|

市場調査レポート

商品コード

1636162

北米のグリーンビルディング:市場シェア分析、産業動向、成長予測(2025~2030年)North America Green Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のグリーンビルディング:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

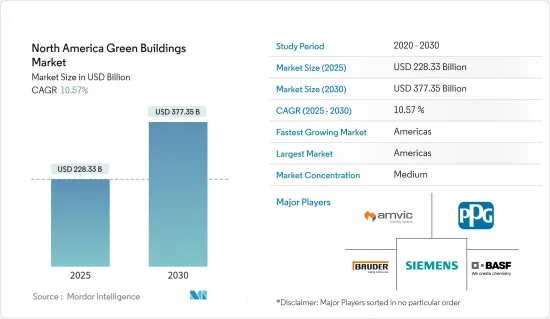

北米のグリーンビルディングの市場規模は2025年に2,283億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは10.57%で、2030年には3,773億5,000万米ドルに達すると予測されます。

米国とカナダでは、連邦、州、地方の環境規制がグリーンビルディングの実践を奨励しています。建築基準法、エネルギー効率基準、排出規制は、持続可能な建設・改修プロジェクトを促進します。

米国のグリーンビルディング協議会(USGBC)やグリーングローブによって設立されたLEED(エネルギー・環境設計におけるリーダーシップ)などの認証プログラムは、持続可能な建築物の設計、建設、運営に関するベンチマークと基準を提供しています。これらのプログラムは、グリーン・ビルディングの実践を奨励し、環境に配慮したプロジェクトを表彰するものです。

エネルギー効率の高いHVACシステム、スマート・ビルディング・オートメーション、再生可能エネルギー・ソリューション(ソーラーパネルや風力タービンなど)、持続可能な材料(リサイクル素材や低排出ガス製品など)など、グリーン・ビルディング技術の進歩は、ビルの性能と持続可能性を高めています。

補助金、リベート、税額控除、低利融資などの金融優遇措置は、グリーン・ビルディング・プロジェクトへの投資を促進します。政府、電力会社、金融機関は、エネルギー効率、再生可能エネルギー導入、持続可能性を促進するために、こうしたインセンティブを提供しています。

多くの政府は、様々なグリーンビルディングの取り組みに対して税額控除を提供しています。例えば、米国連邦政府は太陽エネルギー・システムに対する投資税額控除(ITC)を提供しており、企業や住宅所有者はソーラー・パネルの設置にかかる特定の部分を税金から控除することができます。具体的には、2022年に議会が施行したインフレ削減法に基づき、ITCは2033年まで太陽光発電システム費用の30%で、2035年に失効するまで徐々に減額されます。

同様に、一部の州では、断熱材、エネルギー効率の高い窓、HVACシステムの設置など、エネルギー効率の高い建物のアップグレードに対して税額控除を提供しています。

北米のグリーンビルディング市場動向

スマートビルとIoTの統合による効率と性能の向上

- スマートビルディングとIoT技術の統合は、ビルの設計、建設、運用方法に革命をもたらしています。この動向は、ビル所有者や運営者が効率改善、コスト削減、居住者の快適性向上を求める中で、米国で急速に勢いを増しています。

- 業界専門家によると、米国は2022年に約100.4兆英熱単位の一次エネルギーを消費し、2021年から2.62%増加します。しかし、業界の専門家は、米国における温室効果ガスによる気候変動汚染は2023年に2%近く減少し、好ましい変化であるとも報告しています。

- 米国エネルギー省はまた、センサー、アクチュエーター、コントローラーがスマートビル・エネルギー管理システムの基幹であるとしています。スマート・システムは、集中型デバイスから制御できるサイバー・フィジカル技術であり、室内空気品質やエネルギーなどの要素をリアルタイムで監視・最適化できます。このようなシステムへの投資は、エネルギー価格の妥当性を達成し、削減目標を達成するために不可欠です。

持続可能なビル設計を優先するオフィスが増えている

- 店舗運営におけるエネルギー消費を削減するため、企業はエネルギー効率の高い技術や手法を導入しています。これには、LED照明の改修、稼働センサーを備えたスマートHVACシステム、エネルギー使用量を監視し最適化するエネルギー管理システムなどが含まれます。こうした取り組みは、運営コストを下げ、持続可能性へのコミットメントを示します。

- 多くの企業が、店舗の電力をまかなうために再生可能エネルギー・ソリューションに投資しています。店舗の屋上や駐車場に設置されたソーラーパネルは、クリーンで再生可能なエネルギーを発電し、化石燃料への依存を減らし、二酸化炭素排出量を削減します。また、オフサイトの再生可能エネルギー・プロジェクトに参加したり、再生可能エネルギー・クレジットを購入してカーボンフットプリントを相殺する小売企業もあります。

- 例えば、Amazon.com Inc.の世界237カ所以上のフルフィルメント施設には、屋上に太陽光発電設備が設置されており、施設のエネルギー使用量の最大80%を賄うことができます。第2本社はバージニア州アーリントンにあり、100%再生可能エネルギーで運営されています。2022年には、低炭素コンクリートを使用したデータセンターを16カ所、低炭素スチールを使用したデータセンターを10カ所建設しました。

北米のグリーンビルディング産業の概要

北米では、グリーンビルディング市場の競争は激しいです。主なプレーヤーには、持続可能な建材や技術を提供するインターフェイス社やオーエンズ・コーニング社などの建設メーカーが含まれます。米国のグリーンビルディング協会(USGBC)、LEED認証、グリーン・ビルディング・イニシアティブ(GBI)などの認証機関が業界標準に貢献しています。さらに、地域ごとの規制、インセンティブ、エネルギー効率に対する消費者の需要、環境に対する責任などが、この市場の競争と技術革新を後押ししています。利害関係者間の協力、技術の進歩、持続可能性への注目が、競争情勢をさらに形成しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- グリーンビルディング産業のサプライチェーン/バリューチェーン分析に関する洞察

- プレハブ建築産業で使用されるさまざまな構造に関する概要

- グリーンビルディング産業のコスト構造分析

- COVID-19の影響

第5章 市場力学

- 市場促進要因

- 建設におけるエネルギー効率

- 柔軟性とカスタマイズオプション

- 市場抑制要因

- 建設に適した土地の限られた入手可能性

- 伝統的な建設に比べ低い品質

- 市場機会

- さまざまな分野での需要

- エネルギー効率の高い建設

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 製品別

- エクステリア製品

- インテリア製品

- その他製品(ビルシステム、ソーラーシステムなど)

- エンドユーザー別

- 住宅

- オフィス

- 小売

- 施設

- その他エンドユーザー

- 地域別

- 米国

- カナダ

- メキシコ

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Amvic Inc.

- PPG Industries

- Siemens

- BASF SE

- Bauder Limited

- Forbo International SA

- Owens Corning SA

- CEMEX

- Alumasc Group PLC

- Cold Mix Inc.

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

The North America Green Buildings Market size is estimated at USD 228.33 billion in 2025, and is expected to reach USD 377.35 billion by 2030, at a CAGR of 10.57% during the forecast period (2025-2030).

Federal, state, and local environmental regulations in the United States and Canada incentivize green building practices. Building codes, energy efficiency standards, and emissions regulations promote sustainable construction and renovation projects.

Certification programs such as LEED (Leadership in Energy and Environmental Design), formed by the US Green Building Council (USGBC) and Green Globes, provide benchmarks and standards for sustainable building design, construction, and operation. These programs encourage adopting green building practices and offer recognition for environmentally responsible projects.

Advancements in green building technologies, including energy-efficient HVAC systems, smart building automation, renewable energy solutions (such as solar panels and wind turbines), and sustainable materials (such as recycled content and low-emission products), enhance building performance and sustainability.

Financial incentives such as grants, rebates, tax credits, and low-interest loans encourage investment in green building projects. Governments, utilities, and financial institutions offer these incentives to promote energy efficiency, renewable energy adoption, and sustainability.

Many governments provide tax credits for various green building initiatives. For instance, the U.S. federal government offers the Investment Tax Credit (ITC) for solar energy systems, allowing businesses and homeowners to deduct a particular portion of installing solar panels from their taxes. Specifically, as per the Inflation Reduction Act implemented by Congress in 2022, the ITC is 30% of the solar system cost until 2033 and will gradually reduce until it expires in 2035.

Similarly, some states offer tax credits for energy-efficient building upgrades, such as installing insulation, energy-efficient windows, or HVAC systems.

North America Green Buildings Market Trends

Leveraging Smart Buildings and IoT Integration for Enhanced Efficiency and Performance

- Integrating smart buildings and IoT technologies is revolutionizing how buildings are designed, constructed, and operated. This trend is rapidly gaining momentum in the United States as building owners and operators seek to improve efficiency, reduce costs, and enhance occupant comfort.

- According to industry experts, the United States consumed approximately 100.4 quadrillion British thermal units of primary energy in 2022, a 2.62% increase from 2021. However, industry experts also reported that climate-altering pollution from greenhouse gasses in the United States decreased by nearly 2% in 2023, a positive change.

- The U.S. Department of Energy also states that sensors, actuators, and controllers are the backbone of Smart building energy management systems. Smart systems are cyber-physical technologies that can be controlled from a centralized device, allowing for real-time monitoring and optimization of factors like indoor air quality and energy. Investing in these systems is critical to achieving energy affordability and meeting reduction goals.

Offices Are Increasingly Prioritizing Sustainable Building Designs

- Organizations are implementing energy-efficient technologies and practices to reduce energy consumption in-store operations. These include LED lighting retrofits, smart HVAC systems with occupancy sensors, and energy management systems to monitor and optimize energy usage. These initiatives lower operating costs and demonstrate a commitment to sustainability.

- Many organizations are investing in renewable energy solutions to power their stores. Solar panels installed on store rooftops or parking lots generate clean, renewable energy, reducing reliance on fossil fuels and lowering carbon emissions. Some retailers also participate in offsite renewable energy projects or purchase renewable energy credits to offset their carbon footprint.

- For instance, Amazon.com Inc.'s 237+ global fulfillment facilities have rooftop solar installations, which can power up to 80% of a facility's energy use. Its second headquarters is in Arlington, Virginia, and is powered by 100% renewable energy. In 2022, it constructed 16 data centers using lower-carbon concrete and 10 data centers using lower-carbon steel.

North America Green Buildings Industry Overview

In North America, the green building market is highly competitive. Key players include construction manufacturers like Interface and Owens Corning, which offer sustainable building materials and technologies. Certification bodies like the US Green Building Council (USGBC), LEED certification, and the Green Building Initiative (GBI) contribute to industry standards. Additionally, regional regulations, incentives, consumer demand for energy efficiency, and environmental responsibility drive competition and innovation in this market. Collaboration among stakeholders, technological advancements, and a focus on sustainability further shape the competitive landscape.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis of the Green Buildings Industry

- 4.4 Brief on Different Structures Used in the Prefabricated Buildings Industry

- 4.5 Cost Structure Analysis of the Green Buildings Industry

- 4.6 Impact of COVID 19

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Energy Efficiency in Construction

- 5.1.2 Flexibility and Customization Options

- 5.2 Market Restraints

- 5.2.1 Limited Availability of Suitable Land for Construction

- 5.2.2 Lower Quality Compared to Traditional Construction

- 5.3 Market Opportunities

- 5.3.1 Demand Across Various Sectors

- 5.3.2 Energy Efficient Construction

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Exterior Products

- 6.1.2 Interior products

- 6.1.3 Other Products (Building Systems, Solar Systems, etc.)

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Office

- 6.2.3 Retail

- 6.2.4 Institutional

- 6.2.5 Other End Users

- 6.3 By Geography

- 6.3.1 United States

- 6.3.2 Canada

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Amvic Inc.

- 7.2.2 PPG Industries

- 7.2.3 Siemens

- 7.2.4 BASF SE

- 7.2.5 Bauder Limited

- 7.2.6 Forbo International SA

- 7.2.7 Owens Corning SA

- 7.2.8 CEMEX

- 7.2.9 Alumasc Group PLC

- 7.2.10 Cold Mix Inc.*

- 7.3 Other Companies