|

|

市場調査レポート

商品コード

1639477

ラテンアメリカの受託包装:市場シェア分析、産業動向、成長予測(2025~2030年)Latin America Contract Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ラテンアメリカの受託包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

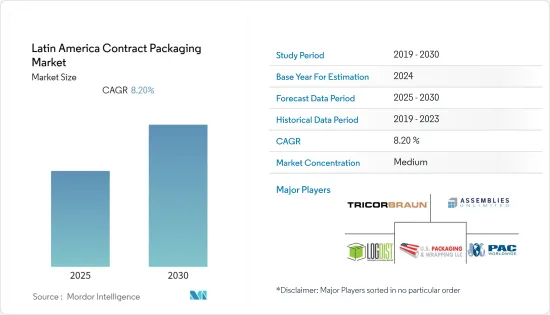

ラテンアメリカの受託包装市場は予測期間中にCAGR 8.2%を記録する見込み

主要ハイライト

- eコマース市場は、パンデミック(世界的大流行)時の規制や社会的距離を置くルールのおかげで急成長しました。その結果、多くの企業が急激な需要の増加に対応するため、エンドツーエンドの包装ソリューションをアウトソーシングするようになりました。

- 最新かつ革新的な包装ソリューションを採用し、コアビジネスに注力する企業の増加もまた、市場の成長を促進すると予想され、企業は最新技術の展開とそれをアップグレードする継続的な必要性で包装インフラをセットアップするために必要な投資を最小限に抑えることができます。

- 医薬品や薬剤がより専門的になるにつれて、専門的な生産の必要性が高まっています。さらに、規制が厳しい包装要件のほとんどで、エンドユーザーは、クライアントの大量の要件を処理するための経験と専門知識を持ち、装備されている包装ベンダーと契約することを好みます。同地域では、医薬品包装に必要な高水準の基準を満たす包装設備を社内に設置できないため、受託包装の需要が増加しています。

- 同地域の製薬産業の成長も市場を牽引する要因のひとつです。製薬会社は、ブラジル、メキシコなどの新興国において、包装業務を第三者に委託しています。さらに、製薬会社に対する価格圧力が高まっていることも、受託包装サービスに対する産業の需要を押し上げています。しかし、エンドユーザー産業による自社包装設備の採用が増加していることが、市場の成長を妨げています。

- COVID-19の大流行により、食品、飲食品、医薬品の需要が増加したため、企業は包装業務を共同包装業者に委託するようになり、この地域の包装受託需要が増加しています。例えば、メキシコシティの主要卸売市場では毎日数件のコロナウイルス感染者が検出され続け、衛生的で安全な包装サービスのニーズが生まれました。さらに、ロシアとウクライナの戦争は、原料やエネルギー価格のコスト上昇により、全体的な包装エコシステムに影響を与えています。

ラテンアメリカの受託包装市場動向

eコマース産業からの需要の増加

- 消費者向け加工品を提供する企業からの要求が変化する中、サプライチェーンのスピードとともに、カスタマイズがeコマースを通じて製品を提供する企業にとっての課題となっており、それによって、柔軟性、敏捷性、臨機応変さを中心に構築されるカスタマイズ型eコマース包装ソリューションに対する受託包装企業からの要求がエスカレートしています。

- 消費者が食料品店で買い物をする頻度は減っており、その結果、買い物客のミッションやバスケットに変化が生じています。eコマースやデジタルチャネルへのシフトは加速しており、消費者のかなりの割合が初めて宅配を試すか、大流行期に宅配を頻繁に利用するようになり、より安全な包装の必要性が高まり、メーカーは包装を第三者ベンダーに委託するようになっています。

- さらに、eコマース企業は、ブラジルなどの国々で現地の荷物配送サービスとの提携を進めており、売上高の増加に対応しています。例えば、2022年11月、AmazonとAzul Cargoは、北ブラジルの航空貨物eコマース荷物の配達をスピードアップするために提携しました。このような提携は、三次包装ソリューションの需要をさらに押し上げると考えられます。

食品産業が著しい成長を遂げる見込み

- 安定性、需要の高まり、契約包装業者に対する食品製造会社の嗜好の変化により、食品会社はコストの最適化と中核事業にますます重点を置くようになっており、需要の高まりにより、そのほとんどが包装とフルフィルメントサービス活動を第三者の契約食品包装業者にアウトソーシングしています。

- 食品販売の増加に伴い、この地域の食品製造企業による投資が増加していることが、市場の成長をさらに後押ししています。例えば、世界の食品企業であるカーギルは、2021年9月にブラジルのベベドゥーロに最先端のペクチン生産施設を新設し、需要増への対応能力を大幅に拡大すると発表しました。

- いくつかの国の政府は、医薬品や食品の表示と包装に関する厳しい法律と規制を実施しており、これが包装受託市場の範囲を広げています。例えば、2022年9月、アルゼンチン政府は最も包括的な食品施策法を発表し、ナトリウム、砂糖、脂肪、カロリーが過剰なレベルの超加工製品には、包装前面に黒い八角形の警告を記載することを義務付けた。

- さらに2022年7月、Buhler、Cargill、GivaudanはFood Tech Hub LATAMとItal Food Technology Instituteと協力し、ブラジルのカンピーナスにTropical Food Innovation Labと呼ばれるイノベーションセンターを建設しました。この新しいハブは、ラテンアメリカにおけるサステイナブル飲食品製品のために開発されました。スタートアップ、企業、投資家、大学、研究機関がプロトタイピング技術にアクセスできます。これにより、ラテンアメリカ食品産業の拡大がさらに進むと考えられます。

ラテンアメリカの受託包装産業概要

ラテンアメリカの受託包装市場は半固定的で競争が激しく、有力な参入企業が市場に進出しています。市場で顕著なシェアを持つこれらの参入企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアを向上させ、収益性を高めるために、戦略的な協力行動を活用しています。

2022年6月:市場力学の変化に伴い、プラスチック包装材料は産業内でコストが上昇する中でも高い需要を維持しています。天候不順、インフラ問題、労働力不足、パンデミックの影響もあり、PETなど広く使用されている包装用樹脂は2021年に50%近い値上がりを記録しました。樹脂包装の生産は、ほとんどのメーカーが輸入原料に頼っており、ポリエチレンやポリスチレンの包装プロジェクトでは短期的な価格緩和は期待できないです。Rabobankのレポートによると、2022年に生産を開始する新工場が2023年にポリエチレン価格を緩和する可能性があります。

さらに、アルミニウム包装産業を妨げている供給ギャップの要因はインフレだけではないです。高い材料費と缶不足の可能性に直面した飲料メーカーは、インフレ圧力が2022年のアルミ飲料包装を複雑にするとして、大規模な包装コストの引き上げに踏み切った。欧州のエネルギー不安は、ガラス包装のコストをも膨張させると予想されます。主要なガラス輸入国であるラテンアメリカユーザーは、エネルギー集約型産業からの価格上昇圧力が続くと予想できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリュー/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業施策

- COVID-19の市場への影響評価

- 世界の受託包装市場概要

第5章 市場力学

- 促進要因

- eコマース産業からの需要増加

- 小売チェーンの開発

- 抑制要因

- 社内包装との競合

第6章 市場セグメンテーション

- サービス別

- 一次包装

- 二次包装

- 三次包装

- エンドユーザー産業別

- 食品

- 飲料

- 医薬品

- 家庭用品・パーソナルケア

- その他

- 国別

- ブラジル

- メキシコ

- アルゼンチン

- その他の国

第7章 競合情勢

- 企業プロファイル

- TricorBraun

- Assemblies Unlimited, Inc.

- VMA LOGDIST

- U.S. Packaging & Wrapping LLC

- PAC Worldwide Corporation

- Rangel

- Colep Consumer Products

第8章 投資分析

第9章 市場の将来展望

The Latin America Contract Packaging Market is expected to register a CAGR of 8.2% during the forecast period.

Key Highlights

- The e-commerce market grew rapidly owing to the restrictions and social distancing rules during the pandemic. It created significant demand, resulting in many businesses outsourcing their end-to-end packaging solutions to meet the sudden increase in demand.

- The increasing focus of companies on adopting the latest and innovative packaging solutions and focus on their core business is also anticipated to foster market growth helping the companies to minimize the investment required to set up packaging infrastructure with the latest technology deployment and the continuous need to upgrade it.

- The need for specialized production has increased as drugs and medications become more specialized. Further, in most of the packaging requirements where the regulations are stringent, the end-users like to engage with packaging vendors who have prior experience, expertise and equipped for handling the volume requirement of the clients. The region has witnessed a rise in demand for contract packaging owing to the inability of in-house packaging facilities to meet high standards needed for pharmaceutical packaging.

- The growing pharmaceutical industry in the region is another factor driving the market. Pharmaceutical companies outsource packaging activities to third parties in emerging countries such as Brazil, Mexico, etc. Further, rising pricing pressure on pharmaceutical companies is boosting the industry's demand for contract packaging services. However, the increasing adoption of in-house packaging facilities by the end-user industries is hampering the market growth.

- Due to the COVID-19 pandemic, there was increased demand for food, beverages, and pharmaceutical drugs, which led companies to outsource their packaging activities to co-packers, thus, increasing the demand for contract packaging in the region. For instance, Mexico City's primary wholesale market continuously detected several coronavirus cases daily, creating the need for hygienic and safe packaging services. Further, the Russia-Ukraine war has an impact on the overall packaging ecosystem with the increased raw materials and energy prices cost.

Latin America Contract Packaging Market Trends

Increasing Demand from E-commerce Industry

- With the changing requirements from the consumer processed goods providing businesses, customization, along with speed in the supply chain, creates a challenge for the product offering companies through e-commerce, thereby escalating the requirements from the contract packaging companies for a customized e-commerce packaging solution, as they are built around flexibility, agility, and resourcefulness.

- Consumers are shopping at grocery stores less frequently, which has resulted in changes in shopper missions and baskets. The shift toward e-commerce and digital channels has accelerated, with a significant proportion of consumers either trying home delivery for the first time or using it more frequently during the pandemic, increasing the need for safer packaging and leading manufacturers to outsource packaging to third-party vendors.

- Moreover, e-commerce companies are undergoing partnerships with local package delivery services in the countries like Brazil to cater to growing sales delivery. For instance, in November 2022, Amazon and Azul Cargo partnered to speed up the delivery of air cargo e-commerce packages in North Brazil. Such partnerships will further boost the demand for tertiary packaging solutions.

Food Industry is Expected to Add Significant Growth

- With the stability, rising demand, and changing preference of food production firms toward contract packagers, and the food companies increasingly focusing on cost optimization and their core business, most of them have been outsourcing their packaging and fulfillment services activities to third-party contract food packagers, owing to the rising demand.

- The growing investment by food manufacturing companies in the region with rising food sales is further augmenting the market growth. For instance, in September 2021, Cargill, a global food corporation, announced the opening of its new, cutting-edge pectin production facility located in Bebedouro, Brazil, to significantly expand the company's ability to meet growing demand.

- Several countries' governments are enforcing strict laws and regulations governing the labeling and packaging of drugs and food products, which is broadening the scope of the contract packaging market. For instance, in September 2022, the government of Argentina announced most comprehensive food policy laws, requiring ultra-processed products with excess levels of sodium, sugar, fats and calories to include black octagonal warnings on the front of the package.

- Moreover, in July 2022, Buhler, Cargill, and Givaudan collaborated with the Food Tech Hub LATAM and Ital Food Technology Institute to build an innovation center called the Tropical Food Innovation Lab in Campinas, Brazil. This new hub is developed for sustainable food and beverage products in Latin America. Startups, companies, investors, universities, and research institutions can access prototyping technologies. This will further add to the expansion of the food industry in Latin America.

Latin America Contract Packaging Industry Overview

The Latin America contract packaging market is semi-consolidated is competitive, with some influential players operating in the market. These players with a noticeable share in the market are concentrating on expanding their customer base across the region. These businesses leverage strategic collaborative actions to improve their market percentage and enhance profitability.

In June 2022: With the changing market dynamics, plastic packaging materials remain in high demand even as costs climb within the industry. Attributed in part to weather events, infrastructure problems, labor shortages, and the pandemic, widely used packaging resins such as PET saw price increases of nearly 50% in 2021. Most of the makers rely on imported materials for resin packaging production, and short-term price relief is not expected for polyethylene and polystyrene packaging projects. The Rabobank report indicates new plants set to begin production in 2022 may ease polyethylene prices in 2023.

Moreover, Inflation isn't the sole factor for the supply gap that has thwarted the aluminum packaging industry, but the cost of the familiar material is up 40% over the past two years. Faced with high materials costs and the possibility of can shortages, beverage producers have taken massive packaging cost increases as inflationary pressure complicates aluminum beverage packaging in 2022. Energy uncertainty in Europe is expected to inflate the cost of glass packaging, as well. As a major glass importer, the users in Latin America can expect continued upward pricing pressure from the energy-intensive industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industrial Value/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's 5 Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers/Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Policies

- 4.5 Assessment of COVID-19 Impact on the Market

- 4.6 Overview of Global Contract Packaging Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increasing Demand from E-commerce Industry

- 5.1.2 Development in the Retail Chain

- 5.2 Restraints

- 5.2.1 Competition from In-house packaging

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Primary Packaging

- 6.1.2 Secondary Packaging

- 6.1.3 Tertiary Packaging

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverages

- 6.2.3 Pharmaceutical

- 6.2.4 Household and Personal Care

- 6.2.5 Other End-user Industries

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Mexico

- 6.3.3 Argentina

- 6.3.4 Other Countries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TricorBraun

- 7.1.2 Assemblies Unlimited, Inc.

- 7.1.3 VMA LOGDIST

- 7.1.4 U.S. Packaging & Wrapping LLC

- 7.1.5 PAC Worldwide Corporation

- 7.1.6 Rangel

- 7.1.7 Colep Consumer Products