|

市場調査レポート

商品コード

1636426

ゼロウェイスト食料品店:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Zero-Waste Grocery Stores - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゼロウェイスト食料品店:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

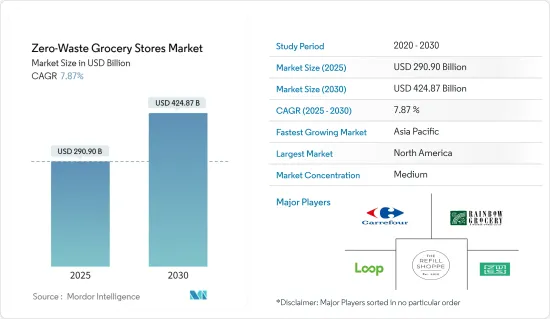

ゼロウェイスト食料品店の市場規模は、2025年に2,909億米ドルと推計され、2030年には4,248億7,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは7.87%です。

廃棄物ゼロの店舗は小売情勢を再構築し、プラスチックや包装を使わないショッピング体験を顧客に提供しています。こうした店舗は主に詰め替え用やバルクフーズオプションに重点を置き、買い物客に食品、パーソナルケア、クリーニング製品用の容器を持参するよう促しています。このような店舗の数は世界的に増加しており、オンライン・プラットフォームでクラウドファンディングを募っている店舗も多いです。包装材を使わないだけでなく、廃棄物ゼロの店舗は、ホリスティックで持続可能な理念を掲げていることが多く、地元産やオーガニックの商品を幅広く紹介しています。この独特なアプローチは、従来の小売店とは一線を画し、ニッチな分野を切り拓いています。

持続可能なショッピング・ムーブメントの最前線に立つゼロウェイスト食料品店は、コンセプトだけでなく、実践においても声明を出しています。そのインパクトは、廃棄物削減への取り組みだけでなく、大手食料品小売チェーンの反応を刺激していることからも明らかです。米国のスーパーマーケットは、食品販売店のわずか10%を占めるにすぎないにもかかわらず、年間の食品廃棄量に数十億米ドルという巨額を上乗せしています。さらに、食品包装だけで、埋め立て廃棄物全体の23%を占めています。

ゼロウェイスト食料品店の市場動向

ゼロウェイスト食料品店はスーパーマーケットとハイパーマーケットで増殖し、成長を促進する

多様な商品を提供することで知られるスーパーマーケットやハイパーマーケットでは、流通チャネルにゼロウェイスト食料品店を含める動きが急増しています。これらの店舗は、ラップや袋、ストローといった従来の包装に代わるものを提供することで、使い捨てプラスチックと闘うまたとない機会を提供しています。にもかかわらず、伝統的なスーパーマーケットやハイパーマーケットは、特に生鮮食品において、依然として人気の高い買い物先です。特に、使い捨てプラスチック包装から脱却したスーパーマーケットでは、野菜の売上が著しく急増しました。環境面でのメリットだけでなく、廃棄物をゼロにすることは、人件費、エネルギー、廃棄費用を削減し、企業にとって大幅なコスト削減につながります。

オンライン小売チャネルは、予測期間中に最も急速に成長する見込みです。この勢いは、世界のオンラインショッピングの増加によるもので、消費者行動の明確な変化を示しています。

市場をリードする北米

環境意識が高まるにつれて、プラスチック廃棄物の影響に対する監視の目も厳しくなっています。米国とカナダの個人は、持続可能性に向けた運動の先頭に立っています。このシフトを後押しするように、この地域の政府は環境廃棄物を管理するイニシアチブを展開しており、今後数年で市場が大きく成長する舞台を整えています。店舗が積極的に廃棄物を削減していることは明らかだが、大手小売スーパーマーケット・チェーンもこの動向を取り入れています。

スーパーマーケットだけでも、米国で年間排出される食品廃棄物の10%を占めています。さらに、食品包装は埋め立てゴミの23%を占めています。ケア・フード、クローガー、ウォルマートなどの大手企業が主導する「10x20X30イニシアティブ」を通じて、今後10年間で食品廃棄物を削減することを目標としています。2030年までに、これらの大手小売業者はそれぞれ少なくとも20のサプライヤーと協力し、廃棄物削減の努力をさらに進めることを目指しています。持続可能な買い物の推進が勢いを増すにつれ、廃棄物ゼロの店舗が新たな常識となりそうです。

ゼロウェイスト食料品店業界の概要

ゼロウェイスト食料品店市場は半固有の状況を示しており、現在利用可能な選択肢はほんの一握りです。本レポートでは、以下のような主要企業を取り上げ、競合のダイナミクスを掘り下げています。 Rainbow Grocery, Loop, Zero Waste Eco Store, Carrefour, and The Refill Shoppe.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 環境意識の高まりが市場を牽引

- 環境に優しい選択肢を求める消費者の需要が市場の成長を促進

- 市場抑制要因

- 初期設定コストの高さが市場の成長を妨げる

- 店舗における衛生基準維持のための物流課題

- 市場機会

- 地元生産者やサプライヤーとのパートナーシップの可能性

- オンライン販売のためのデジタル・プラットフォームの活用

- バリューチェーン分析

- 業界の魅力ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 業界の技術的進歩に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- 専門店

- オンラインストア

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Rainbow Grocery

- Loop

- Zero Waste Eco Store

- Carrefour

- The Refill Shoppe

- Just Gaia

- Zero Muda

- EcoRefill

- ecoTopia

- Lidl*

第7章 今後の市場動向

第8章 免責事項および出版社について

The Zero-Waste Grocery Stores Market size is estimated at USD 290.90 billion in 2025, and is expected to reach USD 424.87 billion by 2030, at a CAGR of 7.87% during the forecast period (2025-2030).

Zero waste stores are reshaping the retail landscape, offering customers a plastic and packaging-free shopping experience. These stores primarily focus on refill and bulk options, encouraging shoppers to bring their containers for food, personal care, and cleaning products. The global count of such stores has surpassed, with many new ones seeking crowdfunding on online platforms. Beyond being packaging-free, zero-waste stores often champion a holistic, sustainable ethos, showcasing a range of local and organic products. This distinctive approach sets them apart from traditional retailers, carving a niche for themselves.

Zero-waste grocery stores, at the forefront of the sustainable shopping movement, are making a statement not just in concept but also in practice. Their impact is evident, not only in their waste reduction efforts but also in catalyzing responses from major retail grocery chains. Despite accounting for just 10% of food outlets, US supermarkets add massive billions of dollars to the total yearly food waste. Furthermore, food packaging alone constitutes 23% of all landfill waste.

Zero-Waste Grocery Stores Market Trends

Zero-Waste Grocery Stores Proliferate in Supermarkets and Hypermarkets, Propelling Growth

Supermarkets and hypermarkets, known for their diverse product offerings, have seen a surge in the inclusion of zero-waste grocery stores within their distribution channels. These stores present a unique opportunity to combat single-use plastic by offering alternatives to traditional packaging, such as plastic wraps, bags, and straws. Despite this, traditional supermarkets and hypermarkets remain popular shopping destinations, especially for fresh produce. Notably, supermarkets that transitioned away from single-use plastic packaging witnessed a remarkable surge in vegetable sales. Beyond the environmental benefits, going zero-waste also translates to significant cost savings for businesses, cutting down on labor, energy, and disposal expenses.

The online retail channel is poised for the swiftest growth during the forecast period. This momentum is fueled by the global uptick in online shopping, indicating a clear shift in consumer behavior.

North America Leading the Market

As environmental consciousness rises, so does the scrutiny of the repercussions of plastic waste. Individuals in the United States and Canada are spearheading the movement toward sustainability. Bolstering this shift, governments in the region have rolled out initiatives to manage environmental waste, setting the stage for significant market growth in the coming years. While it's evident that stores are actively reducing waste in their operations, major retail supermarket chains are also embracing this trend.

Supermarkets alone contribute to 10% of food waste produced annually in the United States. Additionally, food packaging constitutes a significant 23% of landfill waste. Through the "10x20X30 Initiative," spearheaded by major players like Kea Food, Kroger, and Walmart, the goal is to slash food waste over the next decade. By 2030, these leading retailers aim to collaborate with at least 20 suppliers each, furthering their waste reduction efforts. As the push for sustainable shopping gains momentum, zero-waste stores are set to become the new norm.

Zero-Waste Grocery Stores Industry Overview

The zero-waste grocery store market exhibits a semi-consolidated landscape, with only a handful of options available presently. The report delves into the competitive dynamics, highlighting key players such as Rainbow Grocery, Loop, Zero Waste Eco Store, Carrefour, and The Refill Shoppe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Environmental Consciousness Driving the Market

- 4.2.2 Consumer Demand for Eco-friendly Options Fuels Growth of the Market

- 4.3 Market Restraints

- 4.3.1 Higher Initial Setup Costs Hinder Growth of the Market

- 4.3.2 Logistical Challenges in Maintaining Hygiene Standards in Stores

- 4.4 Market Opportunities

- 4.4.1 Potential Partnerships with Local Producers and Suppliers

- 4.4.2 Leveraging Digital Platforms for Online Sales

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Distribution Channel

- 5.1.1 Supermarkets/Hypermarkets

- 5.1.2 Speciality Stores

- 5.1.3 Online Stores

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Italy

- 5.2.2.6 Spain

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Rainbow Grocery

- 6.2.2 Loop

- 6.2.3 Zero Waste Eco Store

- 6.2.4 Carrefour

- 6.2.5 The Refill Shoppe

- 6.2.6 Just Gaia

- 6.2.7 Zero Muda

- 6.2.8 EcoRefill

- 6.2.9 ecoTopia

- 6.2.10 Lidl*