アジア太平洋の廃棄物管理:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636203

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

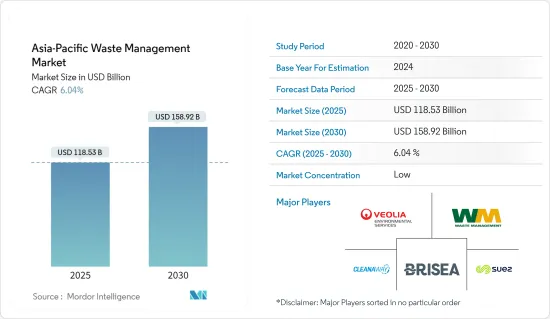

アジア太平洋の廃棄物管理市場規模は、2025年に1,185億3,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは6.04%で、2030年には1,589億2,000万米ドルに達すると予測されています。

過去50年間、廃棄物の発生量はすべての国で増加しています。しかし、日本と韓国は最近減少を見せています。例えば、韓国で進行中の拡大生産者責任(EPR)制度は、製品メーカーに製品から出る廃棄物の回収とリサイクルを義務付けています。こうした政府の取り組みや規制は、廃棄物処理会社が国内で効果的に事業を展開するのに役立っています。

廃棄物管理プロセスにIoT、AI、ロボット工学などの最先端技術を採用することは、産業に革命をもたらしています。2023年9月、インドのメガラヤ州はAIを活用した廃棄物管理方法を導入しました。AI対応のロボットボートが、湖に捨てられた大量のゴミを回収するのです。手作業に比べ、このプロセスは効果的で時間もかからないです。

アジア太平洋ではリサイクル材料の需要が増加しています。各国は、廃棄物を再利用可能な材料に加工するための先進的リサイクル技術に投資しており、リサイクル事業者に新たな市場機会を生み出しています。

例えば、2024年5月、蔚山大学校(UC)と蔚山国際開発協力センター(UIDCC)は、UNEPの国際環境技術センターと共同で、韓国の蔚山で5日間の能力開発プログラムを開催しました。このイベントでは、プラスチックリサイクル技術の進歩が発表され、環境イニシアティブへの地域社会の参加が強調されました。

アジア太平洋の廃棄物管理市場の動向

アジア太平洋の廃棄物管理を牽引するプラスチック廃棄物

- アジア太平洋は、管理不行き届きのプラスチック廃棄物の膨大な量に悩まされており、より効果的な廃棄物管理ソリューションを求める声が世界的に高まっています。この緊急性が、先進的廃棄物管理技術とインフラ強化への需要を高めています。これに後押しされ、民間団体や政府は最先端の廃棄物処理・リサイクル技術の開発・導入への投資を増やしています。

- 例えば、2024年には、中国がアジア太平洋諸国におけるプラスチック廃棄物の誤処理で首位に立ち、その量は推定5,500万トンに上ります。同じ年にはニュージーランドが突出し、誤処理プラスチック廃棄物8,410トンを占めました。

- 2024年6月、オーストラリアの連邦委員会は、国内の水域におけるプラスチック汚染と闘うための22の勧告を行った。2022年11月、オーストラリアは「プラスチック汚染根絶のための高い志連合」に参加し、プラスチック汚染抑制へのコミットメントをさらに強調しました。この連合は、新たな条約によって2040年までに世界のプラスチック汚染を根絶することを目指しています。

- これらの行動は、アジア太平洋における廃棄物管理の状況を形成し、先進的リサイクル技術、廃棄物収集システムの強化、革新的な廃棄物削減戦略の差し迫った必要性を強調しています。

中国の廃棄物管理イニシアティブが市場の成長とイノベーションを促進

- 中国国家統計局のデータによると、2022年現在、中国には約444カ所の衛生埋立地があることが明らかになりました。過去10年間、中国の廃棄物排出量は着実に増加しており、2022年には約2億4,450万トンに達します。

- さらに、中国で発生する通常の固形産業廃棄物の量は、2022年には410億トンに達します。この廃棄物排出量の急増は、中国における先進的廃棄物管理技術とサービスの緊急ニーズを浮き彫りにしており、この動向がアジア太平洋廃棄物管理市場の成長と技術革新を促進すると期待されています。

- 中国はこの廃棄物課題に対処するため、2017年に全国的な廃棄物分別キャンペーンを開始しました。2020年までに、80以上の都市が、食品廃棄物、リサイクル可能物、有害廃棄物、残余物などのカテゴリーへの都市ごみの分による義務化を完全に実施、または検査的に実施しています。2025~2030年にかけて、この分別システムを全都市に拡大する計画です。この取り組みは、廃棄物管理セグメントの成長と技術革新に拍車をかけ、アジア太平洋全体の投資と技術進歩を促進すると期待されています。

アジア太平洋の廃棄物管理産業概要

アジア太平洋の廃棄物管理市場は、地元企業や世界企業が大半を占め、廃棄物収集、リサイクル、有害廃棄物処理などのサービスを提供しています。Suez Environment SA、Veolia Environmental Services、Waste Management Inc.などの産業大手企業が最前線に立ち、その豊富な専門知識と最先端技術を駆使して、地域全体に総合的な廃棄物管理ソリューションを提供しています。

一方、オーストラリアのCleanaway Waste Managementや日本のDaisekiのような地域企業も、地域の需要や規制枠組みに合わせたサービスを提供し、注目すべき市場シェアを占めています。BRISEA Group Inc.、Attero、Remondis AG &Co.Kgといった注目すべき企業が、先進的なリサイクルと廃棄物処理技術を支持しています。これらの企業は一体となって、このセグメントを再構築し、世界のベストプラクティスを導入し、持続可能性を支持し、アジア太平洋における効果的な廃棄物管理ソリューションの急増するニーズに応えています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- サプライチェーン/バリューチェーン分析に関する洞察

- 産業の規制に関する洞察

- 産業の技術的進歩に関する洞察

第5章 市場力学

- 市場促進要因

- 急速な都市化と人口増加

- 政府の規制と取り組み

- 市場抑制要因

- 文化的・行動的障壁

- 農村部のインフラ不足

- 市場機会

- 成長するリサイクル市場

- 廃棄物エネルギー化技術

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 廃棄物タイプ別

- 産業廃棄物

- 都市固形廃棄物

- 電子廃棄物

- プラスチック廃棄物

- 医療廃棄物とその他の廃棄物(建設廃棄物を含む)

- 処分方法別

- 埋立処分

- 焼却

- リサイクル

- その他の処分方法

- 国別

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Suez Environment SA

- Waste Management Inc.

- Cleanaway Waste Management

- Veolia Environmental Services

- BRISEA Group Inc.

- Attero

- Remondis AG & Co. Kg

- Daiseki Co. Ltd

- Averda

- Clean Harbors Inc.*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

目次

The Asia-Pacific Waste Management Market size is estimated at USD 118.53 billion in 2025, and is expected to reach USD 158.92 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

Over the past 50 years, waste generation has risen across all nations. However, Japan and Korea have recently shown a decline. For example, Korea's ongoing Extended Producer Responsibility (EPR) scheme mandates that product manufacturers collect and recycle the waste from their products. These governmental initiatives and regulations have helped waste management companies to operate effectively within the country.

Adopting cutting-edge technologies such as IoT, AI, and robotics in waste management processes is revolutionizing the industry. In September 2023, the Indian state of Meghalaya introduced an AI-enabled waste management method. The AI-enabled robotic boat collects vast quantities of garbage dumped in a lake. Compared to manual labor, this process is effective and less time-consuming.

The APAC region is seeing an increase in the demand for recycled materials. Countries are investing in advanced recycling technologies to process waste into reusable materials, creating new market opportunities for recycling businesses.

For instance, in May 2024, Ulsan College (UC) and the Ulsan International Development Cooperation Center (UIDCC) hosted a five-day capacity-building program in Ulsan, Republic of Korea, in partnership with the UNEP's International Environmental Technology Center. This event showcased advancements in plastic recycling technologies and emphasized community involvement in environmental initiatives.

Asia-Pacific Waste Management Market Trends

Plastic Waste Driving Waste Management in Asia-Pacific

- The Asia-Pacific region grapples with a staggering volume of mismanaged plastic waste, propelling a global call for more effective waste management solutions. This urgency accentuates the demand for advanced waste management technologies and infrastructure enhancements. Driven by this, private entities and governments increasingly invest in developing and deploying cutting-edge waste processing and recycling technologies.

- For instance, in 2024, China led the Asia-Pacific nations in mismanaged plastic waste, with an estimated 55 million metric tons. New Zealand stood out in the same year, accounting for 8.41 thousand metric tons of mismanaged plastic waste.

- In June 2024, an Australian federal committee made 22 recommendations to combat plastic pollution in the nation's water bodies. In November 2022, Australia's commitment to curbing plastic pollution was further underscored as it joined the High Ambition Coalition to End Plastic Pollution. This coalition aims to eradicate global plastic pollution by 2040 through a new treaty.

- These actions shape the waste management landscape in the Asia-Pacific and emphasize the pressing need for advanced recycling technologies, enhanced waste collection systems, and innovative waste reduction strategies.

China's Waste Management Initiatives Propel Market Growth and Innovation

- Data from the National Bureau of Statistics of China revealed that the nation had around 444 sanitary landfill sites as of 2022. Over the past decade, China has steadily increased its waste output, reaching approximately 244.5 million tons by 2022.

- Furthermore, the volume of regular solid industrial waste produced in China amounted to 41 billion metric tons in 2022. This surge in waste generation underscores the urgent need for advanced waste management technologies and services in China, a trend expected to drive growth and innovation in the APAC waste management market.

- China launched a nationwide waste sorting campaign in 2017 to address this waste challenge. By 2020, over 80 cities had fully implemented or were piloting mandatory sorting of municipal waste into categories such as food waste, recyclables, hazardous waste, and residuals. The plan is to extend this sorting system to all cities between 2025 and 2030. This initiative is expected to spur growth and innovation in the waste management sector, encouraging investments and technological advancements throughout the APAC region.

Asia-Pacific Waste Management Industry Overview

Local and global entities dominate the waste management market in Asia-Pacific, offering services spanning waste collection, recycling, and hazardous waste treatment. Industry behemoths like Suez Environment SA, Veolia Environmental Services, and Waste Management Inc. stand at the forefront, harnessing their vast expertise and cutting-edge technologies to deliver holistic waste management solutions across the region.

Meanwhile, regional players like Australia's Cleanaway Waste Management and Japan's Daiseki Co. Ltd also command notable market shares, tailoring their services to local demands and regulatory frameworks. Noteworthy entities such as BRISEA Group Inc., Attero, and Remondis AG & Co. Kg are championing advanced recycling and waste processing technologies. Collectively, these firms are reshaping the sector, infusing global best practices, championing sustainability, and meeting the surging need for effective waste management solutions in Asia-Pacific.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights into Supply Chain/Value Chain Analysis

- 4.4 Insights into Governement Regualtions in the Industry

- 4.5 Insights into Technological Advancements in the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Urbanization and Population Growth

- 5.1.2 Government Regulations and Initiatives

- 5.2 Market Restraints

- 5.2.1 Cultural and Behavioral Barriers

- 5.2.2 Lack of Infrastructure in Rural Areas

- 5.3 Market Opportunities

- 5.3.1 Growing Recycling Market

- 5.3.2 Waste-to-Energy Technologies

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Waste Type

- 6.1.1 Industrial Waste

- 6.1.2 Municipal Solid Waste

- 6.1.3 E-waste

- 6.1.4 Plastic Waste

- 6.1.5 Biomedical and Other Waste Types (Including Construction Waste)

- 6.2 By Disposal Methods

- 6.2.1 Landfill

- 6.2.2 Incineration

- 6.2.3 Recycling

- 6.2.4 Other Disposal Methods

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Suez Environment SA

- 7.2.2 Waste Management Inc.

- 7.2.3 Cleanaway Waste Management

- 7.2.4 Veolia Environmental Services

- 7.2.5 BRISEA Group Inc.

- 7.2.6 Attero

- 7.2.7 Remondis AG & Co. Kg

- 7.2.8 Daiseki Co. Ltd

- 7.2.9 Averda

- 7.2.10 Clean Harbors Inc.*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日