|

市場調査レポート

商品コード

1639456

テレコムアナリティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Telecom Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| テレコムアナリティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

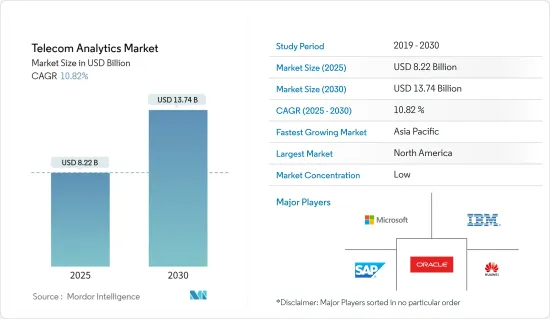

テレコムアナリティクス市場規模は、2025年に82億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.82%で、2030年には137億4,000万米ドルに達すると予測されます。

一般に既存事業者よりも安価で有利な契約を提供する新規参入事業者の出現により競合が激化しているため、解約を減らす必要性はこれまで以上に高まっています。さらに、非構造化データと構造化データの量が増加しているため、顧客の行動や嗜好についてより深い洞察を得るための効果的な分析が必要とされています。リアルタイムのサービス利用パターンが、こうした企業が分析を導入する動機となっています。

主要ハイライト

- 電気通信分析市場は、電気通信産業の複雑な要求を満たす様々な洗練されたビジネスインテリジェンス(BI)技術を組み合わせています。これには、売上開発、解約や偽装の削減、リスク管理の強化、運用コストの削減などが含まれます。そのため、電気通信事業者は、関連データのみをより迅速かつシンプルに処理するための先進的分析主導型データソリューションを採用し、データマイニングや予測分析などのネットワーク分析を使ってタイムリーで正確な洞察を得られるよう支援しています。

- さらに、通信産業は新たな時代を迎え、消費者ではなく企業という新たな顧客フォーカス、5Gやクラウドの新技術、分析やデータサイエンスを活用した俊敏で迅速なサービスを提供するための根本的に新しい働き方へのニーズが高まっています。2023年1月現在、GSAの報告によると、世界中で243の商用5Gが展開されており、112の事業者がスタンドアロン5Gに投資しています。この商用化は、新たなB2BとB2B2Xアプリケーションにつながります。その際、通信事業者は、単に容量を拡大したり、サービスレベルやリソースを柔軟に変更したりするだけでなく、これらの顧客に確実にサービスを提供できるようにする必要があります。

- 例えば、2023年2月、Oracle Corporationは、当社のNetwork Analyticsポートフォリオの2番目のアプリケーションであるOracle Network Analytics Data Directorをリリースすると発表しました。このアプリケーションにより、事業者は、Oracleが提供していないネットワーク機能についても、5Gコアを既存の運用ツールに柔軟に統合できるようになります。Oracle Communications Network Analytics Data Directorは基本的に、SCP(Service Communication Proxy)やNRF(Network Repository Function)といったOracleの5Gネットワーク機能など、さまざまなソースからトラフィックを取り込み、加入者アプリケーションに配信します。

- 世界中でモバイルユーザーが多いため、テレコムアナリティクスサービスはクラウド上でホスティングされることが予想されます。したがって、クラウドホスティングもまた、消費者ベースの継続的な増加により、さらに拡大すると見られています。そのため、通信サービスプロバイダー(CSP)によるこの技術の採用は著しく伸びています。

- テレコムアナリティクスは、通信サービスプロバイダー(CSP)の生産性向上、顧客満足度の向上、収益拡大に貢献しています。例えば、NokiaのNokia AVA分析と洞察は、多くの主要通信企業の市場測定製品の再構築を支援しました。ティア1のサービスプロバイダーであるPOST Luxembourgは、Nokia AVAを使用して、加入者に影響が及ぶ前にネットワーク問題の97%をプロアクティブに特定し、解決しました。さらに、Hutchison 3 Indonesiaはネットワークのスペクトル効率を17%改善しました。さらに、Vodafoneは、異常を検出して根本原因分析の自動化を支援するベルラボの機械学習アルゴリズムを使用することで、ネットワーク問題を最大30%迅速に解決しています。

- データインフラの改善により、通信産業では分析の利用が可能になり、データが豊富な通信事業者は、ビジネスを変革するための有意義なインテリジェンスを得ることができます。テレコムアナリティクスでは、支出やプランに関連する顧客データと、インターネット利用やネットワーク活動時間などの行動データを統合して分析することができます。

- スマートデバイスの普及とIPネットワークの利用の増加により、通信産業では通信詐欺が再燃しています。攻撃はどこからでもやってくるため、詐欺は通信市場にとって最も厄介な問題として浮上しています。このため、当局は通信セクターの安全のために規制を開始しています。インドでは、Telecom Regulatory Authority of India(インド電気通信規制局)が、音声品質の基準を満たさない場合に厳しい規則と罰則を設けています。これにより、同国ではネットワーク分析ソリューションの需要が高まると予想されます。

- COVID-19パンデミックの流行中、通信分析の利用は全体的に拡大しました。在宅勤務が可能になったことによるブロードバンドへのプレッシャーの増加、オンラインストリーミングプラットフォームの台頭、内部プロセスの可視性の向上、テレコム分析による必要不可欠なオペレーションなどの要因により、テレコム分析の需要は活発な封鎖期間中に拡大しました。

テレコムアナリティクス市場動向

解約削減ニーズの急増

- 電気通信セグメントでは、解約とは、あらかじめ決められた期間内にサービスプロバイダーを変更する加入者の割合と定義できます。この割合が年々増加すると、企業ブランドが損なわれるため、企業は解約率の低下に力を入れています。これは、企業の将来の売上やビジネスに悪い影響を与えます。krtrimaiqによると、米国で最も解約率が高いのはニュージャージー州とカリフォルニア州です。

- テレコムアナリティクスを使うことで、解約率を15%削減しました。テレコムサービスプロバイダーは、収益損失を防ぎ、顧客サービスを強化し、マーケティングや販売経費を節約するために、顧客解約分析ソリューションを求めています。加入者分析ソリューションを導入することで、加入者は加入者の利用データから幅広く学び、加入者の行動パターンを特定し、顧客体験を向上させることができます。さらに、通信事業者はクロスセルやアップセルを行うことができます。

- テレコムアナリティクスは、テレコム企業に顧客概要を提供し、最も収益性の高い顧客、最も収益性の低い顧客などを特定できるようにするため、非常に重要です。同時に、顧客関係(購入、更新、問題)の進化を追跡し、各顧客がカスタマージャーニーのどの段階にあるかを確認することもできます。

- さらに、テレコムアナリティクスの利点の1つは、顧客管理において、すべての顧客データが1つのシステムに安全に保存され、いつでもアクセスできることです。後の分析のために、各消費者の詳細を収集する一貫した方法を持つことが重要だからです。

- さらに、Bharti Airtel、Reliance Jio、Vodafoneなどの携帯電話会社は、人工知能を使用して、顧客サービスのタッチポイントのコールセンターやネットワークの提供を通じて顧客体験を向上させ、加入者の定着率を向上させ、解約を減らす方法を見つけようとしています。

- さらに、この市場の各社は、態度を理解するための機械学習を組み込んだ通信分析ソリューションを提供しており、通信事業者がリスクのある加入者や、現在と将来の解約の原因を特定できるようにしています。その結果、事業者は離反を減らすためのマーケティングや顧客サービス施策を展開しています。さらに、データプランのアップグレードの準備が整った加入者や、新サービスの見込み客を発見することもできます。電気通信セグメントでは、解約分析によって、顧客がキャリアやサービスプロバイダーを変更する時期を予測することも可能です。

- 電気通信セグメントの顧客は、さまざまなサービスプロバイダーから選択することができ、事業者間で積極的に乗り換えることができます。このような競争の激しい市場において、電気通信セクターの年間平均解約率は15~25%です。既存顧客を維持するよりも新規顧客を獲得する方が5~10倍もコストがかかるため、顧客維持の重要性は今や顧客獲得を上回っています。収益性の高い消費者を維持することは、多くの既存事業者にとって最大の事業目標です。通信事業者は、顧客離れを減らすために、最も離脱する可能性の高い消費者を特定しなければならないです。

- Vodafoneの2021/2022会計年度の第1四半期におけるドイツのプリペイド解約率は11.3%でした。Vodafoneのプリペイド顧客の解約率が最も高いのは英国(英国)で、解約率は91.9%です。これらの地域では解約率が高いため、解約率削減のニーズが大きく高まっています。

北米が最大の市場シェアを占める

- 北米は、主にビジネスインテリジェンスソリューションへの支出が多いことから、電気通信分析市場で大きな市場シェアを占めると予想されています。また、同地域の通信は高度に発達しており、通信事業者間の競争も激しいことから、同地域の通信分析市場はさらに活性化すると予想されます。

- カスタマーサポートに使用されるITインフラと技術の継続的な進歩、多数の市場ベンダーの存在、最新のカスタマーエクスペリエンスとヘルプデスクソフトウェアを管理するための熟練した技術的専門知識の利用しやすさが、この地域におけるテレコム分析市場の成長に寄与しています。さらに、北米企業は戦略的M&Aを積極的に行っています。例えば、アメリカの技術大手IBMは、クラウドサービスを強化するためにSanovi Technologiesを買収しました。Sanoviは、企業のデータセンターとクラウドインフラ向けに、クラウド移行、事業継続、ハイブリッドクラウドリカバリーソフトウェアを提供しています。

- さらに、BYOD施策はおそらく米国におけるタブレットやスマートフォンの人気の高まりに後押しされています。例えば、米国国勢調査局と消費者技術協会は2022年1月、米国におけるスマートフォンの売上高が2021年の730億米ドルから2022年には747億米ドルに増加すると予測しています。これは、多数の部門や企業でIoTが急速に採用されるにつれて、さらに増加すると予想されます。したがって、スマートフォンユーザーの増加に伴い、詐欺や詐欺の確率も増加しており、これがこの通信分析市場の成長を飛躍的に促進しています。

- 北米には世界最大級の携帯電話サービスプロバイダーが数社あり、消費者からのフィードバックに大きく依存しています。このため、同地域のCSPはテレコムアナリティクスを選ぶことで、より質の高いサービスを高い効率で提供することができます。例えば、米国の通信プロバイダーであるVerizonは、社内に様々な分析ソリューションとAIグループを配備しています。一方、データサイエンスとコグニティブインテリジェンス・グループは、Verizonの顧客対応に分析とコグニティブ技術を導入することに注力しています。他のベンダーも同様の取り組みに注力するようになっており、この地域における通信分析ソリューションの需要を押し上げると考えられます。

- さらに、同国におけるインターネット普及を支援するための政府の取り組みや投資の増加は、通信分析市場の需要を高めると考えられます。例えば、米国農務省(USDA)は2022年7月、11州の企業と3万1,000人の農村住民に高速インターネットアクセスを提供するため、4億100万米ドルを投資すると発表しました。これは、手頃な価格の高速インターネットと地方のインフラへの投資に対する米国政府のコミットメントの一環です。

- Stormforgeが2021年4月に発表した調査結果では、北米の回答者の18%が、自社のクラウドコンピューティングに毎月10万米ドルから25万米ドルを費やしていると回答しています。また、回答者の32%は、今後12ヶ月間に自社のクラウド支出が大幅に拡大すると予測しており、44%は同期間にクラウド支出がわずかに増加すると予測しています。さらに、2022年に実施されたStatista Global Consumer Surveyの調査によると、回答者の44%がファイルや画像にオンラインストレージを使用し、回答者の40%がオフィス文書の作成にオンラインアプリケーションを使用していることが判明しています。このようなクラウドサービスへの高額支出の動向は、同地域の通信分析市場の成長を促進すると考えられます。

テレコムアナリティクス産業概要

テレコムアナリティクス市場は非常に競争が激しく、現在多くの参入企業によって構成されているため、細分化された段階に移行しています。世界のテレコムアナリティクス市場の主要企業数社は、製品の進歩をもたらすために絶え間ない努力を続けています。著名な企業数社は、市場での地位を固めるため、提携を結んだり、新興国市場での拠点を拡大したりしています。主要企業はHuawei Technologies、SAP SE、Oracle Corp.です。

- 2023年3月-IBM Corporationは、Telecom Egypt(TE)にインテリジェントオートメーションソフトウェアを提供し、モバイル、固定、コアネットワーク上のすべてのオペレーションサポートシステム(OSS)を包括するソリューションを導入すると発表しました。Telecom EgyptはRedHat OpenShift上に展開されたIBM Cloud Pak for Watson AIOpsを採用し、IBM Robotic Process Automation(RPA)ソリューションを実装します。このソリューションにより、TEはIT環境全体を俯瞰できるようになり、技術革新の迅速化、運用コストの削減、ネットワーク関連のインシデントのトラブルシューティングと解決にかかる時間の最小化を実現できます。

- 2023年2月-Bharti Airtelは、同社のコンタクトセンターにかかってくるすべてのインバウンドコールの全体的な顧客体験を向上させるために、NVIDIAと協力してAIベースのソリューションを構築すると発表しました。同社はコンタクトセンターにかかってくる電話の84%に自動音声認識アルゴリズムを適用しています。これにより、同社は消費者と対話する際にエージェントの改善点を特定し、より良い顧客体験につなげることができます。同社はNVIDIANeMo会話AIツールキットを活用して、この特殊な音声アプリケーションとNVIDIA AIエンタープライズソフトウェアスイートを開発しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が市場に与える影響

- 市場力学

- 解約削減ニーズの急増

- 不正行為に対する脆弱性の増大

- 市場抑制要因

- 通信事業者の認識不足

第5章 市場セグメンテーション

- 用途別

- 顧客分析

- ネットワーク分析

- 市場分析

- 価格分析

- サービス分析

- その他

- 展開別

- クラウド

- オンプレミス

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他のアジア太平洋

- その他

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Oracle Corporation

- IBM Corporation

- SAP SE

- Microsoft Corporation

- InfoFaces Inc.

- Accenture PLC

- Huawei Technologies Co. Ltd

- Teradata Corporation

- Wipro Limited

- Nokia Corporation

第7章 投資分析

第8章 市場機会と今後の動向

The Telecom Analytics Market size is estimated at USD 8.22 billion in 2025, and is expected to reach USD 13.74 billion by 2030, at a CAGR of 10.82% during the forecast period (2025-2030).

The need for reducing churn is more important than ever, as the competition is increasing with the incidence of new entrants, who provide lucrative deals that are generally inexpensive than the incumbents. In addition, the increasing amount of unstructured and structured data requires effective analysis to get more profound insights into customer behavior and preferences. Real-time service usage patterns motivate these companies to adopt analytics.

Key Highlights

- The telecom analytics market combines various sophisticated business intelligence (BI) technologies that satisfy the complex demands of the telecom industry. These include developing sales, reducing churn and deception, enhancing risk management, and decreasing operational costs. Hence, telecom organizations are adopting advanced analytics-driven data solutions for faster and simpler processing of only relevant data, helping them achieve timely and accurate insights using network analytics such as data mining and predictive analytics.

- Moreover, the telecommunications industry is entering a new era and increasing need for a new customer focus - enterprises instead of consumers, new technologies in 5G and the cloud, and fundamentally new ways of working to deliver agile, faster services using analytics and data science. As of January 2023, the GSA reports that there are 243 commercial 5G deployments worldwide, with 112 operators investing in standalone 5G. This commercialization will lead to new B2B and B2B2X applications. In doing so, operators need to ensure that they can serve these customers beyond simply expanding capacity or flexibly changing service levels and resources.

- For instance, in February 2023, Oracle Corporation announced to release the second application in our Network Analytics portfolio, the Oracle Network Analytics Data Director which enables operators to flexibly integrate their 5G core into their existing operational tools, even for network functions that are not provided by Oracle. Oracle Communications Network Analytics Data Director basically ingests traffic from various sources such as Oracle 5G network functions such as Service Communication Proxy (SCP) and Network Repository Function (NRF) and distributes it to subscriber applications.Both incoming and outgoing data are encrypted, allowing users to guarantee end-to-end data transfer.

- Telecom analytics service is expected to be hosted on the cloud because of the large number of mobile users worldwide. Hence, cloud hosting is also set to expand further due to the continuous rise in the consumer base. Thus, the adoption of this technology by communications service providers (CSPs) is growing significantly.

- Telecom analytics has been helping communications service providers (CSPs) to boost productivity, enhance customer satisfaction, and grow revenues. For instance, Nokia Corporation's Nokia AVA analytics and insights helped many leading telecom companies re-engineer their market measurement products. POST Luxembourg, a Tier-1 service provider, used Nokia AVA to proactively identify and solve 97% of network issues before they could affect subscribers. Moreover, Hutchison 3 Indonesia improved the spectral efficiency of its network by 17%. Additionally, Vodafone solves network issues up to 30% faster by using Bell Labs machine learning algorithms that detect anomalies and help automate root cause analysis.

- The improvements in data infrastructure have enabled the use of analytics in the telecom industry, owing to which data-rich carriers can yield meaningful intelligence to transform their businesses. Telecom analytics allows pages to merge and analyze customer data related to spending and plans and behaviour data like internet usage or duration of networking activities.

- Due to the proliferation of smart devices and the increasing use of IP networks, the telecom industry is experiencing a resurgence of communications fraud. As attacks can come from any source, scam has emerged as the most troublesome problem for the telecom market. Due to this, authorities are initiating regulations for the telecoms sector safety. In India, the Telecom Regulatory Authority of India has issued stringent rules and penalties for failing to meet the voice quality benchmark. It is expected to increase the demand for network analytics solutions in the country.

- During the COVID-19 pandemic outbreak, the overall utilization of telecom analytics has expanded. Due to the factors like the increased pressure on broadband caused by the ability to work from home, the rise in online streaming platforms, improved visibility of internal processes, and essential operations by telecom analytics, the demand for telecom analytics has grown during the active lockdown period.

Telecom Analytics Market Trends

The surge in need for churn reduction

- In the context of the telecom sector, churn can be defined as the percentage of subscribers who switch service providers within a predetermined time frame. Companies are putting a lot of effort into lowering churn since if the percentage increases year over year, it damages the company's brand. This badly impacts future sales and business for the corporation. According to krtrimaiq, New Jersey and California have the highest churn percentage in the US.

- By using telecom analytics, it cut churn by 15%. Telecom service providers demand customer churn analytics solutions to prevent revenue loss, enhance customer service, and save marketing and sales expenses. By implementing telecom analytics solutions, carriers can learn extensively from subscriber usage data to identify subscriber behavior patterns and enhance customer experiences. Additionally, it gives telecom providers the ability to cross-sell and up-sell.

- Telecom analytics is very important as it gives telecom companies an overview of their customers and allows them to identify the most profitable, least profitable, etc. At the same time, it also allows tracking the evolution of customer relationships (purchases, renewals, issues) and seeing where each customer is in the customer journey.

- Furthermore, one of the benefits of telecom analytics is in customer management all customer data is securely stored in one system and can be accessed at any time. As it's important to have a consistent way to collect details about each consumer for later analysis.

- Moreover, mobile phone companies such as Bharti Airtel, Reliance Jio, and Vodafone are using artificial intelligence to enhance customer experience through their customer service touchpoints call centers, and network offerings and try to find ways to improve subscriber stickiness and reduce churn.

- Additionally, companies in the market are providing telecom analytics solutions laced with machine learning to understand attitudes, enabling carriers to identify at-risk subscribers or the causes of current and prospective churn. As a result, businesses are developing marketing or customer service initiatives to reduce turnover. Additionally, it can spot subscribers ready for data plan upgrades and prospective customers for new services. In the telecom sector, churn analytics also makes it possible to predict when customers will likely transfer carriers or service providers.

- Customers in the telecom sector have a variety of service providers to select from, and they can actively switch between operators. The telecoms sector has an average annual churn rate of 15 to 25 percent in this fiercely competitive market. Customer retention has now surpassed customer acquisition in importance since it is 5-10 times more expensive to gain new customers than to keep existing ones. Retaining highly profitable consumers is the top business objective for many established operators. Telecom businesses must identify the consumers who are most likely to leave to reduce customer turnover.

- In the first quarter of Vodafone's financial year 2021/2022, the prepaid churn rate in Germany was 11.3 percent. Vodafone has the highest churn rate among its prepaying customers in the United Kingdom (UK), where the churn rate is 91.9 percent. Since the churn rate is higher in these regions, the need for churn reduction is growing significantly.

North America to Hold the Largest Market Share

- North America is anticipated to occupy a significant market share in the telecom analytics market, primarily owing to the region's high expenditure on business intelligence solutions. Besides, telecommunications in the region is highly developed with intense competition among the communication providers, which is expected further to boost the region's telecom analytics market.

- The continuous advancements in IT infrastructure and technology used for customer support, the presence of a large number of market vendors, and the accessibility of proficient technical expertise in managing the modern customer experience and helpdesk software contribute to the telecom analytics market growth in the region. Furthermore, North American companies actively make strategic mergers and acquisitions. For instance, American technology giant IBM acquired Sanovi Technologies to bolster its cloud offerings. Sanovi provides cloud migration, business continuity, and hybrid cloud recovery software for enterprise data centres and cloud infrastructure.

- Moreover, the BYOD policy is probably driven by the growing popularity of tablets and smartphones in the US. For instance, the US Census Bureau and Consumer Technology Association predicted in January 2022 that sales of smartphones in the US would rise from USD 73 billion in 2021 to USD 74.7 billion in 2022. This is anticipated to increase further with the quick adoption of IoT across numerous sectors and companies. Hence, with the rise of smartphone users, the probability of fraud or scams is also increasing, which in turn is fueling the growth of this telecom analytics market exponentially.

- North America has a few of the world's largest cellular service providers, who rely enormously on consumer feedback. Thus, by opting for telecom analytics, CSPs in the region can offer better quality service at high efficiency. For instance, Verizon, a telecommunications provider in the United States, has deployed various analytic solutions and AI groups around the company. On the other hand, the Data Science and Cognitive Intelligence group focus on implementing analytics and cognitive technology in Verizon's customer interactions. The increased focus of other vendors in order to follow the same would boost the demand for telecom analytics solutions in the region.

- Furthermore, the rising government initiative and investment to support the internet penetration in the country will increase the demand for telecom analytics market. For instance, in July 2022, the United States Department of Agriculture (USDA) has announced a USD 401 million investment to bring high-speed Internet access to businesses and 31,000 rural residents in 11 states. This is part of the US government's commitment to investing in affordable high-speed internet and rural infrastructure.

- In a research study released by Stormforge in April 2021, 18% of respondents from North America claim that their firm spends between $100,000 and $250,000 per month on cloud computing. In addition, 32% of respondents predict that their organization's cloud spending will expand significantly over the following 12 months, while 44% predict a slight increase in cloud spending over the same period. Additionally, as per the research study by Statista Global Consumer Survey conducted in the United States in 2022, it has been found that 44 percent of respondents use online storage for files and pictures, while 40 percent of respondents use online applications to create office documents. This trend of high spending on cloud services will drive the growth of the telecom analytics market in the region.

Telecom Analytics Industry Overview

The Telecom Analytics Market is very competitive and moving towards the fragmented stage as the market currently consists of many players. Several key players in the global telecom analytics market are in constant efforts to bring product advancements. A few prominent companies are entering into collaborations and expanding their footprints in developing regions to consolidate their positions in the market. The major players are Huawei Technologies, SAP SE, and Oracle Corp.

- March 2023- IBM Corporation announced to provide intelligent automation software to Telecom Egypt (TE) to implement an umbrella solution for all its operations support systems (OSS) on mobile, fixed, and core networks. Telecom Egypt will adopt IBM Cloud Pak for Watson AIOps deployed on RedHat OpenShift to implement an IBM Robotic Process Automation (RPA) solution. The solution provides TE with a holistic view of its entire IT environment to help them innovate faster, reduce operating costs, and minimize the time to troubleshoot and resolve network-related incidents.

- February 2023- Bharti Airtel announced to build an AI-based solution by collaborating with NVIDIA to improve the overall customer experience for all inbound calls to its contact center. The company runs an automated speech recognition algorithm on 84% of its calls coming into its contact centers. This will help the company identify improvement areas for the agent when interacting with the consumers, leading to a better customer experience. The company has leveraged the NVIDIANeMo conversational AI toolkit to develop this specialized speech application and NVIDIA AI enterprise software suite.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Market Insights

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Covid-19 on the Market

- 4.5 Market Dynamics

- 4.5.1 The surge in need for churn reduction

- 4.5.2 Increasing Vulnerability to Fraudulent Activities

- 4.6 Market Restraints

- 4.6.1 Lack of Awareness Among Telecom Operators

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Customer Analytics

- 5.1.2 Network Analytics

- 5.1.3 Market Analytics

- 5.1.4 Price Analytics

- 5.1.5 Service Analytics

- 5.1.6 Other Applications

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Latin America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Oracle Corporation

- 6.1.3 IBM Corporation

- 6.1.4 SAP SE

- 6.1.5 Microsoft Corporation

- 6.1.6 InfoFaces Inc.

- 6.1.7 Accenture PLC

- 6.1.8 Huawei Technologies Co. Ltd

- 6.1.9 Teradata Corporation

- 6.1.10 Wipro Limited

- 6.1.11 Nokia Corporation