|

市場調査レポート

商品コード

1637882

フランスの風力エネルギー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)France Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの風力エネルギー:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

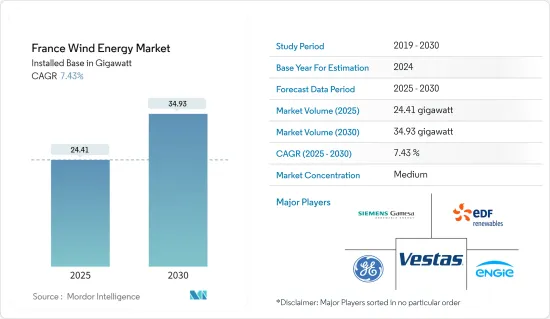

フランスの風力エネルギー市場規模は、設置ベースで2025年の24.41ギガワットから2030年には34.93ギガワットまで、予測期間(2025~2030年)のCAGRは7.43%で成長すると予測されます。

中期的には、投資の増加、今後予定されている風力発電プロジェクトや進行中の風力発電プロジェクト、風力発電容量の拡大といった要因が、予測期間中のフランスの風力エネルギー市場の大きな促進要因になると予想されます。

一方、水力発電や太陽光発電などの代替再生可能エネルギー発電や、原子力発電などの他のエネルギー源による発電の普及は、フランスの風力エネルギー市場の成長にとって大きな抑制要因になると予想されます。

再生可能エネルギー、特に風力エネルギーの生産を支援する政府の施策と関連する奨励制度は、二酸化炭素排出量を削減するためにフランスが強力にバックアップしています。このことは、今後数年間、フランスの風力エネルギー市場に機会をもたらすと考えられます。

フランスの風力エネルギー市場動向

陸上セグメントが市場を独占する見込み

- 2022年現在、風力発電設備容量の大半は陸上風力発電によるもので、洋上風力発電によるものはごく一部です。フランスでは過去10年間、風力エネルギー生産が拡大してきました。フランスの風力エネルギー部門は、水力発電に次いで2番目に大きな再生可能エネルギーです。

- 2022年、フランスの陸上風力エネルギー設備容量は2063万kWを占め、2019年には1642万kWでした。陸上風力エネルギーは2019年と比較して25.6%増加しました。2022年時点で、風力エネルギーの総設備容量はフランスの再生可能エネルギー設備容量の約31.5%を占めています。

- 国家気候エネルギー計画によると、フランスは2020年時点の17GWから2028年までに最大35GWの陸上風力発電の導入を目指しています。これにより、予測期間中に陸上風力エネルギーの利用が増加することが期待されます。

- 2023年11月、SSE Renewablesは27.2MWのChaintrix-Bierges and Velye Wind Farmの建設を開始しました。この風力発電所は、マルヌ県のChaintrix-BiergesとVelyeの間に位置する同社初のフランス陸上風力発電所で、Siemens Gamesa SG 3.4-132風力タービン8基で構成され、1基あたり3.4MWの出力が可能です。この風力発電所は、SSE Renewablesが英国とアイルランド以外で建設を開始する最初のプロジェクトであり、昨年買収した南欧州・パイプラインの最初のプロジェクトでもあります。

- さらに2023年11月、RWE AGとそのプロジェクト・パートナーは、119MWのグロス容量(80MW)を比例配分で獲得しました。RWEは3つのプロジェクトのオーナーであり、さらに2つのプロジェクトがVent du NordとDavid Energies/Energiterと共同で開発されます。全体で37基のタービンがサントル・ヴァル・ド・ロワール、オー・ド・フランス、ペイ・ド・ラ・ロワール、ヌーヴェル・アキテーヌの各地域に設置され、最初のプロジェクトは2024年末に開始されます。風力発電所は、早ければ2025年までに稼動する予定です。

- したがって、今後予定されている、また現在進行中の陸上風力発電プロジェクトが、予測期間中のフランスの風力エネルギー市場を独占することになると考えられます。

代替再生可能エネルギー源の採用増加が市場成長を抑制

- フランスの再生可能エネルギー・ミックスは、風力、水力、原子力によって占められています。しかしこのシナリオは、太陽エネルギーとバイオエネルギーの成長によって急速に変わり始めています。

- フランスは、非化石燃料、すなわち再生可能エネルギーによって最大の電力源を生産している世界でも数少ない国のひとつです。

- フランスでは近年、太陽エネルギーが大きく成長しています。同国の太陽光発電ポテンシャルは国全体に広がっています。国際再生可能エネルギー機関によると、2022年の太陽光発電容量は1,741万kWでした。

- 2022年2月、フランス政府は2050年までに太陽光発電の設置容量を100GW以上にする計画を立てた。以下のような主要開発が、同国の風力エネルギー市場を抑制すると予想されます。

- さらに、同国のバイオエネルギー容量は2020年の1,931MWから2022年には2,051MWに増加し、2019年から6.21%の増加を占めました。

- 2023年1月、TotalEnergiesはフランス南西部のMourenxに、年間生産能力160ギガワット時(GWh)のバイオガス生産ユニットBioBearnを稼働させました。BioBearnは、Lacq盆地の中心に位置する7ヘクタールの旧茶色原野に建設され、TotalEnergiesにとってフランスで18番目のバイオガス生産設備1です。この設備は、地元の農業活動や農業食品産業から排出される年間22万トンの有機廃棄物を変換することができます。

- このため、同国における代替再生可能エネルギーの導入は過去10年間で急速に拡大しており、予測期間中、フランスの風力発電市場を抑制すると予想されます。

フランスの風力エネルギー産業概要

フランスの風力エネルギー市場は半固定的です。同市場の主要企業(順不同)には、Engie SA、EDF Renewables、Vestas Wind Systems AS、General Electric Company、Siemens Gamesa Renewable Energy SAなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの風力発電設備容量と予測(単位:GW)

- 再生可能エネルギーミックス(2022年)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 再生可能エネルギーに対する有利な政府施策

- よりクリーンな発電源の採用

- 抑制要因

- 原子力や他の再生可能エネルギーとの競合

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- 導入場所

- オンショア

- オフショア

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Engie SA

- EDF Renewables

- Vestas Wind Systems AS

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- Albioma SA

- TotalEnergies SE

- Voltalia SA

- Neoen SA

- EOLFI SA

第7章 市場機会と今後の動向

- 国内における厳しい排出量目標の存在

The France Wind Energy Market size in terms of installed base is expected to grow from 24.41 gigawatt in 2025 to 34.93 gigawatt by 2030, at a CAGR of 7.43% during the forecast period (2025-2030).

Over the medium term, factors such as increasing investments, upcoming and ongoing wind energy projects, and expansion of wind energy capacities are expected to be significant drivers for the French wind energy market during the forecast period.

On the other hand, the widespread electricity generation from alternative renewable energy sources such as hydropower and solar and other sources such as nuclear energy are expected to be a significant restraint for the growth of the French wind energy market.

Nevertheless, the supportive government policies and related incentive schemes to support renewable energy production, particularly wind energy, have a strong backhold by the country to reduce its carbon footprints. This will create opportunities for the French wind energy market in the coming years.

France Wind Energy Market Trends

The Onshore Segment is Expected to Dominate the Market

- As of 2022, the majority of the wind energy installed capacity came from onshore wind farms, and a tiny portion came from offshore wind energy. Wind energy production has been growing in France over the past decade. France's wind energy sector is the second-largest renewable energy source after hydropower.

- In 2022, France's installed onshore wind energy capacity accounted for 20.63 GW, compared to 16.42 GW in 2019. Onshore wind energy increased by 25.6% as compared to 2019. As of 2022, the total wind energy installed was about 31.5% of France's renewable installed capacity.

- According to the National Climate and Energy Plan, France aims to install up to 35 GW of onshore wind by 2028, up from 17 GW as of 2020. This is expected to increase the use of onshore wind energy during the forecast period.

- In November 2023, SSE Renewables started construction of the 27.2 MW Chaintrix-Bierges and Velye Wind Farm, its first French onshore wind farm located between Chaintrix-Bierges and Velye in the Marne departement and comprises eight Siemens Gamesa SG 3.4-132 wind turbines, each capable of producing 3.4MW of output. The site is SSE Renewables' first project to enter construction outside of the UK and Ireland and the first from its Southern Europe pipeline acquired last year.

- Further, in November 2023, RWE AG and its project partners have been awarded 119 MW of gross capacity, or 80 MW, on a pro-rata basis. RWE is the controlling owner of three winning projects, while two more will be developed in partnership with Vent du Nord and David Energies/Energiter. Overall, 37 turbines will be installed across the regions of Centre-Val de Loire, Hauts-de-France, Pays de la Loire, and Nouvelle-Aquitaine, with the first projects to be launched at the end of 2024. The wind farms are planned to go online by 2025 at the earliest.

- Therefore, forthcoming and ongoing onshore wind energy projects will dominate the French wind energy market during the forecast period.

Increasing Adoption of Alternative Renewable Energy Sources is Restraining the Market Growth

- France's renewable energy mix is dominated by wind, hydropower, and nuclear energy. But this scenario has begun changing fast with solar energy and bioenergy growth.

- France is one of the few countries in the world which produces the largest source of electricity by nonfossil fuel, i.e., renewable energy sources.

- Solar energy has been growing significantly in France in recent years. The country's solar potential is widespread throughout the country. The solar power capacity in 2022 was 17.41 GW, according to the International Renewable Energy Agency.

- In February 2022, the French government planned to have more than 100GW of installed solar PV capacity by 2050. The following key developments are expected to restrain the wind energy market in the country.

- Further, Bioenergy capacity in the country increased from 1931 MW in 2020 to 2051 MW in 2022, which accounted for a 6.21 % increase from 2019.

- In January 2023, TotalEnergies commissioned the BioBearn biogas production unit in Mourenx, southwest of France, with an annual production capacity of 160 gigawatt hours (GWh). BioBearn has been built on a seven-hectare former brownfield site in the center of the Lacq basin and represents TotalEnergies' 18th biogas production unit1 in France. The unit will be capable of converting 220,000 tons of organic waste every year from local farming activities and the agri-food industry.

- Therefore, the adoption of alternative renewable energy sources in the country has been growing faster during the last decade, and it is expected to restrain the French wind market during the forecast period.

France Wind Energy Industry Overview

The French wind energy market is semi-consolidated. The key players in the market include (in no particular order) include Engie SA, EDF Renewables, Vestas Wind Systems AS, General Electric Company, and Siemens Gamesa Renewable Energy SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Wind Energy Installed Capacity and Forecast in GW, till 2028

- 4.3 Renewable Energy Mix, 2022

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Favorable Government Policies for Renewable Energy

- 4.6.1.2 Adoption of Cleaner Power Generation Sources

- 4.6.2 Restraints

- 4.6.2.1 Competition from Nuclear Energy and Other Renewable Energy Alternatives

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Engie SA

- 6.3.2 EDF Renewables

- 6.3.3 Vestas Wind Systems AS

- 6.3.4 General Electric Company

- 6.3.5 Siemens Gamesa Renewable Energy SA

- 6.3.6 Albioma SA

- 6.3.7 TotalEnergies SE

- 6.3.8 Voltalia SA

- 6.3.9 Neoen SA

- 6.3.10 EOLFI SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Presence of Strict Emission Targets in the Country