|

市場調査レポート

商品コード

1851327

アジア太平洋地域の紙包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Asia Pacific Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の紙包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

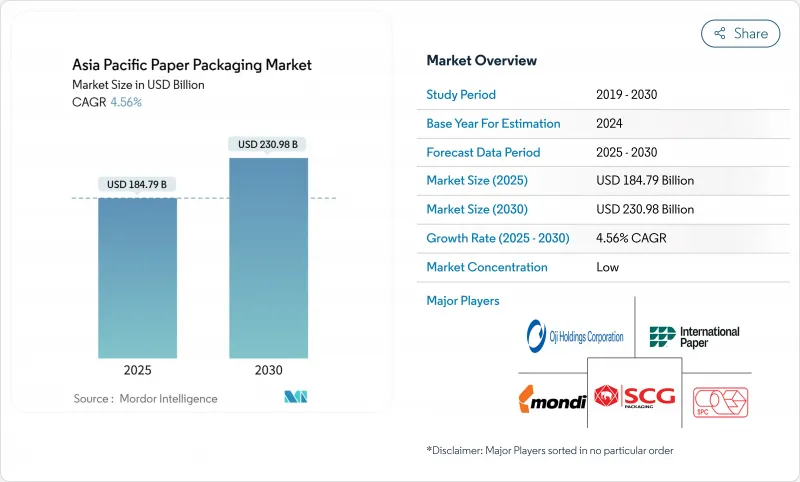

概要

アジア太平洋地域の紙包装の市場規模は2025年に1,847億9,000万米ドルに達し、2030年には2,309億8,000万米ドルに達すると予測されています。

主要経済圏の都市化が60%を超え、eコマースがすでに包装需要の80%を占めていることが、当面の数量拡大を下支えしています。ベトナム、オーストラリア、タイでは、地域全体で拡大生産者責任(EPR)制度が採用され、リサイクル・グレードとハイバリア・コーティングに資本が誘導されています。段ボール原紙はラストワンマイルの物流を支配しているため、依然として主力原紙であるが、カートン原紙は、ブランドオーナーが印刷品質、バリア機能、持続可能性を優先しているため、高級消費財や規制のあるヘルスケアチャネルで急速に支持を集めています。生産者は、広葉樹パルプの価格変動と中国の過剰生産能力によってマージンが圧迫されながらも、爆発的なSKUの増加に対応するため、AI対応設計ソフトウェアと小ロットデジタル印刷に投資しています。

アジア太平洋地域の紙包装市場動向と洞察

eコマースパッケージング需要の急増

2024年には、中国のエクスプレス輸送だけでおよそ2,200万トンの包装廃棄物が発生し、再利用可能な段ボールトートを助成する自治体のパイロット事業が促されました。地域の販売業者は同時に、保護を犠牲にすることなく板紙の使用量を最大30%削減する、製品にフィットするシステムを展開し、アルゴリズムに基づく設計サービスへの需要を高めています。そのためメーカーは、フルフィルメントセンターに近い場所に型抜きやデジタル印刷の能力をもたらすマイクロハブを設立し、カスタムグラフィックの24時間納期を可能にしています。同日配送における競合の激化は、ラストマイルの運賃を下げる軽量で高強度のフルーティンググレードの機会を広げています。

再生紙グレードへの急速なシフト

ベトナムのEPR政令は、2024年からカートン包装の20%リサイクルを義務付け、脱墨能力を高めるクローズドループ繊維回収ラインへの工場投資を加速させる。オーストラリアの2024年規則案では、すべての包装材に再生紙配合率の最低基準を設定し、目標に達しなかった場合の責任をブランド所有者に移譲し、認証されたポストコンシューマー繊維への需要を高めています。インドではすでに紙生産量の70%が非木材由来であり、国内のコンバーターにバージンパルプの変動に対するコストヘッジを提供しています。しかし、二次繊維への依存度が高くなると、汚染物質除去のためにエネルギー集約度が15~20%上昇するため、工場は酵素を用いた洗浄技術を試験的に導入しています。早期の採用企業は、2桁のEPR料金節約を売り物にし、再生グレードのスペシャリストを多国籍消費財の顧客に好まれるサプライヤーとして位置づけています。

パルプ価格の変動と供給ショック

広葉樹パルプは、気候変動による林業生産の制約を受け、2024年に平均30%の価格上昇を記録し、アジアの工場は2025年初頭にトン当たり31.50米ドルの値上げを発表せざるを得なくなりました。インドネシアとタイの通貨安は、陸上コストをさらに5~10%上昇させ、固定契約に結びついたコンバーターのマージンを侵食しました。輸入を多用する加工業者は、供給を固定化するために先買いすることで対応したが、保管の制約と在庫のバリュー・アット・リスクがこの戦術を制限しています。再生繊維への代替はエクスポージャーを低下させるが、回収原料の品質変動はランレートを不安定にします。そのため、自社植林地やバランスの取れたファイバーバスケットを持つ工場は、川下のボックスプラントに対して交渉力を持つことになります。

セグメント分析

段ボールケースはオムニチャネル小売のデフォルトの荷送人となったため、段ボールケースは2024年の売上高の58.34%を占めました。コンテナーボードのアジア太平洋地域の紙包装市場規模は、重量が減少してもボード需要を維持する製品適合アルゴリズムに支えられ、着実に拡大すると予測されます。段ボール原紙のCAGR 5.54%は、プレミアムなポジショニングを反映しています。折りたたみ段ボール原紙と硫酸漂白固形板は、高グラフィックの食品、美容、医薬品のニーズを満たし、硬質プラスチックからシェアを獲得しています。

Norske Skog社の3億2,000万ユーロのGolbey転換は、2025年までにRCFベースのライナーを年産55万トン追加する予定です。大手総合メーカーがOCCストリームを活用する一方、ニッチカートンのスペシャリストは、切り替え時間の短縮と優れた印刷面を活用しています。EPR料金がコストカーブをリサイクル可能な方向へ傾ける中、中規模の独立系企業は統合圧力に直面するか、サービス主導のニッチカートンへ軸足を移さなければならないです。

その他のテストライナーは2024年に段ボール原紙量の39.56%を占め、豊富な回収繊維と低コストから利益を得る。これらのグレードの市場シェアは、ブランドオーナーが棚の見栄えを向上させるような、より強く明るいホワイトトップのバリエーションを求めるにつれて低下する可能性があります。ホワイトトップ・クラフトライナーはCAGR 6.68%で最速の成長を遂げているが、これは高精細フレキソ印刷とデジタル・グラフィックが出荷用カートンに移行しているためであり、この動向はソーシャル・メディアによる箱詰め解除によって増幅されています。

折りたたみボックスボードは41.45%でカートンボードのグレードの大半を占め、CAGR 6.23%でグレードの成長もリードしています。次世代クレイとPVOHコーティングは乳製品パウダーに適した水蒸気透過率を付与し、FBBの拡大を支えています。カーテンコーターを後付けする生産者は、グリースプルーフの食品ライナーと医薬品のブリスターウォレットのバッカーの間を行き来することができ、資産の柔軟性を高めることができます。コーティング能力を欠く工場は、基材、設計、コンプライアンス文書を束ねた総合的なライバルにその座を譲ることになると思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- eコマース包装需要の急増

- 再生紙グレードへの急速なシフト

- 飲食品、ヘルスケア分野の拡大

- プラスチックに代わるハイバリアコート紙

- APAC全域におけるEPRとコンテンツ義務化規制

- ジェネレーティブAIを活用したデザインと小ロット印刷

- 市場抑制要因

- パルプ価格の変動と供給ショック

- コスト競争力のあるフレキシブルプラスチック代替品

- 製紙工場への炭素集約度圧力

- 価格競争に拍車をかける中国の過剰生産能力

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場規模と成長予測

- パッケージングタイプ別

- カートンボード

- 段ボール原紙

- グレード別

- カートンボード

- 固体漂白硫酸塩(SBS)

- 無漂白硫酸塩(SUS)

- 折りたたみボール紙(FBB)

- 塗工再生板(CRB)

- 非塗装リサイクル板(URB)

- 段ボール原紙

- ホワイトトップクラフトライナー

- その他のクラフトライナー

- ホワイトトップテストライナー

- その他のテストライナー

- セミケミカルフルーティング

- リサイクルフルーティング

- カートンボード

- 製品別

- 折りたたみカートン

- 段ボール箱

- 液体包装板

- 紙袋

- エンドユーザー業界別

- 食品

- 飲料

- ヘルスケアと医薬品

- パーソナルケアと化粧品

- 家庭用品

- 電気・電子

- その他のエンドユーザー産業

- 国別

- 中国

- インド

- 日本

- インドネシア

- タイ

- ベトナム

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Nine Dragons Paper(Holdings)Ltd

- Oji Holdings Corporation

- SCG Packaging PCL

- International Paper Co.(APAC)

- Mondi Group

- Smurfit WestRock plc

- Huhtamaki Oyj

- Rengo Co. Ltd

- DS Smith plc

- Pratt Industries

- Stora Enso Oyj

- Nippon Paper Industries

- APP(Asia Pulp & Paper)Group

- Visy Industries

- Harta Packaging Industries

- Sarnti Packaging Co. Ltd

- Hong Thai Packaging Co. Ltd

- New Asia Industries Co. Ltd

- C&H Paperbox(Thailand)Co. Ltd

- Continental Packaging(Thailand)Co. Ltd