|

市場調査レポート

商品コード

1639446

南米の塗料およびコーティング:市場シェア分析、産業動向、成長予測(2025~2030年)South America Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の塗料およびコーティング:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

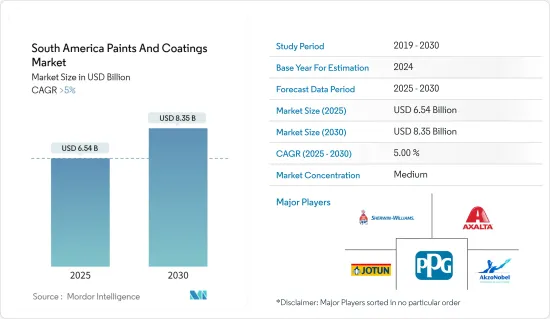

南米の塗料およびコーティング市場規模は2025年に65億4,000万米ドルと推定・予測され、予測期間中(2025-2030年)のCAGRは5%を超え、2030年には83億5,000万米ドルに達すると予測されます。

COVID-19パンデミックは南米の塗料およびコーティング産業に悪影響を与えました。最初の影響に続き、多数の工場や建設現場が閉鎖されたため、業界は需要の減少に見舞われました。その結果、塗料およびコーティングの生産が減少し、サプライチェーンが混乱しました。現在、市場はパンデミックから回復しています。市場は2022年にパンデミック以前の水準に達し、今後数年間は緩やかなペースで成長すると予想されます。

主なハイライト

- 市場を牽引する主な要因は、同地域における建設業界の成長と自動車セクターからの需要の増加です。

- VOCフリー材料の使用に関する厳しい規制が市場成長の妨げになると予想されます。

- バイオベースの塗料およびコーティングの需要の増加と、この地域における航空宇宙セクターの存在感の高まりは、市場に成長機会をもたらすと予想されます。

- 南米では建築分野が市場のエンドユーザー分野を支配しています。

南米の塗料およびコーティング市場動向

建築用塗料およびコーティングが市場を独占

- 建築用塗料およびコーティングは、塗料およびコーティング業界において圧倒的に大きなセグメントです。建築用塗料は表面の保護と装飾を目的としています。建築物や住宅の塗装に使われます。その多くは、屋根用、壁用、デッキ用など、特定の用途に指定されています。どのような用途であっても、建築塗料には一定の装飾性、耐久性、保護機能が求められます。

- 建築用塗料は、オフィスビル、倉庫、コンビニエンスストア、ショッピングモール、住宅などの商業施設に使用されます。このような塗料は外面や内面に塗布され、シーラーや特殊製品も含まれます。

- ブラジルは南半球で最も大きな国のひとつであり、最近ではさまざまな建設プロジェクトに対する投資が増加しています。

- 2023年8月、ブラジルはNovo Programa de Aceleracao do Crescimento(Novo PAC)を策定し、2023年から2026年の間に3,450億米ドルを国内の様々なインフラや建物の建設に投資することを計画しました。

- 同地域では、商業建設に顕著な変化が見られます。2023年に開始されたブラジルのパウリニア・データセンターやポルト・アレグレ・データセンターiのような注目すべきプロジェクトは、この地域で最大級のものです。

- 南米のいくつかの国では、増加する人口のために住宅をより手頃な価格にする取り組みを展開しています。例えば、ブラジルは2023年2月、低所得者を対象とした全国的な連邦住宅プログラムを再開しました。2023年10月、世界銀行はエクアドルに対し、手頃な価格で弾力性のある住宅を強化することを目的とした1億米ドルの融資パッケージを承認しました。

- この地域のこうした動向は、予測期間中の建築用塗料の成長に寄与するとみられます。

市場を独占するブラジル

- ブラジルは、自動車産業と建設産業が確立しており、産業部門への投資が活発であることから、予測期間中、同地域で優位を占めると予想されます。

- OICAによると、同国の2022年の自動車生産台数は237万台で、前年比約5%の成長を記録しました。OICAによると、2022年のブラジル国内の自動車総販売台数は183万台で、2021年の186万台と比較して約1.9%の減少を記録しました。

- 乗用車、小型商用車、大型商用車の2022年の販売台数は、車両コストの上昇により減少しました。しかし、バス・客車の販売台数は2022年に23.4%を占め、自動車分野で最も高い成長を記録しました。

- しかし、ブラジルは南米最大の電気自動車市場を有しています。1月中旬、ブラジルの憲法・司法委員会(CCJ)は、2030年1月以降、国内でガソリン車とディーゼル車の新車販売を禁止する法案を承認しました。ブラジルでは2030年までに約70万台のEVが流通すると予想されています。

- さらに、ブラジルの建設業界は2023年3月も低調で、活動量と雇用者数は5カ月連続で減少しました。しかし、ブラジル建設産業会議所(CBIC)の支援を受けた全国産業連盟(CNI)の最新データによると、活動の落ち込みは深刻ではなく、広範囲に及んでいます。さらに、2023年2月から3月にかけての活動減少は、2022年11月に始まった一連の減少の中で最も穏やかなものです。

- 活動の減少は、エネルギー価格と建設資材価格の高騰、インフレ圧力の高騰、高金利、需要水準の低下、過剰な家計負債に起因しています。2023年3月の建築活動指数は49.5で、5ヵ月連続で50を下回った。2月は47.6、1月は45.9でした。

- ブラジルの家具産業は過去3年間着実に成長しており、最近は新しいデザインの家具の需要が高いです。

- ブラジルは世界第6位の家具生産国であり、多くのブラジルの家具会社やデザイナーは、生産、出荷、配送をスピードアップする革新的なソリューションに投資してきました。こうした努力の結果、家具の輸出は2020年から2021年にかけて50.9%増加し、家具産業におけるブラジルの輸出の35%は特にアメリカの店舗向けとなっています。

- ブラジル家具製造業者協会(ABIMOVEL)によると、ブラジルの家具産業は19,000社で形成されており、その80%はサンパウロ州を筆頭にリオ・グランデ・ド・スル州、ミナス・ジェライス州、パラナ州、サンタ・カタリーナ州の南・南東部に集中しています。

- IEMI Inteligencia de Mercadoによると、ブラジルの家具生産台数は2021年の4億500万台に対し、2022年には3億6,700万台を超えます。しかし、ブラジルの家具生産額は、2021年の680億4,000万ブラジルレアルに対し、2022年は約650億ブラジルレアルでした。

- したがって、建設、インフラ、自動車セクターの成長に伴い、塗料およびコーティング剤の需要は今後数年間で成長すると予想されます。

南米の塗料およびコーティング産業概要

南米の塗料およびコーティング市場は部分的に統合されています。主要企業(順不同)には、PPG Industries, Inc.、Akzo Nobel N.V.、Jotun、Axalta Coating Systems、The Sherwin William Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 地域における建設産業の成長

- 自動車分野での用途と利用の増加

- その他の促進要因

- 抑制要因

- VOC排出に関する厳しい環境規制

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 樹脂タイプ別

- アクリル

- エポキシ

- アルキド

- ポリエステル

- ポリウレタン

- その他の樹脂(ポリプロピレンなど)

- テクノロジー別

- 水性

- 溶剤系

- パウダーコーティング

- UV硬化型コーティング

- エンドユーザー産業別

- 建築

- 自動車

- 木材

- 工業

- その他のエンドユーザー産業

- 地域別

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Akzo Nobel N.V.

- Axalta Coating Systems

- BASF SE

- Hempel

- Jotun

- Lanco Paints

- PPG Industries, Inc.

- Renner Herrmann S.A.

- The Sherwin William Company

- WEG Coatings

第7章 市場機会と今後の動向

- バイオベースおよびエコフレンドリー塗料およびコーティングの需要増加

- 航空宇宙分野における成長機会

The South America Paints And Coatings Market size is estimated at USD 6.54 billion in 2025, and is expected to reach USD 8.35 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the South American paints and coatings industry. Following the initial impact, the industry has experienced a decline in demand due to the shutdown of numerous factories and construction sites. Consequently, paint and coating production declined and disrupted the supply chain. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow at a moderate pace in the coming years.

Key Highlights

- Major factors driving the market studied are the growing construction industry in the region and the increasing demand from the automotive sector.

- It is anticipated that stringent regulations on using VOC-free materials are expected to hinder market growth.

- The increasing demand for bio-based paints and coatings and the growing presence of the aerospace sector in the region are expected to provide growth opportunities in the market.

- The architectural sector dominated the end-user segment of the market in South America.

South America Paints and Coatings Market Trends

Architectural Paints and Coatings to Dominate the Market

- Architectural paints and coatings are by far the largest segment in the paints and coatings industry. Architectural coatings are meant to protect and decorate surface features. They are used to coat buildings and homes. Most are designated for specific uses, such as roof coatings, wall paints, or deck finishes. No matter its use, each architectural coating must provide certain decorative, durable, and protective functions.

- Architectural coatings are used in applications for commercial purposes, such as office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings. Such coatings can be applied on outer surfaces and inner surfaces and include sealers or specialty products.

- Brazil is one of the largest countries in the South that has seen a rise in investments for various construction projects in recent times.

- In August 2023, Under the Novo Programa de Aceleracao do Crescimento (Novo PAC), the government planned to invest USD 345 billion between 2023 and 2026 in the construction of various infrastructure and buildings in the country.

- The region is witnessing a notable shift in its commercial construction landscape. Notable projects like the Paulinia Data Center and Porto Alegre Data Center I of Brazil, initiated in 2023, are among the largest in the region.

- Several South American nations are rolling out initiatives to make housing more affordable for their growing populations. For Instance, in February 2023, Brazil relaunched its nationwide federal housing program, targeting low-income individuals. In October 2023, the World Bank approved a USD 100 million financing package for Ecuador, specifically aimed at bolstering affordable and resilient housing.

- Such trends in the region are expected to contribute to the growth of architectural coatings during the forecast period.

Brazil to Dominate the Market

- Brazil is expected to dominate in the region during the forecast period due to the presence of established automotive and construction industries and investments in the industrial sector.

- As per OICA, the production of automobiles in the country amounted to 2.37 million units in 2022, registering a growth of around 5% compared to the previous year. As per OICA, the total sales of vehicles in the country amounted to 1.83 million units in Brazil in 2022, as compared to 1.86 million units in 2021, registering a decline of around 1.9%.

- Passenger cars, light commercial vehicles, and heavy commercial vehicles witnessed a decline in 2022 sales in the country owing to the growing cost of vehicles. However, bus and coach sales registered the highest growth in the automotive segment, accounting for 23.4% in 2022.

- However, Brazil has the largest electric vehicle market in South America. In mid-January, Brazil's Constitution and Justice Commission (CCJ) approved a bill prohibiting the sale of new petrol and diesel-powered cars in the country as of January 2030. Around 700 thousand EVs are expected to be circulating in Brazil by 2030.

- Furthermore, The Brazilian construction industry remained weak in March 2023, with activity and employment falling for the fifth month. However, the most recent data by the National Confederation of Industry (CNI), with the support of the Brazilian Chamber of Construction Industry (CBIC), indicate that the fall in activity was not severe and broad. Furthermore, the reduction in activity from February to March 2023 is the mildest in the series of declines that began in November 2022.

- The reduction in activity is ascribed to high energy and construction material prices and soaring inflationary pressures, as are high-interest rates, decreasing levels of demand, and excessive household debt. In March 2023, the building activity index was 49.5, marking the fifth consecutive month with a score less than 50. This was preceded by February scores of 47.6 and January 2023 scores of 45.9.

- The Brazilian furniture industry has been growing steadily over the past three years, and the demand for newly designed furniture has been high recently.

- Brazil is the sixth largest producer of furniture globally, and many Brazilian furniture companies and designers have invested in innovative solutions that speed up production, shipping, and delivery. As a result of these efforts and more, furniture exports grew 50.9% from 2020 to 2021, with 35% of Brazil's exports in the furniture industry specifically destined for American stores.

- According to the Brazilian Association of Furniture Manufacturers (ABIMOVEL), Brazil's furniture industry is formed by 19,000 companies, 80% of which are concentrated in the country's South and Southeast regions, led by the state of Sao Paulo and followed by the conditions of Rio Grande do Sul, Minas Gerais, Parana, and Santa Catarina.

- According to IEMI Inteligencia de Mercado, the country produced more than 367 million furniture units in 2022 compared to 405 million units in 2021. However, the furniture production value in Brazil amounted to approximately 65 billion Brazilian reals in 2022 compared to 68.04 billion Brazilian reals in 2021.

- Hence, with the growth in the construction, infrastructure, and automotive sectors, the demand for paints and coatings is expected to witness growth over the coming years.

South America Paints and Coatings Industry Overview

The South American paints and coatings market is partially consolidated. The major companies (not in particular order) include PPG Industries, Inc., Akzo Nobel N.V., Jotun, Axalta Coating Systems, and The Sherwin William Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Construction Industry in the Region

- 4.1.2 Increasing Applications and Usage in the Automotive Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Related to VOC-Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Acrylics

- 5.1.2 Epoxy

- 5.1.3 Alkyd

- 5.1.4 Polyester

- 5.1.5 Polyurethane

- 5.1.6 Other Resin Types (Polypropylene, Etc.)

- 5.2 Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder Coating

- 5.2.4 UV-cured Coating

- 5.3 End-User Industry

- 5.3.1 Architectural

- 5.3.2 Automotive

- 5.3.3 Wood

- 5.3.4 Industrial

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems

- 6.4.3 BASF SE

- 6.4.4 Hempel

- 6.4.5 Jotun

- 6.4.6 Lanco Paints

- 6.4.7 PPG Industries, Inc.

- 6.4.8 Renner Herrmann S.A.

- 6.4.9 The Sherwin William Company

- 6.4.10 WEG Coatings

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Bio-based and Eco-friendly Paints and Coatings

- 7.2 Growing Opportunities in the Aerospace Sector