|

市場調査レポート

商品コード

1632067

アジア太平洋の通関仲介- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Asia-Pacific Customs Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の通関仲介- 市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

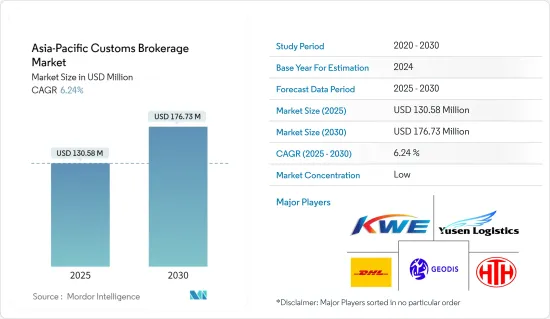

アジア太平洋の通関仲介市場規模は2025年に1億3,058万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.24%で、2030年には1億7,673万米ドルに達すると予測されます。

主要ハイライト

- 2024年現在、アジア太平洋の通関仲介市場は、主に国際貿易の急増と規制枠組みの適応によって力強い成長を遂げています。中国やインドなどの国々は、このクロスボーダー取引ブームの最前線にいます。

- 例えば、2024年9月、中国は3,040億米ドルの輸出と2,220億米ドルの輸入を報告し、817億米ドルの貿易収支を達成しました。前年比を見ると、2023年9月から2024年9月にかけて、中国の輸出は45億8,000万米ドル(1.53%)増加し、2,990億米ドルから3,040億米ドルに上昇しました。同時に輸入は7億300万米ドル(0.32%)増加し、2,210億米ドルから2,220億米ドルになりました。これらの数字は、シームレスな貿易業務と複雑な規制の遵守を確実にするために、熟練した通関仲介サービスの必要性が高まっていることを裏付けています。

- 進化する世界の力学に対応して、各国政府はセキュリティとコンプライアンスを強化するために税関施策を頻繁に改定しています。このような進化により、複雑な規制の地形を巧みに操る熟練した通関業者への需要が高まっている

- 例えば、2024年11月には、AEO(Authorized Economic Operator)プログラムが脚光を浴びた。この自主的なコンプライアンス・イニシアチブは、インド税関が貨物のセキュリティを強化できるようにするものです。これは、輸入業者、輸出業者、ロジスティクス・プロバイダー、ターミナル・オペレーター、通関業者、倉庫業者など、国際的なサプライチェーンの主要な参入企業との緊密な協力を通じて達成されます。企業がこのような厳しい規制基準に沿うよう努力する中、タイムリーでコンプライアンスに準拠した通関を確保する上で、通関業者の極めて重要な役割がますます明らかになっています。

- デジタルツールとプラットフォームを活用することで、通関業者は業務を最適化し、精度を高め、処理期間を短縮することができまします。の子会社で、世界エクスプレス輸送の大手であるフェデックスエクスプレスは2024年 5月9日、中国本土地で「フェデックス・オンライン輸入関税申告ツール」を発表しました。この技術的進歩は業務効率を高めるだけでなく、国際貿易に携わる企業のサプライチェーン管理を改善する上で通関業者が果たす重要な役割を明確にするものでもあります。

- さらに、中国税関総署(GAC)のレポートによると、2023年12月14日、中国とオーストラリアは、認定経済事業者(AEO)の資格を有する認定事業者を通じた商品取引の通関円滑化を開始しました。さらに、ベトナムの環太平洋パートナーシップ包括的と先進的協定(CPTPP)などの協定への参加は、ベトナムの輸出ポテンシャルを顕著に強化し、その後、通関仲介サービスに対する需要を高めています。

アジア太平洋の通関市場の動向

中国の貿易活動の急増が市場成長を後押し

2024年1~10月の中国の輸出入総額は36兆200億元(約5兆500億米ドル)で、前年同期比5.2%増となりました。これは中国の対外貿易総額の64.1%を占める。その内訳は、輸出が6.7%増の20兆8,000億元(2兆8,900億米ドル)、輸入が3.2%増の15兆2,200億元(2兆900億米ドル)です。同じ期間に、中国の加工貿易は6兆5,300億元(9,300億米ドル)に達し、4%の伸びを示し、貿易総額の18.1%を占めました。加工貿易の輸出は1.6%増の4兆1,300億元(5,800億米ドル)、輸入は8.3%増の2兆4,000億元(3,400億米ドル)となりました。

保税物流経由の貿易は5兆900億元(7,200億米ドル)に達し、2023年の前年比14%増という顕著な伸びを示しました。このセグメントの輸出は1兆9,600億元(2,800億米ドル)で11.5%増、輸入は3兆1,300億元(4,400億米ドル)で15.7%増でした。地域別では、ASEANが2024年の中国の主要貿易相手国としてトップに立ち、貿易総額は5兆6,700億元(8,100億米ドル)で、8.8%増となり、中国の対外貿易全体の15.7%を占めました。ASEANへの輸出は12.5%増の3兆3,600億元(4,800億米ドル)、ASEANからの輸入は3.8%増の2兆3,100億元(3,300億米ドル)でした。中国の対ASEAN貿易黒字は1兆500億元(1,500億米ドル)に拡大し、前年比38.2%の大幅な伸びを示しました。

結論として、この輸出入双方の増加傾向は、特に中国が近隣諸国との経済関係を深め、世界市場での地位を強化するにつれて、アジア太平洋の国際貿易動向における通関サービスの重要性が増していることを浮き彫りにしています。

市場の成長を牽引する海上貿易

海上貨物輸送は国際貨物輸送の主要な手段です。海上輸送は通関手続きでリードしているだけでなく、通関市場の収益を牽引しています。国連貿易開発会議(UNCTAD)の報告によると、2024年には世界の輸送能力の90%をアジアと欧州の企業が所有することになります。特筆すべきは、アジア企業が世界のトン数の半分以上を所有していることで、中国(3億1,000万重量トン)と日本(2億4,200万重量トン)がかなりの株式を保有しています。

新興諸国は世界商品貿易の約3分の2を占めています。2024年第1四半期の貿易成長は、中国(9%増)、インド(7%増)、米国(3%増)からの輸出に支えられました。2024年には、コンテナ貿易の約40%がアジアと欧州と米国を結ぶ主要な東西ルートを通過します。一方、南アジアと地中海のような本土以外の航路は、この貿易のおよそ12.9%を占めています。

アジアの造船活動は、2024年には混迷を極めた:中国は15.5%増、韓国は8.3%増となったが、日本は16.4%減となりました。このばらつきは、アジアの造船セクターの競合力学と海上物流への影響を浮き彫りにしています。さらに、アジア諸国、特に中国、ベトナム、韓国、日本は、世界貿易の流れをリードし続けており、コンテナ輸送量のほぼ半分を占めています。

結論として、海上貿易部門は通関市場に大きな影響を与え、アジアは世界の海運・貿易力学において極めて重要な役割を果たしています。造船や貿易ルートの開発が進むにつれ、国際貿易を促進する海上物流の重要性が浮き彫りになっています。

アジア太平洋の通関産業概要

アジア太平洋の通関市場は、多数の通関業者の存在によって細分化され、激しい競合が特徴となっています。差別化を図り競合優位性を確保するため、これらのブローカーの多くはブロックチェーンや統合サプライチェーンソリューションを含む先進技術に目を向けています。市場の主要企業には、Geodis Logistics、Kintetsu World Express、DHL Logistics、Yusen Logistics、HTH Logisticsなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場概要

- 市場促進要因

- 国際貿易の増加

- サプライチェーンの効率化とコスト削減

- 市場抑制要因

- 規制の変化

- 地政学的リスク

- 市場機会

- 越境eコマース

- デジタル変革

- サプライチェーン/バリューチェーン分析へ洞察

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- フォワーディング機能としての通関仲介概要

- 通関価格設定概要

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- 輸送モード別

- 海上輸送

- 航空輸送

- 国境を越えた陸上輸送

- 地域別

- 中国

- 日本

- インド

- オーストラリア

- マレーシア

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- DHL Group Logistics

- Geodis Logistics

- Kintetsu World Express

- HTH Corporation

- Yusen Logistics

- China International Freight Co.

- OEC Group

- Sino Shipping

- Kawasaki Rikuso Transportation Co.,Ltd.

- One Global Logistics*

- その他の企業

第7章 市場機会と今後の動向

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-製品別と仕向地・供給源別輸出入額

The Asia-Pacific Customs Brokerage Market size is estimated at USD 130.58 million in 2025, and is expected to reach USD 176.73 million by 2030, at a CAGR of 6.24% during the forecast period (2025-2030).

Key Highlights

- As of 2024, the Asia-Pacific customs brokerage market is witnessing robust growth, primarily fueled by a surge in international trade and the adaptation of regulatory frameworks. Countries such as China and India are at the forefront of this cross-border transaction boom.

- For example, in September 2024, China reported exports worth USD 304 billion and imports totaling USD 222 billion, achieving a commendable trade balance of USD 81.7 billion. A year-on-year comparison reveals that from September 2023 to September 2024, China's exports rose by USD 4.58 billion (1.53%), climbing from USD 299 billion to USD 304 billion. Simultaneously, imports saw a USD 703 million (0.32%) uptick, moving from USD 221 billion to USD 222 billion. These figures underscore the growing necessity for adept customs brokerage services to ensure seamless trade operations and adherence to intricate regulations.

- In response to evolving global dynamics, governments are frequently revising customs policies to bolster security and compliance. This evolution has heightened the demand for adept customs brokers, skilled at navigating these complex regulatory terrains.

- For instance, in November 2024, the Authorized Economic Operator (AEO) program was highlighted. This voluntary compliance initiative empowers Indian Customs to bolster cargo security. This is achieved through close collaboration with key players in the international supply chain, including importers, exporters, logistics providers, terminal operators, customs brokers, and warehouse operators. As businesses endeavor to align with these stringent regulatory benchmarks, the pivotal role of customs brokers in ensuring timely and compliant goods clearance becomes increasingly evident.

- Leveraging digital tools and platforms, customs brokers can optimize operations, enhance accuracy, and curtail processing durations. In a significant move, FedEx Express, a major player in global express transportation and a subsidiary of FedEx Corp., unveiled its FedEx Online Import Customs Declaration Tool in Mainland China on May 9, 2024. This technological advancement not only boosts operational efficiency but also underscores the vital role of customs brokers in refining supply chain management for businesses involved in global trade.

- Moreover, as of December 14, 2023, China and Australia commenced customs clearance facilitation for commodities trading through certified operators holding Authorized Economic Operator (AEO) status, as reported by China's General Administration of Customs (GAC). Furthermore, Vietnam's engagement in pacts like the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) has notably bolstered its export potential, subsequently heightening the demand for customs brokerage services.

Asia-Pacific Customs Brokerage Market Trends

Surge in Chinese Trade Activities Bolsters Market Growth

In the first ten months of 2024, China's imports and exports totaled 36.02 trillion yuan (around USD 5.05 trillion), marking a 5.2% year-on-year rise. This volume constituted 64.1% of China's total foreign trade value. Breaking it down, exports were valued at 20.8 trillion yuan (USD 2.89 trillion), up by 6.7%, while imports reached 15.22 trillion yuan (USD 2.09 trillion), seeing a 3.2% increase as reported by China Breifing. In the same timeframe, China's processing trade hit 6.53 trillion yuan (USD 0.93 trillion), growing at 4% and making up 18.1% of the total trade. Processing trade exports were 4.13 trillion yuan (USD 0.58 trillion), up 1.6%, and imports climbed to 2.4 trillion yuan (USD 0.34 trillion), marking a robust 8.3% rise as reported by General Administration of Customs - China.

Trade via bonded logistics reached 5.09 trillion yuan (USD 0.72 trillion), showcasing a notable 14% growth from the prior year 2023. This segment saw exports at 1.96 trillion yuan (USD 0.28 trillion), up 11.5%, and imports at 3.13 trillion yuan (USD 0.44 trillion), boasting a 15.7% increase as reported by China Customs. Regionally, ASEAN topped the list as China's primary trading partner in 2024, with trade totaling 5.67 trillion yuan (USD 0.81 trillion)-an 8.8% rise, making up 15.7% of China's overall foreign trade. Exports to ASEAN were 3.36 trillion yuan (USD 0.48 trillion), up 12.5%, while imports from the region stood at 2.31 trillion yuan (USD 0.33 trillion), a 3.8% increase. China's trade surplus with ASEAN grew to 1.05 trillion yuan (USD 0.15 trillion), marking a significant 38.2% jump from the previous year 2023 as reported by Trading Economics.

In conclusion, this rising trend in both imports and exports highlights the increasing importance of customs brokerage services in the Asia-Pacific's international trade landscape, especially as China deepens its economic relationships with its neighbors and bolsters its global market standing.

Maritime Trade Driving the Growth of the Market

Maritime freight transport stands as the dominant mode for international goods transit. Sea transport not only leads in customs entries but also drives the revenue of the customs brokerage market. The United Nations Conference on Trade and Development (UNCTAD) reports that 90% of the world's shipping capacity is owned by entities in Asia and Europe in 2024. Notably, Asian companies own over half of the global tonnage, with China (310 million dwt) and Japan (242 million dwt) holding substantial stakes.

Developing countries account for approximately two-thirds of global goods trade. In Q1 2024, trade growth was buoyed by exports from China (up 9%), India (up 7%), and the US (up 3%). In 2024, about 40% of containerized trade traversed the primary East-West routes linking Asia with Europe and the US. Meanwhile, non-mainland routes, like South Asia to the Mediterranean, captured roughly 12.9% of this trade.

Shipbuilding activities in Asia showcased a mixed bag in 2024: China boosted its shipbuilding capacity by 15.5%, South Korea followed with an 8.3% uptick, but Japan faced a notable decline of 16.4%. This variance underscores the competitive dynamics of Asia's shipbuilding sector and its implications for maritime logistics. Furthermore, Asian nations, particularly China, Vietnam, South Korea, and Japan, continue to lead in global trade flows, collectively representing nearly half of all container traffic.

In conclusion, the maritime trade sector significantly influences the customs brokerage market, with Asia playing a pivotal role in global shipping and trade dynamics. The ongoing developments in shipbuilding and trade routes underscore the importance of maritime logistics in facilitating international commerce.

Asia-Pacific Customs Brokerage Industry Overview

The Asia-Pacific customs brokerage market is characterized by fragmentation and intense competition, driven by the presence of numerous customs brokers. To differentiate themselves and secure a competitive advantage, many of these brokers are turning to advanced technologies, including blockchain and integrated supply chain solutions. The major players in the market include Geodis Logistics, Kintetsu World Express, DHL Logistics, Yusen Logistics, HTH Logistics, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising International Trade

- 4.2.2 Supply Chain Efficiency and Cost Reduction

- 4.3 Market Restraints

- 4.3.1 Regulatory Changes

- 4.3.2 Geopolitical Risks

- 4.4 Market Oppurtunities

- 4.4.1 Cross-Border E-Commerce

- 4.4.2 Digital Transformation

- 4.5 Insights into Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Brief on Customs Brokerage as a Freight Forwarding Function

- 4.8 Overview of Customs Pricing

- 4.9 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Mode Of Transport

- 5.1.1 Sea

- 5.1.2 Air

- 5.1.3 Cross-Border Land Transport

- 5.2 By Geography

- 5.2.1 China

- 5.2.2 Japan

- 5.2.3 India

- 5.2.4 Australia

- 5.2.5 Malaysia

- 5.2.6 South Korea

- 5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 DHL Group Logistics

- 6.2.2 Geodis Logistics

- 6.2.3 Kintetsu World Express

- 6.2.4 HTH Corporation

- 6.2.5 Yusen Logistics

- 6.2.6 China International Freight Co.

- 6.2.7 OEC Group

- 6.2.8 Sino Shipping

- 6.2.9 Kawasaki Rikuso Transportation Co.,Ltd.

- 6.2.10 One Global Logistics*

- 6.3 Other Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin