|

市場調査レポート

商品コード

1636213

建設廃棄物管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Construction Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 建設廃棄物管理:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

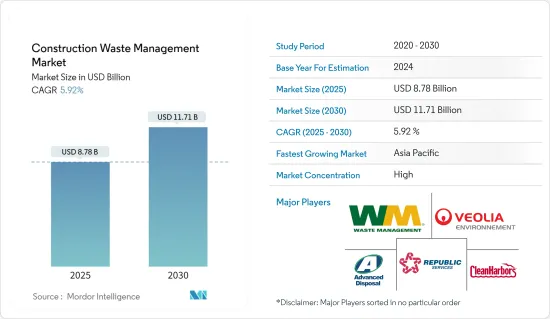

建設廃棄物管理の市場規模は2025年に87億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.92%で、2030年には117億1,000万米ドルに達すると予測されます。

主なハイライト

- 急速な都市化と持続可能性の重視の高まりが、建設廃棄物管理市場の主な促進要因です。現在、建設資材廃棄物の75%以上は、固有の価値があるにもかかわらずリサイクルされないままです。2018年、環境保護庁(EPA)は、建設廃棄物が家庭と企業の両方から出る一般廃棄物の2倍であることを強調しました。米国は家庭からの廃棄物排出量で世界首位です。

- 建設・解体(C&D)廃棄物のカテゴリは、コンクリート、アスファルト、木材、レンガ、粘土タイル、石膏乾式壁、アスファルトシングル、金属などの材料に及ぶ。コンクリートや金属は容易にリサイクル可能だが、その他の材料、特にレンガ、粘土瓦、石膏乾式壁は再利用が難しく、埋立地行きになることが多いです。

- 急速な都市化が進むインドでは、建設部門が大気汚染の主要な原因であり、資源の大量消費者であるとの認識が高まっています。特に、インドの資源採取量は1エーカーあたり1,580トンと、世界平均の450トンをはるかに上回っています。

- 国家大気浄化計画は、インドの131の非汚染都市に対し、2026年までに粒子状物質汚染を40%削減するという厳しい目標を設定しています。その結果、建設・解体(C&D)廃棄物の効果的な管理は、汚染レベルを抑制する上で最重要課題となっています。

- しかし、最近のCSEレビューでは、多くの都市が体系的かつ科学的なC&D廃棄物管理を行う体制が整っていないという、懸念すべき動向が浮き彫りになっています。さらに、2016年のC&D廃棄物管理規則の採択は遅々として進まず、その実行には顕著なギャップがあります。このことは、制度設計の理解と効果的な実施のための戦略の両方を強化する包括的なガイダンスの緊急の必要性を強調しています。

- ハードルにもかかわらず、建設部門は持続可能性において進歩を示しており、廃棄物の75%以上を再利用することに成功しています。特に、米国が廃棄物総排出量のわずか3分の1しかリサイクルしていないことを考えると、リサイクル活動は廃棄物管理業務の85%以上を占めており、その重要性は明らかです。

- 規制機関や建設会社が廃棄物抑制への取り組みを強化する中、建設廃棄物管理市場は拡大に向かっています。リーンコンストラクションやバリューエンジニアリングのようなアプローチは、プロジェクト開始時から廃棄物削減に磨きをかけ、事後計画サービスは効率的な廃棄物撤去・処分ソリューションを提供しています。

建設廃棄物管理市場の動向

住宅建設廃棄物が市場で大きなシェアを占める

住宅建設廃棄物は、世界の建設廃棄物問題の大きな原因となっており、効果的な廃棄物管理の緊急性が強調されています。予測では、2025年までに世界の建設廃棄物は年間22億トンに増加するとされており、これは主に住宅プロジェクトや改築に起因しています。

米国内では、住宅廃棄物を含む建設・解体(C&D)廃棄物が、国の廃棄物総排出量の実に25%を占めています。この統計は、住宅から排出される廃棄物の多さを際立たせるだけでなく、商業施設や公共施設からの廃棄物の多さをも示しています。

住宅建設廃棄物に含まれる一般的な材料は、木材、乾式壁、コンクリート、梱包材などです。驚くべきことに、建設現場に搬入される資材の約30%が廃棄物となり、この部門の資材効率の悪さを際立たせています。

管理されていない建設廃棄物の影響は深刻で、環境汚染や資源の枯渇につながります。生態系の破壊とそれに続く汚染は、野生生物と公衆衛生の両方に影響を及ぼし、広範囲に及ぶ結果をもたらす可能性があります。

資材のリサイクルや再利用といった持続可能な手法を取り入れることは、住宅建設廃棄物の急増を抑制するための実行可能な解決策となります。無駄のない建設や堅実な廃棄物管理計画といった戦略は、住宅建設における廃棄物排出量を大幅に削減する有望な手段です。

アジア太平洋が市場で大きなシェアを占める

アジアにおける建設廃棄物管理は、国によって大きな格差があります。日本、香港、シンガポールのような国々は、リサイクルと適切な処分を重視する先進的なシステムで際立っています。韓国は97%を超える驚異的なリサイクル率を誇り、台湾もリサイクル率50%を突破するなど躍進しています。対照的に、多くの開発途上国はリサイクル率の低さに悩んでおり、多くの場合、課題だらけの野外投棄に頼っています。

建設廃棄物管理に関するアジアの規制状況は多様だが、共通しているのは、地方自治体の責任に重点を置いていることです。特筆すべきは、インドのような国が廃棄物管理の監督を強化するための規制を制定していることです。包括的な法律の一部であるこれらの規制は、建設廃棄物処理のコンプライアンスと効率性を高めることを目的としています。

進展が見られるとはいえ、アジアは建設廃棄物管理において根強い課題に直面しています。資金不足や標準化された慣行の欠如から、不法投棄や不十分な廃棄物処理インフラまで、問題は多岐にわたる。さらに、特に開発途上国では、非正規の廃棄物産業や複雑な政府の責任が、効果的な廃棄物管理をさらに妨げています。

今後、アジアの建設廃棄物管理市場は成長を遂げると思われます。この成長軌道は、都市化の進展と持続可能性への関心の高まりに後押しされています。今後予想されるリサイクル技術の革新は、規制の厳格化と相まってリサイクル率を大幅に押し上げると思われます。さらに、建設会社と廃棄物管理事業体との協力関係の強化により、廃棄物管理基準の遵守が強化され、循環型経済が促進されると予想されます。

建設廃棄物管理業界の概要

建設廃棄物管理市場は細分化されています。複数の主要企業が、建設プロジェクト向けに効率的で持続可能な廃棄物管理ソリューションを提供しようと競い合っています。この分野で注目すべき企業には、Waste Management、Veolia Environment、Clean Harbors、Republic Services、Advanced Disposal Servicesなどがあります。これらの企業は、廃棄物収集、リサイクル、埋立地管理、環境コンサルティングなど幅広いサービスを提供し、建設会社が規制要件や環境基準を遵守しながら廃棄物を効果的に管理できるよう支援しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 市場を牽引する都市化と人口増加

- 市場を牽引する経済成長

- 抑制要因

- 市場に影響を与える規制の枠組み

- リサイクル・プロセスに伴う高コストが市場に影響

- 機会

- 市場を牽引する技術の進歩

- 促進要因

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 廃棄物リサイクルサービス市場における技術開拓

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 廃棄物タイプ別

- 有害

- 非有害

- 発生源別

- 住宅

- 非住宅

- 材料別

- コンクリート・レンガ

- 木材

- 金属

- プラスチック

- ガラス

- その他の材料(土壌、乾式壁、しっくいなど)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Waste Management

- Veolia Environment

- Clean Harbors

- Republic Services

- Advanced Disposal Services

- Biffa

- Covanta Holding

- Daiseki

- Hitachi Zosen

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標

- 資本フローの洞察(建設セクターへの投資)

- 対外貿易統計

The Construction Waste Management Market size is estimated at USD 8.78 billion in 2025, and is expected to reach USD 11.71 billion by 2030, at a CAGR of 5.92% during the forecast period (2025-2030).

Key Highlights

- Rapid urbanization and a growing emphasis on sustainability are the primary drivers of the construction waste management market. Currently, over 75% of construction material waste remains unrecycled despite its inherent value. In 2018, the Environmental Protection Agency (EPA) highlighted that construction waste doubled that of municipal waste from both households and businesses. The United States leads globally in household waste generation.

- The construction and demolition (C&D) waste category spans materials like concrete, asphalt, wood, brick, clay tiles, gypsum drywall, asphalt shingles, and metal. While concrete and metal are readily recyclable, others, especially brick, clay tiles, and gypsum drywall, face reusability challenges, often ending up in landfills.

- In India, amid rapid urbanization, the construction sector is increasingly recognized as a key source of air pollution and a substantial consumer of resources. Notably, India's resource extraction rate, at 1,580 tonnes per acre, far exceeds the global average of 450 tonnes per acre.

- The National Clean Air Programme has set a stringent target for the 131 non-attainment cities in India: a 40% reduction in particulate pollution by 2026. Consequently, effective management of construction and demolition (C&D) waste has become paramount in curbing pollution levels.

- However, a recent CSE review highlights a concerning trend: many cities lack the institutional readiness for systematic and scientific C&D waste management. Moreover, the adoption of the C&D Waste Management Rules of 2016 has been sluggish, with noticeable gaps in their execution. This underscores the urgent need for comprehensive guidance to enhance both the understanding of the system's design and the strategies for its effective implementation.

- Despite hurdles, the construction sector has shown progress in sustainability, managing to repurpose more than 75% of its waste. Notably, recycling activities account for over 85% of waste management jobs, underscoring their significance, especially when considering that the United States recycles only a third of its total waste output.

- With regulatory bodies and construction companies intensifying their efforts to curb waste, the construction waste management market is set for expansion. Approaches like lean construction and value engineering are honing in on waste reduction from the project's inception, while post-planning services are offering efficient waste removal and disposal solutions.

Construction Waste Management Market Trends

Residential Construction Waste Holds a Significant Share of the Market

Residential construction waste is a significant contributor to the global construction debris challenge, emphasizing the urgency of effective waste management. Projections suggest that annual construction waste worldwide will escalate to 2.2 billion tons by 2025, largely driven by residential projects and renovations.

Within the United States, construction and demolition (C&D) debris, including residential waste, constitute a striking 25% of the nation's total waste output. This statistic not only underscores the substantial waste from residential endeavors but also highlights the significant contributions from commercial and institutional construction.

Common materials in residential construction waste encompass wood, drywall, concrete, and packaging materials. Alarmingly, around 30% of materials delivered to construction sites end up as waste, accentuating the sector's material inefficiency.

The ramifications of unmanaged construction waste are dire, leading to environmental pollution and resource depletion. Ecosystem disruptions and subsequent pollution can have far-reaching consequences, affecting both wildlife and public health.

Embracing sustainable practices, like material recycling and reusing, presents a viable solution to curbing the surge in residential construction waste. Strategies such as lean construction and robust waste management plans hold promise in significantly reducing waste output during residential endeavors.

Asia-Pacific Holds a Significant Share of the Market

Construction waste management practices in Asia exhibit significant disparities across nations. Countries like Japan, Hong Kong, and Singapore stand out for their advanced systems, emphasizing recycling and proper disposal. South Korea boasts an impressive recycling rate exceeding 97%, while Taiwan has also made strides, surpassing a 50% recycling rate. In contrast, many developing nations grapple with low recycling rates, often resorting to open dumping, a practice laden with challenges.

Asia's regulatory landscape for construction waste management is diverse, with a common thread: a focus on local authorities' responsibilities. Notably, countries like India are enacting regulations to bolster oversight of waste management practices. These regulations, part of comprehensive acts, aim to enhance compliance and efficiency in handling construction waste.

Despite progress, Asia faces persistent challenges in construction waste management. Issues range from funding shortages and a lack of standardized practices to illegal dumping and inadequate waste processing infrastructure. Moreover, informal waste industries and complex governmental responsibilities further hinder effective waste management, particularly in developing nations.

Looking forward, Asia's construction waste management market is set for growth. This trajectory is fueled by rising urbanization and an amplified focus on sustainability. Anticipated innovations in recycling technologies, coupled with stricter regulations, are poised to significantly boost recycling rates. Moreover, increased collaboration between construction firms and waste management entities is expected to bolster compliance with waste management standards and foster a circular economy.

Construction Waste Management Industry Overview

The construction waste management market is fragmented in nature. Several key players are competing to provide efficient and sustainable waste management solutions for construction projects. Some notable companies in this space include Waste Management, Veolia Environment, Clean Harbors, Republic Services, and Advanced Disposal Services. These companies offer a range of services such as waste collection, recycling, landfill management, and environmental consulting to help construction firms effectively manage their waste while adhering to regulatory requirements and environmental standards.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Urbanization and Population Growth Driving the Market

- 4.2.1.2 Economic Growth Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Regulatory Frameworks Affecting the Market

- 4.2.2.2 High Costs Associated with the Recycling Process Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Technological Advancements Driving the Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Developments in the Waste Recycling Services Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Waste Type

- 5.1.1 Hazardous

- 5.1.2 Non-hazardous

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Non-residential

- 5.3 By Material

- 5.3.1 Concrete & Bricks

- 5.3.2 Wood

- 5.3.3 Metal

- 5.3.4 Plastics

- 5.3.5 Glass

- 5.3.6 Other Materials (Soil, Drywall, Plaster, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Italy

- 5.4.2.6 Spain

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Waste Management

- 6.2.2 Veolia Environment

- 6.2.3 Clean Harbors

- 6.2.4 Republic Services

- 6.2.5 Advanced Disposal Services

- 6.2.6 Biffa

- 6.2.7 Covanta Holding

- 6.2.8 Daiseki

- 6.2.9 Hitachi Zosen

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators

- 8.2 Insights into Capital Flows (Investments in Construction Sector)

- 8.3 External Trade Statistics