中国のプロジェクト物流:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Project Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1630268

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

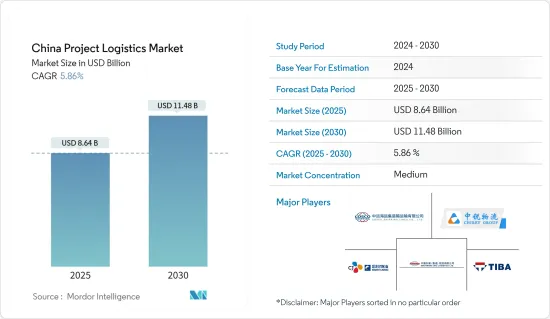

中国のプロジェクトロジスティクス市場規模は2025年に86億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.86%で、2030年には114億8,000万米ドルに達すると予測されます。

主要ハイライト

- 中国の一帯一路構想(BRI)は、国内のインフラ投資を強化するだけでなく、近隣地域にもその範囲を広げており、それによってプロジェクトロジスティクスの機会も拡大しています。中国が主導するBRIは、ユーラシア、ラテンアメリカ、アフリカにまたがる連結性、貿易、通信を強化することを主目的とした、記念碑的なインフラ投資の試みです。BRIの傘下から生まれた注目すべきプロジェクトには、ブリタニカが取り上げたように、中国・パキスタン経済回廊(CPEC)、中国・モンゴル・ロシア経済回廊、新ユーラシア陸橋などがあります。

- 建設やインフラプロジェクトが成長し続けるにつれ、鉄鋼や関連資材を輸送する効率的なロジスティクスサービスへの需要が高まっています。中国は毎年、その他を合わせたのと同量の鉄鋼を生産しています。2024年8月、中国工業情報化部(MIIT)は新たな製鉄生産プロジェクトを停止する通達を出しました。この動きは、MIITが鉄鋼セクターの過剰生産能力を抑制することを目的とした施策を見直したことによる。変動する生産水準と国内需要の減少を考えると、ロジスティクス・プロバイダーは戦略の適応を余儀なくされています。在庫を効果的に管理し、潜在的な混乱に対処しながらタイムリーな配送を確保しなければならないです。

- さらに、石油化学産業の拡大は、中国のプロジェクトロジスティクス、特に原料と完成品の輸送に大きな影響を与えます。i.C.I.S.が2024年7月に発表した報告書によると、中国の製油所能力は2027年から年間約10億トンで安定し、少なくとも2040年まではこの水準を維持すると予測されています。これは、2,000~2026年にかけて250%以上の能力急増が予測されていたことを考慮すると、大幅な転換を意味します。

- プロジェクト貨物輸送の制限が厳しくなるにつれ、関連するリスクもエスカレートしています。貨物量の制約だけでなく、特にDSU(Delay in Start-up)値の面で、財務的な影響も顕著になってきています。再加工、船積み料金、収入損失、その他の運営経費などの要因を考慮すると、貨物の破損や到着遅延が大幅な財務的後退につながることは明らかで、数十0万米ドルのDSU損失に達することも少なくありません。

中国のプロジェクトロジスティクス市場の動向

中国のインフラ投資が主要部門を強化

- 中国政府がインフラ開発を優先する中、これらの投資は建設、エネルギー、製造などのセクターにわたる大規模プロジェクトを強化する上で極めて重要な役割を果たしています。例えば、2024年3月にロードスターが報じたところによると、中国は今後1年間に1,730億米ドルを輸送プロジェクトに充てる予定で、これは2023年からおよそ35億米ドルの増加です。この大幅な支出は、中国の物流インフラ強化へのコミットメントを強調するものです。

- 注目すべき地域の動きとして、2024年7月、国家統計局(NBS)は、今年上半期の固定資産投資が前年同期比3.9%増加し、24兆5,300億人民元(3兆3,800億米ドル)に達したことを示すデータを発表しました。さらにNBSは、インフラ投資が5.4%増加したと報告しました。インフラ投資の主要セグメントである水利管理、航空、鉄道はすべて2桁成長を記録し、NBSの評価通り、景気拡大を後押しした、世界のタイムズ紙は報じました。

- 鉄道網の開発は、インフラ投資の市場牽引力をさらに例証しています。2024年3月の報道では、浦東国際空港を含む主要交通ハブとの接続性を強化することを目的とした、現在進行中の地域鉄道プロジェクトが取り上げられました。

- 結論として、中国の大幅なインフラ投資がプロジェクトロジスティクス市場を大きく牽引しています。こうした開発は、当分の間、市場の情勢を形成し続けると予想されます。

中国の原油生産が市場を押し上げる

- 原油消費量と生産量の両方で世界のヘビー級である中国は、その原油生産動向がロジスティクス戦略を形成していると見ています。例えば、PRS Newswireが報じたように、2024年1月、中国海洋石油総公司(CNOOC)は石油・ガスの生産量を5%増やし、石油換算で日量195万バレル(b/d)の生産を目指すという目標を設定しました。この増産は、今年2024年に開始される13の新規プロジェクトから予想されるもので、Suizhong 36-1やBozhong 19-2油田プロジェクトのような国内ベンチャーが目立つ。その結果、資源のタイムリーな供給と生産目標の達成を確実にするため、効率的なプロジェクトロジスティクスが重視されるようになります。

- さらに、2024年1月、Offshore Energyは、中国の原油生産量が2023年比で2%増加したと報告しました。この上昇は、中国が石油精製品の有力な輸出国であることを裏付けています。COSCO Shipping Logisticsのような企業は、特注のロジスティクスソリューションに磨きをかけ、石油部門におけるプロジェクト貨物の輸送という明確な課題に取り組んでいます。

- 結論として、中国の原油生産量の増加がプロジェクトロジスティクス市場の成長を牽引しています。効率的なロジスティクスソリューションに注力することは、生産目標を達成し、世界の石油産業における中国の主要企業としての地位を維持するために極めて重要です。

中国のプロジェクトロジスティクス産業概要

中国のプロジェクトロジスティクス市場は、多数の中小企業の存在によるセグメント化が主要特徴です。有名な企業には、Chirey Group、Sinotrans、COSCO Shipping Logisticsなどがあり、国内企業が市場を独占しています。国内からの重量貨物の需要と輸出の増加に対応するため、企業はネットワークを拡大する必要があります。

プロジェクト・クリティカルな設備は、貨物輸送戦略の策定、輸送トラックの配備、トラック、船舶、フローティング・クレーンの連携、時間管理など、非常に厳しい基準があります。このような機器は、より短い期間内に安全に納入されなければなりません。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 再生可能エネルギーの利用増加によるプロジェクトロジスティクス企業のビジネス機会拡大

- eコマースの成長

- 抑制要因

- コスト高

- 熟練労働者の不足

- 機会

- 一帯一路(the Belt and Road)イニシアティブは企業にとってより多くの機会を生み出すと考えられます。

- 再生可能エネルギープロジェクトの成長

- 促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 政府の規制と取り組み

- 競争企業間の敵対関係

- 技術動向

- 注目-一帯一路構想(BRI)と投資

- プロジェクト貨物輸送に伴うリスクの詳細

- バリューチェーン/サプライチェーン分析

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 輸送

- フォワーディング

- 倉庫業

- その他付加価値サービス

- エンドユーザー別

- 石油・ガス、石油化学

- 鉱業・採石業

- エネルギー・電力

- 建設

- 製造業

- その他のエンドユーザー(航空宇宙・防衛、自動車など)

第6章 競合情勢

- 市場集中概要

- 企業プロファイル

- COSCO Shipping Logistics Co., Ltd.

- Chirey Group

- Translink International Logistics Group

- Kerry Logistics Network Limited

- Trans Global Projects Group(TGP)

- Sinotrans(HK)Logistics Ltd.

- CJ Smart Cargo

- Tiba Group

- Mitsubishi Logistics Corporation

- InterMax Logistics Solution Limited

- Wangfoong Transportation Ltd.

- Global Star Logistics (China) Co., Ltd.

- Sunshine Int'l Logistics Co.,ltd.

- Kuehne+Nagel

- Agility Logistics Pvt. Ltd.*

- その他の企業

第7章 市場機会と今後の動向

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-製品別と仕向地・供給源別輸出入額

目次

The China Project Logistics Market size is estimated at USD 8.64 billion in 2025, and is expected to reach USD 11.48 billion by 2030, at a CAGR of 5.86% during the forecast period (2025-2030).

Key Highlights

- The Belt and Road Initiative (BRI) in China is not only bolstering domestic infrastructure investments but also extending its reach to neighboring regions, thereby amplifying opportunities in project logistics. Spearheaded by China, the BRI is a monumental infrastructure investment endeavor, with the primary goal of enhancing connectivity, trade, and communication spanning across Eurasia, Latin America, and Africa. Noteworthy projects birthed from the BRI umbrella encompass the China-Pakistan Economic Corridor (CPEC), the China-Mongolia-Russia Economic Corridor, and the New Eurasia Land Bridge, as highlighted by Britannica.

- As construction and infrastructure projects continue to grow, the demand for efficient logistics services to transport steel and related materials intensifies. Each year, China produces as much steel as the rest of the world combined. On August 2024, China's Ministry of Industry and Information Technology (MIIT) issued a notice suspending new steelmaking production projects. This move comes as MIIT reviews a policy aimed at controlling overcapacity in the steel sector. Given the fluctuating production levels and a decline in domestic demand, logistics providers are compelled to adapt their strategies. They must manage inventory effectively and ensure timely deliveries, all while navigating potential disruptions.

- Furthermore, the petrochemical industry's expansion significantly impacts project logistics in China, particularly in transporting raw materials and finished products. According to a report by I.C.I.S. in July 2024, China's refinery capacity is set to stabilize at approximately 1 billion tonnes annually from 2027 and is projected to maintain this level until at least 2040. This marks a substantial shift, considering the forecasted capacity surge of over 250% from 2000 to 2026.

- As the limits on project cargo movement tighten, the associated risks are escalating. Beyond just the constraints on cargo volume, the financial repercussions, especially in terms of Delay in Start-up (DSU) values, are becoming more pronounced. When considering factors such as re-fabrication, shipping charges, lost revenues, and other operational expenses, it's evident that a shipment arriving damaged or late can lead to substantial financial setbacks, often reaching multi-million dollar DSU losses.

China Project Logistics Market Trends

China's Infrastructure Investments Bolster Key Sectors

- As the Chinese government prioritizes infrastructure development, these investments play a pivotal role in bolstering large-scale projects across sectors like construction, energy, and manufacturing. For example, in March 2024, Loadster reported that China is set to allocate USD 173 billion for transport projects over the coming 12 months, marking an increase of roughly USD 3.5 billion from 2023. This significant outlay underscores China's commitment to enhancing its logistics infrastructure.

- In a notable regional move, in July 2024, the National Bureau of Statistics (NBS) released data indicating that fixed-asset investment in the first half of the year increased by 3.9 percent year-on-year, reaching CNY 24.53 trillion (USD 3.38 trillion). Additionally, NBS reported a 5.4 percent rise in infrastructure investment. Key areas of infrastructure investment, namely water conservancy management, aviation, and railways, all experienced double-digit growth, bolstering economic expansion, as per NBS's assessment, reported Global Times.

- Rail network developments further exemplify the market-driving power of infrastructure investments. In March 2024, reports highlighted ongoing regional rail projects aimed at enhancing connectivity with major transport hubs, including Pudong International Airport.

- In conclusion, China's substantial investments in infrastructure are significantly driving the project logistics market. These developments are expected to continue shaping the market landscape in the foreseeable future.

China's Crude Oil Production Boosts Market

- China, a global heavyweight in both crude oil consumption and production, sees its oil production trends shaping its logistics strategies. For example, in January 2024, China National Offshore Oil Corporation (CNOOC) set a goal to boost its oil and gas output by 5%, targeting a production rate of 1.95 million barrels per day (b/d) of oil equivalent, as reported by PRS Newswire. This uptick is anticipated from 13 new projects kicking off this year 2024, prominently featuring domestic ventures like the Suizhong 36-1 and Bozhong 19-2 oilfield projects. Consequently, there's a heightened emphasis on efficient project logistics to ensure timely resource delivery and meet production goals.

- Additionally, in January 2024, Offshore Energy reported a 2% rise in China's crude oil production compared to 2023. This uptick underscores China's stature as a prominent exporter of refined petroleum products. Companies such as COSCO Shipping Logistics are honing in on bespoke logistics solutions, tackling the distinct challenges of transporting project cargo within the oil sector.

- In conclusion, China's increasing crude oil production is driving the growth of its project logistics market. The focus on efficient logistics solutions is crucial for meeting production targets and maintaining China's position as a key player in the global oil industry.

China Project Logistics Industry Overview

China's project logistics market is characterized by fragmentation, largely due to the presence of numerous small and medium-sized enterprises. Some of the well-known businesses include Chirey Group, Sinotrans, and COSCO Shipping Logistics Co., Ltd. Domestic businesses dominate the market. To meet the rising demand and exports of heavy cargo from the nation, businesses must broaden their networks.

Project-critical equipment has highly strict criteria for the creation of a cargo transport strategy, the deployment of transport trucks, the coordination of trucks, ships, and floating cranes, as well as time management. This equipment must be delivered securely within shorter periods.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Usage of Renewable Energies Boosts Opportunities for Project Logistics Companies

- 4.2.1.2 Growth of E-commerce

- 4.2.2 Restraints

- 4.2.2.1 Cost - Intensive

- 4.2.2.2 Lack of Skilled Labor

- 4.2.3 Opportunities

- 4.2.3.1 Belt and Road Initiative will creates more opportunities for the companies

- 4.2.3.2 Growth in Renewable Energy Projects

- 4.2.1 Drivers

- 4.3 Industry Attractiveness- Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Government Regulations and Initiatives

- 4.4.1 Intensity of Competitive Rivalry

- 4.5 Technological Trends

- 4.6 Spotlight - Belt and Road Initiative (BRI) and Investments

- 4.7 Elaboration on risks involved in project cargo movement

- 4.8 Value Chain / Supply Chain Analysis

- 4.9 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.2 Forwarding

- 5.1.3 Warehousing

- 5.1.4 Other Value-added Services

- 5.2 By End-user

- 5.2.1 Oil and Gas, Petrochemical

- 5.2.2 Mining and Quarrying

- 5.2.3 Energy and Power

- 5.2.4 Construction

- 5.2.5 Manufacturing

- 5.2.6 Other End-Users (Aerospace & Defense, Automotive, etc.)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 COSCO Shipping Logistics Co., Ltd.

- 6.2.2 Chirey Group

- 6.2.3 Translink International Logistics Group

- 6.2.4 Kerry Logistics Network Limited

- 6.2.5 Trans Global Projects Group (TGP)

- 6.2.6 Sinotrans (HK) Logistics Ltd.

- 6.2.7 CJ Smart Cargo

- 6.2.8 Tiba Group

- 6.2.9 Mitsubishi Logistics Corporation

- 6.2.10 InterMax Logistics Solution Limited

- 6.2.11 Wangfoong Transportation Ltd.

- 6.2.12 Global Star Logistics (China) Co., Ltd.

- 6.2.13 Sunshine Int'l Logistics Co.,ltd.

- 6.2.14 Kuehne + Nagel

- 6.2.15 Agility Logistics Pvt. Ltd.*

- 6.3 Other companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日