|

市場調査レポート

商品コード

1639410

インドネシアのプラスチック市場:シェア分析、産業動向、成長予測(2025~2030年)Indonesia Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアのプラスチック市場:シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

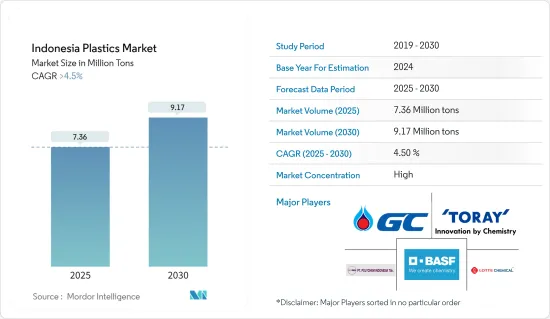

インドネシアのプラスチック市場規模は2025年に736万トンと推定され、予測期間(2025~2030年)のCAGRは4.5%を超え、2030年には917万トンに達すると予測されます。

COVID-19の大流行は、鎖国中の同国のプラスチック生産と供給に悪影響を与えました。しかし、パンデミック期間中にオンライン食品や小売eコマースサービスの利用が増加したため、包装セグメントの需要が急増しました。2020年以降は、国内の継続的な活動により、市場は着実に改善しました。

主要ハイライト

- 中期的には、包装、電気・電子、建設産業などのエンドユーザー産業からの需要増と、下流の処理能力増設の急増が、調査対象市場の成長を牽引すると予想されます。

- しかし、プラスチックの使用に関する政府の規制と原料の輸入への過度の依存は、調査した市場の成長を妨げる主要要因です。

- 環境に優しい製品に対する需要の高まりは、調査対象市場の成長にさまざまな機会を提供すると期待されています。

インドネシアのプラスチック市場動向

包装産業からの需要の高まり

- プラスチックの主要用途は、耐摩耗性、耐薬品性、成形の容易さ、リサイクル性、耐穿孔性、機械的強度の高さから包装セグメントです。さらに、ポリエチレンテレフタレート(PET)はインドネシアで最も一般的な包装用プラスチックです。

- プラスチックは、携帯性、デザインの柔軟性、洗浄のしやすさ、軽量性、他の材料よりも湿気から保護されるといった特性から、食品、小売、医薬品のセグメントで商品の包装によく使われています。さらに、取り扱いの危険性が低いこと、毒性が低いこと、ビスフェノールA(BPA)や重金属を含まないことも、PETが食品包装に使われる要因となっています。

- 製薬産業では、プラスチックは血液バッグ、注射器、ネブライザー、薬瓶の包装によく使われています。さらに、インドネシアでは人口が増加していることが医薬品開発の主要理由となっており、これが同国内でのプラスチック消費を増加させています。

- インドネシアでは、eコマース産業で商品の包装にプラスチックを使用するケースが増えています。例えば、カナダ農業・農業食品省によると、インドネシアにおける小売eコマースの販売額は2022年に480億7,000万米ドルと評価されました。2026年には904億7,000万米ドルに達すると予測されています。

- 米国農務省によると、インドネシアの包装食品の小売販売額は2022年に2022年には375億米ドルに達し、2021年の334億米ドルと比較して成長を記録しました。国内の食品包装におけるプラスチック消費の増加を示すこの動向は、今後も続くと予想されます。

- プラスチック材料は、耐久性、柔軟性、医薬品の完全性を維持する能力などの品質を提供し、医薬品包装において重要な役割を果たしています。プラスチックボトル、ブリスターパック、バイアルはその代表例です。

- プラスチックは、その効果的なバリア特性、柔軟性、軽量性、費用対効果、透明性、信頼性機能、継続的な技術革新により、無菌包装に一般的に選ばれています。しかし、プラスチック廃棄物に関連する環境問題に対処するため、サステイナブル代替品の開発にますます注目が集まっています。

- プラスチック産業を強化する動きとして、無菌包装用の最高品質の製品とソリューションを提供する著名なリーダーであるLamipakは、2022年5月にインドネシアに第2工場を建設する計画を明らかにし、1億6,000万米ドルの多額の投資を示しました。

- 上記の要因は、予測期間中、イノドネシアのプラスチック需要にかなりの影響を与えると予想されます。

射出成形技術が市場を独占する

- 射出成形技術では、熱可塑性ポリマーを融点以上に加熱し、低粘度の溶融状態にします。その後、この溶融プラスチックを所望の形態の金型に押し込んで射出し、目的の製品を得る。

- 射出成形技術は、熱可塑性ポリマーを使って、ヘルメット、ボトルキャップ、扇風機など、単純なプラスチックや複雑なプラスチックの形態を作るのに使われます。また、電線の絶縁、ボトル、化粧品の包装にも使用されます。

- 射出成形は、高品質の加工樹脂を使って行われます。設計の柔軟性、費用対効果、迅速な製造プロセス、低い人件費、合理的な色管理、良好な製品品質など、いくつかの利点があります。加えて、この製法はほとんどの場合、資本を消費するが、他の技術タイプよりも優れた、より正確な製品を記載しています。

- 射出成形は、ビーカー、検査管、キャップ、シール、クロージャー、バルブ、注射器、吸入器など、さまざまな医療機器部品の製造に利用されているため、製薬産業の需要は増加しています。さらに、国連のComtradeによると、インドネシアは2022年に輸入医薬品に約15億1,000万米ドルを支出しました。この動向は、医薬品セグメントにおける射出成形技術の将来的な可能性を示しています。

- 射出成形は、ドアパネル、バンパー、グリル、ライトハウジング、フェンダーなどの自動車部品の製造により広く使用されています。国際自動車建設機構(OICA)によると、インドネシアは2022年に約121万台の自動車を生産し、前年比37.5%の成長率を記録しました。

- さらに、プラスチックはエレクトロニクス産業で重要な役割を果たしており、筐体、筐体、部品、コネクターの軽量で耐久性のある材料として、配線や回路基板の絶縁材として、プリント基板(PCB)の生産に貢献し、包装を容易にし、ディスプレイやスクリーンを作成し、試作品の3Dプリンティングを可能にし、電子部品の損傷を防ぐ帯電防止特性を提供しています。

- 工業省によると、インドネシアの電子機器製造業の投資額は2022年に7兆5,000億ルピア(4億8,000万米ドル)に達します。

- 上記の要因から、調査対象市場は予測期間中に安定した成長が見込まれます。

インドネシアのプラスチック産業概要

インドネシアのプラスチック市場は統合されています。同市場の主要企業(順不同)には、BASF SE、PT LOTTE CHEMICAL TITAN Tbk、PTT Global Chemical Public Company Limited、PT Polychem Indonesia Tbk、TORAY INDUSTRIES INC.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エンドユーザー産業からの需要拡大

- 下流の処理能力増強の急増

- その他の促進要因

- 抑制要因

- 原料輸入への過度の依存

- プラスチックの使用に関する政府の規制

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- タイプ

- 従来のプラスチック

- ポリエチレン

- ポリプロピレン

- ポリ塩化ビニル

- ポリスチレン

- エンジニアリング・プラスチック

- ポリエチレンテレフタレート(PET)

- ポリブチレンテレフタレート(PBT)

- ポリカーボネート(PC)

- スチレンポリマー(ABS &SAN)

- フッ素樹脂

- ポリオキシメチレン(POM)

- ポリメチルメタクリレート(PMMA)

- ポリアミド(PA)

- その他エンジニアリングプラスチック(液晶ポリマー、ポリエーテルエーテルケトン)

- バイオプラスチック

- 従来のプラスチック

- 成形技術

- 射出成形

- 押出成形

- ブロー成形

- その他

- 用途

- 包装

- 電気・電子

- 建築・建設

- 自動車と輸送

- 家具・寝具

- その他の用途(家庭用品)

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Asahimas Chemical Company

- BASF SE

- LOTTE CHEMICAL TITAN HOLDING BERHAD.

- PT. INNAN

- PT Pertamina(Persero)

- PT Polychem Indonesia Tbk

- PT Chandra Asri Petrochemical

- LyondellBasell Industries Holdings BV

- PT. Standard Toyo Polymer(Tosoh Corporation)

- Sulfindo Adiusaha

- PTT Global Chemical Public Company Limited

- P.T. Solvay Chemicals Indonesia

- P.T. Toray International Indonesia

第7章 市場機会と今後の動向

- 環境に優しい製品に対する需要の高まり

- その他の機会

The Indonesia Plastics Market size is estimated at 7.36 million tons in 2025, and is expected to reach 9.17 million tons by 2030, at a CAGR of greater than 4.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the country's production and supply of plastics during the lockdown. However, the demand from the packaging segment surged due to the increasing use of online food and retail e-commerce services during the pandemic. After 2020, the market improved steadily due to continuous activities within the country.

Key Highlights

- Over the medium term, growing demand from the end-user industries, such as packaging, electrical, and electronics, as well as the construction industry, along with the rapid increase in the downstream processing capacity additions, is expected to drive the growth of the market studied.

- However, government regulations on the use of plastics and over-reliance on the imports of raw materials are the primary factors hindering the growth of the market studied.

- Nevertheless, the rising demand for eco-friendly products is expected to offer various opportunities for the growth of the market studied.

Indonesia Plastics Market Trends

Growing Demand from the Packaging Industry

- The primary utilization of plastics is in the packaging segment due to better wear and chemical resistance, ease of molding, recyclability, puncture resistance, and high mechanical strength. Furthermore, polyethylene terephthalate (PET) is Indonesia's most common plastic used for packaging purposes.

- Plastics are more commonly used in the food, retail, and pharmaceutical sectors for packaging goods due to their properties, such as portability, design flexibility, ease of cleaning, lightweight, and protection against moisture over other materials. In addition, low handling hazards, low toxicity, and the absence of bisphenol A (BPA) and heavy metals are other factors that allow PET to be used for food packaging.

- In the pharmaceutical industry, plastics are commonly used for packaging blood bags, syringes, nebulizers, and medicine bottles. Furthermore, the growing population in Indonesia is the main reason for pharmaceutical development, which has increased the consumption of plastics within the country.

- In Indonesia, the use of plastics for packaging goods is increasing in the e-commerce industry. For instance, according to Agriculture and Agri-Food Canada, the sales value of retail e-commerce in Indonesia was valued at USD 48.07 billion in 2022. It is forecasted to reach USD 90.47 billion in 2026.

- According to the United States Department of Agriculture, the retail sales value of packaged foods in Indonesia reached USD 37. 5 billion in 2022 and registered growth when compared to USD 33.4 billion in 2021. This trend, which shows the growing consumption of plastics in food packaging within the country, is expected to continue.

- Plastic materials play a crucial role in pharmaceutical packaging, offering qualities such as durability, flexibility, and the ability to maintain the integrity of medicines. Plastic bottles, blister packs, and vials are common examples.

- Plastic is commonly chosen for aseptic packaging due to its effective barrier properties, flexibility, lightweight nature, cost-effectiveness, transparency, reliability features, and ongoing innovations. However, there is an increased focus on developing sustainable alternatives to address environmental concerns associated with plastic waste.

- In a move to bolster the plastic industry, Lamipak, a prominent leader in delivering top-quality products and solutions for aseptic packaging, revealed its plans to build a second factory in Indonesia in May 2022, demonstrating a substantial investment of USD 160 million.

- The factors mentioned above are expected to have a considerable impact on Inodnesia's demand for plastic during the forecast period.

Injection Molding Technology to Dominate the Market

- In injection molding technology, the thermoplastic polymer is heated above its melting point and converted into a molten form of low viscosity. This molten plastic is then forced and injected into a mold of the desired shape to get the desired product.

- Injection molding technology is used to make the shape of simple or complex plastics such as helmets, bottle caps, and fans using thermoplastic polymers. It is also used for wire insulation, bottles, and cosmetics packaging.

- Injection molding is done using high-quality processing resins. It has several advantages: design flexibility, cost-effectiveness, fast manufacturing process, low labor costs, reasonable color control, and good product quality. In addition, this process is mostly capital-consuming, but it offers better and more accurate products than other technology types.

- The pharmaceutical industry's demand for injection molding is increasing since it is utilized to manufacture various medical equipment parts such as beakers, test tubes, caps, seals, closures, valves, syringes, and inhalers. Furthermore, according to the UN Comtrade, Indonesia spent approximately USD 1.51 billion on imported pharmaceutical products in 2022. This trend demonstrates future opportunities for injection molding technology in the pharmaceutical sector.

- Injection molding is more extensively used in the manufacturing of automotive parts such as door panels, bumpers, grilles, light housings, fenders, and other parts. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), Indonesia produced around 1.21 million units of vehicles in 2022, witnessing a growth rate of 37.5% as compared to the previous year.

- Furthermore, plastics play a crucial role in the electronics industry, serving as lightweight and durable materials for casings, enclosures, components, and connectors, providing insulation for wiring and circuit boards, contributing to the production of printed circuit boards (PCBs), facilitating packaging, creating displays and screens, enabling 3D printing of prototypes, and offering antistatic properties to prevent damage to electronic components.

- According to the Ministry of Industry, the investment value of the electronics manufacturing industry in Indonesia reached IDR 7.5 trillion (USD 0.48 billion) in 2022.

- Due to the factors mentioned above, the market studied is expected to have steady growth during the forecast period.

Indonesia Plastics Industry Overview

The Indonesian plastics market is consolidated. Some major players in the market (not in any particular order) include BASF SE, PT LOTTE CHEMICAL TITAN Tbk, PTT Global Chemical Public Company Limited, PT Polychem Indonesia Tbk, and TORAY INDUSTRIES INC., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the End-user Industries

- 4.1.2 Rapid Increase in the Downstream Processing Capacity Additions

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Over-reliance on the Imports of Raw Materials

- 4.2.2 Government Regulations on the Use of Plastics

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polyvinyl Chloride

- 5.1.1.4 Polystyrene

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polybutylene Terephthalate (PBT)

- 5.1.2.3 Polycarbonates(PC)

- 5.1.2.4 Styrene Polymers (ABS & SAN)

- 5.1.2.5 Fluoropolymers

- 5.1.2.6 Polyoxymethylene (POM)

- 5.1.2.7 Polymethyl Methacrylate (PMMA)

- 5.1.2.8 Polyamide (PA)

- 5.1.2.9 Other Engineering Plastics (Liquid Crystal Polymer, Polyether Ether Ketone)

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 Technology

- 5.2.1 Injection Molding

- 5.2.2 Extrusion Molding

- 5.2.3 Blow Molding

- 5.2.4 Other Technologies

- 5.3 Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Furniture and Bedding

- 5.3.6 Other Applications (Houseware)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asahimas Chemical Company

- 6.4.2 BASF SE

- 6.4.3 LOTTE CHEMICAL TITAN HOLDING BERHAD.

- 6.4.4 PT. INNAN

- 6.4.5 PT Pertamina(Persero)

- 6.4.6 PT Polychem Indonesia Tbk

- 6.4.7 PT Chandra Asri Petrochemical

- 6.4.8 LyondellBasell Industries Holdings BV

- 6.4.9 PT. Standard Toyo Polymer (Tosoh Corporation)

- 6.4.10 Sulfindo Adiusaha

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 P.T. Solvay Chemicals Indonesia

- 6.4.13 P.T. Toray International Indonesia

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising demand for Eco-friendly Products

- 7.2 Other Opportunities