北米のオペレーショナルインテリジェンス:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Operational Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639427

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

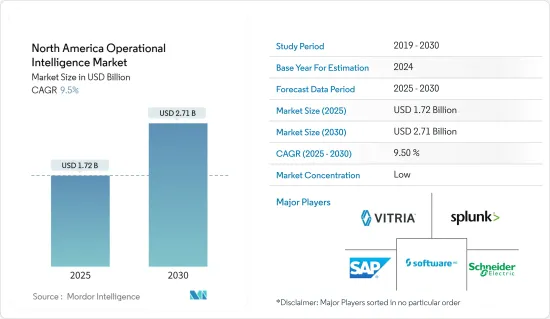

北米のオペレーショナルインテリジェンスの市場規模は、2025年に17億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.5%で、2030年には27億1,000万米ドルに達すると予測されています。

データ品質管理、発見、可視化の必要性から、企業はオペレーショナルインテリジェンス・ソフトウェアを採用せざるを得ないです。オンプレミスのESBとBPM(ビジネスプロセス管理)ソリューションは、企業の複雑な社内システムとアーキテクチャを統合しながら、垂直方向の拡張性を確保するのに適しています。

主なハイライト

- オペレーショナルインテリジェンス(OI)は、ビジネスとITの運用に関する洞察を提供する、動的なリアルタイムのビジネス分析の一形態です。これらのソリューションは、データ収集と分析のプロセスを合理化する機会を企業に提供します。企業はリアルタイムで監視とトラブルシューティングを行い、セキュリティとコンプライアンス手法を改善することで、顧客へのサービス提供をスピードアップできます。

- 企業は、ビジネス・インテリジェンスやデータウェアハウス・ツールのような従来の分析ツールでは、意思決定のために利用可能なデータの可能性をフルに活用することはできないです。こうした従来の情報管理システムでは、データの量が多く多様性があるため、実用的で実用的な方法でデータを分析することができないです。

- シスコシステムズは、センサー、ネットワーク、セキュリティ・システム、サーバー、ストレージ、アプリケーションなど、生成される全データの約42%が機械からのものになると推定しています。リアルタイムのデータ分析は、IoTとビッグデータ機能に影響を及ぼし、事業運営を強化することができます。

- さらに、異なるデバイスやプラットフォーム間の相互運用性の課題は、動的なアプリケーション、サービス、データを接続することが困難であるため、企業にとって複雑な問題となっています。そのため、クラウド・ソリューションへの移行は、企業が現在の統合の課題を解決すると同時に、将来に向けて必要となる管理性、拡張性、信頼性を提供するのに役立ちます。

北米のオペレーショナルインテリジェンス市場の動向

クラウドが大きな市場シェアを占める

- クラウドの導入は、コスト削減、アクセス性、拡張性、サービスの一元化といった付加的なメリットにより、大きな市場シェアを占めると予想されます。また、企業ワークロードの83%以上がクラウドになると予想され、そのうち41%はパブリッククラウドプラットフォームで実行されます。さらに20%はプライベートクラウドベースとなり、22%はハイブリッドクラウドの採用に依存することになります。

- フレクセラの調査によると、クラウド戦略はパブリックでもプライベートでもなく、ハイブリッドに焦点を当てる傾向が強まっています。ハイブリッド・クラウドは、製品やサービスを提供する企業にとって新たな規範となっています。フレクセラによると、ハイブリッド・クラウドの普及率は2023年には72%に増加するといいます。

- さらに、オペレーショナルインテリジェンスへのクラウド導入の推進には、コスト効率が重要な役割を果たします。クラウドプロバイダーは従量課金モデルを提供しているため、ハードウェアやインフラへの多額の先行投資が不要となります。そのため、企業はリソースを効率的に配分し、必要に応じてオペレーショナルインテリジェンス・ツールに投資することができます。クラウドは弾力性に富んでいるため、企業は消費したリソースに対してのみ料金を支払えばよく、コストを管理しながらオペレーショナルインテリジェンスへの取り組みを最適化したい企業にとって、魅力的な選択肢となります。

- さらに、クラウドベースのオペレーショナルインテリジェンスソリューションのスピードと俊敏性は、今日のペースの速いビジネス環境では非常に貴重です。リアルタイムのデータ分析により、企業は情報に基づいた意思決定を即座に行い、変化する市場環境に迅速に対応し、新たな動向を把握することができます。クラウドの分散アーキテクチャと高度な分析機能により、企業は記録的な速さで多様なデータソースから実用的な洞察を導き出すことができます。

小売業が大きな市場シェアを占める見込み

- 小売業界におけるAIの導入は、手作業を減らし、配送を迅速化し、顧客と注文の管理を改善し、オペレーションを合理化することで、小売関連のプロセスを自動化し、最終的にすべてのコストを削減します。

- さらに、小売業のインフラは複雑かつ分散しており、POS(販売時点情報管理)、レジ端末、セルフレジ、PC、バックオフィスのサーバーなどが含まれます。そのため、卸売業者や流通業者からメーカーやサプライヤーに至るまで、ITへの依存度が高まっており、シームレスな小売バリューチェーンを可能にする統合インフラが求められています。これは、オペレーショナルインテリジェンスの成長に対応しています。

- オックスフォード・エコノミクスによると、大手小売企業の83%がデジタルトランスフォーメーションを中核的な事業目標としています。オックスフォード・エコノミクスはまた、中堅・中小小売企業(59%)がデジタルトランスフォーメーションを推進していることにも注目しています。デジタルトランスフォーメーションが浸透しつつある今、小売業界の変革志向に伴い、調査対象市場も拡大することが予想されます。

- さらに、小売業界ではクラウドベースのソリューションの採用が進んでおり、在庫や注文処理など複数の業種を統合することで、在庫補充能力を向上させています。

- さらに、クラウド・コンピューティングを利用すれば、小売企業は全社的なサプライチェーンの可視化を実現できます。最近では、Gap Inc.がIntermixブランドの世界オペレーションにクラウドテクノロジーを採用しました。このファッション小売企業は、オラクルが提供するクラウドサービスを導入し、小売マーチャンダイジング、統合、在庫管理などのソリューションを提供しています。

北米のオペレーショナルインテリジェンス業界の概要

北米のオペレーショナルインテリジェンス市場は、大小さまざまなベンダーが業務に関する包括的な可視化と考察を提供しており、細分化と激しい競合が特徴です。これにより、企業は情報に基づいたデータ主導の意思決定を行うことができます。このダイナミックな市場におけるその他の主要企業には、ビトリア・テクノロジー社やスプランク社などがあります。

2023年5月、SAP SEはIBMとの戦略的提携を発表しました。このパートナーシップの下、SAPはIBM Watsonテクノロジーを自社のソリューションに統合します。この統合により、SAP SEはAIを活用した高度な洞察と自動化を実現し、イノベーションを加速させ、幅広いソリューション・ポートフォリオを通じてユーザー体験を向上させることができます。

2022年8月、National Rural Telecommunications Cooperative(NRTC)はオペレーショナルインテリジェンス・プラットフォームの一般提供を発表しました。このプラットフォームはベンダーを問わない分析機能が特徴で、ブロードバンドプロバイダーの業務を最適化するように設計されています。リアルタイムのデータ分析と機械学習を活用することで、このプラットフォームは加入者の問題やサービス中断の可能性を積極的に特定し、プロバイダーは利用者に影響が及ぶ前にこれらの問題に対処することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- リアルタイムデータ分析のニーズの高まり

- ビッグデータ解析とIoTの採用拡大

- 市場抑制要因

- 複数のデータソースからのデータの結合

第6章 市場セグメンテーション

- 展開タイプ別

- クラウド

- オンプレミス

- エンドユーザー業界別

- 小売

- 製造業

- BFSI

- 政府機関

- IT・通信

- 軍事・防衛

- 運輸・物流

- ヘルスケア

- エネルギー・電力

第7章 競合情勢

- 企業プロファイル

- Vitria Technology Inc.

- Splunk Inc.

- SAP SE

- Inside Analysis(The Bloor Group)

- Software AG

- Schneider Electric SE

- Rolta India Limited

- SolutionsPT Ltd

- IBENOX Pty Ltd

- Turnberry Corporation

- HP Inc.

- OpenText Corporation

第8章 投資分析

第9章 市場機会と今後の動向

目次

The North America Operational Intelligence Market size is estimated at USD 1.72 billion in 2025, and is expected to reach USD 2.71 billion by 2030, at a CAGR of 9.5% during the forecast period (2025-2030).

The need for data quality management, discovery, and visualization compels businesses to adopt operational intelligence software. On-premise ESB and BPM (business process management) solutions are well suited for vertical scalability while integrating an enterprise's complex internal systems and architecture.

Key Highlights

- Operational intelligence (OI) is a form of dynamic, real-time business analytics that delivers insights into business and IT operations. These solutions provide enterprises with the opportunity to streamline the process of data collection and analysis. Enterprises can monitor and troubleshoot in real-time and improve their security and compliance methods, thereby speeding up the delivery of their services to customers.

- Enterprises cannot tap the full potential of the available data for making decisions using traditional analytical tools, such as business intelligence and data warehouse tools. These conventional information management systems cannot analyze the data in any practical and actionable way due to their high volume and diversity.

- Cisco Systems estimates that around 42% of all data generated will likely be from machines, including sensors, networks, security systems, servers, storage, and applications. Real-time data analytics can influence the IoT and Big Data capabilities to enhance business operations.

- Moreover, the challenge of interoperability between different devices and platforms has complicated issues for businesses, as it is challenging to connect dynamic applications, services, and data. Therefore, the shift to cloud solutions helps enterprises address their current integration challenges while giving them the manageability, scalability, and reliability they need for the future.

North America Operational Intelligence Market Trends

Cloud Accounts for Significant Market Share

- Cloud deployment is expected to hold a prominent market share owing to the added benefits, such as cost-saving, accessibility, scalability, and centralized service. It is also expected that more than 83% of the enterprise workload will be in the cloud, out of which 41% of the enterprise workload will be run on public cloud platforms. Another 20% will be private-cloud-based, while 22% will rely on hybrid-cloud adoption.

- According to the survey by Flexera, cloud strategy is increasingly focused on hybrid instead of public and private. A hybrid cloud is a new norm for businesses delivering products and services. According to Flexera, the hybrid cloud penetration rate increased to 72% in 2023.

- Moreover, cost-effectiveness plays a crucial role in driving cloud adoption for operational intelligence. Cloud providers offer a pay-as-you-go model, eliminating the need for substantial upfront investments in hardware and infrastructure. This allows businesses to allocate resources efficiently, investing in operational intelligence tools as necessary. The cloud's elasticity ensures that organizations only pay for the resources they consume, making it an attractive option for companies looking to optimize their operational intelligence efforts while managing costs.

- Furthermore, the speed and agility of cloud-based operational intelligence solutions are invaluable in today's fast-paced business landscape. Real-time data analysis enables organizations to make informed decisions on the fly, respond swiftly to changing market conditions, and identify emerging trends. The cloud's distributed architecture and advanced analytics capabilities empower businesses to derive actionable insights from diverse data sources in record time.

Retail is Expected to Account For Significant Market Share

- The adoption of AI in the retail industry automates retail-related processes with lesser manual work, faster delivery, better customer and order management, and streamlined operations, all of which eventually reduce costs.

- Moreover, retail infrastructure is complex and distributed and includes POS (point of sale), checkout terminals, self-checkout units, PCs, and back-office servers. Thus, the increasing dependency on IT, ranging from wholesalers and distributors to manufacturers and suppliers, demands an integrated infrastructure that enables a seamless retail value chain. This caters to the growth of operational intelligence.

- According to Oxford Economics, 83% of large retailers consider digital transformation a core business goal. Oxford also highlighted the traction from small and midsize retailers ((59%) and their belief in digital transformation. In the era where digital transformation is gaining traction, the market studied is expected to grow along with the retail sector's inclination to transform.

- Additionally, the retail sector is increasingly witnessing the adoption of cloud-based solutions, as they integrate several verticals, like inventory and order processing, thus improving the restocking capabilities.

- Furthermore, with cloud computing, retailers may have enterprise-wide supply chain visibility. Recently, Gap Inc. adopted cloud technology across its global operations for its Intermix brand. The fashion retailer has deployed cloud services provided by Oracle, with solutions comprising retail merchandising, integration, and inventory management.

North America Operational Intelligence Industry Overview

The North American operational intelligence market is marked by fragmentation and fierce competition, featuring a wide range of vendors, both large and small, that offer comprehensive visibility and insights into business operations. This enables companies to make informed, data-driven decisions. Notable key players in this dynamic market include Vitria Technology Inc. and Splunk Inc., among others.

In May 2023, SAP SE announced a strategic collaboration with IBM. Under this partnership, SAP will be integrating IBM Watson technology into its solutions. This integration is set to empower SAP SE in delivering advanced AI-driven insights and automation, accelerating innovation, and enhancing user experiences throughout its extensive solution portfolio.

In August 2022, the National Rural Telecommunications Cooperative (NRTC) unveiled the general availability of its operational intelligence platform. This platform is characterized by its vendor-agnostic analytics capabilities, designed to optimize the operations of broadband providers. Leveraging real-time data analysis and machine learning, this platform proactively identifies subscriber issues and potential service disruptions, enabling providers to address these concerns before they impact users.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Real Time Data Analytics

- 5.1.2 Increasing Adoption of Big Data Analytics and the Internet-of-Things (IoT)

- 5.2 Market Restraints

- 5.2.1 Combining Data from Multiple Data Sources

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 Cloud

- 6.1.2 On-premise

- 6.2 By End-user Vertical

- 6.2.1 Retail

- 6.2.2 Manufacturing

- 6.2.3 BFSI

- 6.2.4 Government

- 6.2.5 IT and Telecommunication

- 6.2.6 Military and Defense

- 6.2.7 Transportation and Logistics

- 6.2.8 Healthcare

- 6.2.9 Energy and Power

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vitria Technology Inc.

- 7.1.2 Splunk Inc.

- 7.1.3 SAP SE

- 7.1.4 Inside Analysis (The Bloor Group)

- 7.1.5 Software AG

- 7.1.6 Schneider Electric SE

- 7.1.7 Rolta India Limited

- 7.1.8 SolutionsPT Ltd

- 7.1.9 IBENOX Pty Ltd

- 7.1.10 Turnberry Corporation

- 7.1.11 HP Inc.

- 7.1.12 OpenText Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日