|

市場調査レポート

商品コード

1636208

アジア太平洋地域のプラスチック廃棄物管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia-Pacific Plastic Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のプラスチック廃棄物管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

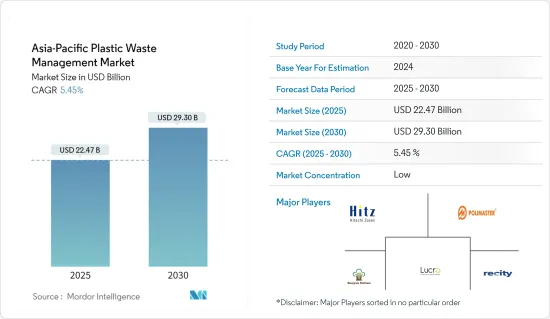

アジア太平洋地域のプラスチック廃棄物管理の市場規模は、2025年に224億7,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5.45%で、2030年には293億米ドルに達すると予測されます。

アジア太平洋地域における急速な都市化と工業の拡大が、プラスチック消費と廃棄物生産の急増に拍車をかけています。特に、中国やインドのような国々の都市部は、プラスチック廃棄物の主な発生源として際立っています。APAC地域の政府は、ますます厳しくなる対策で対応しています。これには、使い捨てプラスチックの禁止、拡大生産者責任(EPR)プログラムのイントロダクション、リサイクル促進のためのインセンティブなどが含まれます。例えば、中国はプラスチック廃棄物の輸入禁止を実施し、インドは独自のプラスチック廃棄物管理規制を展開しています。

高度な選別システムからケミカルリサイクル、生分解性リサイクルに至るまで、リサイクルの技術的進歩がプラスチック廃棄物管理の状況を再構築しています。同時に、デジタル廃棄物追跡・管理ソリューションの採用動向も高まっています。プラスチック汚染をめぐる環境問題に対する社会の意識が高まるにつれ、消費者はより持続可能な製品と責任ある廃棄物管理を求めるようになっています。その結果、企業は環境に配慮した取り組みや、リサイクル・インフラへの多額の投資を行うようになります。

アジア太平洋地域におけるプラスチック廃棄物管理市場の経済的可能性は、特に回収、分別、リサイクル、廃棄物エネルギー化技術などの分野において広大です。その結果、リサイクル・インフラや廃棄物管理施設への投資が増加しています。しかし、APACのいくつかの国では廃棄物管理インフラが不十分であること、リサイクル率が低いこと、混合プラスチック廃棄物や汚染プラスチック廃棄物が蔓延していることなどの課題が残っています。これらの課題に対処するためには、インフラのアップグレードや、廃棄物分別に対する一般市民の意識の向上と取り組みが必要です。

アジア太平洋地域のプラスチック廃棄物管理市場の動向

急速な都市化がアジア太平洋地域のプラスチック問題を悪化させる

人口約40億人のアジア太平洋地域(APAC)は急速な都市化を目の当たりにしており、深刻化するプラスチックの苦境をさらに悪化させています。国連の報告書によると、APACにはすでに28のメガシティが存在し、毎日推定12万人がこの地域の都市部に移転しています。予測によれば、2050年までにアジア太平洋地域の都市に住む人口は33億人に達するといいます。この都市化の波は消費に拍車をかけ、特に軟質プラスチック分野の使い捨て包装の需要を急増させています。このままいけば、2030年までにAPACは1億4,000万トンものプラスチック廃棄物を生み出すことになります。

世界で最も人口の多い国の多くがAPAC地域にあることを考えると、都市化の急増はライフスタイルの変化と包装商品への食欲の高まりを伴っています。包装における柔軟性は、APACにおける重要な関心事となっています。この地域の生産、特に食品分野での魅力は、関連コストの低さによって強化されています。2023年、APACは軟包装市場で52.2%のシェアを占めました。UflexやFuji Seal Internationalのような注目すべき企業が、この地域における業界の地位を強化しています。APACの使い捨てプラスチック包装、特にパウチや小袋包装(例:インドのシングルサーブウォーターパッケージ)への傾倒は、これらの素材が提供するコスト優位性によるところが大きいです。

インドネシアにおける使い捨てプラスチック袋の事例は、APAC規制の有効性を鮮明に示しています。23の都市と自治体での試行が成功した後、ジャカルタは2020年7月にレジ袋の全面禁止を実施しました。当初は企業からの反発もあったが、規制は維持され、違反企業は罰金に、再犯者は許可取り消しのリスクに直面することになった。

報告された結果は、禁止措置の成功を示しています。2018年、ジャカルタの年間レジ袋消費量は推定2億4,000万~3億枚だった。2021年までに、この消費量は1万1,192トンから6,452トンへと42%減少しました。

世界規模では、バングラデシュが2002年に全国的なレジ袋禁止を実施し、先陣を切った。中国は2020年に禁止を開始し、最終段階は2025年に設定されています。インドもこの動きに加わり、2022年に使い捨てプラスチックの禁止を実施しました。

こうした進歩にもかかわらず、アジア太平洋地域(APAC)地域の一部は遅れを取らないよう奮闘しています。韓国ゼロ・ウェイスト運動ネットワークの報告によれば、韓国では毎年190億枚ものレジ袋が消費されています。一方、タイ政府の調査によると、年間約2,000億枚のレジ袋が消費されており、これは国民1人当たり1日平均8枚のレジ袋を消費していることになります。オーシャン・コンサーバンシー(海洋保護団体)は、タイを世界の海洋廃棄物の第6位の排出国としています。

結論として、APAC各国におけるプラスチック規制の顕著な進展にもかかわらず、この地域は依然としてプラスチックの消費と廃棄物管理の大きな課題を克服する必要があります。特にこの地域の急速な都市化を考えると、これに対処するためには厳格な施行と革新的な解決策が不可欠です。

廃棄物管理で躍進する中国

2023年、浙江省の6,000人以上の個人と200社以上の企業が主導する中国のイニシアティブは、海洋プラスチック廃棄物への取り組みにおける躍進を評価され、国連環境賞の最高賞を受賞した。このプログラムは、海洋プラスチックのリサイクルの過程を透明化し、地元の漁師を助け、沿岸海域の汚染を顕著に抑制しています。プロジェクト開始以来、61,600人以上が参加し、約1万936トンの海洋ゴミを回収しました。

廃棄物管理に対する中国のコミットメントは、インフラや技術への多額の投資を通じて明らかになっています。廃棄物焼却発電所や最先端のリサイクルセンターなど、埋立地の負担を減らすための先駆的な取り組みを行っています。中国東部の浙江省は、食品配送に使用されるプラスチックの削減とリサイクルを目標とした「浙江省食品配送プラスチック廃棄物ゼロ・プログラム」を発表しました。このイニシアチブは、2023年末までに、特に大学などの主要部門で食品配送プラスチックの「廃棄物ゼロ」モデルを確立することを目的としています。2025年までに、このモデルは学校、商業スペース、地域社会に展開されます。

浙江省の戦略には協調的な取り組みが含まれ、食品宅配プラットフォーム、加盟店、大学、廃棄業者、リサイクル協会などの利害関係者を結束させ、食品宅配におけるプラスチック廃棄に反対する統一戦線を形成します。浙江省はまた、プラスチック廃棄の多い地域に廃棄物回収施設を設置する計画で、食品宅配プラットフォームには、大学の寮やカフェテリアのような場所にこうした施設を設置することを課し、大学がそのメンテナンスを行う。

全体として、浙江省の「プラスチック廃棄物ゼロプログラム」に見られるように、中国の廃棄物問題への取り組みは、プラスチック汚染と闘うための国の革新的で協力的な取り組みを示しています。これらの取り組みは先駆的であり、より広いAPAC地域の青写真を確立しています。

アジア太平洋地域のプラスチック廃棄物管理産業の概要

アジア太平洋地域のプラスチック廃棄物管理市場は非常に細分化されており、ローカルプレイヤーと世界プレイヤーが混在しています。この多様性は、国によって異なる独自の廃棄物管理要件と規制枠組みに起因しています。この分野の主要企業には、Hitz日立造船、Polimaster、Banyan Nation、Lucro、Recityなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- プラスチック消費量の増加

- プラスチック廃棄物削減を目指した規制と政策の強化

- 市場抑制要因

- 施設の設立と維持に伴う高コスト

- 市場機会

- リサイクル技術の革新

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- PESTLE分析

- 市場の技術革新に関する洞察

第5章 市場セグメンテーション

- ポリマー別

- ポリプロピレン(PP)

- ポリエチレン(PE)

- ポリ塩化ビニル(PVC)

- テレフタレート(PET)

- その他のポリマー

- 供給源別

- 住宅用

- 商業用

- 工業用

- その他(建設、ヘルスケアなど)

- 処理別

- リサイクル

- 化学処理

- 埋立地

- その他の処理

- 国別

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

第6章 競合情勢

- Market Concetration Overview

- 企業プロファイル

- Hitachi Zosen Corporation

- Polimaster

- Banyan Nation

- Lucro

- Recity

- SUEZ

- Waste Management Inc.

- Cleanaway Waste Management Limited

- Plastic Bank

- Agilyx

- GreenTech Environmental Co. Ltd

第7章 今後の動向

The Asia-Pacific Plastic Waste Management Market size is estimated at USD 22.47 billion in 2025, and is expected to reach USD 29.30 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

Rapid urbanization and industrial expansion in Asia-Pacific are fueling a surge in plastic consumption and waste production. Notably, urban centers in countries like China and India stand out as primary plastic waste generators. Governments in the APAC region are responding with increasingly stringent measures. These include bans on single-use plastics, the introduction of extended producer responsibility (EPR) programs, and incentives to promote recycling. For instance, China has enforced a ban on plastic waste imports, while India has rolled out its own set of plastic waste management regulations.

Technological advancements in recycling, spanning from sophisticated sorting systems to chemical and biodegradable recycling methods, are reshaping the plastic waste management landscape. Simultaneously, there is a rising trend in adopting digital waste tracking and management solutions. As public awareness of environmental issues surrounding plastic pollution grows, consumers demand more sustainable products and responsible waste management. This, in turn, pushes companies toward eco-friendly practices and substantial investments in recycling infrastructure.

The economic potential of the plastic waste management market in Asia-Pacific is vast, especially in areas like collection, sorting, recycling, and waste-to-energy technologies. As a result, investments in recycling infrastructure and waste management facilities are rising. However, challenges persist, including inadequate waste management infrastructure in several APAC nations, low recycling rates, and the prevalence of mixed and contaminated plastic waste. Addressing these challenges will require infrastructure upgrades and heightened public awareness and engagement in waste segregation.

Asia-Pacific Plastic Waste Management Market Trends

Rapid Urbanization Exacerbates Escalating Plastic Predicament in Asia-Pacific

With a population of approximately 4 billion, Asia-Pacific (APAC) is witnessing rapid urbanization, exacerbating its escalating plastic predicament. A UN report highlights that APAC already hosts 28 megacities, and an estimated 120,000 individuals are relocating to urban centers in the region daily. Projections suggest that a staggering 3.3 billion people will live in cities in Asia-Pacific by the year 2050. This surge in urbanization has fueled consumption, notably spiking the demand for single-use packaging, especially in the flexible plastic segment. If the current trajectory persists, APAC is set to generate a colossal 140 million tonnes of plastic waste by 2030.

Given that many of the world's most populous countries reside in the APAC region, the surge in urbanization is accompanied by shifting lifestyles and heightened appetites for packaged goods. Flexibility in packaging emerges as a focal concern in APAC. The region's allure for production, especially in the food sector, is bolstered by its lower associated costs. In 2023, APAC commanded a 52.2% share in the flexible packaging market. Noteworthy players like Uflex and Fuji Seal International fortify the industry's standing in the region. APAC's penchant for single-use plastic packaging, notably in pouches and sachets (e.g., single-serve water packages in India), is largely due to the cost advantage these materials offer.

The case of single-use plastic bags in Indonesia vividly illustrates the efficacy of APAC regulations. Following a successful trial in 23 cities and municipalities, Jakarta enforced a blanket ban on plastic bags in July 2020. Despite initial pushback from businesses, the regulation was upheld, with non-compliant companies facing fines and repeat offenders risking permit revocation.

The reported results indicate the ban's success. In 2018, Jakarta consumed an estimated 240-300 million plastic bags annually. By 2021, this consumption had dropped by 42%, from 11,192 tons to 6,452 tons.

On a global scale, Bangladesh led the way by implementing a national plastic bag ban in 2002. China initiated its ban in 2020, with the final phase set for 2025. India also joined the movement, implementing a ban on single-use plastics in 2022.

Despite these advancements, parts of the Asia-Pacific (APAC) region are struggling to keep pace. South Korea consumes a staggering 19 billion plastic bags each year, as reported by the Korea Zero Waste Movement Network. Meanwhile, Thailand's government survey revealed an annual consumption of around 200 billion plastic bags, translating to an average of eight bags per citizen per day. The Ocean Conservancy highlights Thailand as the sixth-largest contributor to global marine waste.

The conclusion is that despite notable progress in plastic regulation across various APAC nations, the region still needs to overcome significant plastic consumption and waste management challenges. Stringent enforcement and innovative solutions are imperative to address this, especially given the region's rapid urbanization.

China is Making Strides in Waste Management

In 2023, China's initiative, spearheaded by over 6,000 individuals and 200+ enterprises from Zhejiang, clinched the UN's top environmental accolade for its strides in tackling marine plastic waste. The program offers a transparent view of marine plastics' recycling journey, aiding local fishermen and notably curbing pollution in coastal waters. Since its inception, the project has engaged over 61,600 participants and collected approximately 10,936 tons of marine debris, 2,254 tons of which were plastic waste.

China's commitment to waste management is evident through substantial investments in infrastructure and technology. The nation is pioneering initiatives like waste-to-energy plants and cutting-edge recycling centers to slash landfill contributions. Zhejiang Province in eastern China unveiled the "Zhejiang Food Delivery Plastic Zero Waste Program," targeting reducing and recycling plastics used in food delivery. The initiative was aimed at establishing a "zero waste" model for food delivery plastics in key sectors, notably universities, by the end of 2023. By 2025, this model will be rolled out across schools, commercial spaces, and communities.

Zhejiang's strategy involves a collaborative effort, uniting stakeholders like food delivery platforms, merchants, universities, disposal firms, and recycling associations to form a unified front against plastic waste in food delivery. Zhejiang also plans to install waste collection facilities in areas with heightened plastic waste, tasking food delivery platforms with setting up these facilities in locations like university dorms and cafeterias, with the universities handling their maintenance.

Overall, China's commitment to tackling waste, which is evident in Zhejiang's "Plastic Zero Waste Program," showcases the nation's innovative and collaborative efforts to combat plastic pollution. These initiatives are pioneering and establishing a blueprint for the broader APAC region.

Asia-Pacific Plastic Waste Management Industry Overview

In Asia-Pacific, the plastic waste management market is highly fragmented, featuring a mix of local and global players. This diversity stems from the unique waste management requirements and regulatory frameworks that vary from country to country. Some of the key players in this sector are Hitachi Zosen Corporation, Polimaster, Banyan Nation, Lucro, and Recity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Plastic Consumption

- 4.2.2 Stricter Regulations and Policies Aimed at Reducing Plastic Waste

- 4.3 Market Restraints

- 4.3.1 High Cost Associated with Establishing and Maintaining Facilities

- 4.4 Market Opportunities

- 4.4.1 Innovations in Recycling Technologies

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Insights into Technological Innovation in the Market

5 MARKET SEGMENTATION

- 5.1 By Polymer

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene (PE)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Terephthalate (PET)

- 5.1.5 Other Polymers

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Other Sources (Construction, Healthcare, etc.)

- 5.3 By Treatment

- 5.3.1 Recycling

- 5.3.2 Chemical Treatment

- 5.3.3 Landfill

- 5.3.4 Other Treatments

- 5.4 By Country

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Hitachi Zosen Corporation

- 6.2.2 Polimaster

- 6.2.3 Banyan Nation

- 6.2.4 Lucro

- 6.2.5 Recity

- 6.2.6 SUEZ

- 6.2.7 Waste Management Inc.

- 6.2.8 Cleanaway Waste Management Limited

- 6.2.9 Plastic Bank

- 6.2.10 Agilyx

- 6.2.11 GreenTech Environmental Co. Ltd