要因

- 熟練したOT/ICSエンジニアの不足

- 高い設備投資と長い投資回収期間

- 半導体のリードタイム変動がコントローラ供給を混乱させる(アンダーザレーダー)

- レガシーシステム統合の複雑性(アンダーザレーダー)

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- 主要マクロ経済動向の影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場のマクロ経済動向の評価

第5章 市場規模と成長予測

- オペレーション技術別

- 監視制御およびデータ収集(SCADA)

- 分散型制御システム(DCS)

- プログラマブルロジックコントローラ(PLC)

- インテリジェント電子デバイス(IED)

- ヒューマン・マシン・インターフェース(HMI)

- その他システム

- ソフトウェア別

- アセット・パフォーマンス・マネジメント(APM)

- 製品ライフサイクル管理(PLM)

- 製造実行システム(MES)

- 企業資源計画(ERP)

- 産業用サイバーセキュリティ・プラットフォーム

- その他ソフトウェア

- 展開モード別

- オンプレミス

- クラウドベース

- エッジ/ハイブリッド

- エンドユーザー業界別

- 石油・ガス

- 化学・石油化学

- 電力・ユーティリティ

- 飲食品

- 自動車および輸送機器

- ライフサイエンス

- 上下水道

- 金属および鉱業

- 紙・パルプ

- エレクトロニクスと半導体

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Siemens AG

- ABB Ltd.

- Rockwell Automation Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- GE Digital(General Electric Co.)

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Beckhoff Automation GmbH

- Hitachi Ltd.

- Delta Electronics Inc.

- Advantech Co., Ltd.

- Johnson Controls International plc

- Fortinet Inc.(ICS-cybersecurity)

- Palo Alto Networks Inc.(ICS-cybersecurity)

- ICS-Secure LLC