|

市場調査レポート

商品コード

1636205

北米のプラスチック廃棄物管理:市場シェア分析、産業動向、成長予測(2025~2030年)North America Plastic Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のプラスチック廃棄物管理:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

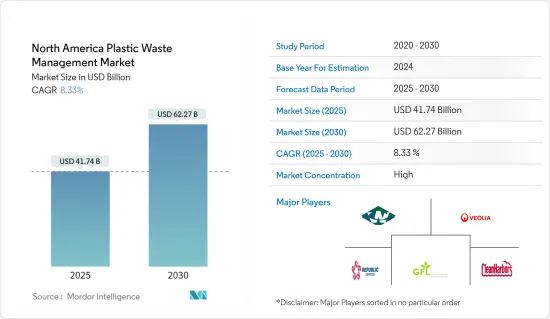

北米のプラスチック廃棄物管理の市場規模は、2025年に417億4,000万米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは8.33%で、2030年には622億7,000万米ドルに達すると予測されています。

北米のプラスチック廃棄物管理市場は、旺盛なプラスチック消費と厳しい規制に後押しされて成長しています。この勢いは、環境意識の高まり、規制の強化、廃棄物管理ソリューションの技術的進歩によるものです。

米国のプラスチック生産量は年間3,500万トンを超えます。レジ袋から包装に至るまで、アメリカ人の消費は貪欲です。しかし、このプラスチックへの食欲は悲惨な結果をもたらします。年間約800万トンの廃棄物が海に流れ込み、わずか9%がリサイクルされているにすぎないです。この環境保護の怠慢は大きな代償を伴い、プラスチック汚染は米国に年間130億米ドルの損失をもたらしていると推定されています。こうしたコストにもかかわらず、プラスチック産業は依然として重要な雇用主であり、100万人以上のアメリカ人に雇用を提供しています。地方自治体は廃棄物処理の負担を負い、年間33億米ドル以上の出費をしています。プラスチック生産は米国の国内総生産の約2.7%に寄与しています。

米国とカナダは、プラスチック廃棄物の使用禁止やリサイクルの義務化など、プラスチック廃棄物対策に大きく舵を切った。同時に、プラスチックが環境に与える影響に対する人々の意識が高まり、より効果的な廃棄物管理ソリューションへの需要に拍車がかかっています。ケミカルリサイクルや高度な選別システムのような注目すべき技術革新が、プラスチック廃棄物管理の有効性を高めています。さらに、企業が持続可能性と循環型経済の原則にますます軸足を移しているため、市場はさらに強化されています。

北米のプラスチック廃棄物管理市場は、規制の後押し、技術革新、環境意識の高まりによって、持続的な成長が見込まれています。この分野の企業は、革新的なリサイクル技術を優先し、リサイクル能力を強化し、戦略的提携を結んで市場での地位を固めていくと思われます。

北米のプラスチック廃棄物管理市場の動向

プラスチック業界のロードマップが耐久消費財のサーキュラー・エコノミーへの道を開く

プラスチック業界のロードマップは、耐久消費財の使用済み段階を再構築する大きな機会を強調しています。北米で生産されるプラスチックの60%近くが耐久消費財に使用されていることを考えると、これらの素材を保護し、プラスチックを廃棄するのではなく、新しい製品にリサイクルする循環型経済への転換を図る解決策を見出すことが不可欠です。

米国化学工業協会(ACC)のプラスチック部会は、政策立案者、ビジネスリーダー、そして一般市民をより持続可能な実践へと導く業界ロードマップを発表しました。このロードマップは、自動車、建築・建設、エレクトロニクス、インフラストラクチャー、医療の5つの主要セクターにおける循環型慣行の導入を促進するための政策と戦略の概要を示しています。

ロードマップで強調されている主なハイライトには、分解、修理、リサイクルが容易な製品とその部品の設計の必要性、使用済み部品の新製品への転換が強調されています。

高度な(ケミカル)リサイクルの極めて重要な役割は、リサイクル可能なプラスチックの範囲を広げることであり、特に従来の機械的リサイクルでは困難であった耐久性のある用途に使用されるものです。耐久性のある製品がプラスチックの循環型経済と合致するよう、基準、方法、認証プログラムを確立することの重要性。

ACCがオークリッジ国立研究所と協力して耐久性プラスチックの分別・選別・リサイクルの技術的・経済的実現可能性を評価したような、より多くのパイロットプログラムの必要性が叫ばれています。ACCは、業界のロードマップに示された循環型社会の目標を実現するため、政策立案者や耐久プラスチックのバリューチェーンと協力していくことを約束します。

米国化学工業協会(American Chemistry Council)の指導のもと、プラスチック業界は、特に自動車、建設、エレクトロニクス分野において、循環型経済への転換を図っています。業界のロードマップで強調されているこの転換は、高度なリサイクル、解体設計、厳格な基準の設定に重点を置いています。これは、政策立案者、業界大手、ACCを巻き込んだ協調的な取り組みであり、耐久性のあるプラスチックの管理方法に革命をもたらすものです。目標は、リサイクルと再利用の継続的なサイクルを確保し、廃棄物を大幅に削減することです。

米国、プラスチック消費量で高所得国をリード

米国を含む高所得国は、豊かでない国に比べて一人当たりのプラスチック消費量が多いという傾向が見られます。米国はその中でも際立っており、平均的な米国人は1日に約0.34キログラムのプラスチックを使用しています。この数字は、カナダとメキシコがそれぞれ1日1人当たり0.09キログラムであるのに対し、3倍近い使用量です。年間消費量は3,783万トンで、米国は世界第2位のプラスチック消費国であり、中国の6,000万トンという驚異的な消費量を大きく引き離しています。しかし、消費量がトップだからといって、自動的に汚染者であるということにはならないです。裕福な国は、一人当たりのプラスチック消費量が多い一方で、より効果的な廃棄方法を実現する財力も持っています。

米国をはじめとする裕福な国々は、経済的な見返りが少なくても、プラスチック廃棄物を適切に管理された埋立地に処分するか、リサイクルを選ぶ。逆に、プラスチックの消費率が低い低所得国の多くは、規制のない埋立地と格闘しているか、廃棄物管理システムが欠如しているため、プラスチック廃棄物が海洋に流入するリスクが高まっています。

2024年、米国海洋大気庁(NOAA)は、米国沿岸、五大湖、準州、自由連合州において、重大な海洋ゴミを除去し、ゴミを阻止する実証済みの技術を導入することを目的とした、変革的な複数年にわたる取り組みに約7,000万米ドルを割り当てた。さらに、NOAAは29のシーグラント・プロジェクトに2,700万米ドルを割り当て、長期的に海洋ゴミと闘うための連携構築と革新的な研究に焦点を当てた。

プラスチック消費量の格差を浮き彫りにしているのは、米国が世界第2位の消費国であることです。米国は先進的な廃棄物管理と海洋ゴミ除去に取り組んでいるが、NOAAが海洋ゴミプロジェクトに7,000万米ドルを拠出するなどの取り組みは、プラスチック汚染と闘い、海洋生態系を保護するための献身的なアプローチを強調しています。こうした試みは、消費と持続可能な廃棄物管理慣行との間の世界のギャップを埋める上で極めて重要な役割を果たしています。

北米のプラスチック廃棄物管理産業の概要

北米のプラスチック廃棄物管理市場は非常に集中しており、少数の大手企業が大半のシェアを占めています。これらの業界大手は、多大な資源、最先端技術、強固なインフラを誇り、地域規模でのプラスチック廃棄物の効果的な管理を促進しています。この市場の主要企業には、Waste Connection、Veolia Environment、GFL Environmental、Republic Services、Clean Harborsなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 意識の高まりと厳しい規制

- リサイクル技術の採用増加

- 市場抑制要因

- リサイクル施設への高額な初期投資

- 市場機会

- 環境に優しい製品や包装に対する消費者の嗜好の高まり

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- PESTLE分析

- 市場における技術革新の洞察

第5章 市場セグメンテーション

- ポリマー別

- ポリプロピレン(PP)

- ポリエチレン(PE)

- ポリ塩化ビニル(PVC)

- テレフタレート(PET)

- その他のポリマー

- 供給源別

- 住宅

- 商業

- 工業

- その他(建設、ヘルスケアなど)

- 処理別

- リサイクル

- 化学処理

- 埋立地

- その他の処理

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- Market Concetration Overview

- 企業プロファイル

- Waste Connection

- Veolia Environnement

- GFL Environmental

- Casella Waste Management

- Republic Services

- Clean Harbors

- Agilyx

- Brightmark LLC

- Advanced Disposal Services Inc.

- Covanta Holding Corporation

- Waste Management Inc.

第7章 今後の動向

The North America Plastic Waste Management Market size is estimated at USD 41.74 billion in 2025, and is expected to reach USD 62.27 billion by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

The North American plastic waste management market is growing, fueled by robust plastic consumption and stringent regulations. This momentum is attributed to a rising environmental consciousness, tightening regulations, and technological strides in waste management solutions.

Plastic production in the United States surpasses 35 million tons annually. From plastic bags to packaging, Americans' consumption is voracious. However, this appetite for plastic has dire consequences. About 8 million metric tons of waste end up in the oceans yearly, with a mere 9% recycled. This environmental negligence comes at a steep price, with plastic pollution costing the United States an estimated USD 13 billion annually. Despite these costs, the plastic industry remains a significant employer, providing jobs for over 1 million Americans. Local governments bear the brunt of waste management, shelling out more than USD 3.3 billion annually. Plastic production contributes around 2.7% to the US gross domestic product.

The United States and Canada have taken significant steps to combat plastic waste, including bans and recycling mandates. Concurrently, a swelling public awareness of plastic's environmental repercussions is spurring the demand for more effective waste management solutions. Noteworthy innovations, like chemical recycling and advanced sorting systems, are elevating the efficacy of plastic waste management. Moreover, as corporations increasingly pivot toward sustainability and circular economy principles, the market is further fortified.

The North American plastic waste management market is set for sustained growth, propelled by regulatory backing, technological innovations, and a heightened environmental consciousness. Companies in this space will likely prioritize innovative recycling technologies, bolster recycling capacities, and forge strategic alliances to solidify their market standing.

North America Plastic Waste Management Market Trends

Plastics Industry's Roadmap Paves the Way for Circular Economies in Durable Goods

The plastics industry's roadmap underscores significant opportunities to reshape the end-of-life phase for durable goods. Given that nearly 60% of domestically produced North American plastics are channeled into durable goods, it is imperative to find solutions that preserve these materials, pivoting toward a circular economy where plastics are recycled into new products rather than discarded.

The American Chemistry Council's (ACC) Plastics Division has unveiled an industry roadmap to guide policymakers, business leaders, and the public toward more sustainable practices. This roadmap outlines policies and strategies to expedite the adoption of circular practices within five key sectors: automotive, building and construction, electronics, infrastructure, and medical.

Some of the key points highlighted in the roadmap include the necessity of designing products and their components for easy disassembly, repair, and recycling, emphasizing the transformation of spent components into new products.

The pivotal role of advanced (chemical) recycling broadens the scope of recyclable plastics, especially those used in durable applications that traditional mechanical recycling struggles with. The significance of establishing standards, methods, and certification programs to ensure durable products align with a circular economy for plastics.

There is a call for more pilot programs, akin to ACC's collaboration with Oak Ridge National Laboratory to assess the technical and economic feasibility of separating, sorting, and recycling durable plastics. ACC is committed to collaborating with policymakers and the durable plastics value chain to realize the circularity goals outlined in the industry roadmap.

As guided by the American Chemistry Council, the plastics industry is pivoting toward a circular economy, especially in the automotive, construction, and electronics sectors. This shift, highlighted in the industry's roadmap, focuses on advanced recycling, designing for disassembly, and setting stringent standards. It is a concerted effort involving policymakers, industry giants, and the ACC to revolutionize how durable plastics are managed. The goal is to ensure a continuous cycle of recycling and repurposing, significantly curbing waste.

United States Leads High-income Nations in Plastic Consumption

High-income countries, including the United States, exhibit a trend of higher per capita plastic consumption compared to their less affluent counterparts. The United States stands out, with the average American using approximately 0.34 kilograms of plastic daily. This figure is nearly triple the usage of Canada and Mexico, each at 0.09 kg/person per day. With an annual consumption of 37.83 million tons, the United States ranks as the world's second-largest plastic consumer, trailing significantly behind China's staggering 60-million-ton consumption. However, being a top consumer does not automatically equate to being a polluter. Wealthier nations, while consuming more plastic per person, also possess the financial resources for more effective disposal methods.

The United States and other affluent nations predominantly dispose of their plastic waste in well-managed landfills or opt for recycling, even with minimal financial returns. Conversely, many lower-income countries with lower plastic consumption rates grapple with unregulated landfills or lack waste management systems, leading to heightened risks of plastic waste entering the oceans.

In 2024, the National Oceanic and Atmospheric Administration (NOAA) allocated nearly USD 70 million for transformative, multi-year initiatives aimed at removing significant marine debris and deploying proven technologies to intercept debris along the US coasts, Great Lakes, territories, and Freely Associated States. Furthermore, NOAA earmarked USD 27 million for 29 Sea Grant projects, focusing on coalition-building and innovative research to combat marine debris over the long term.

Highlighting the disparity in plastic consumption, the United States emerges as the world's second-largest consumer, showcasing a stark contrast between affluent and less affluent nations in waste management capabilities. While the United States demonstrates a commitment to advanced waste management and marine debris removal, initiatives like NOAA's substantial funding of USD 70 million for marine debris projects underscore a dedicated approach to combatting plastic pollution and safeguarding marine ecosystems. These endeavors play a pivotal role in bridging the global gap between consumption and sustainable waste management practices.

North America Plastic Waste Management Industry Overview

The plastic waste management market in North America is highly concentrated, with a few major players holding the majority share. These industry leaders boast significant resources, cutting-edge technologies, and robust infrastructure, facilitating the effective management of plastic waste on a regional scale. Some of the key players in this market are Waste Connection, Veolia Environment, GFL Environmental, Republic Services, and Clean Harbors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Awareness and Stringent Regulations

- 4.2.2 Rising Adoption of Recycling Technologies

- 4.3 Market Restraints

- 4.3.1 High Initial Investment for Recycling Facilities

- 4.4 Market Opportunities

- 4.4.1 Increasing Consumer Preference for Eco-friendly Products and Packaging

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Insights into Technological Innovations in the Market

5 MARKET SEGMENTATION

- 5.1 By Polymer

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene (PE)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Terephthalate (PET)

- 5.1.5 Other Polymers

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Other Sources (Construction, Healthcare, etc.)

- 5.3 By Treatment

- 5.3.1 Recycling

- 5.3.2 Chemical Treatment

- 5.3.3 Landfill

- 5.3.4 Other Treatments

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Waste Connection

- 6.2.2 Veolia Environnement

- 6.2.3 GFL Environmental

- 6.2.4 Casella Waste Management

- 6.2.5 Republic Services

- 6.2.6 Clean Harbors

- 6.2.7 Agilyx

- 6.2.8 Brightmark LLC

- 6.2.9 Advanced Disposal Services Inc.

- 6.2.10 Covanta Holding Corporation

- 6.2.11 Waste Management Inc.