|

市場調査レポート

商品コード

1636554

欧州のプラスチック廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Plastic Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のプラスチック廃棄物管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

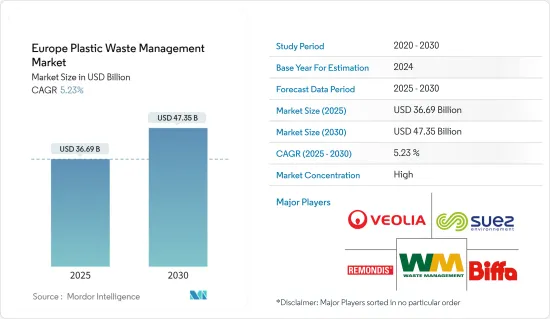

欧州のプラスチック廃棄物管理の市場規模は、2025年に366億9,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5.23%で、2030年には473億5,000万米ドルに達すると予測されます。

主なハイライト

- 欧州のプラスチック廃棄物管理市場は、急速な廃棄物発生を抑制するための政府の取り組みと、持続可能性への嗜好の高まりが主な要因です。

- プラスチック廃棄物汚染は世界の喫緊の課題です。プラスチックの大量消費国である欧州は、この問題を悪化させる上で極めて重要な役割を果たしています。同地域の年間プラスチック廃棄物発生量は、特に包装のような使い捨て品目から増加傾向にあります。しかし、リサイクル率は遅れをとっており、プラスチックの循環型経済を実現するためには、欧州がかなりの距離を越えなければならないことが浮き彫りになっています。

- 2023年、欧州連合(EU)は推定6,000万トンのプラスチック廃棄物を排出します。予測によれば、この傾向は今後も続き、2060年までにプラスチック廃棄物の発生量は倍増し、年間1億トンを超える可能性があります。

- 欧州では、包装材がプラスチック廃棄物の主な発生源となっており、EU加盟国は2023年には合計で1,600万トンを超えます。過去10年間で、EUのプラスチック包装廃棄物は約30%急増しました。

- 欧州では、埋め立てとエネルギー回収のための焼却がプラスチック廃棄物管理の大半を占め続けているが、リサイクルは遅れており、欧州大陸の廃棄物処理の15%にも満たないです。欧州連合(EU)のプラスチック包装のリサイクル率は、多少の進歩は見られるもの、50%には届かず、EUが掲げる2025年のリサイクル目標には達していないです。

- EU域外に輸出されるプラスチック廃棄物は、EU域内で処理されることを前提にリサイクル率に組み込まれています。しかし、これらの輸出品は、受け入れ国の廃棄物インフラが不十分なため、しばしば不始末に直面しています。にもかかわらず、この地域のプラスチック廃棄物輸出は減少傾向にあります。これは、プラスチック廃棄物の輸入を禁止・制限する国が増加しているためです。

- 欧州ではプラスチック汚染が喫緊の課題となっており、同地域では新たな政策の制定を促しています。例えば、欧州連合(EU)の単一使用プラスチック指令には、欧州の海岸でよく見かけるさまざまな使い捨てプラスチック製品の使用禁止が盛り込まれています。欧州では、より広範な使い捨てプラスチック禁止の機運が高まっています。特に、2023年11月、EUは2026年までにOECD非加盟国へのプラスチック廃棄物の輸出を停止することを約束したが、全面的な輸出禁止を求める声は根強いです。

欧州のプラスチック廃棄物管理市場の動向

EUの新政策は包装業界を変革し、2050年までに気候中立性を推進する

欧州連合(EU)は2023年から包装と包装廃棄物に関する法律を改正しました。この改正は、2050年までに包装業界を気候ニュートラルに導くという、より広範な目標の一環です。

2023年以降、飲食店、宅配サービス、レストランは、テイクアウト食品のオプションとして再利用可能な容器を提供することが義務付けられ、使い捨てプラスチックからの脱却が図られました。英国では2025年までに、使い捨ての飲料ボトルに25%以上の再生プラスチックを使用することが義務づけられると予測されています。

これらの新政策は、特に中小企業に恩恵をもたらし、ビジネスチャンスの波が到来する準備が整っています。また、バージン素材への依存を減らし、欧州のリサイクル能力を強化し、欧州大陸の一次資源や外部サプライヤーへの依存を軽減します。重要なことは、これらの取り組みが、2050年までの気候中立性目標に包装業界を合致させるように設定されていることです。

ネットゼロとネットポジティブの野心的な目標を目指す一方で、プラスチック産業は3つの柱、すなわちスピード、労働力、政策にかかっています。これらのマイルストーンを達成することは、欧州の競争力を高め、気候変動との闘いにおいて大きな前進を意味します。今後3~5年は、今世紀半ばまでに脱炭素化を達成できるかどうかを見極める上で極めて重要な年となります。

世界の変化の中、プラスチック廃棄物への取り組みを強化する英国

手頃な価格、耐久性、多用途性で賞賛されるプラスチックは、世界社会に定着しています。しかし、その廃棄の限界は、環境にとって大きな脅威となっています。英国はプラスチック廃棄物の排出量において際立っており、その家庭は年間1,000億個という途方もない量のプラスチック包装材を廃棄しています。2021年には、250万トンのプラスチック包装廃棄物が発生しました。

環境意識の高まりにもかかわらず、2021年のプラスチック包装廃棄物のリサイクル率は44%にとどまり、この半世紀は比較的横ばいでした。この率には、直接リサイクルと焼却によるエネルギー回収の両方が含まれています。驚くべきことに、英国のプラスチック廃棄物の半分近くがエネルギーとして焼却されている一方で、国内でリサイクルされているのはわずか12%で、25%は埋め立て地に、残りは海外に運ばれています。

国内での処理能力が不十分なため、英国はますます輸出に頼っており、特にオランダへの輸出が多く、2022年には英国のプラスチック廃棄物輸入の4分の1を占めました。しかし、世界のシナリオは変わりつつあります。伝統的な廃棄物輸入国である中国のような国々は、そのような慣行を厳しく取り締まり、廃棄物管理戦略を見直すよう英国への圧力を強めています。リサイクル・インフラを強化し、高度なリサイクル技術を導入するよう求める声が大きくなっています。

プラスチックの分解速度が遅いことから、英国では公害への懸念が高まっています。これに対して英国政府は、スーパーマーケットのレジ袋発行を顕著に抑制した使い捨てレジ袋有料化など、さまざまな政策を開始しました。さらなる禁止を求める声も出ており、スコットランドはカトラリー、皿、コーヒーカップなど問題のある使い捨てプラスチックを禁止することで先陣を切った。これに続き、イングランドも2023年10月1日から同様の禁止措置を実施することが決まった。さらに、当初2023年に予定されていた飲料容器の全国的なデポジット・リターン制度(DRS)は、経済的課題を理由に2025年に延期されました。

欧州のプラスチック廃棄物管理産業の概要

欧州のプラスチック廃棄物管理市場は細分化されています。以下のような主要企業が競合情勢を形成しています。 Veolia Environnement SA, Suez, Remondis, Biffa, Waste Management Inc., and Renewi. These industry leaders vie for market share through pioneering recycling technologies, streamlined collection and sorting, and eco-conscious waste disposal methods. Their strategies pivot on adhering to regulations, championing circular economy tenets, and curbing the environmental toll of plastic waste.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 持続可能性への需要の高まりが市場を牽引

- 環境問題への関心の高まり

- 抑制要因

- 市場に影響を与える規制要因

- 市場に影響を与えるインフラの課題

- 市場機会

- 市場を牽引する技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 政府の規制、貿易協定、イニシアチブ

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- プラスチック廃棄物管理市場における技術開拓

- COVID-19の市場への影響

第5章 市場セグメンテーション

- ポリマー別

- ポリプロピレン(PP)

- ポリエチレン(PE)

- ポリ塩化ビニル(PVC)

- ポリエチレンテレフタレート(PET)

- その他のポリマー

- 排出源別

- 住宅用

- 商業用

- 工業用

- その他(建設、ヘルスケア)

- 処理別

- リサイクル

- 化学処理

- 埋立地

- その他の処理

- 地域別

- 英国

- ドイツ

- スペイン

- フランス

- イタリア

- ロシア

- その他欧州

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Veolia Environment

- Suez Environment

- Biffa Group

- Waste Management Inc.

- REMONDIS

- Renewi

- FCC Environment

- Viridor

- DS Smith

- TOMRA

- その他の企業

第7章 市場の将来

第8章 付録

The Europe Plastic Waste Management Market size is estimated at USD 36.69 billion in 2025, and is expected to reach USD 47.35 billion by 2030, at a CAGR of 5.23% during the forecast period (2025-2030).

Key Highlights

- The European plastic waste management market is mainly driven by government initiatives to curb rapid waste generation and a growing preference for sustainability.

- Plastic waste pollution is a pressing global concern. As a significant consumer of plastics, Europe plays a pivotal role in exacerbating this issue. The region's annual plastic waste production, notably from single-use items like packaging, is on the rise. However, recycling rates are lagging, underscoring the considerable distance Europe must traverse to achieve a circular economy for plastics.

- In 2023, the European Union produced an estimated 60 million metric tons of plastic waste. Projections suggest this trend will persist, potentially leading to a doubling of plastic waste generation by 2060, exceeding 100 million metric tons annually.

- Within Europe, packaging represents the primary source of plastic waste, with EU Member States collectively producing over 16 million metric tons in 2023. Over the last decade, plastic packaging waste in the European Union surged by approximately 30%.

- In Europe, landfilling and incineration for energy recovery continue to dominate plastic waste management, while recycling lags, making up less than 15% of the continent's waste disposal. Despite some progress, the plastic packaging recycling rate in the European Union has struggled to breach the 50% mark, falling short of the bloc's 2025 recycling goal.

- The plastic waste exported from the European Union to countries outside the bloc intended for treatment is factored into recycling rates. However, these shipments often face mismanagement due to inadequate waste infrastructure in the receiving nations. Despite this, plastic waste exports in the region have been on a downward trend, attributed to an increasing number of countries enforcing bans and restrictions on such imports.

- Plastic pollution is a pressing issue in Europe, prompting the region to enact new policies. For instance, the Single-use Plastics Directive of the European Union includes bans on various disposable plastic items commonly found on European beaches. The momentum for a broader single-use plastics ban in Europe is gaining traction. Notably, in November 2023, the European Union committed to halting plastic waste exports to non-OECD nations by 2026, although calls for a total export ban persist.

Europe Plastic Waste Management Market Trends

The European Union's New Policies Set to Transform the Packaging Industry and Drive Climate Neutrality by 2050

The European Union revised its legislation on packaging and packaging waste, effective 2023. This revision is part of a broader goal to steer the packaging industry toward climate neutrality by 2050.

From 2023, eateries, delivery services, and restaurants were mandated to provide reusable containers as an option for takeout food, moving away from single-use plastics. By 2025, the United Kingdom is projected to require disposable beverage bottles to contain a minimum of 25% recycled plastic content.

These new policies are poised to usher in a wave of business opportunities, particularly benefiting smaller enterprises. They will also reduce the reliance on virgin materials, bolster Europe's recycling capabilities, and lessen the continent's dependence on primary resources and external suppliers. Crucially, these initiatives are set to align the packaging industry with climate neutrality targets by 2050.

While striving for ambitious net-zero and net-positive goals, the plastics industry hinges on three pillars, i.e., speed, workforce, and policy. Achieving these milestones positions Europe competitively and marks a significant stride in combating climate change. The upcoming three to five years will be pivotal in gauging the industry's ability to decarbonize by mid-century.

The United Kingdom Ramps up Efforts to Tackle Plastic Waste Amid Global Shifts

Plastics, lauded for their affordability, durability, and versatility, have entrenched themselves in the global society. However, the limitations in their disposal pose a significant environmental threat. The United Kingdom stands out in its plastic waste production, with its households discarding a monumental 100 billion plastic packaging pieces annually, averaging 66 per week. In 2021, the country generated 2.5 million metric tons of plastic packaging waste.

Despite heightened environmental awareness, the country's recycling rate for plastic packaging waste lingered at 44% in 2021, which remained relatively static for half a decade. This rate encompasses both direct recycling and energy recovery from incineration. Alarmingly, nearly half of the United Kingdom's plastic waste is incinerated for energy, while a mere 12% is recycled domestically, with 25% ending up in landfills and the rest shipped overseas.

With insufficient domestic processing capabilities, the United Kingdom has increasingly turned to exports, notably channeling a significant portion to the Netherlands, which accounted for a quarter of UK plastic waste imports in 2022. However, the global scenario is shifting. Countries like China, a traditional waste importer, have clamped down on such practices, intensifying the pressure on the United Kingdom to revamp its waste management strategies. Calls for bolstered recycling infrastructure and the adoption of advanced recycling technologies have grown louder.

Given the slow decomposition rate of plastic, concerns over pollution are mounting in the United Kingdom. In response, the UK government has initiated various policies, including the single-use carrier bag charge, which has notably curbed supermarket plastic bag issuance. Calls for further bans have emerged, with Scotland leading the way by prohibiting problematic single-use plastics like cutlery, plates, and coffee cups. Following suit, England was set to implement a similar ban starting October 1, 2023. Additionally, a nationwide deposit return scheme (DRS) for beverage containers, initially slated for 2023, has been delayed to 2025, citing economic challenges.

Europe Plastic Waste Management Industry Overview

The European plastic waste management market is fragmented in nature. It boasts a competitive landscape shaped by key players such as Veolia Environnement SA, Suez, Remondis, Biffa, Waste Management Inc., and Renewi. These industry leaders vie for market share through pioneering recycling technologies, streamlined collection and sorting, and eco-conscious waste disposal methods. Their strategies pivot on adhering to regulations, championing circular economy tenets, and curbing the environmental toll of plastic waste.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Demand for Sustainability Driving the Market

- 4.2.1.2 Environmental Concerns Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory Factors Affecting the Market

- 4.2.2.2 Infrastructure Challenges Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Government Regulations, Trade Agreements, and Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Developments in the Plastic Waste Management Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Polymer

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene (PE)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Polyethylene Terephthalate (PET)

- 5.1.5 Other Polymers

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Other Sources (Construction and Healthcare)

- 5.3 By Treatment

- 5.3.1 Recycling

- 5.3.2 Chemical Treatment

- 5.3.3 Landfill

- 5.3.4 Other Treatments

- 5.4 By Region

- 5.4.1 The United Kingdom

- 5.4.2 Germany

- 5.4.3 Spain

- 5.4.4 France

- 5.4.5 Italy

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Veolia Environment

- 6.2.2 Suez Environment

- 6.2.3 Biffa Group

- 6.2.4 Waste Management Inc.

- 6.2.5 REMONDIS

- 6.2.6 Renewi

- 6.2.7 FCC Environment

- 6.2.8 Viridor

- 6.2.9 DS Smith

- 6.2.10 TOMRA*

- 6.3 Other Companies