欧州のオペレーショナルインテリジェンス:市場シェア分析、産業動向、成長予測(2025年~2030年)

Europe Operational Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637867

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

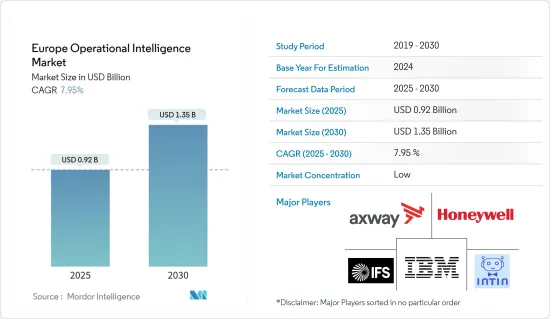

欧州のオペレーショナルインテリジェンス市場規模は、2025年に9億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.95%で、2030年には13億5,000万米ドルに達すると予測されています。

データ品質管理、データ発見、データ可視化の必要性から、企業はオペレーショナルインテリジェンスソフトウェアの導入を余儀なくされています。オンプレミスのESBとBPM(ビジネスプロセス管理)ソリューションは、組織の複雑な内部システムやアーキテクチャと統合しながら、垂直方向の拡大性を確保するのに適しています。

主要ハイライト

- 欧州では、さまざまな産業がビッグデータ分析とモノのインターネット(IoT)を導入しており、オペレーショナルインテリジェンス市場の成長を後押ししています。しかし、オペレーショナルインテリジェンスツールのコストが高いことがオペレーショナルインテリジェンス市場の成長を抑制しています。OIツールの導入とその複雑なプログラミングは、企業にとってコストのかかる作業となります。高コスト要因や、ソフトウェアの操作に熟練した専門家が必要といった要因の結果、同地域の市場成長はより良くなる可能性があります。

- 多くの産業がデジタルインフラに投資しています。また、多くの欧州諸国がデジタルインフラに多額の投資を行っています。それでもなお、スキルのギャップを埋め、クラウドの導入率を加速させるために、民間や公的な取り組みが開始されています。この流行期に、欧州連合(EU)で先進的デジタル技術を導入したことのある企業の53%が、デジタル化への投資を増やしました。これは、危機を契機にデジタル変革への投資を開始した非デジタルEU企業の34%と比較してのことです。

- クラウドの採用は、拡大性、コスト削減、アクセシビリティ、サービスの一元化といったその他の特典により、大きな市場シェアを獲得すると予想されます。同地域の統計機関であるEurostatによると、クラウドに移行する企業が大幅に増加しています。同機関が発表したレポート「企業によるクラウドコンピューティング利用統計」の中で、クラウドに移行する企業がEU全体で23%増加したのは、マルタ(65%)、キプロス(50%)、ハンガリー(50%)、ドイツ(45%)、英国(45%)だったと報告しています。ネットアップによると、ハイブリッドクラウドインフラは欧州で最も好まれるクラウド導入方法だといいます。

- さらに、OI導入の主要メリットは、予知保全のように、運用上の問題や機会が発生した時点、あるいは発生する前に対処できることです。また、オペレーショナルインテリジェンスによって、ビジネスリーダーや従業員は日々、より多くの情報に基づき、より良い意思決定を行うことができるようになります。最終的に、ビジネスオペレーションの可視性と洞察が向上し、適切に管理されれば、収益が増加し、競合他社に対する競争上の優位性を獲得することができます。

- COVID-19の大流行は、欧州のオペレーショナルインテリジェンス市場に大きな影響を与えました。多くの企業が混乱に直面し、業務を適応させなければならなかった。医療やロジスティクスなど一部のセグメントでは、課題に対処するためのオペレーショナルインテリジェンスソリューションに対する需要が高まった。しかし、経済の不確実性により、他の産業では技術投資の予算が制約されました。

欧州のオペレーショナルインテリジェンス市場動向

IT・通信エンドユーザー部門が大きな市場シェアを占める見込み

- リアルタイムの分析と意思決定に対するニーズの高まりと、さまざまなエンドユーザー産業からのオペレーショナルインテリジェンス(OI)に対する需要の急増が、市場成長の原動力となっています。さまざまな産業でデータ駆動型技術の導入が進んでいることが、主に欧州のオペレーショナルインテリジェンス市場を牽引しています。また、民間企業も公共企業もデジタル技術やデータ駆動型技術に投資しており、それが同国のオペレーショナルインテリジェンス市場の成長を後押ししています。

- モノのインターネットの成長により、生産機械、パイプライン、エレベーター、その他の機器から収集したセンサデータを分析するオペレーショナルインテリジェンスアプリケーションが台頭しています。これにより、機器の潜在的な故障を事前に検出することを目的とした予知保全活動が可能になります。サーバー、ネットワーク、ウェブサイトのログなど、さまざまな種類のマシンデータもOI用途の原動力となり、リアルタイムで分析されて、セキュリティ上の脅威やIT運用上の問題を探します。

- リアルタイムで運用できるビジネスインテリジェンスシステムの採用が増えたことが、オペレーショナルインテリジェンスシステムに対する需要を押し上げ、IT動向の採用が増えたことが市場成長の原動力となっています。SWZDによると、欧米の組織で導入済みまたは導入予定のIT動向としてIoTが最も多く、2023年には57%を占めました。

- さらに2023年12月、スペインの多国籍通信会社であるTelefonicaは、技術サービスのリーダーの1つであるTelefonica Techが、サイバー脅威に対するプロアクティブな防御で企業を強化するサイバーインテリジェンスサービスを拡大したと発表しました。Telefonica Techの先進的サイバーインテリジェンスサービスは、ネクストディフェンスのマネージドサービスの一部であり、企業に強固なサイバー耐性を記載しています。企業の成熟度レベルや利用するプロフェッショナルのプロファイルに合わせて、さまざまな製品を提供しています。このサービスは、セキュリティリスクの強化、特定、伝達、軽減に重点を置き、進化する脅威に対して組織を強化します。運用インテリジェンスサイバー攻撃者の戦術、技術、手順(TTP)に関する洞察を提供し、セキュリティチームが進化する攻撃パターンに適応できるよう支援します。

- データ主導の世界におけるオペレーショナルインテリジェンスの影響力は明らかであり、著しく高まっています。世界中の企業経営幹部は、リアルタイムデータによる予測的な意思決定がビジネスに影響を与える最も重要な原動力の1つであることに同意しています。

ドイツが大きな市場シェアを占める見込み

- ドイツのオペレーショナルインテリジェンス市場はダイナミックで、技術の進歩とセキュリティ脅威の変化に合わせて進化し続けています。防衛・情報機関を含むドイツ政府は、オペレーショナルインテリジェンス機能に多額の投資を行っています。これには、国内外の潜在的脅威をモニタリングするためのモニタリング技術、シグナルインテリジェンス、データ分析が含まれます。

- サイバー脅威がますます蔓延する中、ドイツではサイバーセキュリティが作戦インテリジェンスの重要な側面となっています。サイバーセキュリティを専門とする企業は、サイバー攻撃やデータ漏洩、その他のデジタル脅威から組織を守るためのサービスやソリューションを提供しています。

- NATOによると、2023年、ドイツは国防に推定680億米ドルを支出しました。サイバー脅威の拡大、規制状況、デジタルトランスフォーメーション、政府の取り組み、サイバーセキュリティのスキル不足を背景としたサイバーセキュリティへの投資の増加が、ドイツにおけるオペレーショナルインテリジェンスソリューションの需要を押し上げています。

- ドイツのオペレーショナルインテリジェンス市場は、人工知能、機械学習、ビッグデータ分析などの技術革新の恩恵を受けています。これらの技術により、より効果的なデータ処理、リアルタイムのモニタリング、予測機能が可能になります。

欧州のオペレーショナルインテリジェンス産業概要

欧州のオペレーショナルインテリジェンス市場は細分化されており、小規模ベンダーから大規模ベンダーまでが事業運営の可視性と洞察力を高め、企業がデータ主導の意思決定を行えるよう支援しています。同市場の主要企業には、Axway, Inc.、Honeywell International Inc.、Industrial And Financial Systems Ab(IFS)、Intelligent Insites, Inc.、IBMなどがあります。市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年3月-OpenTextは、デジタル業務の合理化を目的としたバイエルとの戦略的協業を発表しました。この取り組みにおいて、Bayerは、コンシューマーヘルス部門と製薬部門におけるB2B統合のための極めて重要なソリューションとして、OpenText Business Network Cloud Enterpriseを導入します。その目的は、俊敏性と業務効率を高めることです。

- 2023年8月-IBMは欧州の石油・ガス会社向けにAI Center of Competenceを構築。Wintershall Deaは、事業内部の多様な部門にわたってAIを使用し、拡大するための全体的なアプローチを育成します。Wintershall DeaのAIセンター・オブ・コンピテンシーは、石油・ガス会社の幅広いAI資産を統合し、その利用と会社と顧客にとってのメリットをよりよく調整することを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- エンドユーザー産業全体におけるリアルタイム分析と意思決定の増加がオペレーショナルインテリジェンス市場を牽引

- 業務効率と生産性の向上に重点を置く組織

- 将来のリスクを特定するための綿密なデータ分析の必要性

- 市場抑制要因

- ビジネス要件を管理するためのデータ転送と処理の複雑さ

- オペレーショナルインテリジェンスソリューションの導入にかかるコストの高さ

第6章 市場セグメンテーション

- 導入タイプ

- クラウド

- オンプレミス

- エンドユーザー産業別

- 小売業

- 製造業

- BFSI

- 政府機関

- IT・通信

- 軍事・防衛

- 運輸・物流

- 医療

- エネルギー・電力

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

第7章 競合情勢

- 企業プロファイル

- Axway, Inc.

- Honeywell International Inc.

- Industrial And Financial Systems Ab(IFS)

- Intelligent Insites, Inc.

- IBM

- Open Text Corporation

- Opsveda, Inc.

- Rolta India Limited

- SAP SE

- Schneider Electric SE

- Software AG

- Splunk Inc.

- Turnberry Solutions

- Vitria Technology, Inc

第8章 市場機会と今後の動向

目次

The Europe Operational Intelligence Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 1.35 billion by 2030, at a CAGR of 7.95% during the forecast period (2025-2030).

The need for data quality control, data discovery, and data visualization is forcing companies to deploy operational intelligence software. On-premises ESB and BPM (Business Process Management) solutions are well suited for vertical scalability while integrating with an organization's complex internal systems and architectures.

Key Highlights

- In Europe, various industries are adopting big data analytics and the Internet of Things (IoT), in turn propelling the growth of the operational intelligence market. However, the high cost of operational intelligence tools is restraining the operational intelligence market growth. The deployment of OI tools and their complex programming becomes a costly affair for business enterprises. As a result of factors like the high-cost factor and the requirement of skilled professionals to operate the software, the market growth could be better in the region.

- Many industries are spending on their digital infrastructures. Also, many European countries are investing heavily in their digital infrastructure. Still, private and public initiatives have been launched to fill the skills gap and accelerate the rate of cloud adoption. During the epidemic, 53% of enterprises in the European Union that had previously implemented advanced digital technology increased their investment in digitalization. This is compared to 34% of non-digital EU enterprises that used the crisis as an opportunity to begin investing in their digital transformation.

- Cloud adoption is expected to gain significant market share due to additional benefits such as scalability, cost-saving, accessibility, and centralized service.Europe had the highest adoption rate of cloud services. According to Eurostat, the region's statistics agency, there has been significant growth in businesses migrating to the cloud. In its published report "Cloud Computing Statistics on the Use by Enterprises" report, the agency reported the 23% EU-wide growth in businesses migrating to the cloud was led by Malta (65%), Cyprus (50%), Hungary (50%), Germany (45%), and the United Kingdom (45%). According to NetApp, the hybrid cloud infrastructure is Europe's most preferred cloud deployment method.

- Moreover, the major benefit of an OI implementation is that operational problems and opportunities can be addressed as they arise or even before they occur, as in predictive maintenance. Operational intelligence also enables business leaders and employees to make more informed and better decisions every day. Ultimately, increased visibility and insight into business operations, if managed properly, can lead to increased revenue and competitive advantage over competitors.

- The COVID-19 pandemic significantly impacted the European operational intelligence market. Many businesses faced disruptions and had to adapt their operations. Some sectors, like healthcare and logistics, saw increased demand for operational intelligence solutions to manage challenges. However, economic uncertainties led to budget constraints for technology investments in other industries.

Europe Operational Intelligence Market Trends

IT and Telecommunication End-User Vertical is Expected to Hold Significant Market Share

- The rising need for real-time analytics & decision-making and the surge in demand for operational intelligence (OI) from various end-user industries have driven market growth. The rising incorporation of data-driven technologies across various industries is mainly driving the operational intelligence market in Europe. Also, both the private and public sector enterprises are investing in digital and data-driven technologies, thereby propelling the growth of the Operational intelligence market in the country.

- The growth of the Internet of Things has given rise to operational intelligence applications for analyzing sensor data collected from production machines, pipelines, elevators, and other devices. This enables predictive maintenance actions aimed at detecting potential equipment failures before they occur. Different types of machine data, such as server, network, and website logs, also power OI applications and are analyzed in real-time to look for security threats and IT operational issues.

- Increased adoption of a business intelligence system that can operate in real-time has driven the demand for an operational intelligence system, and increased adoption of IT trends drives market growth. According to SWZD, IoT was one of the most popular information technology trends implemented or planned to be implemented in European and North American organizations, with 57 percent in 2023.

- Furthermore, in December 2023, Telefonica, a Spanish multinational telecommunications company, announces that Telefonica Tech, one of the leaders in technology services, has expanded its cyber intelligence services to empower companies with a proactive defense against cyber threats. Telefonica Tech's advanced cyber intelligence service is a part of the NextDefense managed services, offering businesses robust cyber resilience. It provides a range of products tailored to the maturity level of companies and the profiles of professionals using it. This service focuses on enhancing, identifying, communicating, and mitigating security risks to fortify organizations against evolving threats. The operational intelligence Provides insights into cyber attackers' tactics, techniques, and procedures (TTPs), aiding security teams in adapting to evolving attack patterns.

- The impact of operational intelligence in a data-driven world is clear and rising significantly. Enterprise operational executives worldwide agreed that predictive decisions based on real-time data are one of the most significant drivers impacting their businesses.

Germany is Expected to Hold Significant Market Share

- The German operational intelligence market is dynamic and continues to evolve with technological advancements and changing security threats. The German government, including its defense and intelligence agencies, invests significantly in operational intelligence capabilities. This includes surveillance technologies, signal intelligence, and data analytics to monitor potential threats, both domestically and internationally.

- With the increasing prevalence of cyber threats, cybersecurity has become a critical aspect of operational intelligence in Germany. Companies specializing in cybersecurity provide services and solutions to protect organizations from cyber attacks, data breaches, and other digital threats.

- According to NATO, in 2023, Germany spent an estimated USD 68 billion on defense. Increasing investments in cybersecurity driven by the growing cyber threat landscape, regulatory requirements, digital transformation, government initiatives, and cybersecurity skills shortage collectively propel the demand for operational intelligence solutions in Germany.

- The German operational intelligence market benefits from technological innovation, including artificial intelligence, machine learning, and big data analytics advancements. These technologies enable more effective data processing, real-time monitoring, and predictive capabilities.

Europe Operational Intelligence Industry Overview

The European operational intelligence market is fragmented, with both small and large vendors facilitating enhanced visibility and insights into business operations, empowering companies to formulate data-driven decisions. Some of the major players in the market are Axway, Inc., Honeywell International Inc., Industrial And Financial Systems Ab (IFS), Intelligent Insites, Inc., and IBM. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2023 - OpenText revealed a strategic collaboration with Bayer to streamline digital operations. In this initiative, Bayer will implement OpenText Business Network Cloud Enterprise as a pivotal solution for B2B integration within the consumer health and pharmaceutical divisions. The aim is to boost agility and operational efficiencies.

- August 2023 - IBM built an AI Center of Competence for a European oil and gas company. Wintershall Dea to foster a holistic approach to using and scaling AI across diverse units inside businesses. The AI Center of Competency at Wintershall Dea aims to bring together the oil and gas company's broad AI assets to better coordinate their use and benefits to the company and its customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Real-time Analytics & Decision Making Across End-user Industries Drive Operational Intelligence Market

- 5.1.2 Organizations Emphasizing on Improving Operational Efficiency and Productivity

- 5.1.3 Need of In-depth Data Analysis in Order to Identify Future Risks

- 5.2 Market Restraints

- 5.2.1 Complexity in Data Transferring and Handling to Manage Business Requirements

- 5.2.2 High Cost for Implementing Operational Intelligence Solutions

6 MARKET SEGMENTATION

- 6.1 Deployment Type

- 6.1.1 Cloud

- 6.1.2 On-premise

- 6.2 End-User Vertical

- 6.2.1 Retail

- 6.2.2 Manufacturing

- 6.2.3 BFSI

- 6.2.4 Government

- 6.2.5 IT and Telecommunication

- 6.2.6 Military and Defense

- 6.2.7 Transportation and Logistics

- 6.2.8 Healthcare

- 6.2.9 Energy and Power

- 6.3 By Country

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Axway, Inc.

- 7.1.2 Honeywell International Inc.

- 7.1.3 Industrial And Financial Systems Ab (IFS)

- 7.1.4 Intelligent Insites, Inc.

- 7.1.5 IBM

- 7.1.6 Open Text Corporation

- 7.1.7 Opsveda, Inc.

- 7.1.8 Rolta India Limited

- 7.1.9 SAP SE

- 7.1.10 Schneider Electric SE

- 7.1.11 Software AG

- 7.1.12 Splunk Inc.

- 7.1.13 Turnberry Solutions

- 7.1.14 Vitria Technology, Inc

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日